Industry Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

* This Document Is Important and Requires Your

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in doubt as to any aspect of this document, you should consult your licensed securities dealer, bank manager, Sch I front page solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Henderson China Holdings Limited, you should at once hand this document and the accompanying forms of proxy to the purchaser or transferee or to the bank, licensed securities dealer or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this document, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. * (Stock Code: 0246) PROPOSED PRIVATISATION BY BY WAY OF A SCHEME OF ARRANGEMENT (UNDER SECTION 99 OF THE COMPANIES ACT 1981 OF BERMUDA) INVOLVING THE CANCELLATION OF ALL THE ISSUED SHARES OF HK$1.00 EACH IN HENDERSON CHINA HOLDINGS LIMITED HELD BY THE SCHEME SHAREHOLDERS (AS DEFINED HEREIN) Financial Adviser to Henderson Land Development Company Limited Sch I Para 1 Independent financial adviser to the Independent Board Committee (as defined herein) of Henderson China Holdings Limited A letter from the board of directors of Henderson China Holdings Limited is set out on pages 8 to 17 of this document. An explanatory statement regarding the Proposal (as defined herein) is set out on pages 46 to 63 of this document. -

Three Red Lines” Policy

Real Estate Developers with High Leverage to See Inventory Quality Tested Under Broader “Three Red Lines” Policy October 28, 2020 In our view, the widening of regulations aimed at controlling real estate developers’ interest- ANALYSTS bearing debt would further reduce the industry’s overall credit risk in the long term. However, the nearer term may see less headroom for highly leveraged developers to finance in the capital Xiaoliang Liu, CFA market, pushing them to sell off inventory to ease liquidity pressure. Beijing +86-10-6516-6040 The People’s Bank of China said in September that measures aimed at monitoring the funding [email protected] and financial management of key real estate developers will steadily be expanded. Media reports suggest that the new regulations would see a cap of 15% on annual growth of interest-bearing Jin Wang debt for all property developers. Developers will be assessed against three indicators, which are Beijing called “red lines”: whether asset liability ratios (excluding advance) exceeded 70%; whether net +86-10-6516-6034 gearing ratio exceeded 100%; whether cash to short-term debt ratios went below 1.0. Developers [email protected] which breached all three red lines won’t be allowed to increase their debt. If only one or two of the red lines are breached, such developers would have their interest-bearing debt growth capped at 5% and 10% respectively. The first half of the year saw debt grow rapidly among developers. In a sample of 87 real estate developers that we are monitoring, more than 40% saw their interest-bearing debt grow at a faster rate than 15% year over year as of the end of June (see the chart below). -

ANNUAL REPORT ADDITIONAL INFORMATION All Figures in This Document Are Expressed in Canadian Dollars, Unless Otherwise Indicated

2009 ANNUAL REPORT ADDITIONAL INFORMATION All figures in this document are expressed in Canadian dollars, unless otherwise indicated. This publication, as well as the 2009 Annual Report, are available at www.lacaisse.com. Information: 514 842-3261 [email protected] Ce document, de même que le Rapport annuel 2009, sont disponibles en français sur www.lacaisse.com. Legal Deposit – Bibliothèque et Archives nationales du Québec, 2010 50% Annual Report 2009 – Additional Information I. Tables of returns 1. Auditors’ Report ................................................................................................. 1 2. General Notes .................................................................................................... 2 3. Short Term Investments ....................................................................................... 4 4. Real Return Bonds ............................................................................................... 6 5. Long Term Bonds ................................................................................................. 8 6. Bonds .............................................................................................................. 10 7. Bonds - Fixed Income .......................................................................................... 12 8. Canadian Equity ................................................................................................ 14 9. Publicly Traded Canadian Equity Markets ............................................................. -

The Annual Report on the Most Valuable and Strongest Real Estate Brands June 2020 Contents

Real Estate 25 2020The annual report on the most valuable and strongest real estate brands June 2020 Contents. About Brand Finance 4 Get in Touch 4 Brandirectory.com 6 Brand Finance Group 6 Foreword 8 Executive Summary 10 Brand Finance Real Estate 25 (USD m) 13 Sector Reputation Analysis 14 COVID-19 Global Impact Analysis 16 Definitions 20 Brand Valuation Methodology 22 Market Research Methodology 23 Stakeholder Equity Measures 23 Consulting Services 24 Brand Evaluation Services 25 Communications Services 26 Brand Finance Network 28 © 2020 All rights reserved. Brand Finance Plc, UK. Brand Finance Real Estate 25 June 2020 3 About Brand Finance. Brand Finance is the world's leading independent brand valuation consultancy. Request your own We bridge the gap between marketing and finance Brand Value Report Brand Finance was set up in 1996 with the aim of 'bridging the gap between marketing and finance'. For more than 20 A Brand Value Report provides a years, we have helped companies and organisations of all types to connect their brands to the bottom line. complete breakdown of the assumptions, data sources, and calculations used We quantify the financial value of brands We put 5,000 of the world’s biggest brands to the test to arrive at your brand’s value. every year. Ranking brands across all sectors and countries, we publish nearly 100 reports annually. Each report includes expert recommendations for growing brand We offer a unique combination of expertise Insight Our teams have experience across a wide range of value to drive business performance disciplines from marketing and market research, to and offers a cost-effective way to brand strategy and visual identity, to tax and accounting. -

For Personal Use Only Use Personal For

13 November 2014 Norton Rose Fulbright Australia ABN 32 720 868 049 Level 15, RACV Tower 485 Bourke Street MELBOURNE VIC 3000 AUSTRALIA Tel +61 3 8686 6000 Company Announcements Fax +61 3 8686 6505 Australian Securities Exchange GPO Box 4592, Melbourne VIC 3001 Level 2 120 King Street DX 445 Melbourne MELBOURNE VIC 3000 nortonrosefulbright.com Direct line +61 3 8686 6710 Email [email protected] Our reference: 2813782 Dear Sir/Madam Takeover bid by Transcendent Resources Limited for Roc Oil Company Limited (ROC) – interests of substantial holder We act for Transcendent Resources Limited ( Fosun ) and its associated companies and controllers, which includes Fosun International Limited ( Fosun Parties ) in relation to Fosun’s off-market takeover bid for all of the ordinary shares in Roc Oil Company Limited ( ROC ). On behalf of the Fosun Parties and in accordance with section 671B of the Corporations Act 2001 (Cth), we enclose a notice of change of interests of substantial holder in respect of ROC ( Form 604 ). This notice will be provided to ROC today. Yours faithfully James Stewart Partner Norton Rose Fulbright Australia Encl. For personal use only APAC-#24924633-v1 Norton Rose Fulbright Australia is a law firm as defined in the Legal Profession Acts of the Australian states and territory in which it practises. Norton Rose Fulbright Australia, Norton Rose Fulbright LLP, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP, each of which is a separate legal entity, are members of Norton Rose Fulbright Verein, a Swiss Verein. -

China Equity Strategy

June 5, 2019 09:40 AM GMT MORGAN STANLEY ASIA LIMITED+ China Equity Strategy | Asia Pacific Jonathan F Garner EQUITY STRATEGIST [email protected] +852 2848-7288 The Rubio "Equitable Act" - Our Laura Wang EQUITY STRATEGIST [email protected] +852 2848-6853 First Thoughts Corey Ng, CFA EQUITY STRATEGIST [email protected] +852 2848-5523 Fran Chen, CFA A new bill sponsored by US Senator Marco Rubio has the EQUITY STRATEGIST potential to cause significant change in the listing domains of [email protected] +852 2848-7135 Chinese firms. After the market close in the US yesterday 4th June the Wall Street Journal published an Op-Ed by US Senator Marco Rubio in which he announced that he intends to sponsor the “Equitable Act” – an acronym for Ensuring Quality Information and Transparency for Abroad-Based Listings on our Exchanges. At this time the text of the bill has not been published and we are seeking additional information about its contents and likelihood of passing. However, our early reaction is that this has the potential to cause significant changes in the domain for listings of Chinese firms going forward with the potential for de- listing of Chinese firms on US exchanges and re-listing elsewhere (most likely Hong Kong). More generally we see this development as part of an increased escalation of tensions between China and the US on multiple fronts which should cap the valuation multiple for China equities, in particular in the offshore index constituents and US-listed parts of the universe. We provide a list of the potentially impacted China / HK names with either primary or secondary listings on Amex, NYSE or Nasdaq. -

Sustainability Development Work Sustainability Development Work

2019 Shimao Group Holdings Limited Sustainability Report Chairman's Message Chairman's Message Harmonic co-existence and empowered development Invest in philanthropy and conserve cultural legacy In 2019, due to the advantage of diverse business and investment Over the years, Shimao adheres its originality and takes social planning in advance, Shimao shifted from the role of city operator responsibility. At present, Shimao is actively engaged in philanthropic to the role of city empowerment, the core of which is framework of sectors, such as cultural inheritance, medical assistance for poverty Big Plane Strategy: body is the property development; wings are the alleviation, community care, life illumination, etc. commercial office, property management, hotel operation, culture and Chairman's Message entertainment; stabilizers are high technology, healthcare, education, In 2019, Shimao continued to invest into the conservation of cultural elder care, finance and etc. The rapid-moving Big Plane will power up legacy and integrated Chinese cultural IP into products and service through those components, injecting the power into the sustainable of Shimao, energizing traditional Chinese culture in current popular development and working on high-quality and better life of people. market. From Quanzhou Shimao • The Palace Museum Maritime Silk Road Museum (temporary name) to The Forbidden City Gallery • Wuyi Activating the new engine of Chinese economy and attracting Mountain Branch, Shimao keeps exploring and practicing and shifted worldwide attention -

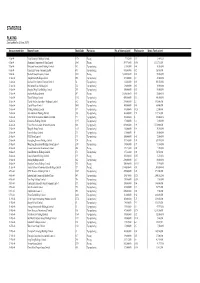

PLACING (Last Updated on 22 June 2007)

STATISTICS PLACING (Last updated on 22 June 2007) Announcement date Name of issuer Stock Code Particulars No. of shares placed Placing price Gross Funds raised (HK$) 5-Jan-04 Vitop Bioenergy Holdings Limited 1178 Placing 7,752,000 0.31 2,403,120 6-Jan-04 Aluminum Corporation of China Limited 2600 Placing 549,976,000 5.658 3,111,764,208 7-Jan-04 Perfectech International Holdings Limited 765 Top-up placing 21,000,000 0.68 14,280,000 8-Jan-04 China Eagle Group Company Limited 493 Top-up placing 473,000,000 0.12 56,760,000 9-Jan-04 Medtech Group Company Limited 1031 Placing 5,000,000,000 0.01 50,000,000 12-Jan-04 Tongda Group Holdings Limited 698 Top-up placing 227,500,000 0.2 45,500,000 13-Jan-04 Kowloon Development Company Limited 34 Top-up placing 83,000,000 6.85 568,550,000 13-Jan-04 Millennium Sense Holdings Ltd 724 Top-up placing 30,000,000 0.63 18,900,000 13-Jan-04 Shanghai Ming Yuan Holdings Limited 233 Top-up placing 100,000,000 0.55 55,000,000 13-Jan-04 Starbow Holdings Limited 397 Placing 2,000,000,000 0.01 20,000,000 13-Jan-04 Titan (Holdings) Limited 1192 Top-up placing 450,000,000 0.92 414,000,000 15-Jan-04 Chaoda Modern Agriculture (Holdings) Limited 682 Top-up placing 280,000,000 2.5 683,000,000 15-Jan-04 Capital Prosper Limited 1003 Top-up placing 140,000,000 0.05 68,000,000 15-Jan-04 Paliburg Holdings Limited 617 Top-up placing 180,000,000 0.128 22,500,000 15-Jan-04 Asia Aluminum Holdings Limited 930 Top-up placing 332,000,000 1.56 517,920,000 15-Jan-04 Silver Grant International Industries Limited 171 Top-up placing 165,000,000 -

U.S. Investors Are Funding Malign PRC Companies on Major Indices

U.S. DEPARTMENT OF STATE Office of the Spokesperson For Immediate Release FACT SHEET December 8, 2020 U.S. Investors Are Funding Malign PRC Companies on Major Indices “Under Xi Jinping, the CCP has prioritized something called ‘military-civil fusion.’ … Chinese companies and researchers must… under penalty of law – share technology with the Chinese military. The goal is to ensure that the People’s Liberation Army has military dominance. And the PLA’s core mission is to sustain the Chinese Communist Party’s grip on power.” – Secretary of State Michael R. Pompeo, January 13, 2020 The Chinese Communist Party’s (CCP) threat to American national security extends into our financial markets and impacts American investors. Many major stock and bond indices developed by index providers like MSCI and FTSE include malign People’s Republic of China (PRC) companies that are listed on the Department of Commerce’s Entity List and/or the Department of Defense’s List of “Communist Chinese military companies” (CCMCs). The money flowing into these index funds – often passively, from U.S. retail investors – supports Chinese companies involved in both civilian and military production. Some of these companies produce technologies for the surveillance of civilians and repression of human rights, as is the case with Uyghurs and other Muslim minority groups in Xinjiang, China, as well as in other repressive regimes, such as Iran and Venezuela. As of December 2020, at least 24 of the 35 parent-level CCMCs had affiliates’ securities included on a major securities index. This includes at least 71 distinct affiliate-level securities issuers. -

Shanghai Forte Land Co., Ltd.*

14.63(2)(c) THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt about this circular or as to the action to be taken, you should consult your stockbroker, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Shanghai Forte Land Co., Ltd.*, you should at once hand this circular to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchange and Clearing Limited and The Stock Exchange of Hong Kong Limited take no 14.58(1) responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. App1B1 SHANGHAI FORTE LAND CO., LTD.* (a sino-foreign joint stock company incorporated in the People’s Republic of China with limited liability) 13.51A (Stock Code: 02337) MAJOR TRANSACTION ACQUISITION OF THE ENTIRE ISSUED QUOTAS IN THE CAPITAL OF GARDEN PLAZA CAPITAL SRL A letter from the Board is set out on pages 5 to 10 of this circular. * For identification purpose only 25 June 2010 CONTENTS pages Definitions ............................................................... 1 Letter from the Board ..................................................... 5 Appendix I — Financial Information of the Group .......................... I-1 Appendix II — Financial information of the Target Group .................... II-1 Appendix III — Unaudited pro forma financial information of the Enlarged Group ...................................III-1 Appendix IV — Valuation Report .........................................IV-1 Appendix V — General Information ..................................... -

Xinyuan Real Estate Co., Ltd

FORM 6-K SECURITIES AND EXCHANGE COMMISSION Washington D.C. 20549 REPORT OF FOREIGN ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 OF THE SECURITIES EXCHANGE ACT OF 1934 For the month of December 2008 Commission File Number: 001-33863 XINYUAN REAL ESTATE CO., LTD. 27/F, China Central Place, Tower II 79 Jianguo Road, Chaoyang District Beijing 100025 People’s Republic of China (Address of principal executive offices) Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F. Form 20-F Form 40-F o Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): o Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): o Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934. Yes o No If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82- N/A TABLE OF CONTENTS Page Signature 4 Exhibit Index 5 EX-99.1 Press Release regarding acquiring New York city development site 2 Acquiring New York City Development Site Xinyuan Real Estate Co., Ltd. (“Xinyuan”) (NYSE: XIN), a residential real estate developer with a focus on high growth, strategic cities in China, today announced that its U.S. -

CEBI Research China Property

CEBI Research China Property Sector Report ─ China Property Fine tuning policy yet to boost sales volume ñ Housing policy shows signal of relaxation especially after Local’s Dominic Chan Two sessions Senior Equity Analyst ñ Debt financing surged with lower funding cost in Jan 2019, [email protected] reflecting a loose credit conditions. (852) 2916-9631 ñ Relatively stable in RMB currency YTD ñ Chinese property companies met its 2018 sales target, but home sales growth is likely to slow down in 2019 27 Feb 2019 ñ Maintain our bullish view on COLI (688 HK) and Logan Property (3380 HK) More fine tuning policies to come: China property sector continued to rebound in 2019. During the working conference held by Ministry of Housing and Urban-Rural Development of China by the end of 2018, the ministry highlighted 10 key tasks in 2019, including stabilize home and land prices in 2019. Meanwhile, more cities announced fine-tuning policies on property market, we expect more to come in the near future. Debt refinancing surged by 90% in Jan2019: As per our Key Data previous report, debt repayment for China property companies Avg.19 E P/E (x) 5.88 Avg.19E P/B (x) 1.32 will soar from 2019 to 2021. However, China property succeed to Avg.18 E Dividend Yield (%) 5.20 raise money by debt refinancing in recent months. According to Source: Bloomberg, CEBI the data of CRIC,the amount of debt issuance in Jan2019 was Rmb109.6bn, surged by 91.8% MoM. RMB appreciated against US dollars: As developers are Sector Performance (%) having a high level of foreign-denominated debt, RMB 1-mth 7.6 depreciation will weigh on their profitabilities and cash flows.