Annual Report 2019 Promoting the Big Screen

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Cinema Media Guide 2017

Second Edition THE CINEMA MEDIA GUIDE 2017 1 WELCOME TO OUR WORLD CONTENTS. Our vision 1 ABC1 Adults 41 Foreword 2 War for the Planet of the Apes 43 Fast facts 3 Dunkirk 44 The cinema audience 5 American Made 45 The WOW factor 6 Victoria and Abdul 46 Cinema’s role in the media mix 7 Goodbye Christopher Robin 47 Building Box Office Brands 8 Blade Runner 2049 48 The return on investment 9 The Snowman 49 How to buy 11 Murder on the Orient Express 50 Buying routes 12 Suburbicon 51 Optimise your campaign 16 16-34 Men 53 Sponsorship opportunities 17 Spider-Man: Homecoming 55 The production process 19 Atomic Blonde 56 Our cinemas 21 The Dark Tower 57 Our cinema gallery 22 Kingsman: The Golden Circle 58 Cineworld 23 Thor: Ragnarok 59 ODEON 24 Justice League 60 Vue 25 16-34 Women 61 Curzon Cinemas 26 The Beguiled 63 Everyman Cinemas 27 It 64 Picturehouse Cinemas 28 Flatliners 65 Independents 29 A Bad Mom’s Christmas 66 2017 films by audience Mother! 67 Coming soon to a cinema near you 31 Pitch Perfect 3 68 Adults 33 Main Shoppers with Children 69 Valerian and the City of Cars 3 71 a Thousand Planets 35 Captain Underpants: The First Epic Movie 72 Battle of the Sexes 36 The LEGO Ninjago Movie 73 Paddington 2 37 My Little Pony: The Movie 74 Daddy’s Home 2 38 Ferdinand 75 Star Wars: The Last Jedi 39 Coming in 2018 77 Jumanji: Welcome to the Jungle 40 OUR VISION. FOREWORD. -

CE2018 Schedule of Events.Indd

SCHEDULE OF EVENTS OFFICIAL CORPORATE SPONSOR 11-14 JUNE 2018 • BARCELONA WELCOME TO CINEEUROPE This is your official schedule of events for CineEurope 2018. NOTE: The schedule of events no longer grants access to events. The Access Pass replaces the passport and must be shown to gain entry to CineEurope events. Lost or stolen Access Passes will not be replaced and are non-transferable. IMPORTANT NOTICE FOR TICKETED DELEGATES Security continues to be a major initiative at all CineEurope screenings. In order to maintain and protect the integrity of all films and product reels screened, we kindly advise that the use of mobile phones or any other kind of photo or video recording equipment is strictly prohibited in the Auditorium. To further protect product being shown we will also have security personnel at each event utilizing night-vision goggles. Anyone caught using any type of recording device will have their Access Pass confiscated and will be escorted out of the Auditorium. Due to increased security at all screenings, large bags are subject to search upon arrival at the theatre. We ask that none of the films screened or product featured are reviewed or commented on—regardless of good or bad. Please note, this includes speaking to members of the press, personal and professional blogs, social networking sites like Facebook, Snapchat, Instagram, LinkedIn, Twitter, or likewise. Also, please do not take photos of celebrities on the stage. We appreciate your cooperation and understanding of this matter. ENJOY THE SHOW! SCHEDULE OF EVENTS - 11-14 JUNE 2018 Official Corporate Sponsor *Grab a complimentary beverage in the Auditorium Foyer prior to each studio presentation. -

A Filmmakers' Guide to Distribution and Exhibition

A Filmmakers’ Guide to Distribution and Exhibition A Filmmakers’ Guide to Distribution and Exhibition Written by Jane Giles ABOUT THIS GUIDE 2 Jane Giles is a film programmer and writer INTRODUCTION 3 Edited by Pippa Eldridge and Julia Voss SALES AGENTS 10 Exhibition Development Unit, bfi FESTIVALS 13 THEATRIC RELEASING: SHORTS 18 We would like to thank the following people for their THEATRIC RELEASING: FEATURES 27 contribution to this guide: PLANNING A CINEMA RELEASE 32 NON-THEATRIC RELEASING 40 Newton Aduaka, Karen Alexander/bfi, Clare Binns/Zoo VIDEO Cinemas, Marc Boothe/Nubian Tales, Paul Brett/bfi, 42 Stephen Brown/Steam, Pamela Casey/Atom Films, Chris TELEVISION 44 Chandler/Film Council, Ben Cook/Lux Distribution, INTERNET 47 Emma Davie, Douglas Davis/Atom Films, CASE STUDIES 52 Jim Dempster/bfi, Catharine Des Forges/bfi, Alnoor GLOSSARY 60 Dewshi, Simon Duffy/bfi, Gavin Emerson, Alexandra FESTIVAL & EVENTS CALENDAR 62 Finlay/Channel 4, John Flahive/bfi, Nicki Foster/ CONTACTS 64 McDonald & Rutter, Satwant Gill/British Council, INDEX 76 Gwydion Griffiths/S4C, Liz Harkman/Film Council, Tony Jones/City Screen, Tinge Krishnan/Disruptive Element Films, Luned Moredis/Sgrîn, Méabh O’Donovan/Short CONTENTS Circuit, Kate Ogborn, Nicola Pierson/Edinburgh BOXED INFORMATION: HOW TO APPROACH THE INDUSTRY 4 International Film Festival, Lisa Marie Russo, Erich BEST ADVICE FROM INDUSTRY PROFESSIONALS 5 Sargeant/bfi, Cary Sawney/bfi, Rita Smith, Heather MATERIAL REQUIREMENTS 5 Stewart/bfi, John Stewart/Oil Factory, Gary DEALS & CONTRACTS 8 Thomas/Arts Council of England, Peter Todd/bfi, Zoë SHORT FILM BUREAU 11 Walton, Laurel Warbrick-Keay/bfi, Sheila Whitaker/ LONDON & EDINBURGH 16 article27, Christine Whitehouse/bfi BLACK & ASIAN FILMS 17 SHORT CIRCUIT 19 Z00 CINEMAS 20 The editors have made every endeavour to ensure the BRITISH BOARD OF FILM CLASSIFICATION 21 information in this guide is correct at the time of GOOD FILMS GOOD PROGRAMMING 22 going to press. -

Thesis Final S R Perrin Pdf Version 1.Pdf

A critical analysis of the effect of copyright infringement on the UK film and cinema industries Stephen R Perrin Submitted in partial fulfilment for the degree LLM by Research School of Law University of Sheffield September 2017 ABSTRACT Film studios and major cinema operators strongly contend that copyright infringement, commonly known as piracy, is costing the worldwide industry many billions of dollars in lost revenue. A number of senior industry figures, as well as other commentators, foresee the industry’s slow death due to illegal consumption. Consequently, for the past two decades the industry has lobbied governments and legislators to provide legislation that restricts illegal online access to their product. During this period, however, the industry has witnessed significant growth in worldwide box office returns, admissions, film production investment and in the number and quality of cinema available for the exhibition of films. These two observations appear to be at odds. Arguing that film, and especially cinemas, provide socio-cultural as well as economic benefits, this thesis critically examines the industry and academic evidence pointing to the quantum of revenue loss, as well as academic evidence examining the effectiveness of the legal measures that the industry has been successful in establishing. The thesis reaches two conclusions. First, the equivocal nature of research findings regarding revenue losses suggests that estimates of infringement revenue effects appear to have been overstated. Second, the effectiveness of legal measures appears to be in doubt, with any positive effects being short-lived. However, it is argued that the equivocality of the evidence does not permit the counterfactual conclusion that the industry is totally unaffected by copyright infringement, or that legal measures are totally ineffective. -

BULLETIN Vol 50 No 1 January / February 2016

CINEMA THEATRE ASSOCIATION BULLETIN www.cta-uk.org Vol 50 No 1 January / February 2016 The Regent / Gaumont / Odeon Bournemouth, visited by the CTA last October – see report p8 An audience watching Nosferatu at the Abbeydale Sheffield – see Newsreel p28 – photo courtesy Scott Hukins FROM YOUR EDITOR CINEMA THEATRE ASSOCIATION (founded 1967) You will have noticed that the Bulletin has reached volume 50. How- promoting serious interest in all aspects of cinema buildings —————————— ever, this doesn’t mean that the CTA is 50 years old. We were found- Company limited by guarantee. Reg. No. 04428776. ed in 1967 so our 50th birthday will be next year. Special events are Registered address: 59 Harrowdene Gardens, Teddington, TW11 0DJ. planned to mark the occasion – watch this space! Registered Charity No. 1100702. Directors are marked ‡ in list below. A jigsaw we bought recently from a charity shop was entitled Road —————————— PATRONS: Carol Gibbons Glenda Jackson CBE Meets Rail. It wasn’t until I got it home that I realised it had the As- Sir Gerald Kaufman PC MP Lucinda Lambton toria/Odeon Southend in the background. Davis Simpson tells me —————————— that the dome actually belonged to Luker’s Brewery; the Odeon be- ANNUAL MEMBERSHIP SUBSCRIPTIONS ing built on part of the brewery site. There are two domes, marking Full Membership (UK) ................................................................ £29 the corners of the site and they are there to this day. The cinema Full Membership (UK under 25s) .............................................. £15 Overseas (Europe Standard & World Economy) ........................ £37 entrance was flanked by shops and then the two towers. Those Overseas (World Standard) ........................................................ £49 flanking shops are also still there: the Odeon was demolished about Associate Membership (UK & Worldwide) ................................ -

View Annual Report

2016 ANNUAL REPORT CONTENT MESSAGES FROM THE SUPERVISORY BOARD AND THE MANAGEMENT BOARD 02 1 4 Profile of the Group and its Businesses | Financial Report | Statutory Auditors’ Report Financial Communication, Tax Policy on the Consolidated Financial Statements | and Regulatory Environment | Risk Factors 05 Consolidated Financial Statements | 1. Profi le of the Group and its Businesses 07 Statutory Auditors’ Report on 2. Financial Communication, Tax policy and Regulatory Environment 43 the Financial Statements | Statutory 3. Risk Factors 47 Financial Statements 183 Selected key consolidated fi nancial data 184 I - 2016 Financial Report 185 II - Appendix to the Financial Report: Unaudited supplementary fi nancial data 208 2 III - Consolidated Financial Statements for the year ended December 31, 2016 210 Societal, Social and IV - 2016 Statutory Financial Statements 300 Environmental Information 51 1. Corporate Social Responsibility (CSR) Policy 52 2. Key Messages 58 3. Societal, Social and Environmental Indicators 64 4. Verifi cation of Non-Financial Data 101 5 Recent Events | Forecasts | Statutory Auditors’ Report on EBITA forecasts 343 1. Recent Events 344 2. Forecasts 344 3 3. Statutory Auditors’ Report on EBITA forecasts 345 Information about the Company | Corporate Governance | Reports 107 1. General Information about the Company 108 2. Additional Information about the Company 109 3. Corporate Governance 125 6 4. Report by the Chairman of Vivendi’s Supervisory Board Responsibility for Auditing the Financial Statements 347 on Corporate Governance, Internal Audits and Risk 1. Responsibility for Auditing the Financial Statements 348 Management – Fiscal year 2016 172 5. Statutory Auditors’ Report, Prepared in Accordance with Article L.225-235 of the French Commercial Code, on the Report Prepared by the Chairman of the Supervisory Board of Vivendi SA 181 ANNUAL REPORT 2016 ANNUAL REPORT 2016 The Annual Report in English is a translation of the French “Document de référence” provided for information purposes. -

The Changing Meanings of the 1930S Cinema in Nottingham

FROM MODERNITY TO MEMORIAL: The Changing Meanings of the 1930s Cinema in Nottingham By Sarah Stubbings, BA, MA. Thesis submitted to the University of Nottingham for the degree of Doctor of Philosophy, August 2003 c1INGy G2ýPF 1sinr Uß CONTENTS Abstract Acknowledgements ii Introduction 1 PART ONE: CONTEMPORARY REPORTING OF THE 1930S CINEMA 1. Contested Space, Leisure and Consumption: The 1929 36 Reconstruction of the Market Place and its Impact on Cinema and the City 2. Luxury in Suburbia: The Modern, Feminised Cinemas of 73 the 1930s 3. Selling Cinema: How Advertisements and Promotional 108 Features Helped to Formulate the 1930s Cinema Discourse 4. Concerns Over Cinema: Perceptions of the Moral and 144 Physical Danger of Going to the Pictures PART TWO: RETROSPECTIVECOVERAGE OF THE 1930S CINEMA 5. The Post-war Fate of the 1930s Cinemas: Cinema Closures - 173 The 1950s and 1960s 6. Modernity and Modernisation: Cinema's Attempted 204 Transformation in the 1950s and 1960s 7. The Continued Presence of the Past: Popular Memory of 231 Cinema-going in the 'Golden Age' 8. Preserving the Past, Changing the Present? Cinema 260 Conservation: Its Context and Meanings Conclusion 292 Bibliography 298 ABSTRACT This work examines local press reporting of the 1930s cinema from 1930 up to the present day. By focusing on one particular city, Nottingham, I formulate an analysis of the place that cinema has occupied in the city's history. Utilising the local press as the primary source enables me to situate the discourses on the cinema building and the practice of cinema-going within the broader socio-cultural contexts and history of the city. -

Cineeurope 2019 Schedule of Events Sunday, 16 June 08:00

CINEEUROPE 2019 SCHEDULE OF EVENTS SUNDAY, 16 JUNE 08:00-18:00 Trade Show Registration (Booth Exhibitors Only) (Entrance C Foyer, Level 0) 14:00-18:00 Convention Registration (Entrance B Foyer, Level 0) MONDAY, 17 JUNE 07:30-18:00 Convention Registration (Entrance B Foyer, Level 0) 07:30-18:00 Trade Show Registration (Booth Exhibitors Only) (Entrance C Foyer, Level 0) 08:15-08:45 Breakfast (Foyer 1, Level 1) Sponsor: DTS:X 09:00-12:00 CineEurope Business Sessions** (Room 116-117, Level 1) (**Simultaneous Translation Provided In French, German, Spanish And Russian) An Update on Europe and a Focus on Emerging Global Markets EMERGING GLOBAL MARKETS The shape of the global cinema industry continues to change, with new regions and territories growing in importance to match long-established markets in North America and much of Europe . This session will feature two dynamic presentations featuring prominent players from two key emerging markets: Serbia and South Africa. It will provide an in-depth look into the cinema landscape in both countries, from an exhibition, distribution and production point of view, with the aim of identifying key opportunities for growth and investment. Opening Remarks: Arturo Guillén, Vice President, EMEA & India, Comscore Movies 09:00 A FOCUS ON SOUTH AFRICA Film Distribution and Exhibition: A 2019 Perspective on South Africa / Africa as an Emerging Market Presenter: Aboobaker ‘AB’ Moosa, CEO, Avalon Group 09:20 A FOCUS ON SERBIA An Introduction and Overview of the Region Presenter: Christof Papousek, Chief Financial Officer, Cineplexx 09:30 The Importance of Local Production Presenter: Dragana Tešić, Executive Manager of Continental Film 09:40 Deal-Making 101: How Distribution Works in the Region 10:00 Executive Roundtable Almost a decade after conversion to digital cinema technology brought about huge changes to the industry landscape, it could be argued that we are now seeing a "second digital revolution" that will certainly have equal - if not greater - impact. -

Cineworld/City Screen Merger Inquiry

APPENDIX A Terms of reference and conduct of the inquiry Terms of reference 1. On 30 April 2013, the OFT sent the following reference to the CC: 1. In exercise of its duty under section 22(1) of the Enterprise Act 2002 (‘the Act’) to make a reference to the Competition Commission (‘the CC’) in relation to a completed merger the Office of Fair Trading (‘the OFT’) believes that it is or may be the case that – a. a relevant merger situation has been created in that: i. enterprises carried on by or under the control of Cineworld Group plc have ceased to be distinct from enterprises carried on by or under the control of City Screen Limited; and ii. the condition specified in section 23(4) of the Act is satisfied; and b. the creation of that situation has resulted, or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods or services, including the supply of film services. 2. Therefore, in exercise of its duty under section 22 of the Act, the OFT hereby refers to the CC, for investigation and report within a period ending on 14 October 2013, on the following questions in accordance with section 35 of the Act— a. whether a relevant merger situation has been created; and b. if so, whether the creation of that situation has resulted, or may be expected to result, in a substantial lessening of competition within any market or markets in the UK for goods and services. -

Acquisition by Terra Firma Investments (GP) 2 Ltd of United Cinemas International (UK) Limited and Cinema International Corporation (UK) Limited

Acquisition by Terra Firma Investments (GP) 2 Ltd of United Cinemas International (UK) Limited and Cinema International Corporation (UK) Limited The OFT's decision on reference under section 22 given on 7 January 2005 PARTIES 1. Terra Firma Investments (GP) 2 Ltd (Terra Firma) manages a number of private equity funds. On 2 September 2004, Terra Firma acquired Odeon Equity Co. Limited (Odeon), the largest cinema exhibitor in the UK, with 95 cinemas. 2. United Cinemas International (UK) Limited and Cinema International Corporation (UK) Limited (collectively UCI) operate multiplex cinemas in the UK. Prior to the merger, UCI was the fourth largest cinema exhibitor in the UK, with 32 cinemas nation-wide. Its UK turnover in the year to 31 December 2003 amounted to £123 million. TRANSACTION 3. On 28 October 2004, Terra Firma acquired sole control of UCI through its wholly-owned subsidiaries. The transaction completed on 28 October 2004. The administrative deadline expires on 7 January 2005. JURISDICTION 4. As a result of this transaction, Terra Firma and UCI have ceased to be distinct. The UK turnover of UCI exceeds £70 million, so that the turnover test in section 23(1)(b) of the Enterprise Act 2002 (the Act) is satisfied. The OFT therefore believes that it is, or may be the case, that a relevant merger situation has been created. RELEVANT MARKET 1 Product market 5. The parties overlap in the supply of cinema exhibition services in the UK, in the acquisition of film exhibition rights from film distributors, and in the provision of facilities for film premieres. -

Anticipated Acquisition by Odeon Cinemas Limited and Cineworld Cinemas Limited of Carlton Screen Advertising Limited

Anticipated acquisition by Odeon Cinemas Limited and Cineworld Cinemas Limited of Carlton Screen Advertising Limited ME/3632/08 The OFT's decision on reference under section 33(1) given on 1 July 2008. Full text of decision published on 17 July 2008. Please note that square brackets indicate figures or text which have been deleted or replaced at the request of the parties for reasons of commercial confidentiality. PARTIES 1. Odeon Cinemas Limited (Odeon) is the UK's largest cinema operator with 108 cinemas (831 screens). Odeon is a subsidiary of Corleone Capital Limited (Corleone) and its ultimate parent company is TFCP Holdings Limited (formerly Terra Firma Capital Partners Holdings Limited), the private equity fund manager. 2. Cineworld Cinemas Limited (Cineworld) is the UK's second largest cinema operator with 72 cinemas (741 screens). It is a subsidiary of Cineworld Group plc whose main shareholder (with 46.8 per cent)1 is Blackstone Capital Partners (Cayman) IV LP. 3. Carlton Screen Advertising Limited (CSA) is a provider of cinema advertising services in the UK. It is a wholly owned subsidiary of ITV plc (ITV), a television broadcaster. 1 As of 5 February 2008. 51.2 per cent of its shares are publicly traded on the London Stock Exchange and two per cent are Management owned. 1 TRANSACTION 4. The proposed transaction will proceed by way of two separate steps. The first is the formation of a 50:50 joint venture (JV) between Odeon and Cineworld.2 The JV will be incorporated as Digital Cinema Media Limited (DCM). 5. The second step is that DCM will acquire CSA from ITV plc for £500,000. -

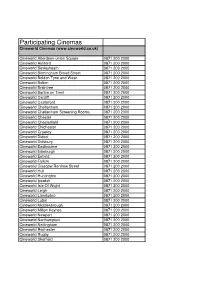

Participating Cinemas 2013 Excel

Participating Cinemas Cineworld Cinemas (www.cineworld.co.uk) Cineworld Aberdeen-union Square 0871 200 2000 Cineworld Ashford 0871 200 2000 Cineworld Bexleyheath 0871 200 2000 Cineworld Birmingham Broad Street 0871 200 2000 Cineworld Boldon Tyne and Wear 0871 200 2000 Cineworld Bolton 0871 200 2000 Cineworld Braintree 0871 200 2000 Cineworld Burton on Trent 0871 200 2000 Cineworld Cardiff 0871 200 2000 Cineworld Castleford 0871 200 2000 Cineworld Cheltenham 0871 200 2000 Cineworld Cheltenham Screening Rooms 0871 200 2000 Cineworld Chester 0871 200 2000 Cineworld Chesterfield 0871 200 2000 Cineworld Chichester 0871 200 2000 Cineworld Crawley 0871 200 2000 Cineworld Didcot 0871 200 2000 Cineworld Didsbury 0871 200 2000 Cineworld Eastbourne 0871 200 2000 Cineworld Edinburgh 0871 200 2000 Cineworld Enfield 0871 200 2000 Cineworld Falkirk 0871 200 2000 Cineworld Glasgow Renfrew Street 0871 200 2000 Cineworld Hull 0871 200 2000 Cineworld Huntington 0871 200 2000 Cineworld Ipswich 0871 200 2000 Cineworld Isle Of Wight 0871 200 2000 Cineworld Leigh 0871 200 2000 Cineworld Llandudno 0871 200 2000 Cineworld Luton 0871 200 2000 Cineworld Middlesbrough 0871 200 2000 Cineworld Milton Keynes 0871 200 2000 Cineworld Newport 0871 200 2000 Cineworld Northampton 0871 200 2000 Cineworld Nottingham 0871 200 2000 Cineworld Rochester 0871 200 2000 Cineworld Rugby 0871 200 2000 Cineworld Sheffield 0871 200 2000 Cineworld Shrewbury 0871 200 2000 Cineworld Solihull 0871 200 2000 Cineworld St Helens 0871 200 2000 Cineworld Stevenage 0871 200 2000 Cineworld Wakefield