Fisher Companies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Shiloh Road Corridor Finding of No Significant Impact STPU 1031(2) CN 4666 May 2007

Finding of No Significant Impact Shiloh Road Corridor May 2007 STPU 1031(2) Control Number 4666 Shiloh Road Corridor Finding of No Significant Impact STPU 1031(2) CN 4666 May 2007 Table of Contents 1.0 Coordination Process.................................................................................................... 1 1.1 Press Release and Advertising....................................................................................... 1 1.2 Availability of EA.......................................................................................................... 1 1.3 Public Hearing and Comments ...................................................................................... 2 1.4 Other Federal Requirements ......................................................................................... 8 1.5 Availability of FONSI .................................................................................................... 8 2.0 Clarifications to the EA ................................................................................................. 8 2.1 Summary .................................................................................................................... 8 2.2 Purpose and Need ......................................................................................................11 2.3 Alternatives................................................................................................................12 2.4 Impacts .....................................................................................................................12 -

Issue 736 with So Much Happening at a Breakneck Pace the Last Several Weeks, It Would Be Easy to Overlook the State of the Format in the Month of November

W E E K L Y PPM: A November Not To Remember December 21, 2020, Issue 736 With so much happening at a breakneck pace the last several weeks, it would be easy to overlook the state of the format in the month of November. In fact, it might be for the best if you did. Even with a record poor showing overall, however, Country also had its share of notably strong performances on the station level. The November survey started Oct. 8 and concluded the day after Election Day. For that period, aggregate Country shares in PPM markets stood at its lowest total (excluding Holiday books) since the start of PPM measurement, with four stations setting new low water marks. And for the first time in the PPM era, the format experienced a non-Holiday month without a single market being led by a Country station. The apparent culprit: News-Talk. Just how big were News-Talk’s gains for the month? The aggregate 6+ share for all PPM subscribing News-Talk stations in September was 577.5. October rose to 623.0 and, by November, that number had jumped to 658.0 – a 14% increase over two Happy Holi-Glaze: Country Aircheck months. Conversely, the corresponding congratulates Capitol staffers on their 12th aggregate for Country trended 360.4 consecutive label of the year win. Pictured to 350.8 to 339.2 for a 5.8% decrease (clockwise) are Royce Risser, Donna over the same span. Country wasn’t Hughes, Annie Sandor, Bobby Young, alone: AC and Classic Hits were down Rod Phillips Megan O’Gara, Megan Youngblood, 2% each during the same span, and Top Ashley Knight, Chris Schuler, David 40 was off 3%. -

Cross-Platform Measurement Helps Local Stations Add Value to Broadcast and Digital

Case Study Cross-Platform Measurement Helps Local Stations Add Value to Broadcast and Digital Ecosystem The local game is changing. Daily deal sites like Groupon and LivingSocial.com in the U.S. have altered the way businesses reach out to consumers. For years, traditional local media – TV, radio and newspapers – has struggled with how to use their websites to complement their offerings and provide more to local businesses. Local TV stations, for example, have typically put video of reports or entire newscasts on their sites. As gateways to local news and events, websites for TV stations typically attract large numbers of visitors, yet it has been difficult to determine the effects and value of those visitors. The challenge has been leveraging “digital touchpoints,” quantifying their benefits and creating new models to attract more from local and national businesses who advertise and encourage those who otherwise might not advertise online at all. As new technology, such as location-based couponing, measurement capabilities, and integrated TV and Internet audience measurement, brings precision to local advertising, marketers are gaining the ability to better package local ad inventory to reach customers and amplify local TV audience value, combining TV and Online. In turn, the precision enables greater efficiency, meaning the opportunity to attract advertisers to spend more, locally. In other words, there’s a fortune to be made in your own backyard. Background Working with this valuable information, Fisher Communications Inc., an innovative local media company with TV, radio, Internet and mobile operations, found themselves positioned to provide their advertiser clients one-stop TV and digital local exposure. -

Bangor, ME Area Radio Stations in Market: 2

Bangor, ME Area Radio stations in market: 2 Count Call Sign Facility_id Licensee I WHCF 3665 BANGOR BAPTIST CHURCH 2 WJCX 421 CSN INTERNATIONAL 3 WDEA 17671 CUMULUS LICENSING LLC 4 WWMJ 17670 CUMULUS LICENSING LLC 5 WEZQ 17673 CUMULUS LICENSING LLC 6 WBZN 18535 CUMULUS LICENSING LLC 7 WHSN 28151 HUSSON COLLEGE 8 WMEH 39650 MAINE PUBLIC BROADCASTING CORPORATION 9 WMEP 92566 MAINE PUBLIC BROADCASTING CORPORATION 10 WBQI 40925 NASSAU BROADCASTING III, LLC II WBYA 41105 NASSAU BROADCASTING III, LLC 12 WBQX 49564 NASSAU BROADCASTING III, LLC 13 WERU-FM 58726 SALT POND COMMUNITY BROADCASTING COMPANY 14 WRMO 84096 STEVEN A. ROY, PERSONAL REP, ESTATE OF LYLE EVANS IS WNSX 66712 STONY CREEK BROADCASTING, LLC 16 WKIT-FM 25747 THE ZONE CORPORATION 17 WZON 66674 THE ZONE CORPORATION IH WMEB-FM 69267 UNIVERSITY OF MAINE SYSTEM 19 WWNZ 128805 WATERFRONT COMMUNICATIONS INC. 20 WNZS 128808 WATERFRONT COMMUNICATIONS INC. B-26 Bangor~ .ME Area Battle Creek, MI Area Radio stations in market I. Count Call Sign Facility_id Licensee I WBCH-FM 3989 BARRY BROADCASTING CO. 2 WBLU-FM 5903 BLUE LAKE FINE ARTS CAMP 3 WOCR 6114 BOARD OF TRUSTEES/OLIVET COLLEGE 4 WJIM-FM 17386 CITADEL BROADCASTING COMPANY 5 WTNR 41678 CITADEL BROADCASTING COMPANY 6 WMMQ 24641 CITADEL BROADCASTING COMPANY 7 WFMK 37460 CITADEL BROADCASTING COMPANY 8 WKLQ 24639 CITADEL BROADCASTING COMPANY 9 WLAV-FM 41680 CITADEL BROADCASTING COMPANY 10 WAYK 24786 CORNERSTONE UNIVERSITY 11 WAYG 24772 CORNERSTONE UNIVERSITY 12 WCSG 13935 CORNERSTONE UNIVERSITY 13 WKFR-FM 14658 CUMULUS LICENSING LLC 14 WRKR 14657 CUMULUS LICENSING LLC 15 WUFN 20630 FAMILY LIFE BROADCASTING SYSTEM 16 WOFR 91642 FAMILY STATIONS, INC. -

Fisher Communications, Inc

UNITEDSTATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON D.C 20549-3010 DIVISION OF CORPORATION FINANCE December 19 2007 Andrew Bor Perkins Coie 1201 Third Avenue Suite 4800 Seattle WA 98101-3099 Re Fisher Communications Inc Incoming letter dated November 29 2007 Dear Mr Bor This is in response to your letters dated November 29 2007 and December 11 2007 concerning the shareholder proposal submitted to Fisher Communications by GAMCO Asset Management Inc We also have received letter from the proponent dated December 2007 Our response is attached to the enclosed photocopy of your correspondence By doing this we avoid having to recite or summarize the facts set forth in the correspondence Copies of all of the correspondence also will be provided to the proponent In connection with this matter your attention is directed to the enclosure which sets forth brief discussion of the Divisions informal procedures regarding shareholder proposals Sincerely Jonathan Ingram Deputy Chief Counsel Enclosures cc Peter Goldstein Director of Regulatory Affairs GAMCO Asset Management Inc One Corporate Center Rye NY 10580-1435-1422 December 19 2007 Response of the Office of Chief Counsel Division of Corporation Finance Re Fisher Communications Inc Incoming letter dated November 29 2007 The proposal relates to acquisitions for view that Fisher Communications There appears to be some basis your may Fisher Communications received it exclude the proposal under rule 14a-8e2 because after the deadline for submitting proposals We note in particular your representations -

Download the SCEC Final Report (Pdf Format)

Seattle Commission on Electronic Communication Steve Clifford Michele Lucien Commission Chair Fisher Communications/KOMO-TV Former CEO, KING Broadcasting Betty Jane Narver Rich Lappenbusch University of Washington Commission Vice Chair Microsoft Amy Philipson UWTV David Brewster Town Hall Vivian Phillips Family Business Margaret Gordon University of Washington Josh Schroeter Founder, Blockbuy.com Bill Kaczaraba NorthWest Cable News Ken Vincent KUOW Radio Norm Langill One Reel Jean Walkinshaw KCTS-TV Commission Staff City Staff Anne Fennessy Rona Zevin Cocker Fennessy City of Seattle Kevin Evanto JoanE O’Brien Cocker Fennessy City of Seattle Table of Contents Final Report Letter from the Commission Chair ......................................................................... 2 Executive Summary .................................................................................................. 3 Diagram of TV/Democracy Portal.......................................................................... 4 Commission Charge & Process ............................................................................... 6 Current Environment................................................................................................. 8 Recommended Goal, Mission Statement & Service Statement...................... 13 Commission Recommendations ............................................................................ 14 Budget & Financing ................................................................................................ 24 Recommended -

Seattle a Digital Community Still in Transition Jessica Durkin, Tom Glaisyer, and Kara Hadge, Media Policy Initiative June 2010, Release 2.0

New America Foundation An Information Community Case Study: Seattle A digital community still in transition Jessica Durkin, Tom Glaisyer, and Kara Hadge, Media Policy Initiative June 2010, Release 2.0 Seattle, Washington, could be considered a city singularly suited to develop a healthy democracy in the digital age. The city government, citizens and business have created a productive environment for the next generation of information-sharing and community engagement. Years of economic growth and relative prosperity have fostered new, superior practices in news and information. Yet, losing a major print newspaper, as Seattle did when The Seattle Post-Intelligencer closed, adversely affects a community, by leaving it with one less place to provide public service journalism, stories about people and general community updates. In parallel, Seattle has been at the center of an explosion of alternative news outlets, especially online, which has created a critical mass of information portals for geographic and social communities. As the Knight Report, Informing Communities: Sustaining Democracy in a Digital Age, highlights, it is important to understand that there are three important elements to be considered as we analyze media and democracy in the 21st century: • availability of relevant and credible information to all Americans and their communities; • capacity of individuals to engage with information; and • individual engagement with information and the public life of the community. However, despite the relative vibrancy of the media scene, and even with all its demographic and other advantages, it is unclear how much of this innovation is sustainable. The local web is littered with websites that are no longer updated, and few of the startups boast anything like the journalistic firepower or profitability of the papers of the past. -

Redacted -- for Public Inspection

REDACTED -- FOR PUBLIC INSPECTION July 19, 2017 By Electronic Filing Marlene H. Dortch Secretary Federal Communications Commission 445 Twelfth Street SW Washington, D.C. 20554 Re: MB Docket No. 17-179 Tribune Media Company and Sinclair Broadcast Group, Inc. Consolidated Applications for Consent to Transfer Control Dear Ms. Dortch: Pursuant to the Protective Order in this proceeding,1 Tribune Media Company hereby submits the enclosed unredacted, Highly Confidential Information for inclusion in the record of the referenced proceeding. The enclosed submission consists entirely of Highly Confidential Information. Accordingly, pursuant to paragraph 7 of the Protective Order, access to the submission is limited to Outside Counsel and Outside Consultants and their employees who have executed and filed the Acknowledgement attached as Appendix B to the Protective Order. The information in the submission previously was included as Attachments V and VII to the Comprehensive Exhibit to the Consolidated Applications with a request for confidentiality under Section 0.459 of the Rules. It is being resubmitted herewith in conformity with the requirements of the Protective Order. Separately, also pursuant to the Protective Order, Tribune is submitting (1) two copies of the submission in an encrypted .pdf file to David Roberts of the Media Bureau, and (2) a 1 Tribune Media Company and Sinclair Broadcast Group, Inc., Consolidated Applications for Consent to Transfer Control, Protective Order, DA 17-678 (July 14, 2017) (the “Protective Order”). DC: 6472326-1 Marlene H. Dortch, Secretary July 19, 2017 Page 2 REDACTED -- FOR PUBLIC INSPECTION redacted, public version of this submission (as reflected in Attachments V and VII to the Comprehensive Exhibit) via ECFS. -

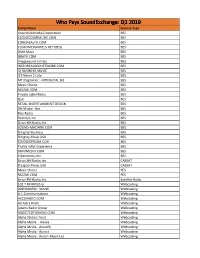

Licensee Count Q1 2019.Xlsx

Who Pays SoundExchange: Q1 2019 Entity Name License Type Aura Multimedia Corporation BES CLOUDCOVERMUSIC.COM BES COROHEALTH.COM BES CUSTOMCHANNELS.NET (BES) BES DMX Music BES GRAYV.COM BES Imagesound Limited BES INSTOREAUDIONETWORK.COM BES IO BUSINESS MUSIC BES It'S Never 2 Late BES MTI Digital Inc - MTIDIGITAL.BIZ BES Music Choice BES MUZAK.COM BES Private Label Radio BES Qsic BES RETAIL ENTERTAINMENT DESIGN BES Rfc Media - Bes BES Rise Radio BES Rockbot, Inc. BES Sirius XM Radio, Inc BES SOUND-MACHINE.COM BES Stingray Business BES Stingray Music USA BES STUDIOSTREAM.COM BES Thales Inflyt Experience BES UMIXMEDIA.COM BES Vibenomics, Inc. BES Sirius XM Radio, Inc CABSAT Stingray Music USA CABSAT Music Choice PES MUZAK.COM PES Sirius XM Radio, Inc Satellite Radio 102.7 FM KPGZ-lp Webcasting 999HANKFM - WANK Webcasting A-1 Communications Webcasting ACCURADIO.COM Webcasting Ad Astra Radio Webcasting Adams Radio Group Webcasting ADDICTEDTORADIO.COM Webcasting Aloha Station Trust Webcasting Alpha Media - Alaska Webcasting Alpha Media - Amarillo Webcasting Alpha Media - Aurora Webcasting Alpha Media - Austin-Albert Lea Webcasting Alpha Media - Bakersfield Webcasting Alpha Media - Biloxi - Gulfport, MS Webcasting Alpha Media - Brookings Webcasting Alpha Media - Cameron - Bethany Webcasting Alpha Media - Canton Webcasting Alpha Media - Columbia, SC Webcasting Alpha Media - Columbus Webcasting Alpha Media - Dayton, Oh Webcasting Alpha Media - East Texas Webcasting Alpha Media - Fairfield Webcasting Alpha Media - Far East Bay Webcasting Alpha Media -

President's Daily Diary Collection (Box 74A) at the Gerald R

Scanned from the President's Daily Diary Collection (Box 74A) at the Gerald R. Ford Presidential Library NATIONAL ARCHIVE AND RECORDS SERVICE WITHDRAWAL SHEET (PRESI ENTIAL LI RARIES) FOAM OF DOCUMENT CORRESPONDENTS OR TITLE DATE RESTRICTION A;ppeVltA,' y I'A'I . [Rfolac~.eJ top~ QVat'loJJle in open ~ I ·'~ FII.E LOCATION "l"'o.. 'I " 'VY"(."S1 J.e"~s ~o.l '-I J.J\'o.r,,! ~ol.l.ar ~ \t M4r~h I~ \c;, 5 " RESTRICTION CODES (AI Closed by E'x!!Cl./tivo Order 12358 governing access to nalional securltv information . (8) Closed by statute or by dIll agency which orIginated the document, Ie) CI In c:cordan'".e with restrictions contained In the donor's deed of gift. THE WHITE HOUSE THE DAILY DIARY OF PRESIDENT GERALD R. FORD PLACE DAY BEGAN DATE (Mo.. Day, Yr.) THE WHITE HOUSE MARCH 12, 1975 \." WASHINGTON, D.C. TIME DAY 7:05 a.m. WEDNESDA' -PHONE TIME "0 1:: .~'" ACTIVITY 0:'" ..: II I In Out "" ..: 7:05 The President had breakfast. 7:38 The President went to the Oval Office. 7:42 8:02 The President met with: David A. Peterson, Chief, Central Intelligence Agency/Office of Current Intelligence (CIA/OCI) White House Support Staff Lt. Gen. Brent,Scowcroft, Deputy Assistant for National Security Affairs The President met with: 8:02 8:40 Robert T. Hartmann, Counsellor 8:19 8:40 John T. Calkins, Executive Assistant to Mr. Hartmann 8:40 9:00 The President met with his Assistant, Donald H. Rumsfeld. 9:00 9:18 The President met with his Counsellor, John O. -

Las Vegas Towers

The Magazine for TV and FM DXers January 2020 The Official Publication of the Worldwide TV-FM DX Association Las Vegas Towers Courtesy of Bill Nollman IN THIS ISSUE Using a RTL-SDR Dongle to Listen to HD Radio And all the usual stuff. THE VHF-UHF DIGEST THE WORLDWIDE TV-FM DX ASSOCIATION Serving the UHF-VHF Enthusiast THE VHF-UHF DIGEST IS THE OFFICIAL PUBLICATION OF THE WORLDWIDE TV-FM DX ASSOCIATION DEDICATED TO THE OBSERVATION AND STUDY OF THE PROPAGATION OF LONG DISTANCE TELEVISION AND FM BROADCASTING SIGNALS AT VHF AND UHF. WTFDA IS GOVERNED BY A BOARD OF DIRECTORS: DOUG SMITH, KEITH McGINNIS, JIM THOMAS AND MIKE BUGAJ. Treasurer: Keith McGinnis wtfda.org/info Webmaster: Tim McVey Forum Site Administrator: Chris Cervantez Editorial Staff: Jeff Kruszka, Keith McGinnis, Fred Nordquist, Nick Langan, Doug Smith, John Zondlo and Mike Bugaj Your WTFDA Booard of Directors Doug Smith Mike Bugaj Keith McGinnis Jim Thomas [email protected] [email protected] [email protected] [email protected] Renewals by mail: Send to WTFDA, P.O. Box 501, Somersville, CT 06072. Check or MO for $10 payable to WTFDA. Renewals by Paypal: Send your dues ($10USD) from the Paypal website to [email protected] or go to https://www.paypal.me/WTFDA and type 10.00 or 20.00 for two years in the box. Our WTFDA.org website webmaster is Tim McVey, [email protected]. Our WTFDA Forums webmaster is Chris Cervantez, [email protected]. Fred Nordquist is in charge of club statistics at [email protected] Our email reflector is on Googlegroups. -

530 CIAO BRAMPTON on ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb

frequency callsign city format identification slogan latitude longitude last change in listing kHz d m s d m s (yy-mmm) 530 CIAO BRAMPTON ON ETHNIC AM 530 N43 35 20 W079 52 54 09-Feb 540 CBKO COAL HARBOUR BC VARIETY CBC RADIO ONE N50 36 4 W127 34 23 09-May 540 CBXQ # UCLUELET BC VARIETY CBC RADIO ONE N48 56 44 W125 33 7 16-Oct 540 CBYW WELLS BC VARIETY CBC RADIO ONE N53 6 25 W121 32 46 09-May 540 CBT GRAND FALLS NL VARIETY CBC RADIO ONE N48 57 3 W055 37 34 00-Jul 540 CBMM # SENNETERRE QC VARIETY CBC RADIO ONE N48 22 42 W077 13 28 18-Feb 540 CBK REGINA SK VARIETY CBC RADIO ONE N51 40 48 W105 26 49 00-Jul 540 WASG DAPHNE AL BLK GSPL/RELIGION N30 44 44 W088 5 40 17-Sep 540 KRXA CARMEL VALLEY CA SPANISH RELIGION EL SEMBRADOR RADIO N36 39 36 W121 32 29 14-Aug 540 KVIP REDDING CA RELIGION SRN VERY INSPIRING N40 37 25 W122 16 49 09-Dec 540 WFLF PINE HILLS FL TALK FOX NEWSRADIO 93.1 N28 22 52 W081 47 31 18-Oct 540 WDAK COLUMBUS GA NEWS/TALK FOX NEWSRADIO 540 N32 25 58 W084 57 2 13-Dec 540 KWMT FORT DODGE IA C&W FOX TRUE COUNTRY N42 29 45 W094 12 27 13-Dec 540 KMLB MONROE LA NEWS/TALK/SPORTS ABC NEWSTALK 105.7&540 N32 32 36 W092 10 45 19-Jan 540 WGOP POCOMOKE CITY MD EZL/OLDIES N38 3 11 W075 34 11 18-Oct 540 WXYG SAUK RAPIDS MN CLASSIC ROCK THE GOAT N45 36 18 W094 8 21 17-May 540 KNMX LAS VEGAS NM SPANISH VARIETY NBC K NEW MEXICO N35 34 25 W105 10 17 13-Nov 540 WBWD ISLIP NY SOUTH ASIAN BOLLY 540 N40 45 4 W073 12 52 18-Dec 540 WRGC SYLVA NC VARIETY NBC THE RIVER N35 23 35 W083 11 38 18-Jun 540 WETC # WENDELL-ZEBULON NC RELIGION EWTN DEVINE MERCY R.