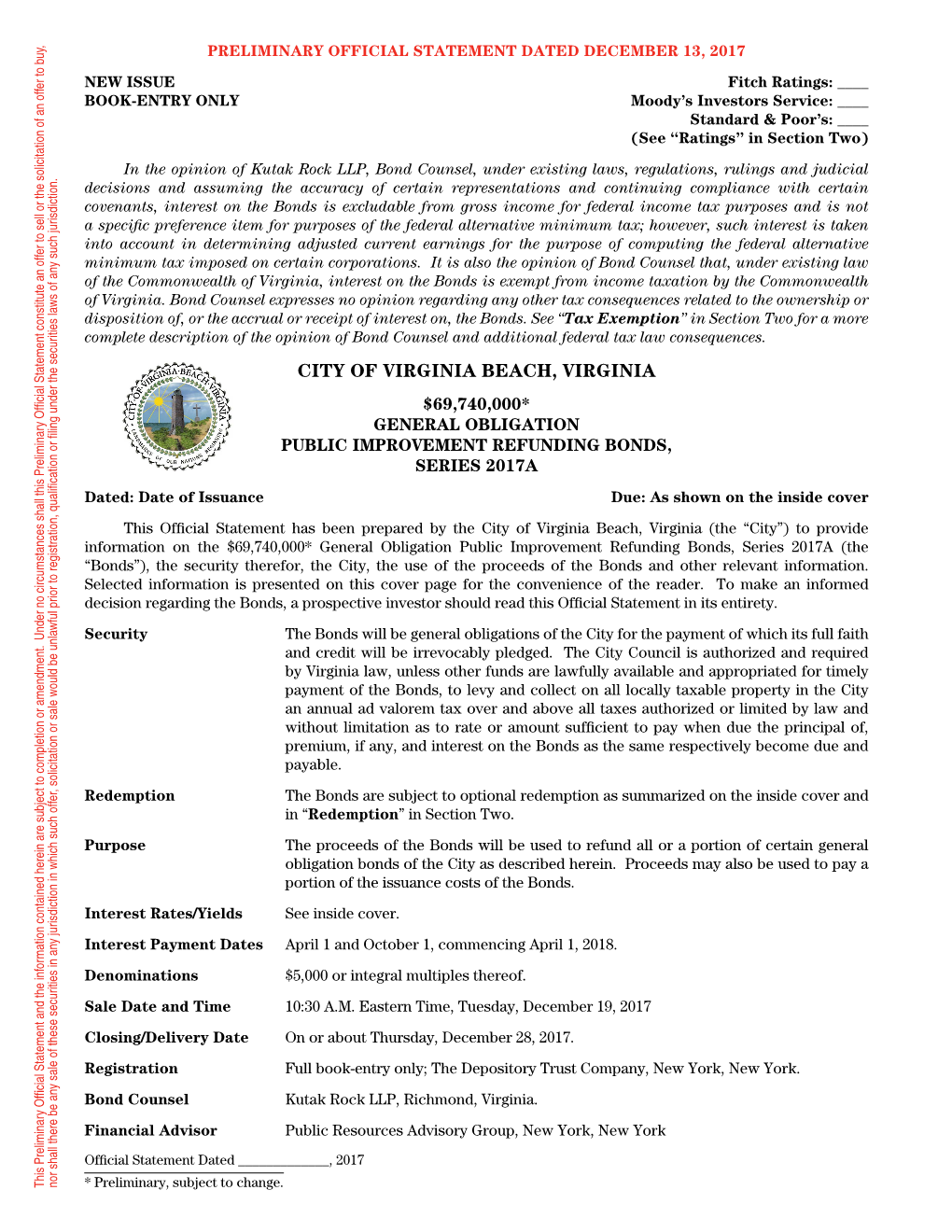

City of Virginia Beach

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Amazon HQ2! the Cavalier Hotel Is Back! How Virginia Incentivizes Big Real Estate Deals

Amazon HQ2! The Cavalier Hotel is Back! How Virginia Incentivizes Big Real Estate Deals Friday, July 19 2019 | The Omni Homestead Resort | Hot Springs, VA CONTINUING Written Materials LEGAL EDUCATION A presentation of The Virginia Bar Association’s Real Estate Law Section Amazon HQ2! The Cavalier Hotel is Back! How Virginia Incentivizes Big PRESENTERS Real Estate Deals Sandra “Sandi” Jones McNinch Sandi McNinch currently serves as General Counsel for the Virginia Economic Development Partnership. In this capacity, she performs all legal functions for VEDP, including the negotiation and preparation of grant performance agreements with Virginia companies receiving discretionary economic development incentives administered by VEDP. Prior to working for VEDP, Sandi worked as a public finance lawyer at Troutman Sanders, LLP, and its predecessor, Mays & Valentine, LLP. She represented localities, issuers, borrowers, investment bankers, credit providers and trustees in financings for public and private facilities and infrastructure. She also represented localities and developers in negotiating and implementing public-private partnerships, including community development authorities, public-private procurement and incentive packages. Sandi graduated from the College of William & Mary, Marshall-Wythe School of Law with a Doctor of Jurisprudence. She received a Bachelor of Arts in Criminal Justice from Michigan State University. Sandi is a member of the Local Government Attorneys of Virginia Association and the Virginia Economic Developers Association, for which she has served as its General Counsel, Vice Chair and member of its Board of Directors. She is also a member of the Virginia State Bar, for which she is a former Chair of the Board of Governors of its Corporate Counsel Section and a former member of the Board of Governors of its Local Government Law Section. -

Chesapeake Community Services Board Resource Directory

Chesapeake Community Services Board Resource Directory 2005/2006 Edition EMERGENCY NUMBERS Ambulance and Fire – EMERGENCY ONLY . 911 Chesapeake Crime Line . 487-1234 Coast Guard . 483-8567 Crisis Center . 399-6393 Dominion Virginia Power . .1-888-667-3000 Navy Information and Referral . 444-NAVY Police Department –EMERGENCY ONLY . .911 Public Utilities (Waterworks)-EMERGENCY . 421-2146 Rescue-EMERGENCY ONLY. 911 Time. 622-9311 Virginia Natural Gas . .1-877-572-3342 Virginia State Police . .424-6820 Weather . 666-1212 Women-in-Crisis . .625-5570 ______________________________________________________________________ PREFACE The Chesapeake Community Services Resource Directory, 2005/2006 Edition, has been compiled for the citizens of Chesapeake by the Chesapeake Community Services Board. The directory is designed to assist in locating specific local and regional services available to Chesapeake citizens. Every attempt has been made to ensure accuracy and to provide a comprehensive, diverse directory of community services. If you know of services not listed, or identify changes that should be made to specific listings for future publications, please feel free to let us know by sending in the Directory Update Form located at the end of this document. The preparers have not made a complete evaluation of the services and programs contained in this directory and the listings therefore do not indicate endorsement. The Community Services Board would also like to thank the Department of Human Resources, who provided a student intern to help complete this directory. In addition, we would like to thank the City of Chesapeake Manager’s office and the City Council for providing the funding for the student internship program. Special Note: Unless otherwise indicated, telephone/fax/pager numbers listed in this directory are assumed to begin with the 757 area code prefix. -

![Vbfun Guide Full[1].Pdf](https://docslib.b-cdn.net/cover/2495/vbfun-guide-full-1-pdf-712495.webp)

Vbfun Guide Full[1].Pdf

W E L C O M E T O oouu rr gguuiiddee YY TO SEIZING THE DAY Life’s rewarding experiences – do they just happen, unplanned and unexpected? Or do these moments only occur as a plan comes together? This Vacation Guide will help you make the most of your time in Virginia Beach. You’ll find places to stay, what’s cool to see, things you won’t want to miss doing, and where to find it all. This is your handbook for creating your best vacation. Use it along with the videos and features you’ll find at www.VisitVirginiaBeach.com. Items listed throughout the guide are identified by a color block, showing in which area of Virginia Beach you’ll find a particular attraction or accommodation. The color-coded map on page 5 shows the areas. To help you find your way around when you’re here, there is a pullout map page in the center of the guide. More information is always available online at www.VisitVirginiaBeach.com, or by calling the Visitor Information Center at 800-VA BEACH. 1-800-VA BEACH VisitVirginiaBeach.com Beyond memories, you experience a feeling. It’s the thrill of loading the car with beach gear, tucking in your beside-themselves-with- excitement family, and hitting the open road that leads to the oceanfront. It’s the sweet reminiscence of youth as you watch your children chasing crabs for the first time. It’s the TRIP ADVISOR TRAVELERS’ CHOICE 2012 warmth of the sun’s rays on your neck as you step out for the first summer beach session. -

Nomination Form

I I Fc,rrn 10-300 UNITED STATES DEPARTMENT OF THE INTERIOR (?mu. 6-71) NATIONAL PARK SERVICE HATlONAh REGISTER OF HjSTORIC PLACES INVENTORY - NOMIHATFON FORM (Type all entries - complete applicable sections) Rose Hall t-AND/OR HISTORICI 1 3133 Virainia Beach Boulevard ClTY OR TOWN: . CONGRL5SIONAL DiSTRICT: L Pginia Beach l~econd(G. William Whitehurst) 57'ATh CODE I STATUS [T~~,~~~f,c/ Public Acqui%itian: Yss: In Procss~ 5 VortstrEctsd 0 Obicct Both a Being Considsrsd iJ Prtseruat+onwork PRESRN f Us E (Check One or Mar* ou AwroprisC-) I I-J Gov~rnment n Pork m .Canmkrciol , 0 Industrial n Private Residence Other {~peeiip) - Educationel Mifitmry 13 Auligious None -- Entarhinmemt 0 Museum Scientific Industrial Security Corporation - 820 United VFrginia Bank Butlding , - ClfY QR TOWN: STATE. Eurfolk , Virginia 5 1 t , , -. oEScn~Prrow--- . ., . ... RY OF DEEDS. ETC. Virginia Beach City Hall STPEE T AND NVhlBhR: Historic @er ican euildings Survey I?rlve~t~rv nATB OF SURVEY: 1958 Federul fi Sta~s 3 Coun:y rl LOCO! DEPOSITORY FOR SUNVEY RECOHOS: Library of Cangrcss -- STREET AND NUMBER. -. STATE: I)* c* =.- The Francis Land House, known in recent years as Rose Hall, stands on an open tract about 200 yards south of the highly commercialized Virginia Beach Boulevard. In front of the house are several large trees and the remnants of a garden. The house is a five-bay, one-and-one-half-story, gambrel-roofed building set on a high basement. Its walls are of brick laid in Flemish bond with rubbed and gauged jack arches. At each end are brick interior end chimneys with corbeled caps. -

Twixt Ocean and Pines : the Seaside Resort at Virginia Beach, 1880-1930 Jonathan Mark Souther

University of Richmond UR Scholarship Repository Master's Theses Student Research 5-1996 Twixt ocean and pines : the seaside resort at Virginia Beach, 1880-1930 Jonathan Mark Souther Follow this and additional works at: http://scholarship.richmond.edu/masters-theses Part of the History Commons Recommended Citation Souther, Jonathan Mark, "Twixt ocean and pines : the seaside resort at Virginia Beach, 1880-1930" (1996). Master's Theses. Paper 1037. This Thesis is brought to you for free and open access by the Student Research at UR Scholarship Repository. It has been accepted for inclusion in Master's Theses by an authorized administrator of UR Scholarship Repository. For more information, please contact [email protected]. TWIXT OCEAN AND PINES: THE SEASIDE RESORT AT VIRGINIA BEACH, 1880-1930 Jonathan Mark Souther Master of Arts University of Richmond, 1996 Robert C. Kenzer, Thesis Director This thesis descnbes the first fifty years of the creation of Virginia Beach as a seaside resort. It demonstrates the importance of railroads in promoting the resort and suggests that Virginia Beach followed a similar developmental pattern to that of other ocean resorts, particularly those ofthe famous New Jersey shore. Virginia Beach, plagued by infrastructure deficiencies and overshadowed by nearby Ocean View, did not stabilize until its promoters shifted their attention from wealthy northerners to Tidewater area residents. After experiencing difficulties exacerbated by the Panic of 1893, the burning of its premier hotel in 1907, and the hesitation bred by the Spanish American War and World War I, Virginia Beach enjoyed robust growth during the 1920s. While Virginia Beach is often perceived as a post- World War II community, this thesis argues that its prewar foundation was critical to its subsequent rise to become the largest city in Virginia. -

Designing the Future of Coastal Virginia Beach Landscape Design and Planning Studio

DESIGNING THE FUTURE OF COASTAL VIRGINIA BEACH LANDSCAPE DESIGN AND PLANNING STUDIO Landscape Architecture Program School of Architecture + Design Virginia Polytechnic Institute and State University Dr. Mintai Kim COURSE DESCRIPTION TABLE OF CONTENTS: This book documents the developments in an advanced studio course that enables students to address land- PHASE (1): scape architectural design and planning issues in various contexts and at a range of scales. Course Introduction ..........................................................4 Land planning and design in urban, suburban, and rural environments are a major professional PHASE 2: realm of landscape architects. Informed land planning and design should carefully consider the GIS Analysis for virginia beach ......................................22 impacts of each project on the surrounding wwenvironment. It is essential to understand that macro scale processes that link each project to its larger regional and global context. Responsible planning and design also depends on knowledge of the social needs, historic and cultural values, PHASE 3: political and economical feasibility, and perceptions of the people who are affected by the design Geodesign Workshop......................................................48 and planning activities. PHASE 4: The studio is aimed at providing students with the ability to understand, synthesize and apply Design & Planning...........................................................60 cultural and natural factors and issues on a continuum from a large scale -

Cavalier Hotel

NPS Form 10-900 United States Department of the Interior National Park Service National Register· of Historic Places Registration This form is for use in nominating or requesting determinations for individual properties and districts. See instructions ' Bulletin, How to Complete the National Register of Historic Places Registration Form. If any item does not apply STf141C PLACES 1 documented, enter "NIA" for "not applicable." For functions, architectural classification, materials, and areas of si~~~~Uf!!!f!1~,S~E~RV!,:! 1C2:-E _ _J categories and subcategories from the instructions. 1. Name of Property Historic name: Cavalier Hotel 0ther names/site~-------------------------- number: VDHR#134-0503, Cavalier Hotel, Cavalier on the Hill Name of related multiple property listing: N/A (Enter "NI A" if property is not part of a multiple property listing 2. Location Street & number: 4200 Pacific A venue City or town: Virginia Beach State: VA County: Independent City Not For Publication:~ Vicinity: ~ 3. State/Federal Agency Certification As the designated authority under the National Historic Preservation Act, as amended, I hereby certify that this _x_ nomination _ request for determination of eligibility meets the documentation standards for registering properties in the National Register of Historic Places and meets the procedural and professional requirements set forth in 36 CFR Part 60. In my opinion, the property __x_ meets _ does not meet the National Register Criteria. I recommend that this property be considered significant at the following level(s) of significance: _national _statewide X local Applicable National Register Criteria: X A _B X C _D Date _ Virginia Department of Historic Resources _____ State or Federal agency/bureau or Tribal Government In my opinion, the property _meets_ does not meet the National Register criteria. -

Toronto-Niagara Falls

VIRGINIA BEACH 3 DAYS / 2 NIGHTS Virginia Beach…From the time you arrive, you smell the sea air, hear the planes flying overhead, feel the heat of the burning sun & see the beautiful beaches. • 2 Nights hotel accommodations in Greater Virginia Beach • 2 Breakfasts & 2 Dinners • Day at the beach – Spend a day at leisure for sunbathing in the sun’s rays in beautiful Virginia Beach. Relax, swim, go seashell hunting, play volleyball or build a castle; but don’t forget the sunscreen. The cool water, warm sand, and pleasant air temperatures definitely make for a great school trip. • The Virginia Beach Surf & Rescue Museum – Learn about Virginia Beach’s maritime history, surf and rescue, superstorms, shipwreck and more. • Spirit of Norfolk DJ Cruise – Come onboard for a unique dance cruise. Groove down the Elizabeth River with one of the hottest DJs in Norfolk and feast on a bountiful buffet. Student will have an unforgettable evening! • Virginia Aquarium & Marine Science Center – Explore the ocean’s secrets… Discover the amazing underwater world of the Virginia Aquarium. Travel an aquatic journey from the shore to the depth of the Atlantic Ocean and have the opportunity to be part of so many experiences. • Surf Lessons* – Learn the fundamentals of surfing in a safe and fun environment. Experienced instructors will guide students through beach and weather education and safety, surfing etiquette, equipment knowledge and learn how to read the ocean's tides, rip currents and swells. *Surfboards provided / Limited availability • USS Battleship Wisconsin – A field trip to Nauticus is a fun and exciting way to help your students learn about the fascinating world of science! Berthed at Nauticus, the Battleship Wisconsin is one of the largest and last battleships ever built by the U.S. -

Cavalier Proof FINAL.Pdf

Specifications, drawings, plans, illustrations and representations of amenities are conceptual and subject to change without notice. While every effort has been made towards accuracy, square footage and pricing are approximate and subject to change without notice. Cavalier Realty Associates www.cavalierrealtyassociates.com 757-352-2764 The Hotel That Made Virginia Beach Famous For over 90 years, The Cavalier has been the hotel that The hotel guest rooms had every amenity available. Each made Virginia Beach famous. In the early 1920s, it was bathtub at The Cavalier had a fourth handle for seawater, the crown jewel of a 4,000-acre development (by the which was coveted for its therapeutic effects. The hotel’s original Cavalier Associates) that included Bay Colony, swimming pool was even filled with filtered seawater, what is known today as the Cavalier Yacht Club, and which continued until the mid-70s. The lower lobby Cavalier Shores. The Cavalier was heralded as a world- was filled with an amazing array of shops. Guests could class resort and state-of-the-art architectural masterpiece. get their hair cut, shop for dresses, purchase medicine and gifts, or get a scoop of ice cream. A doctor also kept Since its ceremonious opening in April 1927, the office in the lobby, as did a commercial photographer. luxurious grand hotel has hosted aristocrats, luminaries, However, the most unique shop in The Cavalier was a celebrities, socialites and international political leaders. stock brokerage office, which had a ticker tape directly These have included the likes of Sophie Tucker, Al from the New York Stock Exchange. -

Preservation Assessment of the Lynnhaven House Cemetery, Virginia Beach, Virginia

PRESERVATION ASSESSMENT OF THE LYNNHAVEN HOUSE CEMETERY, VIRGINIA BEACH, VIRGINIA Chicora Research Contribution 554 Preservation Assessment of the Lynnhaven House Cemetery, Virginia Beach, Virginia Prepared By: Michael Trinkley, Ph.D. and Debi Hacker This project is funded in part by a grant from the Tidewater Chapter of the National Society of the Colonial Dames of America CHICORA RESEARCH CONTRIBUTION 554 Chicora Foundation, Inc. PO Box 8664 Columbia, SC 29202 803-787-6910 www.chicora.org August 2013 This report is printed on permanent paper ∞ ©2013 by Chicora Foundation, Inc. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, transmitted, or transcribed in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise without prior permission of Chicora Foundation, Inc. except for brief quotations used in reviews. Full credit must be given to the author and publisher. MANAGEMENT SUMMARY This study was funded in part by a grant This report classifies all of the identified from the Tidewater Chapter of the National needs into three broad categories: Society of the Colonial Dames of America to the City of Virginia Beach. The work was conducted by • Those issues that are so critical – typically Chicora Foundation on July 25 and 26, 2013 and reflecting broad administrative issues, involved two-days on-site and a meeting with health and safety concerns, and issues representatives of the City’s Department of that if delayed will result in significantly Museums involved in the preservation of the greater costs – that require immediate Lynnhaven House Cemetery. attention. These actions should be accomplished either in what remains of The study examines a small family 2013 or 2014. -

The Art of Fine Homes Landing, Virginia Beach, 23454

218 Virginia Beach 219 Two-day combo tickets: $55 pp. Tour Wednesday in Virginia Beach and Thurs- day in Norfolk. Available only at www. vagardenweek.org. Tour headquarters and lunch location: Broad Bay Country Club, 2120 Lords The Art of Fine Homes Landing, Virginia Beach, 23454. $20 pp for buffet lunch served from 11 a.m. to 2:30 p.m. (757) 496-9090 for reservations. Virginia Facilities: Available at Tour Headquarters, Broad Bay Country Club, and All Saints’ Episcopal Church, 1969 Woodside Lane. Directions to tour headquarters: Take I-264E then London Bridge Rd. exit 19C, Wednesday, April 25, 2018 turn left following Great Neck Rd. signs, Beach stay on Great Neck Rd. going south 3.7 10 a.m. to 5:30 p.m. mi., turn right onto Lords Landing. The Painted Garden Art Show at Photo courtesy of Rendy Adams Beach Gallery, 313 Laskin Rd., opens on Saturday, April 14 with a reception from 6 to 9 p.m. and runs through Satur- Great Neck Point has always been desirable real estate. The Chesapean Indians built day, May 12th. The featured artist is Ste- one of their largest permanent encampments on the land protected by Long Creek on phie Jones. Gallery hours from M-F 10 the north and the Lynnhaven River on the west and south. Although the first English a.m. to 6 p.m. and Saturday 10 a.m. to 5 colonists sampled the famed Lynnhaven oyster in 1607, they inexplicably sailed on. p.m. Complimentary refreshments served 4 to 5:30 p.m. -

Sites Listed on the Virginia Beach Historical Register - by Address As of September 13, 2016 (Year Listed Shown in Parenthesis)

Sites Listed on the Virginia Beach Historical Register - By Address As of September 13, 2016 (Year listed shown in parenthesis) 411 16th Street (2004) 301 20th Street, Nita Fay House (2005) – removed from Register 3/20/14 303 20th Street, Coker-Moore House (2004) – removed from Register 3/20/14 211 24th Street, First Police and Fire Station (2014) 408 26th Street, The Ford Property (2002) 315 35th Street, The Edgar Cayce Home (2003) 101 43rd Street, Darden House (2015) 109 43rd Street, Sessoms House (2008) 213 43rd Street (2015) 214 44th Street (Raleigh Drive) (2014) 207 53rd Street (2015) 301 53rd Street, The English Cottage (2002) 304 53rd Street (2016) 301 54th Street, Pine Hill (2002) 215 67th Street, Cayce Hospital for Research and Enlightenment (2003) 207 66th Street, The Howell Residence (2003) 200 78th Street, Spruance Cottage (2003) 229 Bay Colony Drive, Holly House (2003) 4300 Calverton Lane, Calverton (2013) 533 Carolina Avenue, The Towne-Johnson Home (2003) 805 Cavalier Drive (2004) 4136 Cheswick Lane, Ferry Plantation House, (2001) 520 Constitution Drive, Pembroke Manor House (2002) 3425 S. Crestline Drive, Thomas Murray House (2002) 1140 Crystal Lake Drive, The Darden House (2003) 5047 Euclid Road (2004) 3300 Harlie Court, Richard Murray Manor House (2002) 2300 Holland Road, St. John’s Baptist Church (2002) 1909 Indian River Road (2004) 525 Kempsville Road, Kempsville High School (2013) 704 Kings Grant Road, John Biddle House (2016) 420 Linkhorn Drive, Selden Hall (2015) 1033 Little Neck Road, Lynnhaven United Methodist Church (2009) 2380 London Bridge Road, William Woodhouse House (2004) 1560 N.