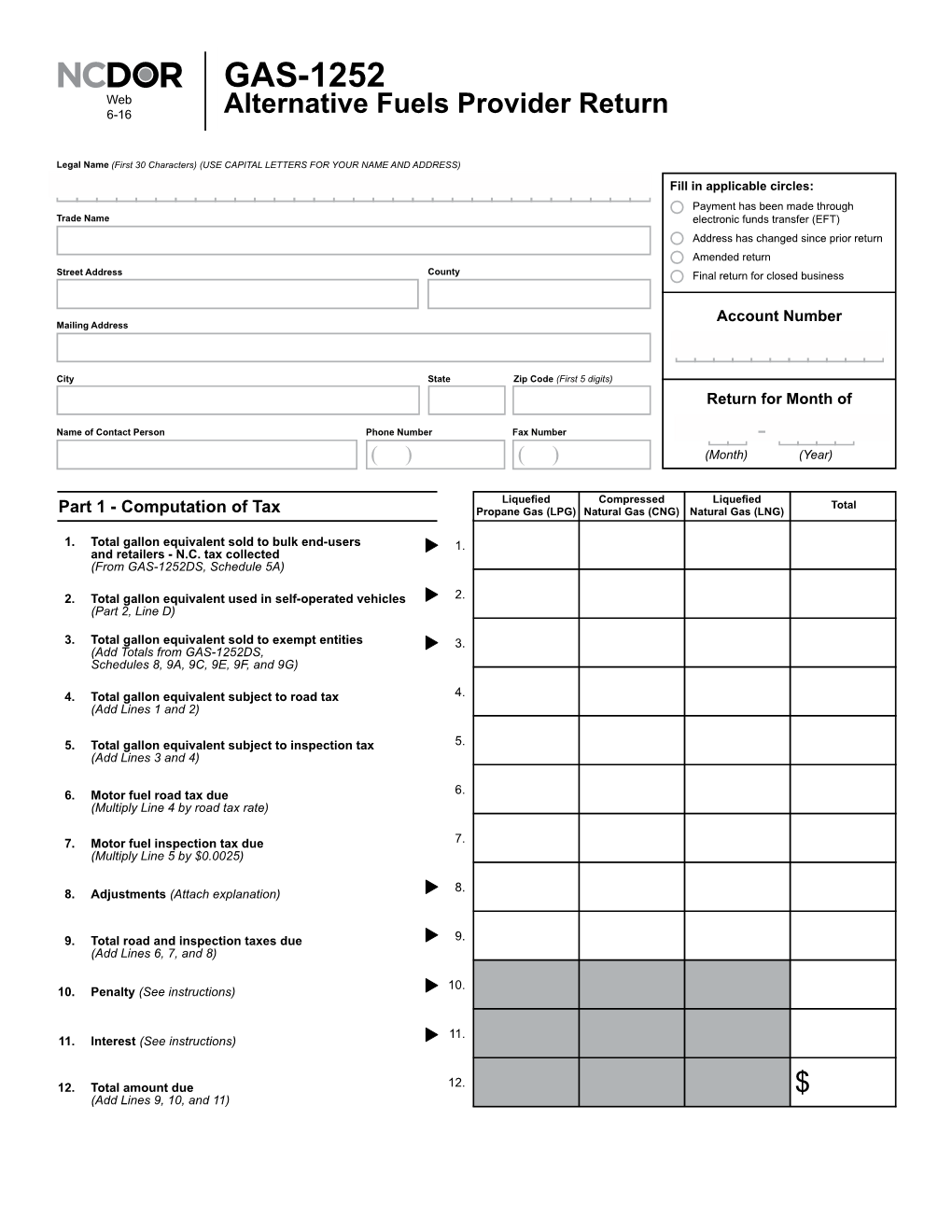

GAS-1252 Web 6-16 Alternative Fuels Provider Return

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Compressed Natural Gas Not Subject to Motor Fuel Tax

External Multistate Tax Alert External Multistate Tax Alert January 18, 2018 IL Appellate Court – compressed natural gas not subject to motor fuel tax Overview In a unanimous, unpublished order issued on December 29, 2017, the Illinois First District Appellate Court (“Appellate Court”) reversed an earlier Illinois Independent Tax Tribunal (“Tax Tribunal”) order which had granted summary judgment in favor of the Illinois Department of Revenue (“Department”).1 Ruling in favor of the taxpayer, the Appellate Court held that compressed natural gas (“CNG”) is not a taxable motor fuel under the Illinois Motor Fuel Tax Law Act (“Motor Fuel Tax”).2 The Appellate Court’s order is subject to discretionary review by the Illinois Supreme Court upon the Illinois Department of Revenue filing an appeal. This tax alert summarizes the factual background of the case, the Tax Tribunal’s and Appellate Court’s decisions, and provides taxpayer refund considerations. Background Illinois imposes a per gallon excise tax on “all motor fuel used in motor vehicles operating on [Illinois] public highways.”3 For purposes of the Motor Fuel Tax Law Act, “motor fuel” is defined as: [A]ll volatile and inflammable liquids produced, blended or compounded for the purpose of, or which are suitable or practicable for, operating motor vehicles. Among other things, “Motor Fuel” includes “Special Fuel” as defined in Section 1.13 of this Act.4 “Special fuel,” in turn, is defined as: [A]ll volatile and inflammable liquids capable of being used for the generation of power in an internal combustion engine except that it does not include gasoline as defined in Section 5, example (A), of this Act, or combustible gases as defined in Section 5, example (B), of this Act . -

Federal Tax Rates on Motor Fuels and Lubricating Oil 1

FEDERAL TAX RATES ON MOTOR FUELS AND LUBRICATING OIL 1/ APRIL 1997 (CENTS PER GALLON) TABLE FE-101A EFFECTIVE DATE OF GASOLINE GASOHOL DIESEL FUEL SPECIAL FUEL LUBRICATING OIL NEW TAX OR REVISION (CENTS PER (CENTS PER (CENTS PER (CENTS PER (CENTS PER OF EXISTING TAX GALLON) 2/ GALLON) GALLON) 3/ GALLON) 4/ GALLON) 5/ June 21, 1932 1¢ (6/) ß ß 4¢ June 17, 1933 1.5¢ ß ß ß ß January 1, 1934 1¢ ß ß ß ß July 1, 1940 1.5¢ ß ß ß 4.5¢ November 1, 1942 ß ß ß ß 6¢ November 1, 1951 2¢ ß 2¢ 2¢ ß September 1, 1955 ß ß ß ß Cutting oil, 3¢; other, 6¢ July 1, 1956 3¢ ß 3¢ 3¢ ß October 1, 1959 4¢ ß 4¢ 4¢ ß January 1, 1966 ß ß ß ß 6¢ 7/ November 10, 1978 4¢ 8/ ß 4¢ 8/ 4¢ 8/ 6¢ 8/ January 1, 1979 4¢ 8/ 9/ (6/) ß 4¢ 8/ 9/ 6¢ 8/ 9/ January 7, 1983 ß ß ß ß Repealed April 1, 1983 9¢ 8/ 10/ 4¢ 9¢ 8/ 10/ 4¢ 8/ 9/ ß August 1, 1984 ß ß 15¢ 8/ 10/ 11/ ß ß January 1, 1985 ß 3¢ ß ß ß January 1, 1987 9.1¢ 8/ 10/ 12/ 3.1¢ 12/ 15.1¢ 8/ 10/ 11/ 12/ ß ß December 1, 1990 14.1¢ 8/ 10/ 12/ 13/ 8.7 & 8.1¢ 12/ 13/ 14/ 20.1¢ 8/ 10/ 11/ 12/ 13/ 14¢ 4/ 8/ 13/ ß January 1, 1993 ß 8.7 & 8.1¢ 12/ 13/ 14/ ß ß ß October 1, 1993 16/ 18.4¢ 8/ 10/ 12/ 15/ 13 & 12.4¢ 12/ 14/ 15/ 24.4¢ 8/ 10/ 11/ 12/ 15/ 18.3¢ 4/ 8/ 15/ ß January 1, 1996 18.3¢ 8/ 10/ 15/ 12.9¢ 14/ 15/ 24.3¢ 8/ 10/ 15/ 18.3¢ 4/ 8/ 15/ ß Scheduled Termination Termination Termination Termination ß change under Oct. -

Washington State Fuel Tax Compliance Manual

Washington State Fuel Tax Compliance Manual Fuel Tax Compliance Manual Table of Contents Introduction ........................................................................................................................................... 3 Applicable Washington Laws and Rules .............................................................................................. 3 Contact Information............................................................................................................................... 3 Tax Structure ......................................................................................................................................... 4 Fuel Licenses and Registrations .......................................................................................................... 4 Filing Methods ....................................................................................................................................... 5 General Information............................................................................................................................... 6 Reporting Requirements ....................................................................................................................... 6 Amended Tax Returns ........................................................................................................................... 7 Records Retention ................................................................................................................................ -

Change to Motor Fuel Tax Reporting of Liquefied Natural Gas And

Illinois Department of Revenue FY 2017-21 June 2017 informational Bulletin Constance Beard, Director Change to Motor Fuel Tax Reporting of Liquefied Natural Gas and Changes to Units of Measurement for Sales of Liquefied Natural Gas, Propane, This bulletin is written to inform you of recent changes; it does not replace and Compressed Natural Gas Sold statutes, rules and regulations, or court decisions. for Use as Motor Fuel To: All licensed Motor Fuel Distributors, Motor Fuel Suppliers, and Alternative Fuel Reporters For information Beginning on July 1, 2017, the Motor Fuel Tax Law, 35 ILCS 505/1, et seq., Visit our website at: requires liquefied natural gas (LNG) to be reported using diesel gallon tax.illinois.gov equivalents (DGEs). Fuel distributors are required to sell LNG used as motor fuel in DGEs and to sell compressed natural gas (CNG) used as motor fuel in Call us at: gasoline gallon equivalents (GGEs). Sales of propane (LP) used as motor fuel 217 782-2291 shall be in either DGEs or actual measured gallon volumetric units, which are Call our TDD then converted to determine the DGEs that are subject to tax. (telecommunications device What is liquefied natural gas? for the deaf) at: The Motor Fuel Tax Law defines “liquefied natural gas” as methane or natural 1 800 544-5304 gas in the form of a cryogenic or refrigerated liquid for use as a motor fuel. What is a diesel gallon equivalent? The Motor Fuel Tax Law defines a “diesel gallon equivalent” as an amount of liquefied natural gas or propane that has the equivalent energy content of a gallon of diesel fuel and shall be defined as 6.06 pounds of liquefied natural gas or 6.41 pounds of propane. -

Motor Fuel Untaxed Products Return This Form Is Issued Under Authority of P.A

Michigan Department of Treasury 4334 (Rev. 11-20) Motor Fuel Untaxed Products Return This form is issued under authority of P.A. 403 of 2000, as amended. Filing is Mandatory. The purpose of this form is to report gallons and remit the applicable tax for production of untaxed motor fuel products. This form may also be used to report gallons and remit tax for motor fuel products purchased without the Michigan excise tax but later used in a taxable manner. This form must be filed by the 20th of the following month after production and/or use. PART 1: COMPANY INFORMATION Name and Mailing Address Report Period (MM/YYYY) Account No. (FEIN, SSN, TR or ME No.) Contact Person Name Telephone Number Fax Number E-Mail Address PART 2: TAX COMPUTATION A B C D Biodiesel Gasoline Ethanol Diesel (see instructions) 1. Total gallons produced for taxable purposes excluding tax-paid gallons of gasoline and diesel fuel (see instructions) ..................... 2. Total gallons acquired tax-free and sold or used for taxable purposes ......................................................................................... 3. Taxable Gallons. Add lines 1 and 2 ................................................ 4. Tax rate ........................................................................................... 0.263 0.263 0.263 0.263 5. Calculated Tax Due. Multiply line 3 by line 4 .................................. 6. Total Tax Due. Add line 5, columns A through D .............................................................................. 7. Penalty (5% of tax due per month to a maximum of 25%) .............................................................. 8. Interest (1% above prime rate set January 1 and July 1 of each year) ........................................... 9. Total Remittance. Add lines 6, 7 and 8 .......................................................................................... PART 3: CERTIFICATION Taxpayer Certification. I declare under penalty of perjury that the information in this Preparer Certification. -

Revenue Impact from Electric and Hybrid Vehicles

ISSUE BRIEF: EDITION 8 | MAY 2020 @invest_nc ncdot.gov/ncfirst COMMISSION FUTURE INVESTMENT RESOURCES FOR SUSTAINABLE TRANSPORTATION The NC FIRST Commission was created in March 2019 to evaluate North Carolina’s transportation investment needs. Their job is to advise the Secretary of Transportation of new or better ways to ensure that critical financial resources are available in the future. As part of this process, we’ll be looking for input from you, the people of North Carolina! This brief examines how increased sales of electric and hybrid vehicles will impact transportation revenues and explores revenue policy options. Revenue Impact from Electric and Hybrid Vehicles Overview Executive Order 80, issued by Governor Roy Cooper on Oct. 29, 2018, directs how North Carolina can address climate change. Among other goals, because North Carolina’s transportation sector contributed 32 precent of the state’s total greenhouse gas emissions in 2017,1 the order seeks to increase the number of zero emission vehicles (ZEVs) to at least 80,000 by 2025. As of March 17, North Carolina has more than 13,482 electric vehicles and 158,081 hybrids. While EV owners pay an additional $130 vehicle registration fee, hybrid owners do not pay an additional fee. Based on Division of Motor Vehicle data, hybrid and electric vehicle owners pay approximately $50 less in state transportation taxes per year than gasoline vehicle owners. This brief explores the fiscal impact of electric and hybrid vehicles, alternatives to a registration fee, and the policy arguments for and against taxation. 1 www.ncdot.gov/initiatives-policies/environmental/climate-change/ Documents/nc-zev-plan.pdf NC FIRST Commission 1 REVENUE IMPACT FROM ELECTRIC VEHICLES MAY 2020 How will EVs and hybrids change the Figure 2: North Carolina’s state’s vehicle fleet? Existing Vehicle Fleet With an average vehicle age of 12.7 years, it will take many years for EV and hybrid vehicles to create a significant change to the state’s vehicle fleet. -

G. Uniform Engine Fuels, Petroleum Products, and Automotive Lubricants Regulation

Handbook 130 - 2006 Engine Fuels, Petroleum Products, and Automotive Lubricants Regulation G. Uniform Engine Fuels, Petroleum Products, and Automotive Lubricants Regulation as adopted by The National Conference on Weights and Measures* 1. Background In 1984, the National Conference on Weights and Measures (NCWM) adopted a section 2.20. in the Uniform Regulation for the Method of Sale of Commodities requiring that motor fuels containing alcohol be labeled to disclose to the retail purchaser that the fuel contains alcohol. The delegates deemed this action necessary since motor vehicle manufacturers were qualifying their warranties with respect to some gasoline-alcohol blends, motor fuel users were complaining to weights and measures officials about fuel quality and vehicle performance, and American Society for Testing and Materials (ASTM) International had not yet finalized quality standards for oxygenated (which includes alcohol- containing) fuels. While a few officials argued weights and measures officials should not cross the line from quantity assurance programs to programs regulating quality, the delegates were persuaded that the issue needed immediate attention. A Motor Fuels Task Force was appointed in 1984 to develop mechanisms for achieving uniformity in the evaluation and regulation of motor fuels. The Task Force developed the Uniform Motor Fuel Inspection Law (see the Uniform Laws section of this Handbook) and the Uniform Motor Fuel Regulation to accompany the Law. The Uniform Law required registration and certification of motor fuel as meeting ASTM standards. The regulation defined the ASTM standards to be applied to motor fuel. In 1992 the NCWM established the Petroleum Subcommittee under the Laws and Regulations Committee. -

Department of Consumer Protection Motor Fuel Quality Testing

Regulations of Connecticut State Agencies TITLE 14. Motor Vehicles. Use of the Highway by Vehicles. Gasoline Agency Department of Consumer Protection Subject Motor Fuel Quality Testing Standards Inclusive Sections §§ 14-327d-1—14-327d-11 CONTENTS Sec. 14-327d-1. Definitions Sec. 14-327d-2. Standard specifications of motor fuel Sec. 14-327d-3. Quality of motor fuels Sec. 14-327d-4. Sale of gasoline Sec. 14-327d-5. Evidence of original purchase Sec. 14-327d-6. Labeling of dispensing devices Sec. 14-327d-7. Registration and branding Sec. 14-327d-8. Octane range number of commercial gasoline Sec. 14-327d-9. Cetane range of commercial diesel fuels Sec. 14-327d-10. Registration provisions Sec. 14-327d-11. Weights and measures sampling procedure for motor fuel octane and oxygenated levels Revised: 2015-3-6 R.C.S.A. §§ 14-327d-1—14-327d-11 - I- Regulations of Connecticut State Agencies TITLE 14. Motor Vehicles. Use of the Highway by Vehicles. Gasoline Department of Consumer Protection §14-327d-1 Motor Fuel Quality Testing Standards Sec. 14-327d-1. Definitions As used in section 14-327d-1 to section 14-327d-11, inclusive, of the Regulations of Connecticut State Agencies: (1) “ASTM” means the American Society for Testing and Materials International. ASTM is an international voluntary consensus standards organization formed for the development of standards on characteristics and performance of materials, products, systems, and services, and the promotion of related knowledge; (2) “Antiknock Index (AKI)” means the arithmetic average of the Research Octane Number (RON) and Motor Octane Number (MON): AKI = (RON+MON)/2. -

Article 36D. Alternative Fuel. § 105-449.130. Definitions. the Following Definitions Apply in This Article: (1) Alternative Fuel

Article 36D. Alternative Fuel. § 105-449.130. Definitions. The following definitions apply in this Article: (1) Alternative fuel. – A combustible gas or liquid that can be used to generate power to operate a highway vehicle and that is not subject to tax under Article 36C of this Chapter. (1a) Bulk end-user. – A person who maintains storage facilities for alternative fuel and uses part or all of the stored fuel to operate a highway vehicle. (1f) Diesel gallon equivalent of liquefied natural gas. – The energy equivalent of 6.06 pounds of liquefied natural gas. (1g) Gas gallon equivalent of compressed natural gas. – The energy equivalent of 5.66 pounds of compressed natural gas. (1h) Gas gallon equivalent of liquefied propane gas. – The energy equivalent of 5.75 pounds of liquefied propane gas. (2) Highway. – Defined in G.S. 105-449.60. (3) Highway vehicle. – Defined in G.S. 105-449.60. (4) Motor fuel. – Defined in G.S. 105-449.60. (5) Motor fuel rate. – Defined in G.S. 105-449.60. (6) Provider of alternative fuel. – A person who does one or more of the following: a. Acquires alternative fuel for sale or delivery to a bulk end-user or a retailer. b. Maintains storage facilities for alternative fuel, part or all of which the person uses or sells to someone other than a bulk end-user or a retailer to operate a highway vehicle. c. Sells alternative fuel and uses part of the fuel acquired for sale to operate a highway vehicle by means of a fuel supply line from the cargo tank of the vehicle to the engine of the vehicle. -

Methanol in a Two Stroke Outboard Low Output Engine

Recent Researches in Engineering Mechanics, Urban & Naval Transportation and Tourism Mixtures of Gasoline-ethanol and gasoline –methanol in a two stroke outboard low output engine. CHARALAMPOS ARAPATSAKOS, MARIANTHI MOSCHOU Department of Production and Management Engineering Democritus University of Thrace V. Sofias Street, 67100, Xanthi GREECE [email protected] Abstract: - This work deals with the examination of a two stroke outboard low output engine from the viewpoint of pollution and consumption, using as fuel gasoline-ethanol and gasoline-methanol mixtures. A series of laboratory instruments were used for the realisation of the experiments Key-Words: - Gasoline - ethanol, Gasoline –methanol, Gas emissions, Two stroke outboard engine 1 Introduction understanding of the use of these two alcohols we The possible increases of the price of crude oil, the must examine them separately. Fuel ethanol is an abrupt oil market changes, the finite of reserves, as alternative fuel that is produced from biologically well as the environmental pollution led to the renewable resources that it can also be used as an reevaluation of the importance of the rural and octane enhancer and as oxygenate. Ethanol (ethyl forestall factor as a renewable resources supplier. alcohol, grain alcohol, ETOH) is a clear, colorless Important quantities of ethanol are produced every liquid alcohol with characteristic odor and as year to be used as fuel [1]. Ethanol has a high octane alcohol is a group of chemical compounds whose number, which means it can be used as a fuel molecules contain a hydroxyl group, -OH, bonded additive, or as a substitute either as pure alcohol or to a carbon atom. -

Kerosene and Motor Fuels Quality Inspection Regulations

RULES OF TENNESSEE DEPARTMENT OF AGRICULTURE DIVISION OF MARKETS CHAPTER 0080-05-12 KEROSENE AND MOTOR FUELS QUALITY INSPECTION REGULATIONS TABLE OF CONTENTS 0080-05-12-.01 Definitions 0080-05-12-.06 Condemned Product 0080-05-12-.02 Standard Specifications 0080-05-12-.07 Repealed 0080-05-12-.03 Classification and Method of Sale 0080-05-12-.08 Test Methods, Reproducibility and 0080-05-12-.04 Water in Retail Tanks and Conformance to Specifications Dispenser Filters 0080-05-12-.09 Sampling of Petroleum Products 0080-05-12-.05 Retail Product Storage Identification 0080-05-12-.10 Disposition of Sample Retains 0080-05-12-.01 DEFINITIONS. (1) “ASTM” (Formerly The American Society for Testing and Materials) means ASTM International, the international voluntary consensus standards organization formed for the development of standards on characteristics and performance of materials, products, systems, and services and the promotion of related knowledge. (2) “Antiknock Index (AKI)” means the arithmetic average of the Research Octane Number (RON) and Motor octane number (MON): AKI = (RON+MON)/2. This value is called by a variety of names, in addition to antiknock index, including: Octane rating, Posted octane, (R+M)/2 octane. (3) “Automotive Fuel Rating” or “fuel rating” means the automotive fuel rating required under the amended Octane Certification and Posting Rule (or as amended, the Fuel Rating Rule), 16 CFR Part 306. Under this Rule, sellers of liquid automotive fuels, including alternative fuels, must determine, certify, and post an appropriate automotive fuel rating. The automotive fuel rating for gasoline and gasoline blending stock is the antiknock index (octane rating). -

State Liquid-Fuels Inspection Fees 1

STATE LIQUID-FUELS INSPECTION FEES 1/ BASED ON INFORMATION OBTAINED FROM STATE TABLE MF-110 AUTHORITIES AND ON THE LAWS OF THE STATES STATUS AS OF JANUARY 1, 1998 AMOUNT FOR INSPECTION OF PETROLEUM PRODUCTS STATE FEE 2/ PRODUCTS INSPECTED INSPECTION AND/OR COLLECTION AGENCY DISPOSITION OF REVENUE REMARKS (CENTS) UNIT (MOTOR FUEL AND OTHER) Alabama 2 Gallon Gasoline, diesel fuel Department of Agriculture and First $175,000 to Agriculture Kerosene, jet fuel, and lubricating oil also taxed, but at other rates Industries Fund each month; balance to Public Road and Bridge Fund and to counties and cities Alaska - - - - - - Arizona - - All State Inspector, Department of - - Weights and Measures Arkansas - - Aviation gasoline, distillate, State Division of Weights and - - kerosene, motor fuel Measures California - - Gasoline, lubricating oil, diesel Department of Food and Agriculture, Petroleum Products Enforcement - fuel, motor fuel, antifreeze, Division of Measurement Standards Program brake fluid, transmission fluid Colorado - - All fuel products State Inspector of Oils - - Connecticut - - - - - - Delaware - - Gasoline, distillate Department of Transportation, Motor - All expenses for testing are paid from Transportation Trust Fund. Fuel Tax Administration Dist. of Col. - - - - - - Florida 0.125 Gallon Gasoline, kerosene, fuel oil, Department of Agriculture General Inspection Fund All revenue used by Department of Agriculture. No fee diesel fuel, gasohol on diesel fuel. Georgia - - All, except liquefied petroleum gas Department of Agriculture, Oil - - Inspection Unit Hawaii - - - - - - Idaho - - - - - - Illinois - - - - - - Indiana .0008 Gallon Gasoline, kerosene, jet fuel Special Tax Division, General Fund - and number 1 fuel oil Department of Revenue Iowa 4/ - Sample Motor fuel, illuminating oil Inspection, Motor Fuel and General Revenue Fund Fee charged for analysis initiated by dealer.