The Philippines: Strategic Purchasing Strategies and Early Results

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Regional Webpage for the Month of March 2019

Republic of the Philippines Office of the President PHILIPPINE DRUG ENFORCEMENT AGENCY REGIONAL OFFICE VI Pepita Aquino Avenue corner Fort San Pedro Drive, Iloilo City 5000 (033) 337-1600 pdea.gov.ph PDEA Top Stories PDEA@PdeaTopStories pdeatopstories pdea.region6 and @PDEA6official [email protected] Regional Webpage for the Month of March 2019 Pusher Beautician in Capiz Caught Selling Shabu Joint elements of the Capiz Provincial Police PIB/PDEU, President Roxas MPS, Police Drug Enforcement Unit, Provincial Intel Section and the PDEA Capiz Provincial Office conducted Buy Bust Operation at around 1:30 early this morning of March 3, 2019 at Sitio Tinundan Barangay Poblacion, President Roxas, Capiz. Suspected person was identifed as Jonathan Cartujano Dela Cruz of Brgy VII Roxas City Capiz, 32 years old and a beautician, who was caught upon recovery from his possession five (5) pieces Php100.00 peso bill buy-bust money in exchange for one (1) heat sealed sachet of suspected shabu and another two (2) heat-sealed sachets of suspected shabu from his possession. Cases for violation of RA 9165 or the Comprehensive Dangerous Drugs Act of 2002 are now being prepared for filing in court. 1 Brgy Igang and Brgy Guiwanon Nueva Valencia, Guimaras Undergo Post Operation Phase The PDEA Guimaras Provincial Office led by Investigation Agent III Jyxyvzcky G Escrupolo, together with DILG, Nueva Valencia MPS, CBRP Facilitators, PAO, MHO and the barangay local officials conducted symposium on anti-illegal drugs, anti-criminality and violence against women and children lectures last March 1, 2019 at Sitio Onisan, Brgy Guiwanon Nueva Valencia Guimaras and last February 21,2019 held at the Igang Elementary School. -

Governor: Address: Region I Gov. Imee R. Ma

Unit 1510, West Tower , Philippine Stock Exchange Centre, Exchange Road, Pasig City Contact Nos :(02) 6875399; 631-0197; 631-0170 Fax No. (02) 687-4048 Website: www. lpponline.org Email Address: [email protected] GOVERNOR: ADDRESS: TELEPHONE NUMBERS FAX NOS. REGION I GOV. IMEE R. MARCOS Provincial Capitol, (077) 772-1211 (077) 772-1772 2900 Laoag City, Ilocos Norte (077) 770-3966 (077) 770-3966 GOV. RYAN LUIS V. SINGSON Provincial Capitol (077) 722-2776 (077) 722-2776 2700 Vigan, Ilocos Sur 722-2746 (077) 722-7063 GOV. MANUEL C. ORTEGA Provincial Capitol (072) 888-3608 (072) 888-4453 2500 San Fernando, La Union GOV. AMADO T. ESPINO JR. Provincial Capitol (075) 542-2368 (075) 542-6438 2401 Lingayen, Pangasinan (075) 542-6438 REGION II GOV. VICENTE D. GATO Provincial Capitol N/A N/A 3900 Basco, Batanes GOV. ALVARO T. ANTONIO Provincial Capitol (078) 304-0083 (078) 846-7576 3500 Tuguegarao, Cagayan (078) 304-2293 GOV. FAUSTINO G. DY, III Provincial Capitol (078) 323-2536 (078) 323-0369 3300 Ilagan, Isabela 323-2038 GOV. RUTH R. PADILLA Provincial Capitol (078) 326-5474 (078) 326-5474 3700 Bayombong, Nueva Vizcaya GOV. JUNIE E. CUA Provincial Capitol (078) 692-5068 (078) 692-5068 3400 Cabarruguis, Quirino (02) 633-2118 CAR GOV. EUSTAQUIO P. BERSAMIN Provincial Capitol (074) 752-8118 (074) 752-7857 2800 Bangued, Abra GOV. ELIAS C. BULUT, JR. Provincial Capitol (02) 932-6495 (02) 932-6495 3809 Kabugao, Apayao 427-8224 GOV. NESTOR B. FONGWAN Provincial Capitol (074) 422-2609 (074) 422-2004 2601 La Trinidad, Benguet GOV. DENIS B. -

VOTERS ID – a No

VOTERS ID – A No. SURNAME GIVEN NAME MIDDLE NAME 1. ABACAN EDUARDO BAUTISTA 2. ABAD ANNA MARIE TEOPIS 3. ABAD MARY JANE MALAZARTE 4. ABAD RODOLFO BALLESTEROS 5. ABAD MARIFE HIDALGO 6. ABAD AILEEN SANTOS 7. ABADIER EMILE JINNO VALDEBELLA 8. ABAG SOTERO NESTOR PAGKALIWAGAN 9. ABALA TEODORA CORTEX 10. ABALLAR ROGELIO CALGAO 11. ABALLE LEAH MACABUHAY 12. ABALOS MELIE COLLADO 13. ABALOS VIVIAN BAUTISTA 14. ABALUS ANNIE BARRUGA 15. ABAN METCHOY TAWASAN 16. ABAN AHMAD-DEO RODRIGO 17. ABANCE ANNIE GRACE ESTILLES 18. ABANDO NOE SALDY CACAYURAN 19. ABANES ZENAIDA CACANINDIN 20. ABANIA ANACLETA PAGULAYAN 21. ABANILLA IVAN PAUL BRIONES 22. ABANILLA CRISTINA PERANO 23. ABANTE NATALIA GARCIA 24. ABAPO JILL PAULA MALINAO 25. ABAPO MARY EVE BALACUIT 26. ABAPO JESSYBEL ITURIAGA 27. ABARCA RONELL BALTAZAR 28. ABARCA IRISH CALVARA 29. ABARILLA JULITA UPLAS 30. ABARRI LUCIA ANTOJADO 31. ABASTILLAS GINA MERABUENO 32. ABASTILLAS CYRIE MARIE FIGURACION 33. ABAT IMELDA BALICAO 34. ABAT ALEX SALAZAR 35. ABAYA ROFFALYN SANTOS 36. ABDON CATHERINE PILAR SENIBALO 37. ABDUL AZIZ NOROLYAQEEN DATUMANONG 38. ABDUL CARIM ANISA BARAGUIR 39. ABDUL RAHMAN YOLANDA VELARDE 40. ABDUL SAUDA BINTI 41. ABDULHAMID NUR INA ALAMMUHADI 42. ABDULLAH NOR SOFEYAH JAFAR 43. ABDULLAH ROSANA JAWARI 44. ABDULLAH SARAH MAMINTAL 45. ABDULLAH ANNA NADIA MUHAMMAD 46. ABDULLAH MOHD. RUZIS DOMINGO 47. ABDULRASHID ABUBACAR CASANGUAN 48. ABEAR SHALLY PESA 49. ABEDES CORAZON AGUERRA 50. ABEJERO NONILON LEOPARTE 51. ABEJO NILROSE CABAYAO 52. ABEJUELA CHIN-CHIN TAMAYO 53. ABELLA JOCELYN POSILERO 54. ABELLA CHONA CAPANGPANGAN 55. ABELLA JOCELYN POSILERO 56. ABELLA RUTHEL GONZALES 57. ABELLERA TERESITA SERVILLANO 58. ABELLO MARK LOUIE FLORES 59. -

Salguet to Zurita

REPUBLIC OF THE PHILIPPINES COMMISSION ON ELECTIONS OFFICE FOR OVERSEAS VOTING CERTIFIED LIST OF OVERSEAS VOTERS (CLOV) (LANDBASED) Country : UNITED STATES OF AMERICA Post/Jurisdiction : LOS ANGELES Source: Server Seq. No Voter's Name Registration Date 43443 SALGUET, MARCELO PLANCO July 13, 2015 43444 SALIBAY, BERNARDO BESARIO October 05, 2015 43445 SALIDO, GLOVIN ASCANO January 22, 2015 43446 SALIDO, HEGINIO NARCISO August 02, 2018 43447 SALIENDRA, NANETTE BABAT April 20, 2015 43448 SALIENDRA, RICHELLE BALAMBAN July 26, 2018 43449 SALIG, ALEXIUS BALBIDO July 16, 2018 43450 SALIGAMBA, RHEA - February 03, 2015 43451 SALIGUMBA, ELLA MAY LOMUGDANG September 10, 2017 43452 SALIGUMBA, MIHDA ALI March 12, 2017 43453 SALIGUMBA, RAFFGER ABELLO September 10, 2017 43454 SALILENG, ARLEEN GONZALES September 01, 2015 43455 SALILENG, KAREN MICHELLE TANAGON July 30, 2015 43456 SALIMBAGAT, RALPH GOGUANCO January 20, 2018 43457 SALIMBANGON, NINA JAZMIN REARIO January 16, 2015 43458 SALIMBANGON, ULPA NOVABOS December 18, 2017 43459 SALIMBANGON, ULPA NOVCABOS August 15, 2012 43460 SALINAS, ALZAIDA FERRER December 18, 2014 43461 SALINAS, ANELIA MONTAS May 03, 2012 43462 SALINAS, AURA FEBE FENIS November 03, 2014 43463 SALINAS, DIOMEDES BANTILAN October 10, 2012 43464 SALINAS, GIGI CUBOS October 24, 2017 43465 SALINAS, GLORIA HERNANDEZ March 29, 2015 43466 SALINAS, IMELDA RAFOLS May 04, 2018 43467 SALINAS, LUZVIMINDA LOPEZ July 27, 2015 43468 SALINAS, MARICAR JOYCE JUAN April 25, 2017 43469 SALINAS, MARICHU DURAN May 24, 2014 43470 SALINAS, MIGUEL JR. GALLIGUEZ October 04, 2017 43471 SALINAS, ROEHMER AYING October 03, 2014 NOTICE: All authorized recipients of any personal data, personal information, privileged information and sensitive personal information contained in this document. -

April-June 2019 Issue

InIn thisthis issue...issue... > PCAF employees convene for Agency Performance Management System.......................................................... 2 > 2019 Farmer-Director program................... 3 > Policymaking and Engagement Competency Workshop for AFCs.............. 4 > AFC orientations of newly recruited members....................................................... 5 > Industry stakeholders recommend DA FY 2020 proposed plan & budget.................... 7 > PCAF celebrates ANIMversary................... 8 ISSN 1656-7277 Volume 5 No.2 April to June 2019 PCAF, PCA collaborate for 2019 National Coconut Summit Almost 200 coconut stakeholders several development programs like President Rodrigo Duterte with “a from the private and government coconut replanting, fertilization, conclusion that it may have violated sectors participated in the 1st National scholarship program for deserving the Constitution and lacked vital Coconut Summit held on June 20, children of coconut farmers, research safeguards to avoid the repetition of 2019 in Quezon City. and development, establishment of the painful mistakes committed in the The summit, a collaboration a coconut farmers’ bank, and other p a s t ”. between the Philippine Council investments. During PCAF consultations for Agriculture and Fisheries However, the funds were diverted conducted on March 19, 2019, coconut (PCAF) and the Philippine Coconut into projects unrelated to its original stakeholders agreed to consolidate Authority (PCA), aimed to come purpose, that is for the development their positions on the proposed bills up with a unified and harmonized of the coconut industry. Numerous of the congress, thus the realization coconut stakeholders’ position on the legislative actions and proposals were of the 1st National Coconut Summit utilization and management of the filed in the past congresses for the 2019. coconut levy funds. utilization and management of the “We are here because we need to Republic Act No. -

Passports Reception Report

Passports Reception Report Report Generation Date : 06-Feb-2019 09:56 Report Date From : 01-Jul-2016 Report Generated By : ISSJESGUERRA Report Date To : 31-Dec-2016 Site Name : 056 Application Reference Passport Passport Application Estimated No Passport No First Name Middle Name Last Name Gender Issuance Site Isuued Date No Type Status Date Collection Date 00561483201607261529 1 EC8452668 CYRUS EDUARD YABUT RUADO Male Regular Received ABU DHABI SITE 26-Jul-2016 26-Sep-2016 07909W 00561483201611031140 2 P1018759A ESPERANZA ARANETA CABANELA Female Regular Received ABU DHABI SITE 03-Nov-2016 23-Nov-2016 04624W 00561483201611031140 3 P1018759A ESPERANZA ARANETA CABANELA Female Regular Received ABU DHABI SITE 03-Nov-2016 23-Nov-2016 04624W 00561483201611241115 4 P1252150A MARK LUTHER DUNGCA FERNANDEZ Male Regular Received ABU DHABI SITE 24-Nov-2016 14-Dec-2016 37997W 00561483201611241115 5 P1252150A MARK LUTHER DUNGCA FERNANDEZ Male Regular Received ABU DHABI SITE 24-Nov-2016 14-Dec-2016 37997W 00563520201611101531 6 P1085892A MARIA ZENY FORTUNO EVASCO Female Regular Received ABU DHABI SITE 10-Nov-2016 30-Nov-2016 32108W 00563520201611141829 7 P1126034A JANETA RAMOS SERGIO Female Regular Received ABU DHABI SITE 14-Nov-2016 04-Dec-2016 08345W 00563520201611211833 8 P1197289A GRACE KELLEY SIMBAJON Female Regular Received ABU DHABI SITE 21-Nov-2016 11-Dec-2016 58897W 00563520201611292026 9 P1278544A JOSEPHINE TOLDO ESPINOSA Female Regular Received ABU DHABI SITE 29-Nov-2016 18-Dec-2016 46775W 00563520201612122126 10 P1397509A JIZELLE AUDREY -

11, 2020 Page 1/ Date Title

STRATEGIC BANNER COMMUNICATION UPPER PAGE 1 EDITORIAL CARTOON STORY STORY INITIATIVES PAGE LOWER SERVICE June 11, 2020 PAGE 1/ DATE TITLE : Source: https://www.facebook.com/1535812816731782/posts/2577173255929061/ STRATEGIC BANNER COMMUNICATION UPPER PAGE 1 EDITORIAL CARTOON STORY STORY INITIATIVES PAGE LOWER SERVICE DENR urges households to segregate suspected June 11, 2020 PAGE 1/ DATE TITLE : hazardous waste 1/2 DENR urges households to segregate suspected hazardous waste By: Cathrine Gonzales - Reporter / @cgonzalesINQ INQUIRER.net / 04:59 PM June 10, 2020 ENHANCED EXPOSURE A garbage collector does a balancing act while stacking up bags of trash on a moving dump truck en route to a waste transfer station in Barangay Santo Niño, Marikina City, in this photo taken on April 11. —LYN RILLON MANILA, Philippines — The Department of Environment and Natural Resources (DENR) on Wednesday urged households, especially those with individuals undergoing home quarantine, to segregate used face masks and other personal protective equipment to help keep garbage collectors safe from the coronavirus disease. Environment Secretary Roy Cimatu said that while the disposal of PPEs in the country is being done accordingly, it could be a challenge in the future if the number of COVID-19 cases in the country continues to swell. Cimatu said strict sanitation measures and proper disposal of wastes are necessary during this time of pandemic to ensure also the health and safety of garbage collectors. Environment Undersecretary Benny Antiporda, DENR spokesperson and head of the department’s solid waste management, also encouraged households to separately dispose of used face masks, gloves and other COVID-related protection gear. -

Unit 1510, West Tower, Philippine Contact Nos:(02) 6875399; 63

Unit 1510, West Tower, Philippine Stock Exchange Centre, Exchange Road, Pasig City Contact Nos:(02) 6875399; 631-0197; 631-0170 Fax No. (02) 687-4048 Website: www.lpponline.org Email Address: [email protected] GOVERNOR: ADDRESS: TELEPHONE NUMBERS FAX NOS. REGION I GOV. IMEE R. MARCOS Provincial Capitol, (077) 772-1211 (077) 772-1772 2900 Laoag City, Ilocos Norte (077) 770-3966 (077) 770-3966 GOV. RYAN LUIS V. SINGSON Provincial Capitol (077) 722-2776 (PA) (077) 722-2776 2700 Vigan, Ilocos Sur 722-2746 GOV. FRANCISCO EMMANUEL R. ORTEGA III Provincial Capitol (072) 888-3608 (072) 888-4453 2500 San Fernando, La Union 888-6035 GOV. AMADO I. ESPINO III Provincial Capitol (075) 542-2368 (075) 542-2368 2401 Lingayen, Pangasinan REGION II GOV. MARILOU CAYCO Provincial Capitol [email protected] [email protected] 3900 Basco, Batanes GOV. MANUEL MAMBA Provincial Capitol (078) (078) 3500 Tuguegarao, Cagayan (078) GOV. FAUSTINO G. DY, III Provincial Capitol (078) 323-2536 (078) 323-0369 3300 Ilagan, Isabela 323-0369 GOV. CARLOS M. PADILLA Provincial Capitol (078) 326-5474 (078) 326-5474 3700 Bayombong, Nueva Vizcaya GOV. JUNIE E. CUA Provincial Capitol (078) 692-5068 (078) 692-5068 3400 Cabarruguis, Quirino (02) 633-2118 CAR GOV. MARIA JOCELYN BERNOS Provincial Capitol (074) 752-8118 (074) 752-7857 2800 Bangued, Abra GOV. ELIAS C. BULUT, JR. Provincial Capitol (02) 932-6495 (02) 932-6495 3809 Kabugao, Apayao 427-8224 GOV. CRESENCIO C. PACALSO Provincial Capitol (074) 422-2004 / 2609 (074) 422-2004 2601 La Trinidad, Benguet (074) 422-2132 (PA) GOV. PEDRO MAYAM-O Provincial Capitol (074) (074) 3600 Lagawe, Ifugao GOV. -

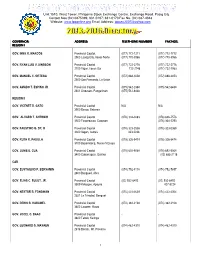

Directory of Members 2004-2007 Name Address Tel

DIRECTORY OF MEMBERS 2004-2007 NAME ADDRESS TEL. NOS. FAX NOS. REGION I Augusto Aureo Q.NISCE San Fernando City, La Union (072)888 -4361 242 -1015 2500 700-3266 888 4453 Windell D. CHUA Laoag City, Ilocos Norte 2900 (077)771 -4499 770 -3262 772-1211 DEogracias VICTOR Vigan, Ilocos Sur 2700 (077)722 -3003 722 -3898 B.SAVELLANO * 722-3898/2746 722-2740 Oscar B. LAMBINO Lingayen, Pangasinan 2401 (075)542 -6011 542 -6010 536-2797 (res) 536-3172 REGION II n/a Constante A.CASTILLEJOS Basco, Batanes 3900 0917 -4203908 (02)927 -2393 Oscar T. PAGULAYAN Tuguegarao, Cagayan 3500 (078)844 -1248 844 -2293 844-5473 844-1064 RAMON M. REYES * Ilagan, Isabela 3300 (078)622 -2672 622 -2672 622-3059 624-2671 JOSE GAMBITO * Bambang, Nueva Vizcaya 3709 (078)805 -7956 805 -7956 DIRECTORY OF MEMBERS 2004-2007 Page 1 DIRECTORY OF MEMBERS 2004-2007 NAME ADDRESS TEL. NOS. FAX NOS. n/a Dakila E. CUA Cabarruguis, Quirino 3400 (078)692 -5060 692 -5038 692-5088692-5011 692-5060 CORDILLERA ADMINSTRATIVE REGION (CAR) Jaime A. LO Bangued, Abra 2800 (074)752 -8146 757 -7769 752-8148 n/a PAUL DELWASEN Kabugao, Apayao 3809 (074)872 -2218 n/a CRESCENCIOPACALSO * La Trinidad, Benguet 2601 (074)422 -2046 422 -2046 422-2004 glenn PRUDENCIANO * Lagawe, Ifugao 3600 (074)382 -2111 382 -2108 382-2109 ROMMEL DIASEN * Tabuk, Kalinga 3800 (074)872 -2367 872 -2367 0912-3884738 BENJAMIN M.DOMINGUEZ * Bontoc, Mt. Province 2616 ((074)602 -1120 602 -1016 602-1036 REGION III Annabelle C.TANGSON Baler, Aurora 3200 (042)209 -4291 209 -4211 209-4213 (02)931-5435 DIRECTORY OF MEMBERS 2004-2007 Page 2 DIRECTORY OF MEMBERS 2004-2007 NAME ADDRESS TEL. -

PDRRMO-Antique in an Interview Last October 19, 2020, Mr

STAFF BOX Editor-in-Chief EDITORIAL Junlee M. Saylo Associate Editor These past two months proved the resiliency of the Antiquenos. Danny C. Atienza While the province and the rest of the country is still struggling with the pandemic, earthquakes shook and typhoons inundated many places in the Philippines, and some parts of Antique were also affected. Photo Editor Ike Decena Nonetheless, no worst scenario was recorded. Staff Writers In these unseemly malevolent manifestations of nature, humanity Andrei Anthony Aganio find ways to adjust and go on with what it considers as the normal way Arnie Barcebal of life. Scientific studies tells how man wielded his mental power to create Kathy Lavega technology and harness the things he found in his environment to make his Irish Manlapaz life easy and things to go as he wills. To increase his food supply he made Macky Torrechilla irrigation, to travel farther and easier he made cars and planes, to protect AJ Patrick Gaan himself from the elements he made houses and clothing, to protect himself from predators and his fellow he made armors and weapons, and so on. Photographers Man always find ways to survive and to, eventually, thrive. Janrey Dungganon Felizardo Dismondo Garfield Heñosa This is true to every Antiqueno, we don’t cower, we press on no matter how difficult the situation maybe. Our tenacity in the face of peril is our heritage form our noble lineage. We are the Lay-out Artists offsprings of brave datus and noble atis. Though the pandemic has Ken Estares pushed us back in our quest for progress and development, we Jeron Nietes refused to hide. -

Talaan Ng Mga Nilalaman

TALAAN NG MGA NILALAMAN I. ANG PAMAHALAANG PAMBANSA A. SANGAY TAGAPAGPAGANAP Tanggapan ng Pangulo 3 Tanggapan ng Pangalawang Pangulo 6 Tanggapang Pampanguluhan sa Operasyong Pangkomunikasyon 7 Iba Pang Tanggapang Tagapagpaganap 9 Kagawaran ng Repormang Pansakahan 14 Kagawaran ng Agrikultura 17 Kagawaran ng Badyet at Pamamahala 22 Kagawaran ng Edukasyon 29 Kagawaran ng Enerhiya 34 Kagawaran ng Kapaligiran at Likas na Yaman 36 Kagawaran ng Pananalapi 41 Kagawaran ng Ugnayang Panlabas 44 Kagawaran ng Kalusugan 54 Kagawaran ng Teknolohiyang Pang-impormasyon at Komunikasyon 60 Kagawaran ng Interyor at Pamahalaang Lokal 62 Kagawaran ng Katarungan 66 Kagawaran ng Paggawa at Empleo 70 Kagawaran ng Tanggulang Pambansa 74 Kagawaran ng mga Pagawaing Bayan at Lansangan 77 Kagawaran ng Agham at Teknolohiya 80 Kagawaran ng Kagalingang Panlipunan at Pagpapaunlad 86 Kagawaran ng Turismo 91 Kagawaran ng Kalakalan at Industriya 94 Kagawaran ng Transportasyon 99 Pambansang Pangasiwaan sa Kabuhayan at Pagpapaunlad 102 Mga Tanggapang Konstitusyonal l Komisyon sa Serbisyo Sibil 109 l Komisyon sa Awdit 111 l Komisyon sa Halalan 114 l Komisyon sa Karapatang Pantao 116 l Tanggapan ng Tanodbayan 118 Mga Korporasyong Pag-aari at/o Kontrolado ng Pamahalaan 123 Mga Pampamahalaang Unibersidad at Kolehiyo 134 B. SANGAY TAGAPAGBATAS Senado ng Pilipinas 153 Kapulungan ng mga Kinatawan 158 C. SANGAY HUDIKATURA Kataas-Taasang Hukuman ng Pilipinas 173 Hukuman ng Apelasyon 174 Hukuman ng Apelasyon sa Buwis 176 Sandiganbayan 177 II. MGA PAMAHALAANG LOKAL Mga Pamahalaang Panlalawigan 181 Mga Pamahalaang Panlungsod 187 Mga Pamahalaang Pambayan 195 Rehiyong Awtonomo sa Muslim Mindanao 248 III. MGA MISYONG DIPLOMATIKO AT KONSULADO 255 IV. MGA AHENSIYA NG NAGKAKAISANG BANSA AT 283 IBA PANG PANDAIGDIGANG ORGANISASYON SANGAY TAGAPAGPAGANAP SANGAY TAGAPAGPAGANAP Ang Sangay Tagapagpaganap ay nagsasakatuparan ng mga pambansang patakaran at nagtataguyod ng mga tungkuling pang- ehekutibo at pampangasiwaan ng Pambansang Pamahalaan. -

Republic of the Philippines Department of Health NATIONAL NUTRITION COUNCIL Region VI Iloilo Provincial Library Luna St., La Paz, Iloilo City

Republic of the Philippines Department of Health NATIONAL NUTRITION COUNCIL Region VI Iloilo Provincial Library Luna St., La Paz, Iloilo City 2018 DIRECTORY GOVERNOR PNAO DNPC AKLAN Dr. Victor A. Santamaria Crescini S. Roxas Florencio T. Miraflores Provincial Health Officer II Nutritionist-Dietitian II (Area code: 036) 268-5626 09106827756 262-3132 268-8679 268-5626 268- 8579 [email protected] ANTIQUE Dr. Leoncio Q. Abierra, Jr. Jocelyn N. Morano Rhodora Cadiao Medical Specialist II Nutritionist-Dietitian II (Area Code: 036) PHO 09293862914 540-8198 540-7054 540-9649 CAPIZ Dr. Leah L. Del Rosario Ma. Divina Bigcas Antonio A. Del Rosario Provincial Health Officer I Nutrition Officer III (Area Code: 036) 09478922275 09198641335 621-0595 Fax 621-0629 621-0042 620-1257 621-0629/6210595 GUIMARAS Dr. N.L. Cathrel Nava Delia G. Hernando Dr. Samuel T. Gumarin Provincial Health Officer II Nutritionist Dietitian II (Area Code: 033) 581-2033 09182955718 581-3349 (Telefax) 09985456545 237-1111 (Fax) 581-2057 581-2114 ILOILO Dr. Maria Socorro C. Quinon, Noniza Lozada Arthur D. Defensor Sr. PHO I Nutritionist Dietitian II (Area Code: 033) Dr. Patricia Grace Trabado, 09202534007 337-4230 PHOII/ECCD Focal Person 336-3669 509-3560 (Fax) 335-1887 (Tel.) 335-1889 (PHO) NEGROS OCCIDENTAL Dr. Ernell Tumimbang, PHO II Zarina Zara Z. Zafra Alfredo G. Maranon Jr. 432-3362 (Fax - PHO) Nurse I (Area Code: 034) 441-2865 09998812732 432-3362 (Admin) 433-3699 [email protected] Republic of the Philippines Department of Health NATIONAL NUTRITION COUNCIL Region VI Iloilo Provincial Library Luna St., La Paz, Iloilo City 2018 DIRECTORY MAYOR CNAO CNPC BAGO CITY Dr.