Future Car Wars 18-19

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

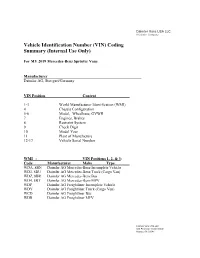

Vehicle Identification Number (VIN) Coding Summary (Internal Use Only)

Daimler Vans USA LLC A Daimler Company Vehicle Identification Number (VIN) Coding Summary (Internal Use Only) For MY 2019 Mercedes-Benz Sprinter Vans Manufacturer Daimler AG, Stuttgart/Germany VIN Position Content 1-3 World Manufacturer Identification (WMI) 4 Chassis Configuration 5-6 Model, Wheelbase, GVWR 7 Engines, Brakes 8 Restraint System 9 Check Digit 10 Model Year 11 Plant of Manufacture 12-17 Vehicle Serial Number WMI - VIN Positions 1, 2, & 3: Code Manufacturer Make Type WDA, 8BN Daimler AG Mercedes-Benz Incomplete Vehicle WD3, 8BU Daimler AG Mercedes-Benz Truck (Cargo Van) WDZ, 8BR Daimler AG Mercedes-Benz Bus WD4, 8BT Daimler AG Mercedes-Benz MPV WDP Daimler AG Freightliner Incomplete Vehicle WDY Daimler AG Freightliner Truck (Cargo Van) WCD Daimler AG Freightliner Bus WDR Daimler AG Freightliner MPV Daimler Vans USA LLC 303 Perimeter Center North Atlanta, GA 30346 Daimler Vans USA LLC A Daimler Company Chassis Configuration - VIN Position 4: Code Chassis Configuration / Intended Market P All 4x2 Vehicle Types / U.S. B All 4x2 Vehicle Types / Canada F All 4x4 Vehicle Types / U.S. C All 4x4 Vehicle Types / Canada Model, Wheelbase, GVWR - VIN Positions 5 & 6: Code Model Wheelbase GVWR E7 C1500/C2500/P1500 3665 mm/ 144 in. 8,000 lbs. to 9,000 lbs. Class G E8 C2500/P2500 4325 mm/ 170 in. 8,000 lbs. to 9,000 lbs. Class G F0 C2500/C3500 3665 mm/ 144 in. 9,000 lbs. to 10,000 lbs. Class H F1 C2500/C3500 4325 mm/ 170 in. 9,000 lbs. to 10,000 lbs. Class H F3 C4500/C3500 3665 mm/ 144 in. -

Daimler AG, Formerly Known As

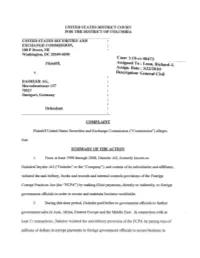

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA UNITED STATES SECURITIES AND EXCHANGE COMMISSION, 100 F Street,NE Washington, DC 20549-6030 Case: 1:10-cv-00473 Plaintiff, Ass~gned To : Leon, RichardJ-.- ASSIgn. Date: 3/22/2010 v. Description: General Civil DAIMLERAG, .Mercedesstrasse 137 70327 . Stuttgart, Germany Defendant. COMPLAINT PlaintiffUnited States Securities and Exchange Commission ("Commission") alleges that: SUMMARY OF THE ACTION 1. From at least 1998 through 2008, Daimler AG, formerly knoWn as DaimlerChrysler AG ("Daimler" or the "Company"), and certain ofits subsidiaries and affiliates, violated the anti-bribery, books and records and internal controls provisions ofthe Foreign _ Corrupt Practices Act (the "FCPA") by making illicit payments, directly or indirectly, to foreign government officials in order to secure and maintain business worldWide. 2. During this time period, Daimler paid bribes to government officials to further government sales in Asia, Africa, Eastern Europe and the Middle East. In connection With at least 51 transactions, Daimler violated the anti-bribery provision of the FCPA by paying tens of millions of dollars in corrupt payments to foreign government officials to secure business in · Russia,Chilia,Vietnam, Nigeria, Hungary, Latvia, Croatia and Bosnia. These corrupt payments were made through the use ofU.S. mails or the means or instrumentality ofU.S. interstate commerce. 3. Daimler also violated the FCPA's books and records and internal controls provisions in connection with the 51 transactions and at least an additional 154 transactions, in which it made improper payments totaling atleast $56 million to secure business in 22 countries, including, among others, Russia, China, Nigeria, Vietnam, Egypt, Greece, Hungary, North Korea, andIndonesia. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: JUNE 30, 2004 Check here if Amendment |_|; Amendment Number: This Amendment (Check only one.): |_| is a restatement. |_| adds new holdings entries. Institutional Investment Manager Filing this Report: Name: ALLSTATE LIFE INSURANCE COMPANY Address: 3075 SANDERS ROAD, SUITE G4A NORTHBROOK, IL. 60062-7127 Form 13F File Number: 28-01037 The institutional manager filing this report and the person by whom it is signed hereby represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: DOUG WELCH Title: ASSISTANT VICE PRESIDENT INVESTMENT OPERATIONS Phone: 847-402-2170 Signature, Place, and Date of Signing: /s/ Doug Welch NORTHBROOK, IL. 8/9/2004 --------------------------- -------------------- ---------------- [Signature] [City, State] [Date] Report Type (Check only one.): |X| 13F HOLDINGS REPORT. (Check here if all holdings of thius reporting manager are reported in this report.) |_| 13F NOTICE. (Check here if no holdings reported are in this report, and all hgoldings are reported by other reporting manager(s).).) |_| 13F COMBINATION REPORT. (Check here if a portion of the holdings for this reporting manager are reported in this report and a portion are reported by other reporting manager(s).) List of Other Managers Reporting for this Manager: FORM 13F SUMMARY PAGE Report Summary: Number of Other Included Managers: ONE Form 13F Information Table Entry Total: 210 Form 13F Information Table Value Total: 374,760 (THOUSAND) List of Other Included Managers: Provide a numbered list of the name(s) and Form 13F file number(s) of all institutional investment managers with respect to which this report is filed, other than the manager filing this report. -

United States Court of Appeals for the Federal Circuit

Case: 15-1914 Document: 48 Page: 1 Filed: 12/21/2015 2015-1914, -1919 United States Court of Appeals for the Federal Circuit ALTERA CORPORATION, XILINX, INC., Plaintiffs-Appellants, v. PAPST LICENSING GMBH & CO. KG, Defendant-Appellee. Appeals from the United States District Court for the Northern District of California in Case Nos. 5:14-cv-04794-LHK and 5:14-cv-04963-LHK, Judge Lucy H. Koh BRIEF FOR AMICI CURIAE AO KASPERSKY LAB, LIMELIGHT NETWORKS, INC., QVC, INC., SAS INSTITUTE INC., SYMMETRY LLC, AND VIZIO, INC. IN SUPPORT OF PLAINTIFF-APPELLANT XILINX, INC. STEVEN D. MOORE DARIUS SAMEROTTE KILPATRICK TOWNSEND & STOCKTON LLP Eighth Floor, Two Embarcadero Center San Francisco, CA 94111 Telephone: 415 576 0200 Attorneys for AMICI CURIAE DECEMBER 21, 2015 COUNSEL PRESS, LLC (888) 277-3259 Case: 15-1914 Document: 48 Page: 2 Filed: 12/21/2015 CERTIFICATE OF INTEREST Counsel for amici certifies the following: 1. The full name of every party or amicus represented by me is: AO Kaspersky Lab, Limelight Networks, Inc., QVC, Inc., SAS Institute Inc., Symmetry LLC, and VIZIO, Inc. 2. The name of the real party in interest represented by us is: N/A 3. All parent corporations and any public companies that own 10 percent or more of the stock of the parties represented by me are: AO Kaspersky Lab is a wholly owned subsidiary of Kaspersky Lab Ltd. Investment entities affiliated with Goldman, Sachs & Co. own over 10 percent of Limelight Networks, Inc. QVC is a wholly owned subsidiary of Liberty Interactive Corporation. SAS Institute Inc. and Symmetry LLC have no parent corporations, and there are no public companies that own 10% or more of them. -

2021 RAM 1500 Special Service Vehicle Upfit Guide SAFETY NOTICE

2019 – 2021 RAM 1500 Special Service Vehicle Upfit Guide SAFETY NOTICE This publication’s purpose is to provide technical training information to individuals in the automotive trade. All test and repair procedures must be performed in accordance with manufacturer’s service and diagnostic manuals. All warnings, cautions, and notes must be observed for safety reasons. The following is a list of general guidelines: . Proper service and repair is critical to the safe, reliable operation of all motor vehicles. The information in this publication has been developed for service personnel, and can help when diagnosing and performing vehicle repairs. Some service procedures require the use of special tools. These special tools must be used as recommended throughout this Technical Training Publication, the diagnostic manual, and the service manual. Special attention should be exercised when working with spring- or tension-loaded fasteners and devices such as E-Clips, circlips, snap rings, etc. Careless removal may cause personal injury. Always wear safety goggles when working on vehicles or vehicle components. Improper service methods may damage the vehicle or render it unsafe. Observe all warnings to avoid the risk of personal injury. Observe all cautions to avoid damage to equipment and vehicles. Notes are intended to add clarity and should help make your job easier. Cautions and warnings cover only the situations and procedures Stellantis has encountered and recommended. Neither Stellantis nor its subsidiaries or affiliates can know, evaluate, and advise the service trade of all conceivable ways in which service may be performed, or of the possible hazards for each. Consequently, Stellantis and its subsidiaries and affiliates have not undertaken any such broad service review. -

Hvy Dty Veh & Eng Res. Guide

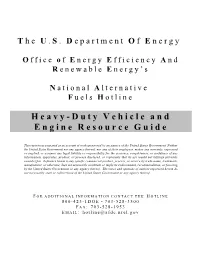

The U.S. Department Of Energy Office of Energy Efficiency And Renewable Energy’s National Alternative Fuels Hotline Heavy-Duty Vehicle and Engine Resource Guide This report was prepared as an account of work sponsored by an agency of the United States Government. Neither the United States Government nor any agency thereof, nor any of their employees, makes any warranty, expressed or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights. Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise, does not necessarily constitute or imply its endorsement, recommendation, or favoring by the United States Government or any agency thereof. The views and opinions of authors expressed herein do not necessarily state or reflect those of the United States Government or any agency thereof. FOR ADDITIONAL INFORMATION CONTACT THE HOTLINE 800-423-1DOE • 703-528-3500 FAX: 703-528-1953 EMAIL: [email protected] Introduction Engine manufacturers are moving forward when it comes to alternative fuel engine technology. This model year (MY96), heavy-duty engine manufacturers are offering a number of natural gas models with additional models nearing production. Electric vehicle manufacturers have several products available with new models nearing completion. Although Caterpillar is the only manufacturer offering propane as a fuel option, Detroit Diesel Corp. (DDC) will be demonstrating a prototype model in 1996, and Cummins will release a model within MY96. Many manufacturers are offering natural gas engines in response to California Air Resource Board’s strict bus emission standards which are effective MY96. -

Navistar and Ford Motor Company Reach New Business Agreement

Navistar and Ford Motor Company Reach New Business Agreement Companies to Continue To Collaborate on Medium Duty Trucks and Other Initiatives DEARBORN, Mich. & WARRENVILLE, Ill., Jan 13, 2009 (BUSINESS WIRE) -- Ford Motor Company (NYSE: F) and Navistar International Corporation (NYSE: NAV) have reached an agreement to restructure their ongoing business relationship and settle all existing litigation between the companies. As a result of the agreement, the companies will end their current diesel engine supply agreement effective Dec. 31, 2009. However, the companies will continue to collaborate on a range of initiatives, including their existing Blue Diamond Truck and Parts joint ventures. Navistar will acquire additional equity in the Blue Diamond joint ventures, which will continue to offer dealers and customers F-650 and F-750 medium duty trucks, as well as parts support for a variety of Ford products, including Ford's PowerStroke Diesel-equipped trucks. Ford and Navistar also will continue their diesel engine supply relationship in South America. As a result of the agreement, Ford will make a payment to Navistar. "Navistar and Ford benefitted from a successful partnership that provided value to both companies for nearly three decades. However, it's in our best interests to resolve our conflict and continue our relationship with each other in other areas," said Dan Ustian, Navistar chairman, president and chief executive officer. "The next phase of our relationship is consistent with Navistar's strategy to diversify our customer base, while continuing to provide value to both companies through our existing joint ventures and our supply agreement in South America." "We are pleased to have reached an agreement with Navistar that we believe is in the best interest of both companies," said Mark Fields, Ford's president of The Americas. -

Ram Truck Donation to Forgotten Harvest

Contact: Kevin Frazier Forgotten Harvest Receives Record-Breaking Farm Equipment Donation from Ram Truck, Case IH and New Holland Agriculture Nearly $400,000 in Equipment for Forgotten Harvest Farms October 8, 2013, Oak Park, Mich. - Forgotten Harvest, Metro Detroit’s only food rescue organization, will be able to provide millions of meals to people who would otherwise go hungry in Southeastern Michigan thanks to major equipment donations announced today by Ram Truck brand, Case IH and New Holland Agriculture. The donated equipment, worth nearly $400,000, will enable the expansion of large-scale farming operations through Forgotten Harvest Farms, where healthy fruits and vegetables are harvested by volunteers and delivered fresh and free of charge to agencies fighting hunger in the region. “In three years of harvesting fresh food from farms ourselves, we’ve gone from 100,000 pounds of food to 440,000 pounds to an estimated 850,000 pounds this year,” said Forgotten Harvest President & CEO Susan Goodell. “One of our greatest barriers to further growth was the lack of equipment to support our staff and volunteers – and today, Ram Truck, Case IH and New Holland have delivered what we need to keep growing our farming operations to feed hungry families in need.” More photos available at: https://www.facebook.com/forgottenharvest#!/forgottenharvest/photos_stream Forgotten Harvest currently has 75 acres of land under cultivation thanks to a lease donation by Forgotten Harvest board member and long-time supporter Nora Moroun, in memory of her grandmother Nora Langan. Today’s equipment donation will allow Forgotten Harvest to expand its operations at Ore Creek Farm. -

Chicago's Largest Publicly Traded Companies | Crain's Book of Lists

Chicago’s Largest Publicly Traded Companies | Crain’s Book of Lists 2018 Company Website Location Walgreens Boots Alliance Inc. www.walgreensbootsalliance.com Deerfield, IL Boeing Co. www.boeing.com Chicago, IL Archer Daniels Midland Co. www.adm.com Chicago, IL Caterpillar Inc. www.caterpillar.com Peoria, IL United Continental Holdings Inc. www.unitedcontinental-holdings.com Chicago, IL Allstate Corp. www.allstate.com Northbrook, IL Exelon Corp. www.exeloncorp.com Chicago, IL Deere & Co. www.deere.com Moline, IL Kraft Heinz Co. www.kraftheinz-company.com Chicago, IL Mondelez International Inc. www.mondelez-international.com Deerfield, IL Abbvie Inc. www.abbvie.com North Chicago, IL McDonald’s Corp. www.aboutmcdonalds.com Oak Brook, IL US Foods Holding Corp. www.USfoods.com Rosemont, IL Sears Holdings Corp. www.searsholdings.com Hoffman Estates, IL Abbott Laboratories www.abbott.com North Chicago, IL CDW Corp. www.cdw.com Lincolnshire, IL Illinois Tool Works Inc. www.itw.com Glenview, IL Conagra Brands Inc. www.conagrabrands.com Chicago, IL Discover Financial Services Inc. www.discover.com Riverwoods, IL Baxter International Inc. www.baxter.com Deerfield, IL W.W. Grainger Inc. www.grainger.com Lake Forest, IL CNA Financial Corp. www.cna.com Chicago, IL Tenneco Inc. www.tenneco.com Lake Forest, IL LKQ Corp. www.lkqcorp.com Chicago, IL Navistar International Corp. www.navistar.com Lisle, IL Univar Inc. www.univar.com Downers Grove, IL Anixter International Inc. www.anixter.com Glenview, IL R.R. Donnelly & Sons Co. www.rrdonnelly.com Chicago, IL Jones Lang LaSalle Inc. www.jll.com Chicago, IL Dover Corp. www.dovercorporation.com Downers Grove, IL Treehouse Foods Inc. -

Administrative Proceeding: Navistar International Corporation, Daniel C

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES ACT OF 1933 Release No. 9132 / August 5, 2010 SECURITIES EXCHANGE ACT OF 1934 Release No. 62653 / August 5, 2010 ACCOUNTING AND AUDITING ENFORCEMENT Release No. 3165 / August 5, 2010 ADMINISTRATIVE PROCEEDING File No. 3-13994 In the Matter of NAVISTAR INTERNATIONAL ORDER INSTITUTING CEASE-AND- CORPORATION, DESIST PROCEEDINGS PURSUANT DANIEL C. USTIAN, TO SECTION 8A OF THE SECURITIES ROBERT C. LANNERT, ACT OF 1933 AND SECTION 21C OF THE THOMAS M. AKERS, JR., SECURITIES EXCHANGE ACT OF JAMES W. MCINTOSH, 1934, MAKING FINDINGS, AND IMPOSING JAMES J. STANAWAY, A CEASE-AND-DESIST ORDER ERNEST A. STINSA, MICHAEL J. SCHULTZ, Respondents. I. The Securities and Exchange Commission (“Commission”) deems it appropriate that cease- and-desist proceedings be, and hereby are, instituted against Navistar International Corporation (“Navistar” or the “Company”), Daniel C. Ustian, Robert C. Lannert, Thomas M. Akers, Jr., James W. McIntosh, James J. Stanaway, Ernest A. Stinsa, and Michael J. Schultz (collectively “Respondents”) pursuant to Section 8A of the Securities Act of 1933 (“Securities Act”) and Section 21C of the Securities Exchange Act of 1934 (“Exchange Act”). II. In anticipation of the institution of these proceedings, Respondents have each submitted Offers of Settlement (the “Offers”), which the Commission has determined to accept. Solely for the purpose of these proceedings and any other proceedings brought by or on behalf of the Commission, or to which the Commission is a party, and without admitting or denying the findings or conclusions contained herein, except as to the Commission’s jurisdiction over Respondents and the subject matter of these proceedings, which are admitted, Respondents consent to the entry of this Order Instituting Cease-and-Desist Proceedings Pursuant to Section 8A of the Securities Act of 1933 and Section 21C of the Securities Exchange Act of 1934, Making Findings, and Imposing a Cease-and-Desist Order (“Order”), as set forth below. -

European Commission

C 268/18 EN Offi cial Jour nal of the European Union 14.8.2020 PROCEDURES RELATING TO THE IMPLEMENTATION OF COMPETITION POLICY EUROPEAN COMMISSION Prior notification of a concentration (Case M.9572 – BMW/Daimler/Ford/Porsche/Hyundai/Kia/IONITY) Candidate case for simplified procedure (Text with EEA relevance) (2020/C 268/06) 1. On 7 August 2020, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 (1). This notification concerns the following undertakings: — BMW AG (‘BMW’, Germany), — Daimler AG (‘Daimler’, Germany), — Ford Motor Company (‘Ford’, USA), — Dr Ing. h.c. F. Porsche Aktiengesellschaft (‘Porsche’, Germany). Porsche is part of the Volkswagen Group, — Hyundai Motor Company (‘Hyundai’, South Korea), which indirectly controls Kia Motor Corporation (‘Kia’, South Korea). Hyundai and Kia (together ‘Hyundai’) both belong to the Hyundai Motor Group (South Korea). BMW, Daimler, Ford, Porsche and Hyundai acquire within the meaning of Article 3(1)(b) and Article 3(4) of the Merger Regulation joint control of the whole of IONITY Holding GmbH & Co. KG (‘IONITY’, Germany), a full function joint venture established in 2017 by BMW, Daimler, Ford and Porsche. The concentration is accomplished by way of purchase of shares. 2. The business activities of the undertakings concerned are: — for BMW: is globally active in the development, production and marketing of passenger cars and motorbikes. BMW and its affiliates also provide financial services for private and business customers,