Press Release Moradabad Bareilly Expressway Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Head Post Office, Katchery Road, Bahraich-271801 Head Post Office, Veer Vinay Chowk, Balrampur

Sr. No. POPSK ADDRESS AMETHI Head post office, Near Bus Station, Amethi-227405 AZAMGARH | 2 Head Post Office, Civil line, Azamgarh-2760001 BAHRAICH Head Post Office, Katchery Road, Bahraich-271801 BALLIA Head Post Office, Harpur Middhi Road, District Court Ballia - 277001 BALRAMPUR Head Post Office, Veer Vinay Chowk, Balrampur- 271201 GONDA Head Post Ofice, Jail Road, Gonda- 271001 MAU Head Post Office, Near Railway Crossing Mau - 275101 PRATAPGARH Head Post Office, Pratapgarh- 230001 8 RAEBAREL Head Post Office, Ghantaghar, Raebareli- 229001 SITAPUR Head Post Office, Sitapur- 261001 10 SULTANPUR Head Post Office, G N Road, Civil Line, Sultanpur-228001 |11 UNNAO Head Post Office, Civil Lines, Near Railway Station, Unnao- 209801 12 JAUNPUR Head Post Office, Alfastinganj, Near Jaunpur Kotwali, Jaunpur- 222001 13 Head Post Office Chunar, Dargah Sharif Station Road, Tammanpatti - 14 CHUNAR 231304 FAIZABAD Head Post Office, Civil Lines Faizabad - 224001 |15 DEORIA Head Post Office Deoria, Sadar Taluk, Deoria 274001 16 Head Post Office Jhansi, In front ofJhansi Hotel, Sadar Bazar, Jhansi JHANSI 17 284001 ALLAHABAD Head Post Office, S.N. Marg Civil Lines, Allahabad 18 Head Post Office Ghazipur, In front of Opium Factory, Mahuwabagh, GHAZIPUR Ghazipur- 233001 19 Head Post office Near Fatehpur Railway Crossing, Behind BSNL FATEHPUR Building, Police Line Fatehpur 212601 20 21 AMBEDKAR NAGAR Head Post Office, SH-5, Moradabad Mohall, Akbarpur,- 224122 22 BANDA BANDA HEAD OFFICE, NEAR BANGALIPURA - 210001 23 HAMIRPUR HAMIRPUR HEAD OFFICE, NEAR BUS STAND-210301 | 24 BHADOHI Bhadohi Mukhya Dakghar, Bhadohi - 221401 25 SIDDHARTHNAGAR HEAD POST OFFICE, TETRI BAZAR, NAUGARH, SIDDHARTHNAGAR, | 272207 (DOMARIYAGANJ) 26 MAHARAJGANJ HEAD POST OFFICE, WARD NO. -

Electrification

Railway Electrification I Executive Summary of Railway Electrification With a view to reduce the Nation’s dependence on imported petroleum based energy and to enhance energy security of the Country, as well as to make the Railway System more eco- friendly and modernized, Indian Railways have been progressively electrifying its rail routes. Upto March 2016, 23,555 Route kilometers which is 35.32% of the total Railway network has been electrified. On this electrified route 64.80% of freight traffic & 51.30% of Passenger traffic is hauled with fuel cost on electric traction being merely 38.70% of the total traction fuel cost on Indian Railways. In XIIth plan(2012-17), the target has been further enhanced to 6,500 RKms, out of which, 5,772 RKms have been electrified in the last four years of XIIth plan i.e. (in 2012-16) as against the proportionate target of 5,200 RKms. II Plan Period wise Progress of Railway Electrification S.No Plan Period RKM Electrified 1. Pre-Independence - 1925-1947 388 2. 1st Five Year Plan - 1951-56 141 3. 2nd Five Year Plan - 1956-61 216 4. 3rd Five Year Plan - 1961-66 1,678 5. Annual Plan - 1966-69 814 6. 4th Five Year Plan - 1969-74 954 7. 5th Five Year Plan - 1974-78 533 8. Inter Plan - 1978-80 195 9. 6th Five Year Plan - 1980-85 1,522 10. 7th Five Year Plan - 1985-90 2,812 11. Inter Plan - 1990-92 1,557 12. 8th Five Year Plan - 1992-97 2,708 13. -

MATHEMATICAL ASSESSMENT of WATER QUALITY at SAMBHAL, MORADABAD, UTTAR PRADESH (INDIA) ASHUTOSH Dixita, NAVNEET Kumarb and D

Int. J. Chem. Sci.: 10(4), 2012, 2033-2038 ISSN 0972-768X www.sadgurupublications.com MATHEMATICAL ASSESSMENT OF WATER QUALITY AT SAMBHAL, MORADABAD, UTTAR PRADESH (INDIA) ASHUTOSH DIXITa, NAVNEET KUMARb and D. K. SINHA* K.G.K. College, MORADABAD (U.P.) INDIA aSinghania University (Raj.) INDIA bCollege of Engineering, Teerthanker Mahaveer University, MORADABAD (U.P.) INDIA ABSTRACT Underground water samples at ten different water sites of public places were collected and analyzed for different water quality parameters following standard methods of sampling and estimation. The water quality index has been calculated for all the sites using the data of all parameters and WHO drinking water standards. The calculated data reveals that the underground water at Sambhal, Moradabad is severely polluted invariably at all the sites of study. The present study suggests that people exposed to this water are prone to health hazards of polluted drinking water. Key words: Water quality, Water quality index, Unit weight, Quality rating. INTRODUCTION Though water is renewable resource, improper management and reckless use of water systems are causing serious threats to the availability and quality of water1-3. It is the duty of scientists to test the available water in any locality in and around any residential area. As a part of society, it is a must. Attention on water pollution and its management has become a need of hour because of far reaching impact on human health4,5. Moradabad is a ‘B’ class city of western Uttar Pradesh. It is situated at the bank of Ram Ganga river and its altitude from the sea level in about 670 feet. -

High Court of Judicature at Allahabad Notification Dated: Allahabad: May 11, 2021

HIGH COURT OF JUDICATURE AT ALLAHABAD NOTIFICATION DATED: ALLAHABAD: MAY 11, 2021 No. 1486 /Admin. (Services)/2021 Sri Nitivan Nigam, Additional Civil Judge, Senior Division/ Additional Chief Judicial Magistrate, Moradabad to be Secretary (Full Time), District Legal Services Authority, Moradabad vice Sri Sachin Kumar Dixit. No. 1487 /Admin. (Services)/2021 Sri Sachin Kumar Dixit, Secretary (Full Time), District Legal Services Authority, Moradabad to be Additional Chief Judicial Magistrate, Moradabad vice Sri Vinay Kumar Jaiswal. He is also appointed U/s 11(2) of the Code of Criminal Procedure 1973 (Act No. 2 of 1974) as Judicial Magistrate, First Class for trying cases relating to Economic Offences at Moradabad. No. 1488 /Admin. (Services)/2021 Sri Vinay Kumar Jaiswal, Additional Chief Judicial Magistrate, Moradabad to be Additional Chief Judicial Magistrate (Northern Railway), Moradabad in the vacant court. No. 1489 /Admin. (Services)/2021 Sri Aishwarya Pratap Singh, Additional Civil Judge, Senior Division/ Additional Chief Judicial Magistrate, Aligarh to be Additional Chief Judicial Magistrate (Northern Railway), Aligarh in the vacant court. No. 1490 /Admin. (Services)/2021 Sri Vikas Chaudhary, Additional Civil Judge, Senior Division/ Additional Chief Judicial Magistrate, Mathura to be Additional Chief Judicial Magistrate (Railway), Mathura in the vacant court. No. 1491 /Admin. (Services)/2021 Smt. Kumud Lata Tripathi, Additional Civil Judge, Senior Division/ Additional Chief Judicial Magistrate, Varanasi to be Secretary (Full Time), District Legal Services Authority, Varanasi vice Sri Vishv Jeet Singh. No. 1492 /Admin. (Services)/2021 Sri Vishv Jeet Singh, Secretary (Full Time), District Legal Services Authority, Varanasi to be Additional Chief Judicial Magistrate, Varanasi vice Sri Ashish Kumar Rai. -

Bijnor District Factbook | Uttar Pradesh

Uttar Pradesh District Factbook™ Bijnor District (Key Socio-economic Data of Bijnor District, Uttar Pradesh) January, 2019 Editor & Director Dr. R.K. Thukral Research Editor Dr. Shafeeq Rahman Compiled, Researched and Published by Datanet India Pvt. Ltd. D-100, 1st Floor, Okhla Industrial Area, Phase-I, New Delhi-110020. Ph.: 91-11-43580781, 26810964-65-66 Email : [email protected] Website : www.districtsofindia.com Online Book Store : www.datanetindia-ebooks.com Report No.: DFB/UP-134-0119 ISBN : 978-93-80590-46-2 First Edition : June, 2016 Updated Edition : January, 2019 Price : Rs. 7500/- US$ 200 © 2019 Datanet India Pvt. Ltd. All rights reserved. No part of this book may be reproduced, stored in a retrieval system or transmitted in any form or by any means, mechanical photocopying, photographing, scanning, recording or otherwise without the prior written permission of the publisher. Please refer to Disclaimer & Terms of Use at page no. 288 for the use of this publication. Printed in India No. Particulars Page No. 1 Introduction 1-3 About Bijnor District | Bijnor District at a Glance 2 Administrative Setup 4-12 Location Map of Bijnor District |Bijnor District Map with Sub-Districts | Reference Map of District |Administrative Unit | Number of Sub-districts, Towns, CD Blocks and Villages | Names of Sub-districts, Tehsils, Towns and their Wards and Villages | Names of District, Intermediate and Village Panchayats | Number of Inhabited Villages by Population Size |Number of Towns by Population Size 3 Demographics 13-34 Population -

Meerut Zone, Opposite Ccs University, Mangal Pandey Nagar, Meerut

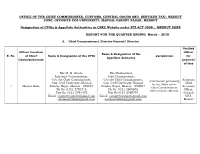

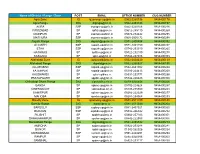

OFFICE OF THE CHIEF COMMISSIONER, CUSTOMS, CENTRAL GOODS AND SERVICES TAX:: MEERUT ZONE, OPPOSITE CCS UNIVERSITY, MANGAL PANDEY NAGAR, MEERUT Designation of CPIOs & Appellate Authorities in CBEC Website under RTI ACT 2005 :: MEERUT ZONE REPORT FOR THE QUARTER ENDING March – 2018 A. Chief Commissioner/ Director General/ Director Notified Office/ Location Officer Name & Designation of the S. No. of Chief Name & Designation of the CPIO Jurisdiction for Appellate Authority Commissionerate payment of fees Shri R. K. Gupta, Shri Roshan Lal, Assistant Commissioner, Joint Commissioner O/o the Chief Commissioner, O/o the Chief Commissioner, Assistant Information pertaining Opp. CCS University, Mangal Opp. CCS University, Mangal Chief to the Office of the 1 Meerut Zone Pandey Nagar, Meerut - 250004 Pandey Nagar, Meerut - 250004 Accounts Chief Commissioner, Ph No: 0121-2792745 Ph No: 0121-2600605 Officer, Meerut Zone, Meerut. Fax No: 0121-2761472 Fax No:0121-2769707 Central Email: [email protected] Email: [email protected] GST, [email protected] [email protected] Meerut B. Commissioner/ Addl. Director General Notified S. Commission Name & Designation of the officer for Name & Designation of the CPIO Jurisdiction No. erate Appellate Authority payment of fees Areas falling Shri Kamlesh Singh Shri Roshan Lal Joint Commissioner under the Assistant Chief Assistant Commissioner Districts of Accounts O/o the Commissioner, Office of the Commissioner of Central Meerut, Officer, Office Central GST Commissionerate Goods & Services Tax, Baghpat, of the Central GST Meerut, Opp. CCS University, Commissionerate: Meerut, Opposite: Muzaffarnagar, Commissioner Meerut Mangal Pandey Nagar, Meerut. Saharanpur, 1 Chaudhary Charan Singh University, of Central Commissione Fax No: 0121-2792773 Shamli, Goods & Mangal Pandey Nagar, Meerut- rate Amroha, Services Tax, 250004 Moradabad, Commissionera Bijnore and te: Meerut Ph No: 0121-2600605 Rampur in the Fax No:0121-2769707 State of Uttar Pradesh. -

Project Summary

Project Summary Proposed Protected forest land to be diverted for Doubling of Railway Track from (Km No.- 0.00 to 80.30) Roza to Sitapur Railway {KM No.- 0.00 – 11.00 in Shahjahanpur district}, {KM No.- 11.00 to 28.00 & 34.00 to 46.00 in Lakhimpur Kheri district}, {KM No.- 28.00 to 34.00 in Hardoi district} and {KM No.- 46.00 to 80.30 in Sitapur district} in Northern Railway Division Moradabad. District wise details of forest land and non forest land are as follows: Sr. No. DISTRICT PROTECTED NON FOREST FOREST LAND LAND Area (in Ha) Area (in Ha) 1 Shahjahanpur 8.80 0.0175 2 Lakhimpur Kheri 24.06 0.3235 3 Hardoi 6.1133 0.0851 4 Sitapur 30.6259 0.6435 Total Area 69.5992 1.0696 Mahesh Chand Executive Engineer/Con Northern Railway,Moradabad Area Calculation Sheet Proposed Protected Forest Land to be Diverted For Proposed new 2nd line along with existing Railway line under Roza - Sitapur Railway Track (Km. no. 0.00 - 80.30) Doubling Project of Northern Railway, from Km. 0.00 to 11.00, in Moradabad Division, District: Shahjahanpur (Uttar Pradesh) Protected Forest Land Area Calculation From To Length Width Area Area Sr. No. (Km) (Km) (m) (m) (SqM) (Ha) 1 1.900 7.360 5460.00 8.00 43680.00 4.3680 2 8.670 11.000 2330.00 8.00 18640.00 1.8640 7790.00 62320.00 6.2320 Proposed Protected Forest Land Area 6.2320Ha Protected Forest Land along Railway Yards Forest Land Area Calculation From To Length Width Area Area Sr. -

Name of District / Range / Zone POST EMAIL OFFICE NUMBER CUG

Name of District / Range / Zone POST EMAIL OFFICE NUMBER CUG NUMBER Agra Zone IG [email protected] 0562-2265736 9454400178 Agra Range DIG [email protected] 0562-2463343 9454400197 AGRA SSP [email protected] 0562-2250106 9454400246 FIROZABAD SP [email protected] 05612-285110 9454400269 MAINPURI SP [email protected] 05672-234442 9454400295 MATHURA SSP [email protected] 0565-2505172 9454400298 Aligarh Range DIG [email protected] 0571-2400404 9454400392 ALIGARH SSP [email protected] 0571-2401150 9454400247 ETAH SSP [email protected] 05742-233319 9454400265 HATHRAS SP [email protected] 05722-232100 9454400278 KASGANJ SP [email protected] 05744-247486 9454400393 Allahabad Zone IG [email protected] 0532-2424630 9454400139 Allahabad Range DIG [email protected] 0532-2260527 9454400195 ALLAHABAD SSP [email protected] 0532-2641902 9454400248 FATEHPUR SP [email protected] 05180-224413 9454400268 KAUSHAMBI SP [email protected] 05331-232771 9454400288 PRATAPGARH SP [email protected] 05342-220423 9454400300 Chitrakoot Dham Range DIG [email protected] 0519-2220538 9454400206 BANDA SP [email protected] 05192-224624 9454400257 CHITRAKOOT SP [email protected] 05198-235500 9454400263 HAMIRPUR SP [email protected] 05282-222329 9454400277 MAHOBA SP [email protected] 05281-254068 9454400293 Bareilly Zone IG [email protected] 0581-2511199 9454400140 Bareilly Range DIG [email protected] 0581-2511049 9454400204 BAREILLY SSP [email protected] 0581-2457021 9454400260 BUDAUN SSP [email protected] 05832-266342 9454400252 PILIBHIT SP [email protected] 05882-257183 9454400301 SHAHJAHANPUR SP [email protected] -

Directory of Officers - Uttar Pradesh (East) Telephone Directory of Income Tax Offices U

DIRECTORY OF OFFICERS - UTTAR PRADESH (EAST) TELEPHONE DIRECTORY OF INCOME TAX OFFICES U. P. (EAST) , LUCKNOW CHIEF COMMISSIONER OF INCOME TAX, LUCKNOW Name S.No. DESIGNATION ADDRESS (O) PHONE (O) FAX (O) MOBILE (Shri/Smt./Ms.) AAYAKAR BHAWAN, 5 - ASHOK 1 ARUN KUMAR SINGH CCIT (CCA) 0522-2233201 0522-2233210 8005445292 MARG, LUCKNOW ADDL. CIT (HQ), O/o AAYAKAR BHAWAN, 5 -ASHOK 8005445319 2 TAJINDER PAL SINGH 0522-2233202 0522-2233209 CCIT, LUCKINOW MARG, LUCKNOW 0872080468 ADDL. CIT (Vig.) O/o AAYAKAR BHAWAN, 5 -ASHOK 8005445319 3 TAJINDER PAL SINGH 0522-2233203 0522-2233213 CCIT, LUCKINOW MARG, LUCKNOW 0872080468 DY. CIT (HQ) Admn., AAYAKAR BHAWAN, 5 -ASHOK 4 O. N. PATHAK 0522-2233204 0522-2233204 8005446100 O/o CCIT, LUCKINOW MARG, LUCKNOW DY. CIT (Judl.), O/o AAYAKAR BHAWAN, 5 -ASHOK 5 RANJAN SRIVASTAVA 0522-2233294 0522-2233294 8005445123 CCIT, LUCKINOW MARG, LUCKNOW DY. CIT (Vig.), O/o AAYAKAR BHAWAN, 5 -ASHOK 6 SARAS KUMAR 0522-2233207 0522-2233207 8005445054 CCIT, LUCKINOW MARG, LUCKNOW ACIT (Tech.), O/o AAYAKAR BHAWAN, 5 -ASHOK 7 G. D. SINGH 0522-2233208 0522-2233208 8005445001 CCIT, LUCKINOW MARG, LUCKNOW ITO (HQ) Admn., O/o AAYAKAR BHAWAN, 5 -ASHOK 8 VIVEK NAGRATH 0522-2233206 0522-2233206 8005445321 CCIT, LUCKINOW MARG, LUCKNOW ITO (HQ) / PR, O/o AAYAKAR BHAWAN, 5 -ASHOK 9 PRAJESH SRIVASTAVA 0522-2233205 0522-2233205 8005445350 CCIT, LUCKINOW MARG, LUCKNOW MSTU, PRAGYA BHAWAN, DTRTI, 10 ATUL SONKAR ITO (MSTU) 0522-2720344 0522-2720344 8005445231 GOMTI NAGAR, LUCKNOW. AAYAKAR BHAWAN, 5 -ASHOK 11 JYOTI SHARMA ITO (OSD) - - 9967033678 MARG, LUCKNOW AO / DDO, O/o CCIT, AAYAKAR BHAWAN, 5 -ASHOK 12 ROOP SAXENA 0522-2233241 0522-2233241 8005445008 LUCKINOW MARG, LUCKNOW AO O/o CCIT, AAYAKAR BHAWAN, 5 -ASHOK 13 MUJEEB ASHRAF 0522-2233239 - 8005445011 LUCKINOW MARG, LUCKNOW PS, O/o CCIT, AAYAKAR BHAWAN, 5 -ASHOK 14 ANITA GUPTA 0522-2233201 0522-2233210 8005445010 LUCKINOW MARG, LUCKNOW PS, O/o CCIT, AAYAKAR BHAWAN, 5 -ASHOK 15 MANJU AGARWAL 0522-2233203 0522-2233213 8005445287 LUCKINOW MARG, LUCKNOW AD (OL), O/o CCIT, RADHA KUNTI BHAWAN, 16 S. -

Agra-Moradabad-Haldwani Sl

AGRA-MORADABAD-HALDWANI SL. No. 1 2 3 4 SERVICE CODE R135 M135 R135 M135 From ARR AGRA DEP 0 0 4:00 5:00 5:30 6:00 ARR 6:15 7:15 7:45 8:15 ALIGARH DEP 88 88 6:30 7:30 8:00 8:30 ARR 11:30 11:45 13:00 12:45 MORADABAD DEP 175 263 12:00 13:30 VIA SAMBHAL VIA CHANDAUSI TO HALDWANI-MORADABAD- AGRA SL. No. 1 2 3 4 SERVICE CODE I136 R136 R136 R136 From ARR MORADABAD DEP 0 0 0:00 4:00 4:30 5:00 ARR 4:15 8:15 8:45 9:15 ALIGARH DEP 175 175 4:30 8:45 9:15 9:45 ARR 6:45 11:15 11:45 12:15 AGRA DEP 88 263 9:00 TO HATHRAS-10:30 Page 1 of 8 AGRA-MORADABAD-HALDWANI SL. No. 5 6 7 8 SERVICE CODE I135 R135 R135 I135 From ALIGARH-4:00 ARR 6:30 AGRA DEP 0 0 6:30 7:00 7:15 7:30 ARR 8:45 9:15 9:30 9:45 ALIGARH DEP 88 88 9:00 9:30 9:45 10:00 ARR 14:00 14:30 14:45 15:00 MORADABAD DEP 175 263 14:30 15:00 15:30 TO HALDWANI HALDWANI-MORADABAD- AGRA SL. No. 5 6 7 8 SERVICE CODE M136 M136 I136 M136 From HALDWANI-5:00 ARR 7:30 MORADABAD DEP 0 0 6:00 7:00 7:45 8:00 ARR 10:15 11:15 12:00 12:15 ALIGARH DEP 175 175 10:30 11:30 12:15 12:30 ARR 13:45 14:30 14:45 AGRA DEP 88 263 15:30 TO VRINDAVAN 13:45 VIA SAMBHAL HATHRAS-ALI-18:00 VIA CHANDAUSI Page 2 of 8 AGRA-MORADABAD-HALDWANI SL. -

Download (17.8

E File no. Q-1401S/S/2017-Stat Government of India Ministry of Drinking Water & Sanitation (Stat Cell) ******** 6th Floor, Pt. Deendayal 'Antyodaya 8hawan' CGO Complex, Lodhi Road, New Delhi-ll0003 Date: 24th January, 2018 To, Principal Secretary / Secretary in charge of Rural Drinking water supply and Sanitation in A & N ISLANDS UT . Subject: Field visit in respect of monitoring of S8M (G) and NRDWP schemes of the Ministry by the Institutional National Level Monitors (NLMs) in 355 selected districts - reg. The Ministry of Drinking Water & Sanitation (Gol) administers two centrally sponsored schemesviz., National Rural Drinking Water Programme (NRDWP)for providing safe drinking water and Swachh Bharat Mission (Gramin) for providing improved sanitation facilities in the rural areas of the country. 2. The Ministry has engaged a number of Institutional National Level Monitors (NLMs), for the monitoring of Swachh Bharat Mission (Gramin) (SBM-G)and National Rural Drinking Water Programme (NRDWP)schemesin 355 selected districts in 24 StatesjUTs namely A & N ISLANDS, ANDHRA PRADESH,ARUNACHALPRADESH,ASSAM, BIHAR,CHHAmSGARH, JAMMU& KASHMIR,JHARKHAND,KARNATAKA,MADHYAPRADESH,MAHARASHTRA,MANIPUR, MEGHALAYA,MIZORAM, NAGALAND,ODISHA, PUDUCHERRYPUNJAB, ,RAJASTHAN,TAMIL NADU,TELANGANA,TRIPURA,UTTARPRADESHand WESTBENGAL. 3. For the aforesaid purpose, the representatives from the Institutional NLMs (as per list enclosed Annexure -8) would visit in alloted Gram Panchayatin the each 355 selected districts of above mentioned States & UT. The detailed list of allotted villages are available on the website of the Ministry (www.mdws.gov.in) under the link " Document Reports-- 7Monitoring & Evaluation". Principal Secretary j Secretary in charge of Rural Drinking water supply and Sanitation in the States and Districts Administration of these States are requested to provide the necessary support to the Institutional NLMs for carrying out the monitoring work effectively. -

Allahabad Bank

ALLAHABAD BANK Central Public Information Officers Appellate Authority Sl No. Name / Designation/Address / Phone / E-mail/ Place / Office Name / Designation Address / Phone / Fax / E-mail Place / Office 1 Sri Shashikar Dayal Allahabad Bank, Zonal Office ALLAHABAD Dr. Rahul Srivastava Deputy General 22 -P, Purushottam Das Tandon Marg, ZONE Circle General Manager Manager Civil Lines, Allahabad-211001. Allahabad Bank, Zonal Office Phone – 0532-2622883 FAX - 2420325 22 -P, Purushottam Das Tandon e-mail – [email protected] Marg, Civil Lines, Allahabad-211001. 2 Sri Vineet Bajpai Allahabad Bank, Zonal Office BAHRAICH Phone – 0532-2622883 FAX – Assistant General 114, Raipur Raja, Civil Lines, ZONE 2420325 Manager Bahraich – 271801Phone – 05252-232539 Email: FAX - 236151e-mail – [email protected] [email protected] 3 Sri Vijay Kumar Allahabad Bank, Zonal Office GONDA Assistant General Near Roadways Bus Stand, Bahraich Road ZONE Manager Gonda (UP) Phone – 05262-232761 FAX - 232762 e-mail – [email protected] 4 Sri Ajit Kumar Jha Allahabad Bank, Zonal Office GORAKHPUR Deputy General Mohaddipur, Kashya Road, Post – Kuraghat, ZONE Manager Gorakhpur- 2731008 Phone – 0551-2202564 FAX – 2200008 e-mail – [email protected] 5 Sri Rananjay Singh Allahabad Bank, Zonal Office HAMIRPUR Assistant General 10/379 Ramedi Tarauns, Hamirpur-210301 ZONE Manager Phone – 05282223205 FAX - 222282 e-mail – [email protected] 6 Sri Vinod kumar Dixit Allahabad Bank, Zonal Office, MIRZAPUR Assistant General Juley Garden, Jangi Road, Mirzapur-231001 ZONE Manager Phone – 05442-245209 FAX - 245984 e-mail – [email protected] 7 Sri Shashank Jain Allahabad Bank, Zonal Office, VARANASI Deputy General Takshal Theatre Building Nadesar, ZONE Manager Varanasi-221 002.