Joint Local Plan Issues Consultation City, Town and Other Centres

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

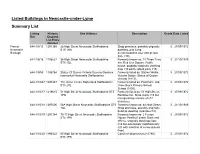

Listed Buildings in Newcastle-Under-Lyme Summary List

Listed Buildings in Newcastle-under-Lyme Summary List Listing Historic Site Address Description Grade Date Listed Ref. England List Entry Number Former 644-1/8/15 1291369 28 High Street Newcastle Staffordshire Shop premises, possibly originally II 27/09/1972 Newcastle ST5 1RA dwelling, with living Borough accommodation over and at rear (late c18). 644-1/8/16 1196521 36 High Street Newcastle Staffordshire Formerly known as: 14 Three Tuns II 21/10/1949 ST5 1QL Inn, Red Lion Square. Public house, probably originally dwelling (late c16 partly rebuilt early c19). 644-1/9/55 1196764 Statue Of Queen Victoria Queens Gardens Formerly listed as: Station Walks, II 27/09/1972 Ironmarket Newcastle Staffordshire Victoria Statue. Statue of Queen Victoria (1913). 644-1/10/47 1297487 The Orme Centre Higherland Staffordshire Formerly listed as: Pool Dam, Old II 27/09/1972 ST5 2TE Orme Boy's Primary School. School (1850). 644-1/10/17 1219615 51 High Street Newcastle Staffordshire ST5 Formerly listed as: 51 High Street, II 27/09/1972 1PN Rainbow Inn. Shop (early c19 but incorporating remains of c17 structure). 644-1/10/18 1297606 56A High Street Newcastle Staffordshire ST5 Formerly known as: 44 High Street. II 21/10/1949 1QL Shop premises, possibly originally build as dwelling (mid-late c18). 644-1/10/19 1291384 75-77 High Street Newcastle Staffordshire Formerly known as: 2 Fenton II 27/09/1972 ST5 1PN House, Penkhull street. Bank and offices, originally dwellings (late c18 but extensively modified early c20 with insertion of a new ground floor). 644-1/10/20 1196522 85 High Street Newcastle Staffordshire Commercial premises (c1790). -

Parish Bulletin 31.05.20.Pub

THE CATHOLIC PASTORAL PARTNERSHIP OF BIDDULPH, GOLDENHILL, KIDSGROVE & PACKMOOR UNDER THE PATRONAGE AND PROTECTION OF OUR LADY OF GRACE SUNDAY BULLETIN PENTECOST SUNDAY SUNDAY 31ST MAY 2020 CHURCHES A WORD FROM THE PARISH PRIEST Biddulph English Martyrs’ Church, Church Road, Biddulph, tion of how we will come guidance is at the moment) ST8 6NE out of the lockdown clo- not be over 70 years old, Goldenhill St Joseph’s Church, sure of churches. It is likely nor have underlying health High Street, Stoke-on-Trent, ST6 to take place in July. The conditions. This is because 5RD first stage will be that we, under the law, have a Kidsgrove St John the Evange- churches will be open for duty of care to volunteers list’s Church, The Avenue, personal prayer, before to safeguard their health Kidsgrove, ST7 1AE being opened again for and safety as far as possi- Packmoor St Patrick’s Church, public celebration of Mass. ble. We have the next Mellor Street, Packmoor, Stoke- The Vicar General has indi- month to get everything in on-Trent, ST7 4SN I wish you a blessed Feast cated that only churches place so that we are ready of Pentecost! Some of you that can guarantee the re- to re-open when the word KEY CONTACTS have been following the quired social distancing comes from the hierarchy Parish Priest nine days of the Pentecost will be able to open. As I that we are able. Rev Fr Julian C Green Novena with me online. I said last week, in our part- Assistant Priest Opening the churches hope that it was a blessed nership, when we open, it Rev Fr Prabhakar Pamisetty MF physically is as nothing time for you, and that the will be St Joseph’s and St Joseph’s Presbytery compared to opening up consecration to the Holy English Martyrs’ which 715 High Street the life of the Church Spirit that we make today will be the first to open. -

Staffordshire 30Undar Es W Th Cheshire Derbyshire Wa Rw Ckshiir and Refg Rid an D Worcester Local

No. 5H2 Review of Non-Metropolitan Counties. COUNTY OF STAFFORDSHIRE 30UNDAR ES W TH CHESHIRE DERBYSHIRE WA RW CKSHIIR AND REFG RID AN D WORCESTER LOCAL BOUNDARY COMMISSION FOH ENGLAND RETORT NO •5112 LOCAL GOVERNMENT BOUNDARY COMMISSION FOR ENGLAND CHAIRMAN Mr G J Ellerton CMC MBE DEPUTY CHAIRMAN Mr J G Powell CBE FRICS FSVA Members Mr K F J Ennals CB Mr G R Prentice Mrs H R V Sarkany PATTEN.PPD THE RT. HON. CHRIS PATTEN HP SECRETARY OF STATE FOR THE ENVIRONMENT REVIEW OF NON-METROPOLITAN COUNTIES COUNTY OF STAFFORDSHIRE: BOUNDARIES WITH CHESHIRE, DERBYSHIRE,. WARWICKSHIRE, AND HEREFORD AND WORCESTER COMMISSION'S FINAL REPORT AND PROPOSALS INTRODUCTION 1. On 26 July 1985 we wrote to Staffordshire County Council announcing our intention to undertake a review of the County under Section 48(1) of the Local Government Act 1972. Copies of our letter were sent to all the principal local authorities and parishes in Staffordshire, and in the adjoining counties of Cheshire, Derbyshire, West Midlands, Shropshire, Warwickshire, Hereford and Worcester and Leicestershire; to the National and County Associations of Local Councils; to the Members of Parliament with constituency interests and to the headquarters of the main political parties. In addition copies were sent to those government departments with an interest; regional health authorities; public utilities in the area; the English Tourist Board; the editors of the Municipal Journal and Local Government Chronicle; and to local television and radio stations serving the area. 2. The County Councils were requested to co-operate as necessary with each other, and with the District Councils concerned, to assist us in publicising the start of the review, by inserting a notice for two successive weeks in local newspapers so as to give a wide coverage in the areas concerned. -

Kidsgrove Town Investment Plan

Classification: NULBC UNCLASSIFIED Kidsgrove Town Investment Plan Newcastle-under-Lyme Borough Council October 2020 Classification: NULBC UNCLASSIFIED Classification: NULBC UNCLASSIFIED Kidsgrove Town Investment Plan Classification: NULBC UNCLASSIFIED Prepared for: Newcastle-under-Lyme Borough Council AECOM Classification: NULBC UNCLASSIFIED Kidsgrove Town Investment Plan Table of Contents 1. Foreword ......................................................................................................... 5 2. Executive Summary ......................................................................................... 6 3. Contextual analysis ......................................................................................... 9 Kidsgrove Town Deal Investment Area ............................................................................................................. 10 Kidsgrove’s assets and strengths .................................................................................................................... 11 Challenges facing the town ............................................................................................................................. 15 Key opportunities for the town ......................................................................................................................... 19 4. Strategy ......................................................................................................... 24 Vision ............................................................................................................................................................ -

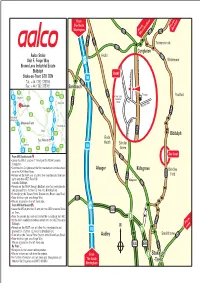

Stoke-On-Trent ST8 7DN A

From The North From Warrington Buxton A54 From A54 MacclesfieldA34 A50 Timbersbrook A5022 A534 Congleton Aalco Stoke Arclid A527 J17 T Whitemoor Unit F, Forge Way u n s Brown Lees Industrial Estate t al A34 Biddulph l R Inset y o a Stoke-on-Trent ST8 7DN a W M6 d A533 e Brown Le g Tel: +44 1782 375700 r o Fax: +44 1782 375701 Sandbach F A50 A34 A60 e Texaco Brown Lees s Poolfold M6 Congleton A614 A53 M1 Industrial R Estate oad J17 A6 Mansfield ay A534 ria W Biddulph Victo J28 A533 A38 J16 A52 A527 Newcastle- Under-Lyme J26 ay W J15 Stoke-on-Trent t c Nottingham e p A53 A50 J25 s Derby o r A527 A453 P Biddulph A34 J24 Rode East Midlands A34 Heath Scholar Stafford A46 M6 A38 Green M6 A51 A42 M1 A6 See Inset From M6 Southbound A50 Leave the M6 at junction 17 and join the A534 towards Congleton. A533 Continue into Congleton at the first roundabout continue ahead Alsager Kidsgrove Brindley onto the A34 West Road. Remain on the A34 over a further two roundabouts then turn Ford A527 right onto the A527 Rood Hill. A34 Kidsgrove A50 towards Biddulph. Remain on the A534 through Biddulph over four roundabouts and proceed for a further 1/2 mile into Brindley Ford. Turn right at the Texaco Petrol Station onto Brown Lees Road. Take the first right onto Forge Way. A500 We are situated on the left hand side. From M6 Northbound J16 Leave the M6 at junction 16 and join the A500 towards Stoke A500 on Trent. -

Submission to the Local Boundary Commission for England Further Electoral Review of Staffordshire Stage 1 Consultation

Submission to the Local Boundary Commission for England Further Electoral Review of Staffordshire Stage 1 Consultation Proposals for a new pattern of divisions Produced by Peter McKenzie, Richard Cressey and Mark Sproston Contents 1 Introduction ...............................................................................................................1 2 Approach to Developing Proposals.........................................................................1 3 Summary of Proposals .............................................................................................2 4 Cannock Chase District Council Area .....................................................................4 5 East Staffordshire Borough Council area ...............................................................9 6 Lichfield District Council Area ...............................................................................14 7 Newcastle-under-Lyme Borough Council Area ....................................................18 8 South Staffordshire District Council Area.............................................................25 9 Stafford Borough Council Area..............................................................................31 10 Staffordshire Moorlands District Council Area.....................................................38 11 Tamworth Borough Council Area...........................................................................41 12 Conclusions.............................................................................................................45 -

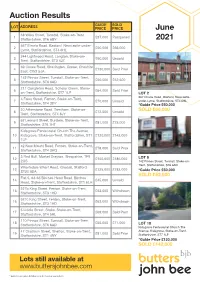

Auction Results June 2021

Auction Results GUIDE SOLD LOT ADDRESS PRICE PRICE June 38 Wilks Street, Tunstall, Stoke-on-Trent, 1 £37,000 Postponed Staffordshire, ST6 6BY 2021 567 Etruria Road, Basford, Newcastle-under- 2 £50,000 £66,000 Lyme, Staffordshire, ST4 6HL 244 Lightwood Road, Longton, Stoke-on- 3 £90,000 Unsold Trent, Staffordshire, ST3 4JZ 69 Crewe Road, Shavington, Crewe, Cheshire 4 £130,000 Sold Prior East, CW2 5JA 142 Pinnox Street, Tunstall, Stoke-on-Trent, 5 £50,000 £52,500 Staffordshire, ST6 6AD 211 Congleton Road, Scholar Green, Stoke- 6 £64,000 Sold Prior on-Trent, Staffordshire, ST7 1LP LOT 2 567 Etruria Road, Basford, Newcastle- 4 Foley Street, Fenton, Stoke-on-Trent, 7 £70,000 Unsold under-Lyme, Staffordshire, ST4 6HL Staffordshire, ST4 3DY *Guide Price £50,000 20 Atherstone Road, Trentham, Stoke-on- 8 £72,500 Unsold SOLD £66,000 Trent, Staffordshire, ST4 8JY 62 Leonard Street, Burslem, Stoke-on-Trent, 9 £81,000 £75,000 Staffordshire, ST6 1HT Kidsgrove Pentecostal Church The Avenue, 10 Kidsgrove, Stoke-on-Trent, Staffordshire, ST7 £120,000 £142,000 1LP 42 New Mount Road, Fenton, Stoke-on-Trent, 11 £78,000 Sold Prior Staffordshire, ST4 3HQ 3 Red Bull, Market Drayton, Shropshire, TF9 12 £150,000 £186,000 LOT 5 2QS 142 Pinnox Street, Tunstall, Stoke-on- Trent, Staffordshire, ST6 6AD Wharfedale Wharf Road, Gnosall, Stafford 13 £125,000 £182,000 ST20 0DA *Guide Price £50,000 Flat 5, 63-65 Birches Head Road, Birches SOLD £52,500 14 £45,000 Unsold Head, Stoke-on-Trent, Staffordshire, ST1 6LH 527b King Street, Fenton, Stoke-on-Trent, 15 £63,000 Withdrawn -

Appendix to 5 Year Housing Land Supply Assessment Report 2017-22

Classification: NULBC UNCLASSIFIED Total New Remaining Site Remaining SHLAA REF Address: Most Recent Planning Application: Brief Description: Dwellings Capacity for next 5 Site Capacity Proposed (net): years at 01/04/2017 Land West Of Ravens Close AB11 Newcastle Under Lyme 16/00727/FUL Erection of 6 dwellings 6 6 6 Staffordshire Audley Working Mens Club New AB17 Road Bignall End Stoke On Trent 15/00692/FUL Erection of 12 houses 12 12 12 Staffordshire ST7 8QF BL20 Land Off Slacken Lane, Kidsgrove 13/00266/FUL Erection of 6 bungalows 6 6 6 Land South Of West Avenue, West Of Church Street And Congleton Road, And BL21 15/00916/REM Residential development of 171 dwellings 171 90 90 North Of Linley Road, Butt Lane, Kidsgrove 13/00625/OUT (COMMERCIAL PERMISSION BL22 Linley Trading Estate, Linley Road, Talke Erection of up to 139 dwellings 139 139 0 IMPLEMENTED) Former Woodshutts Inn, Lower Ash BL23 14/00767/FUL Construction of 22 affordable dwellings 22 22 22 Road, Kidsgrove BL24 Land adjacent 31 Banbury Street, Talke 14/00027/FUL Erection of 13 new dwellings 13 13 13 Methodist Church Chapel Street Butt Erection of 2 two bedroom dwellings, two semi detached houses BL25 14/00266/FUL 10 10 10 Lane and 6 one bedroom apartments BL26 33 - 33A Lower Ash Road, Kidsgrove 15/00452/FUL 8 houses 8 6 6 Land At West Avenue Kidsgrove Residential development for 44 dwellings at West Avenue, BL8 Stoke-On-Trent Staffordshire ST7 15/00368/OUT 44 44 44 Kidsgrove (Phase 4) 1TW Land Rear Of 166 To 188Bradwell Erection of 4 1 bed 2 person apartments and 2 2 bed 4 person BW13 LanePorthillNewcastle Under Lyme 16/00103/FUL 6 6 6 dwellings Staffordshire CH10 Land At Ashfields New Road, Newcastle 15/00699/FUL Construction of 10 houses and 32 flats 42 34 34 CT21 Land off Watermills Road, Chesterton 13/00974/OUT Residential development of up to 65 dwellings 65 65 65 Former Chesterton Servicemen's Club, Mixed use development including new clubhouse, dwellings and CT22 08/00800/REM 19 19 0 Sandford Street, Chesterton commercial unit. -

Potteries Network MASTER May19

Ox-Hey Dr Ox-Hey Halls Rd gate Rd re Pennine Way a H Q u Thames Dr Meadows Way e e Haregate n Station Rd Station Moorland Rd s Dorset Dr D Congleton Rd r i Torville Drive v Akesmoor Ln Rd e ield Novi Lane sf Windsor Drive g Lawton St in 7A Biddulph K Ball Haye GreenP Mount Rd r Well St i n Buxton Rd c e B Brough Top Station Rd Wood St e S l Mill St Abbotts Rd le t C V Park h Springfield Rd Nab Hill AveH u il e u Cornfield Rd lsw r ood Ave R Portland St Woodland c Buxton Rd h d Colliers Way Colliers St John’sStreet Rd R Halls Rd d High St Mow Cop Tower Hill Rd pool Rd Park Lane Westwood Rd 18 Leek ew Park N Ashbo Kniveden Lane Burton St u n rn Lane L Lyneside Rd Lyneside Mayfield Rd e d s R Mow Cop Rd r R Conway Rd a d Chapel St Church St Park Lane d g n g rla e o Compton o Knypersley B Broad St M Knutsford Rd Knutsford Orme Rd Lawton Heath Rd Sands Rd Dales Green Rd Dales Green A523 A Brown Lees W 7 allb F rid Selbourne Rd Mill Hayes Rd e g Dales Green e Brown Lees Rd r Heath End Rd D n Tunstall Rd Tunstall Morrisons w r Sandbach Rd J o u o Barnfield Rd n Le d c Pickmere Rd ice t d st Woodgate B D i on R Hassall Rd e r r A o r v w e Ave n Newcastle Rd Barnfields A Brown Lees Rd network area hous v or e e High St o A Chapel Ln S The Fairway M v Church Lawton unn Sandbach Rd Nth e H yh Wilbrahams Dairylands a ills Shady Gr Shady r R Liverpool Road West rise n d Sandbach Rd Nth Way ahead L Long Lane Alsager Longview Ave Road BOUNDARY Close Ln School High St S network area Rookery c Close Lane h Harriseahead Stadmorslow Lane o Du Co-op AREA -

Planning, Infrastructure and Highways Committee Kidsgrove Town Council Victoria Hall Liverpool Road Kidsgrove Staffordshire ST7 4EL

Planning, Infrastructure and Highways Committee Kidsgrove Town Council Victoria Hall Liverpool Road Kidsgrove Staffordshire ST7 4EL Tel: 01782 782254 www.kidsgrovetowncouncil.gov.uk Minutes of the Planning, Infrastructure and Highways Committee Meeting held on the Thursday, 17th December 2020, 6:30pm, Zoom Meeting Present Cllr M Stubbs, Cllr Dymond, Cllr C Dickens, Cllr G Burnett, Cllr C Dicken, Cllr K Robinson, Cllr V Jukes, Cllr P Waring, Cllr A Cooper (** Cllr Jukes joined the meeting at 19:10) In attendance: Sue Davies, Town Clerk To receive and consider apologies for absence. No apologies. To note declarations of Member’s Interests None To receive and agree the minutes of the meetings held on the 2nd November, 2020 The Committee approved the minutes of the meeting held on the 2nd November 2020. Public Participation – A period not exceeding 15 minutes for members of the public to ask questions or submit comments. None Chair ………………………………… PIH4 2020-21 Page 1 of 7 CCTV provision: To receive an update report from the Clerk and to approve the progression and expenditure detailed in the plan. The Clerk presented a report on progress with recommendations for approval. (See appendix 1). The Committee resolved to approve the recommendations in the report and asked the Clerk to continue to progress the project as a priority. Neighbourhood Plan: To receive an update of the meeting on the 3rd December and to note the date of the next meeting. Cllr M Stubbs provided feedback on the Neighbourhood Plan meetings on the 3rd December 2021. Participants at the meeting, after advice from the Neighbourhood Plan consultant, agreed to progress the Neighbourhood Plan as a priority. -

North Housing Market Area Gypsy and Traveller Accommodation Needs Assessment : Final Report Brown, P, Scullion, LC and Niner, P

North housing market area Gypsy and Traveller accommodation needs assessment : Final report Brown, P, Scullion, LC and Niner, P Title North housing market area Gypsy and Traveller accommodation needs assessment : Final report Authors Brown, P, Scullion, LC and Niner, P Type Monograph URL This version is available at: http://usir.salford.ac.uk/id/eprint/35864/ Published Date 2007 USIR is a digital collection of the research output of the University of Salford. Where copyright permits, full text material held in the repository is made freely available online and can be read, downloaded and copied for non-commercial private study or research purposes. Please check the manuscript for any further copyright restrictions. For more information, including our policy and submission procedure, please contact the Repository Team at: [email protected]. North Housing Market Area Gypsy and Traveller Accommodation Needs Assessment Final report Philip Brown and Lisa Hunt Salford Housing & Urban Studies Unit University of Salford Pat Niner Centre for Urban and Regional Studies University of Birmingham December 2007 2 About the Authors Philip Brown and Lisa Hunt are Research Fellows in the Salford Housing & Urban Studies Unit (SHUSU) at the University of Salford. Pat Niner is a Senior Lecturer in the Centre for Urban and Regional Studies (CURS) at the University of Birmingham The Salford Housing & Urban Studies Unit is a dedicated multi-disciplinary research and consultancy unit providing a range of services relating to housing and urban management to public and private sector clients. The Unit brings together researchers drawn from a range of disciplines including: social policy, housing management, urban geography, environmental management, psychology, social care and social work. -

View Catalogue

ORDER OF SALE CONDITIONS PRINT Property auction catalogue The Best Western Moat House Hotel, Stoke-on-Trent, Staffordshire ST1 5BQ To start at 6.30pm Monday 12 June 2017 www.buttersjohnbee.com ORDER OF SALE CONDITIONS PRINT Property auctions 2017 The Moat House Hotel, Stoke-on-Trent, ST1 5BQ 2017 Auction Dates Closing Date For Entries 23 January 8 December 27 February 19 January 3 April 17 February 8 May 24 March 12 June 28 April 17 July 2 June 21 August 7 July 25 September 11 August 30 October 15 September 4 December 20 October All auctions start at 6.30pm Freehold & Leasehold Lots offered in conjunction with... 2 View property auction results at www.buttersjohnbee.com ORDER OF SALE CONDITIONS PRINT The Region’s Number 1 property auctioneer Meet the team at butters john bee auctions. We also have over 25 expert valuers and John Hand Donna Fern Andy Townsend Auction Manager. Auction Negotiator Managing Director surveyors, who Lettings/Auction can advise on all aspects of selling your property at auction. Peter Sawyer Rob Oulton Tom Wilde Auctioneer Auctioneer Auctioneer Welcome Sales have been strong so far in 2017, and Sandbach, Cheshire, this should continue as we fast approach of a garage forecourt the summer with another 83 properties complete with separate for offer in our June sale. From across living accommodation, the region and catering for every budget, and several building plots we have properties starting with a guide starting at just £5,000. prices as little as £35,000 for a two-bed terrace in Tunstall, Stoke-on-Trent, to a If you are unable to attend the sale, then stunning detached Cottage in Hill Chorlton, you can take advantage of our free online Staffordshire with a guide of £300,000 Internet bidding service.