An Olympic Legacy Lasting Or Leasting? 2–3

Total Page:16

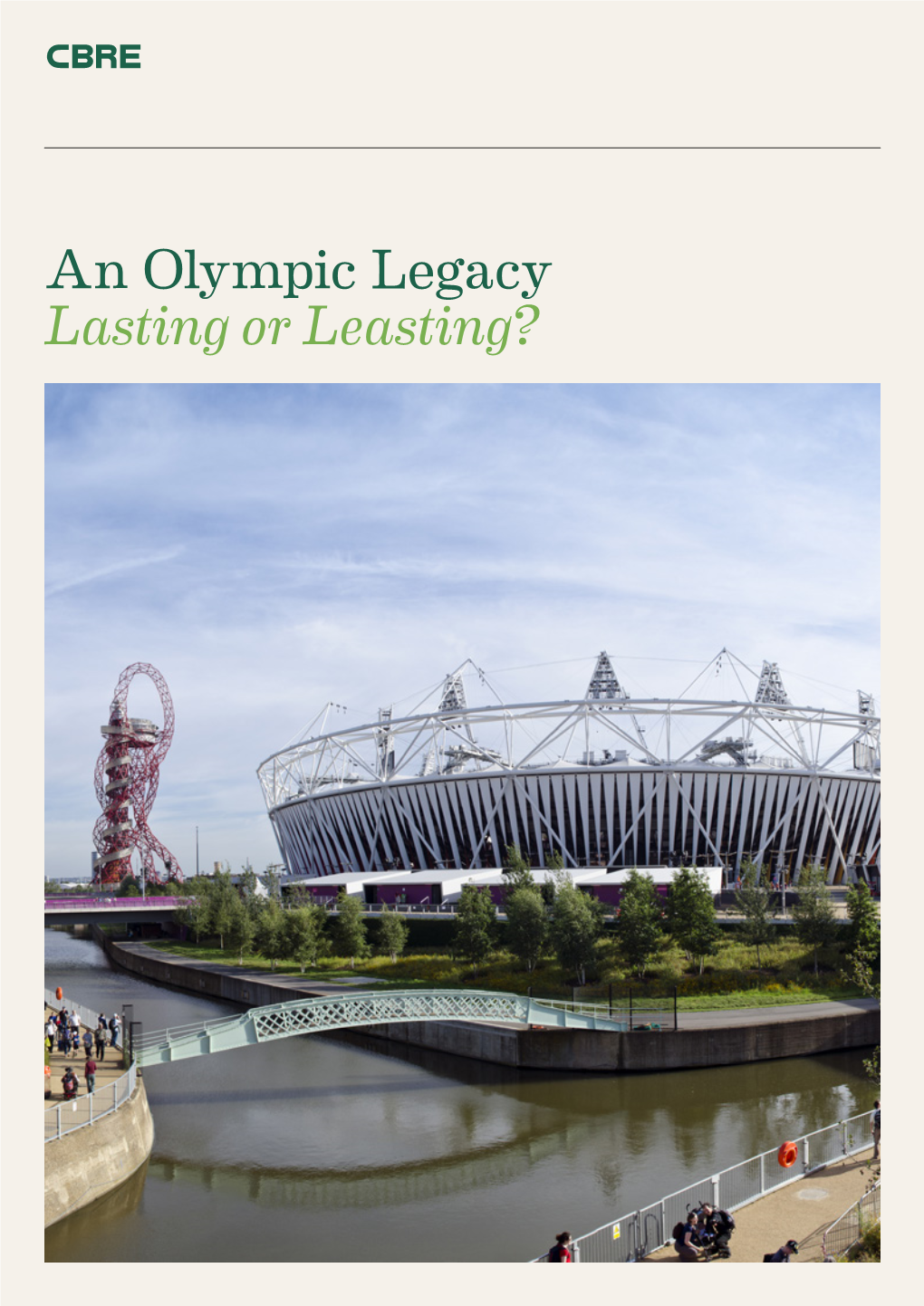

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

London 2012- Schedule by Sport

LONDON- 2012 Schedule by sport Opening Ceremony Closing Ceremony Venue: Olympic Park – Olympic Stadium Venue: Olympic Park – Olympic Stadium Dates: Friday 27 July Dates: Sunday 12 August Archery Gymnastics – Trampoline Venue: Lord’s Cricket Ground Venue: North Greenwich Arena Dates: Friday 27 July – Friday 3 August Dates: Friday 3 – Saturday 4 August Athletics Handball Venue: Olympic Park – Olympic Stadium Venue: Olympic Park – Handball Arena; Olympic Park – Dates: Friday 3 – Saturday 11 August Basketball Arena Dates: Saturday 28 July – Sunday 12 August Athletics – Marathon Hockey Venue: London Venue: Olympic Park – Hockey Centre Date: Sunday 5 and Sunday 12 August Dates: Sunday 29 July – Saturday 11 August Athletics - Race Walk Judo Venue: London Venue: ExCel Dates: Saturday 4 and Saturday 11 August Dates: Saturday 28 July – Friday 3 August Badminton Modern Pentathlon Venue: Wembley Arena Venue: Olympic Park and Greenwich Park Dates: Saturday 28 July – Sunday 5 August Dates: Saturday 11 – Sunday 12 August Basketball Rowing Venue: Olympic Park – Basketball Arena and North Venue: Eton Dorney Greenwich Arena Dates: Saturday 28 July – Saturday 4 August Dates: Saturday 28 July – Sunday 12 August Beach Volleyball Sailing Venue: Horse Guards Parade Venue: Weymouth and Portland Dates: Saturday 28 July – Thursday 9 August Dates: Sunday 29 July – Saturday 11 August Boxing Shooting Venue: ExCeL Venue: The Royal Artillery Barracks Dates: Saturday 28 July – Sunday 12 August Dates: Saturday 28 July – Sunday 5 August Canoe Slalom Swimming Venue: Lee -

Area Guide Brochure

GALLIONS POINT AT ROYAL ALBERT WHARF | E16 AREA GUIDE Photography of show home at Gallions point. SITUATED IN EAST LONDON’S ROYAL DOCKS. Gallions Point is perfectly positioned to take advantage of living in one of the world’s greatest cities. With its rich history and culture, unparalleled shopping opportunities, world-class restaurants, award-winning green spaces, and some of the world’s most iconic buildings and landmarks, the capital has it all in abundance. In this guide you’ll find just a few of the places that make London such an incredible place to live, with a list of amenities and services that we think you’ll find useful as well. Computer generated image of Gallions Point are indicative only. BLACKWELL TUNNEL START YOUR The Blackwall Tunnel is a pair of road tunnels underneath the River Thames in east ADVENTURE AT London, England linking the London Borough of Tower Hamlets with the Royal GALLIONS POINT Borough of Greenwich. EMIRATES AIR LINE Emirates Air Line crosses the River Thames between Greenwich Peninsula and the Royal Docks, just five minutes from the O2 by North Greenwich Tube station. Cabins arrive every 30 seconds and flights are approximately 10 minutes each way. SANTANDER CYCLES DLR – LONDON BIKE HIRE GALLIONS REACH BOROUGH BUSES You can hire a bike from as With the station literally London’s iconic double- little as £2. Simply download at your doorstep, your decker buses are a quick, the Santander Cycles app destination in London is convenient and cheap way or go to any docking station easily in reach. -

Smash Hits Volume 52

-WjS\ 35p USA $175 27 November -10 December I98i -HITLYRtCS r OfPER TROUPER TMCOMINgOUT EMBARRASSMENT MOTORHEAD NOT THE 9 O'CLOCK NEWS FRAMED BLONDIE PRINTS to be won 3 (SHU* Nov 27 — Dec 10 1980 Vol.2 No.24 ^gTEW^lSl TO CUT A LONG STORY SHORT Spandau Ballet 3 ELSTREE Buggies .....10 EMBARRASSMENT Madness 10 SUPER TROUPER Abba 11 I'M COMING OUT Diana Ross 17 BOURGIEBOURGIE Gladys Knight & The Pips 17 I LIKE WHAT YOU'RE DOING TO ME Young & Co ...23 WOMEN IN UNIFORM Iron Maiden 26 I COULD BE SO GOOD FOR YOU Dennis Waterman 26 SPENDING THE NIGHT TOGETHER Dr. Hook 32 LONELY TOGETHER Barry Manilow 32 TREASON The Teardrop Explodes 35 DO YOU FEEL MY LOVE Eddy Grant 38 THE CALL UP The Clash 38 LOOKING FOR CLUES Robert Palmer 47 TOYAH: Feature 4/5/6 NOT THE 9 O'CLOCK NEWS: Feature 18/19 UB40: Colour Poster 24/25 MOTORHEAD: Feature 36/37 MADNESS: Colour Poster 48 CARTOON 9 HIGHHORDSE 9 BITZ 12/13/14 INDEPENDENT BITZ 21 DISCO 22 CROSSWORD 27 REVIEWS 28/29 STAR TEASER 30 FACT IS 31 BIRO BUDDIES 40 BLONDIE COMPETITION 41 LETTERS 43/44 BADGE & CALENDAR OFFERS 44 GIGZ 46 Editor Editorial Assistants Contributors Ian Cranna Bev Hillier Robin Katz Linda Duff Red Starr Fred DeMar Features Editor David Hepworth Advertisement Manager Mike Stand Rod Sopp JiH Furmanovsky (Tel: 01-4398801) Mark Casto Design Editor Steve Taylor Assistant Steve Bush Mark Ellen Adte Hegarty Production Editor Editorial Consultant Publisher Kasper de Graaf Nick Logan Peter Strong Editorial and Advertising address: Smash Hits. -

London 2012 Venues Guide

Olympic Delivery Authority London 2012 venues factfi le July 2012 Venuesguide Contents Introduction 05 Permanent non-competition Horse Guards Parade 58 Setting new standards 84 facilities 32 Hyde Park 59 Accessibility 86 Olympic Park venues 06 Art in the Park 34 Lord’s Cricket Ground 60 Diversity 87 Olympic Park 08 Connections 36 The Mall 61 Businesses 88 Olympic Park by numbers 10 Energy Centre 38 North Greenwich Arena 62 Funding 90 Olympic Park map 12 Legacy 92 International Broadcast The Royal Artillery Aquatics Centre 14 Centre/Main Press Centre Barracks 63 Sustainability 94 (IBC/MPC) Complex 40 Basketball Arena 16 Wembley Arena 64 Workforce 96 BMX Track 18 Olympic and Wembley Stadium 65 Venue contractors 98 Copper Box 20 Paralympic Village 42 Wimbledon 66 Eton Manor 22 Parklands 44 Media contacts 103 Olympic Stadium 24 Primary Substation 46 Out of London venues 68 Riverbank Arena 26 Pumping Station 47 Map of out of Velodrome 28 Transport 48 London venues 70 Water Polo Arena 30 Box Hill 72 London venues 50 Brands Hatch 73 Map of London venues 52 Eton Dorney 74 Earls Court 54 Regional Football stadia 76 ExCeL 55 Hadleigh Farm 78 Greenwich Park 56 Lee Valley White Hampton Court Palace 57 Water Centre 80 Weymouth and Portland 82 2 3 Introduction Everyone seems to have their Londoners or fi rst-time favourite bit of London – visitors – to the Olympic whether that is a place they Park, the centrepiece of a know well or a centuries-old transformed corner of our building they have only ever capital. Built on sporting seen on television. -

Playing Rugby for Jordanhill College Rugby Football Club 1958

Playing Rugby for Jordanhill College Rugby Football Club 1958 - 1966 John Henderson ‘The Boot’ Remembers Playing Rugby for Jordanhill College RFC ‘The Boot’ Remembers When I first matriculated in October 1958 at the Scottish School of Physical Education, Jordanhill, Glasgow to undergo a three year diploma course of training in order to qualify as a teacher of Physical Education, I had no idea that some years later my senior rugby career would turn out to be as creditable as it did. Although I knew then that I was a very accurate and lengthy instep place-kicker of a rugby ball, I was under no illusion that my getting a place in the Jordanhill College Rugby Football Club top squad would be easy, nor did I have any notion then that retaining a first choice spot in the 1st XV for a good number of seasons might possibly occur. However, I was aware of the fact that graduating from College was not the end of the opportunity to play senior rugby for Jordanhill, as former students as players were not only considered eligible, but were also deemed essential in order to maintain a fighting chance for coach Bill Dickinson‟s side to compete at the highest levels possible in Scotland. Thus time was on my side, if only I was patient, and prepared to work hard at the game. But first I had, during my student days, to convince mentors Bill Dickinson and George Orr of my potential, and then, if this was accomplished, to provide consistent proof thereafter of my continuing value as a full back/three-quarter and place kicker in the top side in its annual attempts to win the Scottish Unofficial Club Championship and the Glasgow District Knock-Out Trophy. -

Textually Produced Landscape Spectacles? a Debordian Reading of Finnish Namescapes and English Soccerscapes

Textually Produced Landscape Spectacles? A Debordian Reading of Finnish Namescapes and English Soccerscapes Jani Vuolteenaho Helsinki Collegium for Advanced Studies Sami Kolamo University of Tampere In this article, a critical attempt is made to read the language of contemporary urban boosterism – its eulogistic adjectives and slogans, escapist evocations in nomenclature, nostalgic narratives, etc. – through the lens of The Society of the Spectacle (1995, orig. 1967), Guy Debord’s controversial theoretico-political manifesto. Through discussion of empirical examples, the authors shed light on different types of in-situ landscape texts in Finnish and English cities. In the former national context, culturally escapist and non-native names given to leisurescapes and technoscapes have mushroomed over the last quarter century. While this process represents a semi-hegemonic rather than hegemonic trend, many developers’ reliance on the “independent” representational power of language has substantially reshaped naming practices in the non-Anglophone country. The analysis of different types of promotional texts at England’s major soccerscapes evinces the co-presence of nostalgic evocations of local history amidst the hypercommodification of space. Arguably, the culturally self-sufficient, tradition- aware representational strategies in current English football stem from pressure from fans, the country’s status as the cradle of modern football, and a privileged possibility to promote the game’s “native” meanings via a globally-spoken language. Finally, this article addresses the pros and cons of using the spectacle theoretical framework to analyse critically language-based urban boosterism and branding under the current conditions of neoliberal urbanism. Jani Vuolteenaho, Lieven Ameel, Andrew Newby & Maggie Scott (eds.) 2012 Language, Space and Power: Urban Entanglements Studies across Disciplines in the Humanities and Social Sciences 13. -

Uefa Euro 2020 Final Tournament Draw Press Kit

UEFA EURO 2020 FINAL TOURNAMENT DRAW PRESS KIT Romexpo, Bucharest, Romania Saturday 30 November 2019 | 19:00 local (18:00 CET) #EURO2020 UEFA EURO 2020 Final Tournament Draw | Press Kit 1 CONTENTS HOW THE DRAW WILL WORK ................................................ 3 - 9 HOW TO FOLLOW THE DRAW ................................................ 10 EURO 2020 AMBASSADORS .................................................. 11 - 17 EURO 2020 CITIES AND VENUES .......................................... 18 - 26 MATCH SCHEDULE ................................................................. 27 TEAM PROFILES ..................................................................... 28 - 107 POT 1 POT 2 POT 3 POT 4 BELGIUM FRANCE PORTUGAL WALES ITALY POLAND TURKEY FINLAND ENGLAND SWITZERLAND DENMARK GERMANY CROATIA AUSTRIA SPAIN NETHERLANDS SWEDEN UKRAINE RUSSIA CZECH REPUBLIC EUROPEAN QUALIFIERS 2018-20 - PLAY-OFFS ................... 108 EURO 2020 QUALIFYING RESULTS ....................................... 109 - 128 UEFA EURO 2016 RESULTS ................................................... 129 - 135 ALL UEFA EURO FINALS ........................................................ 136 - 142 2 UEFA EURO 2020 Final Tournament Draw | Press Kit HOW THE DRAW WILL WORK How will the draw work? The draw will involve the two-top finishers in the ten qualifying groups (completed in November) and the eventual four play-off winners (decided in March 2020, and identified as play-off winners 1 to 4 for the purposes of the draw). The draw will spilt the 24 qualifiers -

Download Alto PDF Brochure

A stunning new landmark for London ALTO Alto is the high point of North West Village, located within Wembley Park, the dynamic 85 acre regeneration scheme that’s bringing new energy to this iconic London quarter. Alto’s striking towers set a new benchmark for sophisticated urban living. Beautifully designed and meticulously finished, most of the apartments have their own outdoor space or a balcony that looks across the private courtyard garden or the newly created, formal landscape of Elvin Square Gardens. Residents benefit from an exclusive concierge service and gym, whilst the larger ‘village’ offers fantastic designer shopping, as well as excellent dining and entertainment. For anyone who works in the Capital or simply loves the buzz of metropolitan life, this is an unrivalled opportunity – a chance to live in what is destined to become an icon of the London skyline, with fast and easy connections to everything this great city has to offer. Alto at Wembley Park / 3 London’s evolving architecture A NEW LANDMARK FOR LONDON Standing tall with some iconic London architecture, Alto offers a modern, elegant, new dimension to the skyline. BOND STREET THE SHARD TATE MODERN CITY HALL TOWER BRIDGE BT TOWER REGENT’S PARK WEMBLEY STADIUM ST PAUL’S THE CITY CATHEDRAL SOHO A development by Quintain Alto at Wembley Park / 5 LONDON’S VIBRANT NEW VILLAGE North West Village has a dynamism that is all its own. FRYENT COUNTRY PARK Balancing quality apartments with landscaped green spaces, its designers have created a fresh London quarter with real character, enhanced by new shops, restaurants and leisure facilities. -

London 2012 the Olympic and Paralympic Games Chief Inspector

London 2012 The Olympic and Paralympic Games Chief Inspector Chris Green Metropolitan Police Service London - UK MO6 – Public Order Branch Tokyo November 2019 Summer of 2012 - not just sporting events • Queen’s Diamond Jubilee • World Pride • Olympic and Paralympic Torch Relays • Big screens and Live Sites • Cultural celebrations and events • Music festivals • Notting Hill Carnival • Domestic sporting fixtures The Challenge The Olympic & Paralympic Games in numbers: • 27th July – 9th September 2012 • 34 venues across United Kingdom • 11 million tickets • 14,700 athletes • 205 countries represented • 21,000 media & broadcasters • 28 days of competition • 7,500 team officials & 3,000 technical officials • Peak days 14,500 Police officers deployed • Around 16,500 military played a key role • 70,000 volunteer “Games Makers” selected from 240,000 volunteers • 800,000 visitors to use public transport on busiest day! Planning principles • Needed a consistent national approach that built on what we knew worked • Locally commanded but centrally coordinated (12 of the 43 forces hosted Olympic events. 70% of events in London. Every force (52 in total) provided mutual aid) • 'Blue Games” • Roles and responsibilities were as per the normal national guidance • Threat level – Severe (actually substantial) • Sporting event with a security overlay Venues – not just London Other London Venues: Hampden Park, Glasgow Wembley Arena Earls Court ExCeL St James’s Park, Newcastle Greenwich Park Horse Guards Parade Hyde Park Lord’s Old Trafford, Manchester North -

Stadium Safety Management in England

Stadium Safety Management in England Chris Whalley, Senior Manager, Stadia Safety and Security at The Football Association, comments on the transformation that has occurred in terms of stadium safety in England. In particular, he highlights how each football club now takes responsibility for the safety of all spectators entering its stadium. English Premier League matches are broadcast all over the world. In all continents, those fans with an interest in developments off the pitch as well as on it will have noticed the splendid all-seated stadia, the lack of pitch perimeter and segregation fences and, generally, a positive atmosphere among supporters inside the stadia. But it hasn’t always been like this. Just three decades ago, English football was still blighted by the problems of supporter violence, old stadia and what we can now recognise as a lack of any safety management culture within the stadia. Two major stadium disasters in the 1980’s and a Government-led review of stadium safety brought about a programme of change which has seen the gradual transformation of English stadia and the introduction of a new system of stadium safety management. Before examining these changes in more detail, it is helpful to look at some of the problems that led to the occurrence of these major stadium disasters. Throughout the 1970’s and 1980’s, fighting between rival supporter groups was commonplace in English football stadia. From the early beginnings of football up to the late 1960’s there had been no separation of supporters in English football stadia – home and away supporters could enter any part of the stadium and generally they would stand side by side to watch the match. -

Trade Shows 2020 January 2020 the Lamma Show

Trade Shows 2020 2020 January 2020 The Lamma Show (Agricultural Machinery, Equipment and, Technology) 7-8.01.2020 National Exhibition Centre, Birmingham LAMMA is in its 38th year and is a well attended show with a large number of exhibitors (over 700) who attract 40,000 visitors across all farming sectors. As LAMMA is in the NEC again for 2020, the show will continue to be the UK's premier indoor agricultural event. LAMMA is the event “to do business” and many of those exhibiting comment on not just on the numbers of people visiting their stands, but the quality of the conversation they were having, resulting in plenty of sales and strong leads across the exhibition hall. Zetor UK will be exhibiting a range of Czech Made Tractors in Hall 18 Stand 18.500 https://www.lammashow.com/ Autosport International (incorporating the Engineering Show, the Racing Car Show and, the Performance and Tuning Show) 11-12.01.2020 (Trade and Public Days) 9-10.01.2020 (Trade Only Days) National Exhibition Centre, Birmingham The first two days are dedicated to members of the motorsport, automotive and performance engineering sectors. Featuring over 600 of the biggest and best-known exhibitors, a number of show areas and features, a dedicated business lounge and much more, the show is a hub of international business. In 2019 over 90,000 visitors attended with 30,500 of those being trade professionals. http://www.autosportinternational.com/ Top Drawer 12-14 January 2020 Olympia, London Built on over 30 years of success, Top Drawer is constantly evolving to ensure we remain the destination of choice for design-led brands and top buyers. -

Thank You for Taking the Time to Visit This Online Exhibition About Our Proposals to Expand Excel London

WELCOME Thank you for taking the time to visit this online exhibition about our proposals to expand ExCeL London. Who are ExCeL? Custom House ExCeL’s beginnings can be traced back to 1988, when Prince Regent Royal Victoria ExCeL London LBNCouncil the Association of Exhibition Organisers (AEO) first EXISTING EXISTING PROPOSED Offices PHASE1 PHASE 2 PHASE3 ridge approached architect Ray Moxley to locate and design t B Emirates Royal Albert Dock Footbridg Airline a new exhibition and conference centre within the M25. Royal Victoria Dock Connaugh The Royal Victoria Dock’s site was identified in 1990 e and we opened in November 2000 as one of Europe’s London City Airport Millennium Mills largest regeneration projects. In 2010 we opened Phase London City Airport 2 of the project, London’s International Convention West Silvertown Centre (ICC). Pontoon Dock Elizabeth line DLR ExCeL London is a global leader in exhibitions, international congresses and live events. We are owned Have your say by ADNEC (Abu Dhabi National Exhibitions Company) We are delighted to be launching the first phase and have been a part of the Royal Docks for over 20 of public consultation on the proposals. This is years. your opportunity to learn more and have your say. Our proposals We have been developing proposals for a further Email the project team at expansion of ExCeL London – which we are calling [email protected] ‘Phase 3’. This will add modern, flexible event space to the east of the existing building, creating a more vibrant dock-edge, and delivering improved public realm and pedestrian and cycling connections.