Process Analysis Paving the Way Towards a Superior Customer Experience Deloitte | Process Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Root Cause Analysis in Context of WHO International Classification for Patient Safety

Root cause analysis in context of WHO International Classification for Patient Safety Dr David Cousins Associate Director Safe Medication Practice and Medical Devices 1 NHS | Presentation to [XXXX Company] | [Type Date] How heath care provider organisations manage patient safety incidents Incident External organisation Healthcare Patient/Carer or agency professional Department of Health Incident report Complaint Regulators Health & Safety Request Risk/complaint Request additional manager additional Healthcare information information commissioners and purchasers Local analysis and learning Industry Feed back External report Root Cause AnalysisWhy RCA? (RCA) To identify the root causes and key learning from serious incidents and use this information to significantly reduce the likelihood of future harm to patients Objectives To establish the facts i.e. what happened (effect), to whom, when, where, how and why To establish whether failings occurred in care or treatment To look for improvements rather than to apportion blame To establish how recurrence may be reduced or eliminated To formulate recommendations and an action plan To provide a report and record of the investigation process & outcome To provide a means of sharing learning from the incident To identify routes of sharing learning from the incident Basic elements of RCA WHAT HOW it WHY it happened happened happened Human Contributory Unsafe Acts Behaviour Factors Direct Care Delivery Problems – unsafe acts or omissions by staff Service Delivery Problems – unsafe systems, procedures -

SPEAKER BIOS | in SPEAKING ORDER Greg Fairlie Broadcaster Dubai One Presenter, Broadcaster, Multi Tasked Video Journalist &

SPEAKER BIOS | IN SPEAKING ORDER Greg Fairlie Broadcaster Dubai One Presenter, Broadcaster, Multi tasked Video Journalist & Business Communications Expert with a wealth of experience in the UK, Australia, Europe & MENA region. Bringing a warm, personable, informative and friendly approach to presenting, interviewing and drawing out the best of people in many diverse fields. Fully experienced in a live studio environment and on location. Specialties: Facilitating business programming for both TV and Radio stations. Managing teams within a broadcast unit. Presenting, producing, directing, filming and editing live and recorded TV & Radio content. Experience of anchoring in a live environment. Specialist in media training and presentation on-air delivery. Moderator at events. Magazine and newspaper features writer. Voice Over artist and Voice imaging. Experienced in using AVID inews, Final Cut Pro X, Adobe Premiere, audio editing software including soundtrack pro and Twisted Wave. His Excellency Hani Al Hamli Secretary General Dubai Economic Council (DEC) H.E. Hani Rashid Al Hamli is the Secretary General of the Dubai Economic Council (DEC) since 2006. The Council envisioned acting as the strategic partner for the Government of Dubai in economic-decision making. It provides policy recommendations and initiatives that enhance the sustainable economic development in the Emirate of Dubai. Prior to his service at DEC, Mr. Al Hamli held a number of senior positions in various government and private entities in Dubai such as the Executive Council-Government of Dubai, Dubai Chamber of Commerce and Industry, Investment & Development Authority, and Emirates Bank Group. Under his management of the DEC Secretariat, Mr. Al Hamli has realized many achievements for the DEC, notably the establishment of Dubai Competitiveness Center (DCC) in 2008, and the DEC has embraced the stated center from 2008-2013. -

Guidance for Performing Root Cause Analysis (RCA) with Pips

Guidance for Performing Root Cause Analysis (RCA) with Performance Improvement Projects (PIPs) Overview: RCA is a structured facilitated team process to identify root causes of an event that resulted in an undesired outcome and develop corrective actions. The RCA process provides you with a way to identify breakdowns in processes and systems that contributed to the event and how to prevent future events. The purpose of an RCA is to find out what happened, why it happened, and determine what changes need to be made. It can be an early step in a PIP, helping to identify what needs to be changed to improve performance. Once you have identified what changes need to be made, the steps you will follow are those you would use in any type of PIP. Note there are a number of tools you can use to perform RCA, described below. Directions: Use this guide to walk through a Root Cause Analysis (RCA) to investigate events in your facility (e.g., adverse event, incident, near miss, complaint). Facilities accredited by the Joint Commission or in states with regulations governing completion of RCAs should refer to those requirements to be sure all necessary steps are followed. Below is a quick overview of the steps a PIP team might use to conduct RCA. Steps Explanation 1. Identify the event to be Events and issues can come from many sources (e.g., incident report, investigated and gather risk management referral, resident or family complaint, health preliminary information department citation). The facility should have a process for selecting events that will undergo an RCA. -

Pbfixedincomedailyjan1716.Pdf

mashreq Fixed Income Trading Daily Market Update Sunday, January 17, 2015 Quote of the Day "Wealth consists not in having great possessions, but in having few wants." (Epictetus) Market Update Iran sanctions lifted after IAEA confirms compliance with the nuclear deal, US firms set to miss out as US sanctions remain International sanctions on Iran have been lifted after IAEA, the UN nuclear watchdog confirmed the country had complied with a deal designed to prevent it developing nuclear weapons. The International Atomic Energy Agency concluded that the Islamic Republic had curbed its ability to develop an atomic weapon as required under an accord with world powers. The US and five other nations agreed in July’s accord to lift sanctions on Iran “simultaneously with the IAEA-verified implementation” of the deal. “Iran has undertaken significant steps that many people doubted would ever come to pass,” clearing the way for sanctions to end, US Secretary of State John Kerry said in Vienna late on Saturday after Iran’s compliance with the agreement was certified. Still, he said the accord “doesn’t wipe away all of the concerns” of the international community, and “verification remains, as it always has been, the backbone of this agreement." The EU foreign policy chief, Federica Mogherini, said the deal would contribute to improved regional and international peace and security. “Relations between Iran and the IAEA now enter a new phase. It is an important day for the international community,” Yukiya Amano, director general of the agency, said in a statement. “This paves the way for the IAEA to begin verifying and monitoring Iran’s nuclear-related commitments.” Ahead of the announcement Iran freed four Iranian-Americans as part of a prisoner exchange with the US that had been negotiated in secret for more than a year. -

Root Cause Analysis in Surgical Site Infections (Ssis) 1Mashood Ahmed, 2Mohd

International Journal of Pharmaceutical Science Invention ISSN (Online): 2319 – 6718, ISSN (Print): 2319 – 670X www.ijpsi.org Volume 1 Issue 1 ‖‖ December. 2012 ‖‖ PP.11-15 Root cause analysis in surgical site infections (SSIs) 1Mashood Ahmed, 2Mohd. Shahimi Mustapha, 3 4 Mohd. Gousuddin, Ms. Sandeep kaur 1Mashood Ahmed Shah (Master of Medical Laboratory Technology, Lecturer, Faculty of Pharmacy, Lincoln University College, Malaysia) 2Prof.Dr.Mohd. Shahimi Mustapha,(Dean, Faculty of Pharmacy, Lincoln University College, Malaysia) 3Mohd.Gousuddin, Master of Pharmacy (Lecturer, Faculty of Pharmacy, Lincoln University College, Malaysia) 4Sandeep kaur,(Student of Infection Prevention and control, Wairiki Institute of Technology, School of Nursing and Health Studies, Rotorua: NZ ) ABSTRACT: Surgical site infections (SSIs) are wound infections that usually occur within 30 days after invasive procedures. The development of infections at surgical incision site leads to extend of infection to adjacent tissues and structures.Wound infections are the most common infections in surgical patients, about 38% of all surgical patients will develop a SSI.The studies show that among post-surgical procedures, there is an increased risk of acquiring a nosocomial infection.Root cause analysis is a method used to investigate and analyze a serious event to identify causes and contributing factors, and to recommend actions to prevent a recurrence including clinical as well as administrative review. It is particularly useful for improving patient safety systems. The risk management process is done for any given scenario in three steps: perioperative condition, during operation and post-operative condition. Based upon the extensive searches in several biomedical science journals and web-based reports, we discussed the updated facts and phenomena related to the surgical site infections (SSIs) with emphasis on the root causes and various preventive measures of surgical site infections in this review. -

Root Cause Analysis: the Essential Ingredient Las Vegas IIA Chapter February 22, 2018 Agenda • Overview

Root Cause Analysis: The Essential Ingredient Las Vegas IIA Chapter February 22, 2018 Agenda • Overview . Concept . Guidance . Required Skills . Level of Effort . RCA Process . Benefits . Considerations • Planning . Information Gathering • Fieldwork . RCA Tools and Techniques • Reporting . 5 C’s Screen 2 of 65 OVERVIEW Root Cause Analysis (RCA) A root cause is the most reasonably identified basic causal factor or factors, which, when corrected or removed, will prevent (or significantly reduce) the recurrence of a situation, such as an error in performing a procedure. It is also the earliest point where you can take action that will reduce the chance of the incident happening. RCA is an objective, structured approach employed to identify the most likely underlying causes of a problem or undesired events within an organization. Screen 4 of 65 IPPF Standards, Implementation Guide, and Additional Guidance IIA guidance includes: • Standard 2320 – Analysis and Evaluation • Implementation Guide: Standard 2320 – Analysis and Evaluation Additional guidance includes: • PCAOB Initiatives to Improve Audit Quality – Root Cause Analysis, Audit Quality Indicators, and Quality Control Standards Screen 5 of 65 Required Auditor Skills for RCA Collaboration Critical Thinking Creative Problem Solving Communication Business Acumen Screen 6 of 65 Level of Effort The resources spent on RCA should be commensurate with the impact of the issue or potential future issues and risks. Screen 7 of 65 Steps for Performing RCA 04 02 Formulate and implement Identify the corrective actions contributing to eliminate the factors. root cause(s). 01 03 Define the Identify the root problem. cause(s). Screen 8 of 65 Steps for Performing RCA Risk Assessment Root Cause Analysis 1. -

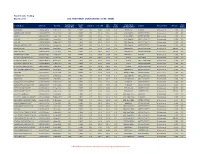

Fixed Income Trading May 10, 2016 USD INVESTMENT GRADE ISSUES (LONG TERM)

Fixed Income Trading May 10, 2016 USD INVESTMENT GRADE ISSUES (LONG TERM) Outstanding Coupon Indic. Offer Credit Rating Risk Security Name ISIN Code Maturity Coupon % Indic. Bid Country Payment Rank Min. Size Amount (Mio) Type Offer Yield % S&P/Moody/Fitch Rating AGRIUM INC US008916AP31 15-Mar-2025 550 FIXED 3.38 99.08 99.08 3.50 BBB/Baa2/- CANADA Sr Unsecured 2,000 P3 AMERICAN INTL GROUP US026874DD67 10-Jul-2025 1250 FIXED 3.75 101.42 101.42 3.56 A-/Baa1/BBB+ UNITED STATES Sr Unsecured 2,000 P3 AON PLC US00185AAF12 14-Jun-2024 600 FIXED 3.50 101.66 101.66 3.26 A-/Baa2/BBB+ UNITED STATES Sr Unsecured 2,000 P3 AT&T INC US00206RBN17 1-Dec-2022 1500 FIXED 2.63 99.33 99.33 2.74 BBB+/Baa1/A- UNITED STATES Sr Unsecured 2,000 P3 AT&T INC US00206RCN08 15-May-2025 5000 FIXED 3.40 101.43 101.43 3.21 BBB+/Baa1/A- UNITED STATES Sr Unsecured 2,000 P3 BANK OF AMERICA CORP US06051GEU94 11-Jan-2023 4250 FIXED 3.30 102.16 102.16 2.94 BBB+/Baa1/A UNITED STATES Sr Unsecured 2,000 P3 BARCLAYS PLC US06738EAE59 16-Mar-2025 2000 FIXED 3.65 97.62 97.62 3.97 BBB/Baa3/A UNITED KINGDOM Sr Unsecured 200,000 P3 BARCLAYS PLC US06738EAN58 12-Jan-2026 2500 FIXED 4.38 100.83 100.83 4.27 BBB/Baa3/A UNITED KINGDOM Sr Unsecured 200,000 P3 BARRICK GOLD CORP US067901AQ17 1-May-2023 730 FIXED 4.10 103.55 103.55 3.52 BBB-/Baa3/- CANADA Sr Unsecured 2,000 P3 BHP BILLITON FIN USA LTD US055451AQ16 24-Feb-2022 1000 FIXED 2.88 100.95 101.92 2.52 A/A3/A+ AUSTRALIA Sr Unsecured 2,000 P3 BP CAPITAL MARKETS PLC US05565QCB23 6-Nov-2022 1000 FIXED 2.50 98.26 98.26 2.80 A-/A2/A UNITED KINGDOM -

SWIFT Gpi Delivering the Future of Cross-Border Payments, Today SWIFT Gpi SWIFT Gpi

SWIFT gpi Delivering the future of cross-border payments, today SWIFT gpi SWIFT gpi SWIFT gpi 4 SWIFT is an innovative The Concept 8 technology company. As an industry cooperative, we listen The Tracker 10 Delivering and respond to the evolving The Observer 12 needs of our Community. The Directory 14 Part of our core mission is to Market infrastructures 16 the future of bring the financial community The Roadmap 18 together to work collaboratively to shape market practice, Enable digital transformation 22 define standards and debate Explore new technology 24 cross-border issues of mutual interest. payments, Innovation is an ongoing process, and through our R&D programmes and initiatives such as SWIFTLab, Innotribe, today and the SWIFT Institute, SWIFT is ideally placed to offer insights into the future of global financial technology and work with our Community to make real world change really happen. 2 3 SWIFT gpi SWIFT gpi SWIFT gpi SWIFT global payments innovation (gpi) In its first phase, SWIFT gpi focuses on business-to-business At Citi, we welcome the launch of As an early member of SWIFT dramatically improves the customer payments. It is designed to help corporates grow their international SWIFT gpi – we see this as a key gpi, Bank of China successfully experience in cross-border payments business, improve supplier initiative in evolving how cross- completed the gpi pilot and by increasing the speed, transparency relationships, and achieve greater border payments are transacted. was one of the first banks to treasury efficiencies. Thanks to SWIFT The time is right for the industry to go live. -

Root Cause Analysis in Health Care Tools and Techniques

Root Cause Analysis in Health Care Tools and Techniques SIXTH EDITION Includes Flash Drive! Senior Editor: Laura Hible Project Manager: Lisa King Associate Director, Publications: Helen M. Fry, MA Associate Director, Production: Johanna Harris Executive Director, Global Publishing: Catherine Chopp Hinckley, MA, PhD Joint Commission/JCR Reviewers for the sixth edition: Dawn Allbee; Anne Marie Benedicto; Kathy Brooks; Lisa Buczkowski; Gerard Castro; Patty Chappell; Adam Fonseca; Brian Patterson; Jessica Gacki-Smith Joint Commission Resources Mission The mission of Joint Commission Resources (JCR) is to continuously improve the safety and quality of health care in the United States and in the international community through the provision of education, publications, consultation, and evaluation services. Joint Commission Resources educational programs and publications support, but are separate from, the accreditation activities of The Joint Commission. Attendees at Joint Commission Resources educational programs and purchasers of Joint Commission Resources publications receive no special consideration or treatment in, or confidential information about, the accreditation process. The inclusion of an organization name, product, or service in a Joint Commission Resources publication should not be construed as an endorsement of such organization, product, or service, nor is failure to include an organization name, product, or service to be construed as disapproval. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. Every attempt has been made to ensure accuracy at the time of publication; however, please note that laws, regulations, and standards are subject to change. Please also note that some of the examples in this publication are specific to the laws and regulations of the locality of the facility. -

An Empirical Approach to Improve the Quality and Dependability of Critical Systems Engineering

Nuno Pedro de Jesus Silva An Empirical Approach to Improve the Quality and Dependability of Critical Systems Engineering PhD Thesis in Doctoral Program in Information Science and Technology, supervised by Professor Marco Vieira and presented to the Department of Informatics Engineering of the Faculty of Sciences and Technology of the University of Coimbra August 2017 An Empirical Approach to Improve the Quality and Dependability of Critical Systems Engineering Nuno Pedro de Jesus Silva Thesis submitted to the University of Coimbra in partial fulfillment of the requirements for the degree of Doctor of Philosophy August 2017 Department of Informatics Engineering Faculty of Sciences and Technology University of Coimbra This research has been developed as part of the requirements of the Doctoral Program in Information Science and Technology of the Faculty of Sciences and Technology of the University of Coimbra. This work is within the Dependable Systems specialization domain and was carried out in the Software and Systems Engineering Group of the Center for Informatics and Systems of the University of Coimbra (CISUC). This work was supported financially by the Top-Knowledge program of CRITICAL Software, S.A. and carried out partially in the frame of the European Marie Curie Project FP7-2012-324334-CECRIS (Certification of CRItical Systems). This work has been supervised by Professor Marco Vieira, Full Professor (Professor Catedrático), Department of Informatics Engineering, Faculty of Sciences and Technology, University of Coimbra. iii iv “Safety is not an option!” James H. Miller Miller, James H. "2009 CEOs Who "Get It"" Interview. Safety and Health Magazine.” February 1, 2009. Accessed October 13, 2016. -

Statistical Process Control, Part 5: Cause-And-Effect Diagrams

Performance Excellence in the Wood Products Industry Statistical Process Control Part 5: Cause-and-Effect Diagrams EM 8984 • August 2009 Scott Leavengood and James E. Reeb ur focus for the first four publications in this series has been on introducing you to Statistical Process Control (SPC)—what it is, how and why it works, and then Odiscussing some hands-on tools for determining where to focus initial efforts to use SPC in your company. Experience has shown that SPC is most effective when focused on a few key areas as opposed to the shotgun approach of measuring anything and every- thing. With that in mind, we presented check sheets and Pareto charts (Part 3) in the context of project selection. These tools help reveal the most frequent and costly quality problems. Flowcharts (Part 4) help to build consensus on the actual steps involved in a process, which in turn helps define precisely where quality problems might be occurring and what quality characteristics to monitor to help solve the problems. In Part 5, we now turn our attention to cause-and-effect diagrams (CE diagrams). CE diagrams are designed to help quality improvement teams identify the root causes of problems. In Part 6, we will continue this concept of root cause analysis with a brief intro- duction to a more advanced set of statistical tools: Design of Experiments. It is important, however, that we do not lose sight of our primary goal: improving quality and in so doing, improving customer satisfaction and the profitability of the company. We’ve identified the problem; now how can we solve it? In previous publications in this series, we have identified the overarching quality prob- lem we need to focus on and developed a flowchart identifying the specific steps in the process where problems may occur. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite