Cochlear Limited Strategy Overview 2020 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Insurance Australia Group Annual Report 2015 Insurance Australia Group Annual Report 2015

Insurance Australia Group Annual Report 2015 Insurance Australia Group Annual Report 2015 INSURANCE AUSTRALIA GROUP LIMITED ABN 60 090 739 923 CONTENTS Five year financial summary 1 Directors’ declaration 98 Directors’ report 2 Independent auditor’s report 99 Remuneration report 16 Shareholder information 101 Lead auditor’s independence declaration 36 Corporate directory 104 Financial statements 37 KEY DATES 2015 financial year end 30 June 2015 Full year results and dividend announcement 21 August 2015 Notice of meeting mailed to shareholders 7 September 2015 Final dividend for ordinary shares Record date 9 September 2015 Payment date 7 October 2015 Annual general meeting 21 October 2015 Half year end 31 December 2015 Half year results and dividend announcement 18 February 2016* Interim dividend for ordinary shares Record date 2 March 2016* * Payment date 30 March 2016 2016 financial year end 30 June 2016 Full year results and dividend announcement 19 August 2016* * Please note: dates are subject to change. Any changes will be published via a notice to the Australian Securities Exchange (ASX) 2015 Annual About this report General Meeting The 2015 annual report of Insurance Australia Group Limited (IAG, or IAG’s 2015 annual general meeting will the Group) includes IAG’s full statutory be held on Wednesday, 21 October 2015, accounts, along with the Directors’ and at the City Recital Hall, Angel Place remuneration reports for the financial Sydney, commencing at 10.00am. Details year 2015. This year’s corporate governance of the meeting, including information report is available in the About Us area of about how to vote, will be contained our website (www.iag.com.au). -

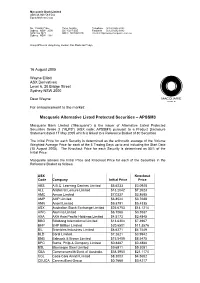

Macquarie Alternative Listed Protected Securities – APSSM3

Macquarie Bank Limited ABN 46 008 583 542 Equity Markets Group No. 1 Martin Place Telex 122246 Telephone (61 2) 8232 3333 Sydney NSW 2000 DX 10287 SSE Facsimile (61 2) 8232 6882 GPO Box 3423 SWIFT MACQAU2S Internet http://www.macquarie.com.au Sydney NSW 1164 Group Offices in Hong Kong, London, Sao Paulo and Tokyo 16 August 2005 Wayne Elliott ASX Derivatives Level 6, 20 Bridge Street Sydney NSW 2000 Dear Wayne For announcement to the market: Macquarie Alternative Listed Protected Securities – APSSM3 Macquarie Bank Limited (“Macquarie”) is the issuer of Alternative Listed Protected Securities Series 3 (“ALPS”) (ASX code: APSSM3) pursuant to a Product Disclosure Statement dated 17 May 2005 which is linked to a Reference Basket of 80 Securities. The Initial Price for each Security is determined as the arithmetic average of the Volume Weighted Average Price for each of the 5 Trading Days up to and including the Start Date (15 August 2005). The Knockout Price for each Security is determined as 55% of the Initial Price. Macquarie advises the Initial Price and Knockout Price for each of the Securities in the Reference Basket as follows: ASX Knockout Code Company Initial Price Price ABS A.B.C. Learning Centres Limited $5.6233 $3.0928 ALL Aristocrat Leisure Limited $13.2042 $7.2623 AMC Amcor Limited $7.0337 $3.8685 AMP AMP Limited $6.8524 $3.7688 ANN Ansell Limited $9.8791 $5.4335 ASX Australian Stock Exchange Limited $25.6753 $14.1214 AWC Alumina Limited $6.1068 $3.3587 AXA AXA Asia Pacific Holdings Limited $4.5173 $2.4845 BBG Billabong International Limited $13.6304 $7.4967 BHP BHP Billiton Limited $20.6501 $11.3576 BIL Brambles Industries Limited $8.6271 $4.7449 BLD Boral Limited. -

IAG Annual Report 2014

Insurance Australia Annual Group Report 2014 Insurance Australia Group Annual Report 2014 THE NUMBERS INSURANCE AUSTRALIA GROUP LIMITED ABN 60 090 739 923 CONTENTS Five year financial summary 1 Financial statements 49 Corporate governance 2 Directors’ declaration 117 Directors’ report 12 Independent auditor’s report 118 Remuneration report 26 Shareholder information 120 Lead auditor’s independence declaration 48 Corporate directory 124 KEY DATES 2014 financial year end 30 June 2014 Full year results and dividend announcement 19 August 2014 Notice of meeting mailed to shareholders 8 September 2014 Final dividend for ordinary shares Record date 10 September 2014 Payment date 8 October 2014 Annual General Meeting 30 October 2014 Half year end 31 December 2014 Half year results and dividend announcement 20 February 2015* Interim dividend for ordinary shares Record date 4 March 2015* Payment date 1 April 2015* 2015 financial year end 30 June 2015 Full year results and dividend announcement 21 August 2015* * Please note: dates are subject to change. Any changes will be published via a notice to the Australian Securities Exchange 2014 ANNUAL 2014 ANNUAL RECYCLED GENERAL MEETING REPORT SUITE PAPER CHOICE IAG’s 2014 annual general meeting The 2014 annual report of Insurance This report is printed on Nordset an will be held on Thursday, 30 October Australia Group Limited (IAG, or the Group) environmentally responsible paper produced 2014, at the Wesley Conference Centre, includes IAG’s full statutory accounts, from FSC® Mixed Sources Chain of Custody 220 Pitt Street, Sydney NSW 2000, along with the Directors’, remuneration (CoC) certified pulp from well managed commencing at 10.00am. -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Joint Submission to the Inquiry Into Impediments to Business

CSL biopharmaceutical manufacturing Broadmeadows, Victoria Cochlear medical device manufacturing Macquarie University, NSW Joint Submission to the House of Representatives Standing Committee on Economics Inquiry into Impediments to Business Investment May 2018 1 Executive Summary CSL and Cochlear are Australian success stories. They are the nation’s two largest and most successful innovation-focussed advanced manufacturing companies, both actively and successfully competing globally from an Australian base. Innovation and Science Australia’s recently released 2030 Strategic Plan predicted that Australia’s future prosperity will need to be driven by knowledge intensive companies that collaborate, innovate and export – companies like CSL and Cochlear. However, in 2017 CSL and Cochlear were two of only four Australian companies to make the list of the world’s top 1000 global R&D spenders1 both with an R&D intensity of over 10 per cent. Cochlear has over 100 research partnerships across the world and CSL has more than 180 in Australia alone. Both companies have a strong interest in enhancing Australia’s international competitiveness and maximising the social and economic benefits flowing from innovation- focussed industries but competition among peer nations for advanced manufacturing and R&D is intense. Policy makers all over the world are actively using micro and macro-economic levers to poach and fiercely compete for skilled job-creating capital investments. The realities are stark - less than 5% of Cochlear’s sales revenue is from Australia but it pays over 73% of its total tax bill here. For CSL, Australian sales revenue represents less than 10% of global external sales revenue, and its global income taxes (US$468.3 million paid in 2017) are paid in the countries where the majority of taxable income is earned. -

Cochlear Announces New Chair

1 University Avenue Macquarie University NSW 2109 AUSTRALIA www.cochlear.com ASX Announcement 31 May 2021 Cochlear announces Alison Deans as new Chair on the retirement of Rick Holliday-Smith from the Board Cochlear Limited, the global leader in implantable hearing solutions, announces that its Chairman, Rick Holliday-Smith will retire from the Board on 20 August 2021. He will be succeeded as Chair by current non-executive director Alison Deans. Mr Holliday-Smith has been a member of Cochlear’s Board since 2005 and has served as Chairman since mid-2010. Commenting on his decision to retire from the Board, Mr Holliday-Smith said, “I have greatly enjoyed my time on the Board of Cochlear and especially as Chairman for the past 11 years. It has been a privilege to work with an exceptional Board and management team. “Cochlear is an incredible company that has stayed true to its Mission to help people hear and be heard, marking a major milestone this year in celebrating its 40th birthday. The Company has provided more than 600,000 implant devices to people globally and continues to be the global market leader in implantable hearing solutions.” Alison Deans has been a non-executive director of Cochlear since January 2015. She was formerly Chief Executive Officer of technology investment companies netus and ecorp, and of eBay Australia. Mr Holliday-Smith said, “Alison’s deep understanding of the Company, breadth of experience as a non- executive director and extensive experience leading technology-enabled businesses means she will be an excellent and well-qualified Chair.” Ms Deans said, “Rick has instilled a relentless focus on Cochlear’s Mission and the importance of investment to drive long-term sustainable growth. -

TELSTRA ANNUAL REPORT 2013 Online Shareholder Services Annual Report Global Reporting Initiative Telstra’S Investor Centre

TELSTRA ANNUAL REPORT 2013 Online Shareholder Services Annual Report Global Reporting Initiative Telstra’s Investor Centre www.telstra. Telstra’s 2013 Annual Report is available We develop our sustainability reporting with com/investor has all the latest news and to all shareholders on our Investor Website reference to industry and sustainability standards information available for shareholders. at www.telstra.com.au/annualreports. including the United Nations Global Compact Communication on Progress, and the Global Shareholders can also easily To receive a hardcopy of the Annual Report Reporting Initiative (GRI) G3 Sustainability manage their shareholding online at (free of charge) you can call our Share Registry on Reporting Guidelines and Telecommunications www.linkmarketservices.com.au/telstra. 1300 88 66 77 and request the report be sent to you. Sector Supplement (pilot). This financial year we To access your information you will need your You may also update your communication have applied the GRI framework to application SRN/HIN and post code. Follow the prompts to preferences online to change the way you level B+. The full GRI Index can be found online log in and select from the following menu options: receive future copies of the Annual Report. at www.telstra.com.au/sustainability/report. Please refer to the Online Shareholder Services Holdings – transaction history, holding balance section for instructions on how to do this. and value and latest closing share price. ®Registered trademark of Telstra Corporation Limited. Sustainability Reporting Payment & Tax – dividend payment history, ™Trademark of Telstra Corporation limited. Selected graphs and data presented in this report payment instructions and TFN details. -

Directors' Report

DIRECTORS' REPORT The directors present their report together with the financial report of Insurance Australia Group Limited and the consolidated financial report of Insurance Australia Group Limited and its subsidiaries for the financial year ended 30 June 2012 and the auditor's report thereon. The following terminology is used throughout the financial report: IAG, Parent or Company - Insurance Australia Group Limited; and Group or Consolidated - the Consolidated entity consists of Insurance Australia Group Limited and its subsidiaries. DIRECTORS OF INSURANCE AUSTRALIA GROUP LIMITED The names and details of the Company's directors in office at any time during or since the end of the financial year are as follows. Directors were in office for the entire period unless otherwise stated. CHAIRMAN BRIAN (BM) SCHWARTZ AM FCA, FAICD, age 59 - Chairman and Independent non-executive director INSURANCE INDUSTRY EXPERIENCE Brian Schwartz was appointed a director of IAG in January 2005 and became chairman in August 2010. He is a member and former chairman of the IAG Nomination, Remuneration & Sustainability Committee and is also chairman of Insurance Manufacturers of Australia Pty Limited, a general insurance underwriting joint venture with RACV Ltd. OTHER BUSINESS AND MARKET EXPERIENCE Brian is a non-executive director of Brambles Limited, the deputy chairman of Westfield Group Limited and the deputy chairman of the board of Football Federation Australia Limited. Brian was the chief executive of Investec Bank (Australia) Ltd from 2005 to 2009. Previously, he was with Ernst & Young Australia from 1979 to 2004 becoming its chief executive in 1998. He was a member of Ernst & Young's global board and managing partner of the Oceania area responsible for the firm's operations in Australia, New Zealand, Indonesia, the Philippines, Vietnam and Fiji. -

Pendal Monthly Commentary Pendal Sustainable Future Australian Shares Portfolio December 2020

Pendal Monthly Commentary Pendal Sustainable Future Australian Shares Portfolio December 2020 Market commentary Portfolio overview Sustainable Future Australian Shares Portfolio The S&P/ASX 200 rose +1.2% in December, taking the year Investment To deliver outperformance relative to the to a +1.4% return. strategy benchmark before fees over a rolling five year period by investing in companies Covid cases continued to rise in the northern hemisphere, which Pendal has identified as having prompting further lockdowns. In the US, this has seen job leading financial, ethical and sustainability growth stall, although strong industrial production is likely to characteristics. have driven decent GDP growth. There is increasing Benchmark S&P/ASX 300 (TR) Index evidence of pressure on health care systems both there and Number of stocks 15-40 (26 as at 31 December 2020) in Europe. Sector limits Cash 2-10% We experienced an outbreak in Sydney at the end of # December, leading to border closures and local lockdowns. Dividend Yield 3.31% Nevertheless, a combination of optimism over vaccines and Top 10 holdings the extraordinary degree of monetary and fiscal policy support was enough to support the local equity market. Code Name Weight Broader economic and sentiment data is also supportive. CSL CSL Limited 9.58% CBA Commonwealth Bank of Australia Ltd 7.89% Retail sales momentum remains good, while the unemployment rate fell from 7% to 6.8% — better than FMG Fortescue Metals Group Limited 6.66% consensus expectations. Consumer and business ANZ ANZ Banking Group Limited 6.14% confidence indicators remain strong. XRO Xero Limited 5.44% Value style has continued to do well in Australia, helped by TLS Telstra Corporation Limited 4.88% strong returns from the miners, which led the 8.8% gain in Materials (+8.8%). -

A Hearing Life - + –

- + – Investor Previous Next Contents Centre COCHLEAR ANNUAL REPORT 2014 A hearing life - + – AR Investor 14 22 Previous Next Contents Centre Pg Financial Report Pg Notes to Financial Statements Pg Additional Reporting 23 Directors’ Report Basis of preparation 77 17. Inventories 106 Directors’ Declaration 23 Principal activities and 61 1. Reporting entity 78 18. Property, plant 107 Independent Audit Report review of operations and equipment and results 61 2. Basis of preparation 108 Additional information 80 19. Intangible assets 31 Remuneration Report Performance for the year 109 Glossary, Company ASX 84 20. Provisions Announcement Record 55 Lead Auditor’s and Company Information 62 3. Operating segments Independence Declaration Financial and capital structure 64 4. Revenue 56 Income Statement 87 21. Net debt and 65 5. Expenses finance costs 57 Statement of Comprehensive Income 65 6. Other income 89 22. Financial risk management 58 Balance Sheet 66 7. Earnings per share 59 Statement of Capital and reserves Changes in Equity 67 8. Dividends 99 23. Capital and reserves 60 Statement of Cash Flows 68 9. Notes to the statement of cash flows 100 24. Capital management Income taxes Other notes 69 10. Income tax expense 101 25. Auditors’ remuneration 70 11. Current and deferred tax 101 26. Commitments assets and liabilities 101 27. Contingent liabilities Employee benefits 102 28. Controlled entities 71 12. Employee expenses 103 29. Parent entity disclosures 71 13. Employee benefit liabilities 104 30. Changes in accounting policies 73 14. Share based payments 105 31. New standards and 76 15. Key management interpretations not personnel yet adopted 105 32. -

Commonwealth Bank of Australia (Incorporated with Limited Liability in the Commonwealth of Australia and Having Australian Business Number 48 123 123 124) As Issuer

Commonwealth Bank of Australia (incorporated with limited liability in the Commonwealth of Australia and having Australian Business Number 48 123 123 124) as Issuer U.S.$30,000,000,000 CBA Covered Bond Programme unconditionally and irrevocably guaranteed as to payments of interest and principal by Perpetual Corporate Trust Limited (incorporated with limited liability in the Commonwealth of Australia and having Australian Business Number 99 000 341 533) as trustee of the CBA Covered Bond Trust Under the U.S.$30,000,000,000 CBA Covered Bond Programme (the Programme) established by Commonwealth Bank of Australia ABN 48 123 123 124 (the Bank and the Issuer), the Issuer may from time to time issue bonds (Covered Bonds) denominated in any currency agreed between the Issuer and the Relevant Dealer(s) (as defined below). The price and amount of the Covered Bonds to be issued under the Programme will be determined by the Issuer and the Relevant Dealer(s) at the time of issue in accordance with the prevailing market conditions. Any Covered Bonds issued under the Programme on or after the date of this Prospectus are issued subject to the provisions described in this Prospectus and in any supplement hereto. Perpetual Corporate Trust Limited ABN 99 000 341 533 in its capacity as trustee of the CBA Covered Bond Trust (the Trust and, in such capacity, the Covered Bond Guarantor) has guaranteed payments of interest and principal under the Covered Bonds pursuant to a guarantee which is secured over the Mortgage Loan Rights (as defined in this Prospectus) and the other Assets of the Trust.