Uxw 33-35, September 2, 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Developing an Intergovernmental Nuclear Regulatory Organization

Developing an Intergovernmental Nuclear Regulatory Organization: Lessons Learned from the International Civil Aviation Organization, the International Maritime Organization, and the International Telecommunication Union Clarence Eugene Carpenter, Jr. Bachelor of Science in Mechanical Engineering, May 1988 Seattle University, Seattle, WA Master of Science in Technical Management, May 1997 The Johns Hopkins University, Baltimore, MD Master of Arts in International Science and Technology Policy, May 2009 The George Washington University, Washington, DC A Dissertation submitted to The Faculty of The Columbian College of Arts and Sciences of The George Washington University in partial fulfillment of the requirements for the degree of Doctor of Philosophy January 10, 2020 Dissertation directed by Kathryn Newcomer Professor of Public Policy and Public Administration The Columbian College of Arts and Sciences of The George Washington University certifies that Clarence Eugene Carpenter, Jr. has passed the Final Examination for the degree of Doctor of Philosophy as of November 26, 2019. This is the final and approved form of the dissertation. Developing an Intergovernmental Nuclear Regulatory Organization: Lessons Learned from the International Civil Aviation Organization, the International Maritime Organization, and the International Telecommunication Union Clarence Eugene Carpenter, Jr. Dissertation Research Committee: Kathryn Newcomer, Professor of Public Policy and Public Administration, Dissertation Director Philippe Bardet, Assistant Professor, -

The Ukrainian Weekly 1999, No.36

www.ukrweekly.com INSIDE:• Forced/slave labor compensation negotiations — page 2. •A look at student life in the capital of Ukraine — page 4. • Canada’s professionals/businesspersons convene — pages 10-13. Published by the Ukrainian National Association Inc., a fraternal non-profit association Vol. LXVII HE No.KRAINIAN 36 THE UKRAINIAN WEEKLY SUNDAY, SEPTEMBER 5, 1999 EEKLY$1.25/$2 in Ukraine U.S.T continues aidU to Kharkiv region W Pustovoitenko meets in Moscow with $16.5 million medical shipment by Roman Woronowycz the region and improve the life of Kharkiv’s withby RomanRussia’s Woronowycz new increasingprime Ukrainian minister debt for Russian oil Kyiv Press Bureau residents, which until now had produced Kyiv Press Bureau and gas. The disagreements have cen- few tangible results. tered on the method of payment and the KYIV – The United States government “This is the first real investment in terms KYIV – Ukraine’s Prime Minister amount. continued to expand its involvement in the of money,” said Olha Myrtsal, an informa- Valerii Pustovoitenko flew to Moscow on Ukraine has stated that it owes $1 bil- Kharkiv region of Ukraine on August 25 tion officer at the U.S. Embassy in Kyiv. August 27 to meet with the latest Russian lion, while Russia claims that the costs when it delivered $16.5 million in medical Sponsored by the Department of State, the prime minister, Vladimir Putin, and to should include money owed by private equipment and medicines to the area’s hos- humanitarian assistance program called discuss current relations and, more Ukrainian enterprises, which raises the pitals and clinics. -

Ukraine Nuclear Fuel Cycle Chronology

Ukraine Nuclear Fuel Cycle Chronology Last update: April 2005 This annotated chronology is based on the data sources that follow each entry. Public sources often provide conflicting information on classified military programs. In some cases we are unable to resolve these discrepancies, in others we have deliberately refrained from doing so to highlight the potential influence of false or misleading information as it appeared over time. In many cases, we are unable to independently verify claims. Hence in reviewing this chronology, readers should take into account the credibility of the sources employed here. Inclusion in this chronology does not necessarily indicate that a particular development is of direct or indirect proliferation significance. Some entries provide international or domestic context for technological development and national policymaking. Moreover, some entries may refer to developments with positive consequences for nonproliferation. 2003-1993 1 August 2003 KRASNOYARSK ADMINISTRATION WILL NOT ALLOW IMPORT OF UKRAINE'S SPENT FUEL UNTIL DEBT PAID On 1 August 2003, UNIAN reported that, according to Yuriy Lebedev, head of Russia's International Fuel and Energy Company, which is managing the import of spent nuclear fuel to Krasnoyarsk Kray for storage, the Krasnoyarsk administration will not allow new shipments of spent fuel from Ukraine for storage until Ukraine pays its $11.76 million debt for 2002 deliveries. —"Krasnoyarskiy kray otkazhetsya prinimat otrabotannoye yadernoye toplivo iz Ukrainy v sluchaye nepogasheniya 11.76 mln. dollarov dolga," UNIAN, 1 August 2003; in Integrum Techno, www.integrum.com. 28 February 2002 RUSSIAN REACTOR FUEL DELIVERIES TO COST $246 MILLION IN 2002 Yadernyye materialy reported on 28 February 2002 that Russian Minister of Atomic Energy Aleksandr Rumyantsev and Ukrainian Minister of Fuel and Energy Vitaliy Gayduk signed an agreement under which Ukraine will buy reactor fuel worth $246 million from Russia in 2002. -

Appendix C October 8, 2014

Nuclear Fuel Cycle Evaluation and Screening – Final Report – Appendix C October 8, 2014 APPENDIX C EVALUATION CRITERIA AND METRICS Nuclear Fuel Cycle Evaluation and Screening – Final Report – Appendix C ii October 8, 2014 Nuclear Fuel Cycle Evaluation and Screening – Final Report – Appendix C October 8, 2014 iii CONTENTS C. Evaluation Criteria and Metrics ......................................................................................................... 1 C-1. Nuclear Waste Management Criterion ..................................................................................... 1 C-1.1 Background on Nuclear Waste Management .............................................................. 1 C-1.2 Metric Development for the Nuclear Waste Management Criterion .......................... 5 C-1.3 Mass of SNF+HLW Disposed per Energy Generated ................................................ 6 C-1.4 Activity of SNF+HLW (@100 years) per Energy Generated ..................................... 7 C-1.5 Activity of SNF+HLW (@100,000 years) per Energy Generated .............................. 7 C-1.6 Mass of DU+RU+RTh Disposed per Energy Generated ............................................ 8 C-1.7 Volume of LLW per Energy Generated ...................................................................... 9 References for C-1. ........................................................................................................................... 25 C-2. Proliferation Risk Criterion ................................................................................................... -

The French Approach for the Regulation of Research Reactors

The French approach for the regulation of research reactors D. Conte, A. Chevallier Autorité de sûreté nucléaire, Paris, France Abstract. The French Nuclear Safety Authority (ASN) regulates civil nuclear facilities in France. In addition to the pool of 58 pressurized water reactors ASN also regulates several research reactors which are all unique installations. The regulatory approach for research reactors takes cognisance of the different level of hazard encountered in their operation and hence requires a different approach to the management of safety in comparison with nuclear power reactor operations. For a number of years, ASN has been striving to optimise its regulation of experimental reactors. To ensure the optimum level of safety by focusing on the most important safety issues and allowing the licensee to exercise its full responsibilities through the use of internal authorisations. The internal authorisations system, which has been in operation for several years now with a number of experimental reactors, is designed to achieve this two-fold objective. In addition to the careful use of a new range of tools for its regulatory framework in the research reactors area, ASN has other safety challenges for example the ageing of most of the existing facilities and the licensing of new reactors with a high international profile such as the Jules Horowitz reactor or the ITER fusion reactor. 1. Introduction The French Nuclear Safety Authority (ASN) regulates civil nuclear facilities in France (164). In addition to the pool of 58 pressurized water reactors ASN also regulates research reactors which are all unique installations. Most of the research reactors are operated by the atomic energy commission (CEA). -

Analysis of Advanced Sodium-Cooled Fast Reactor Core Designs with Improved Safety Characteristics

Analysis of Advanced Sodium-cooled Fast Reactor Core Designs with Improved Safety Characteristics THÈSE NO 5480 (2012) PRÉSENTÉE LE 3 SEPTEMBRE 2012 À LA FACULTÉ DES SCIENCES DE BASE LABORATOIRE DE PHYSIQUE DES RÉACTEURS ET DE COMPORTEMENT DES SYSTÈMES PROGRAMME DOCTORAL EN ENERGIE ÉCOLE POLYTECHNIQUE FÉDÉRALE DE LAUSANNE POUR L'OBTENTION DU GRADE DE DOCTEUR ÈS SCIENCES PAR Kaichao SUN acceptée sur proposition du jury: Prof. R. Schaller, président du jury Prof. R. Chawla, directeur de thèse Dr J. Krepel, rapporteur Dr A. Pautz, rapporteur Prof. J. Wallenius, rapporteur Suisse 2012 Abstract In order to meet the steadily increasing worldwide energy demand, nuclear power is expected to continue playing a key role in electricity production. Currently, the large majority of nuclear power plants are operated with thermal-neutron spectra and need regular fuel loading of enriched uranium. According to the identified conventional uranium resources and their current consumption rate, only about 100 years’ nuclear fuel supply is foreseen. A reactor operated with a fast-neutron spectrum, on the other hand, can induce self-sustaining, or even breeding, conditions for its inventory of fissile material, which effectively allow it – after the initial loading – to be refueled using simply natural or depleted uranium. This implies a much more efficient use of uranium resources. Moreover, minor actinides become fissionable in a fast-neutron spectrum, enabling full closure of the fuel cycle and leading to a minimization of long-lived radioactive wastes. The sodium-cooled fast reactor (SFR) is one of the most promising candidates to meet the Generation IV International Forum (GIF) declared goals. -

4Th International

4th International September 9-10, 2014 Sponsored by U.S. Department of Energy | Office of Fossil Energy | National Energy Technology Laboratory 1 TABLE OF CONTENTS Synopsis .................................................................................................................3 Technology Summary .............................................................................................3 Organizing Committee ............................................................................................3 Agenda-At-A-Glance ...............................................................................................4 Sheraton Station Square Floor Plan .........................................................................5 Detailed Program for Monday, September 8, 2014 ..................................................6 Detailed Program for Tuesday, September 9, 2014 ..................................................6 Detailed Program for Wednesday, September 10, 2014 ...........................................9 Speaker/Presenter Biographies .............................................................................13 2 SYNOPSIS The 4th International Supercritical CO2 Power Cycles Symposium is a technical meeting organized and designed by industry, academia, and government agencies to advance the development of power cycles with supercritical carbon dioxide (CO2) as the working fluid. Every two to three years, researchers, industry, and end users meet to learn about advancements in the field, discuss priorities, and establish -

Oversight of Research Reactors in the Southeast of France: ASN Regulatory Experience

Oversight of Research Reactors in the Southeast of France: ASN Regulatory Experience Julien Vieuble, Carole Dormant, Pierre Perdiguier Autorité de Sûreté Nucléaire (French Nuclear Safety Authority), Division de Marseille, 67/69 Avenue du Prado, 13 286 Marseille Cedex 6, France Email of the corresponding author: [email protected] The French Nuclear Safety Authority (ASN), which is an independent administrative authority, is in charge of regulating nuclear safety and radiation protection in order to protect workers, patients, the public and the environment from the risks associated with nuclear activities. ASN also contributes to the public information and the promotion of transparency and openness among stakeholders. The key values of ASN are independence, competence, rigor and transparency, enabling its 450 staff to perform their various duties with the needed legitimacy. ASN’s oversight covers more than 160 civil basic nuclear installations all over France. These installations are of very different varieties and sizes: nuclear power plants, research reactors, nuclear laboratories, fuel cycle facilities, and at different stages in their lives: conception, construction, operation, dismantling. ASN also oversees the safety of radioactive material transport. The ASN division of Marseille oversees the nuclear civil activities in the southeast area of France, which covers, inter alia, the nuclear site of Marcoule (4 civil nuclear installations) and the nuclear site of Cadarache (20 civil nuclear installations). The French public Atomic Energy Commission (CEA) has nine research reactors currently in operation: six of them are located in the southeast of France, and a new one, the Jules Horowitz reactor (JHR), is under construction on the nuclear site of Cadarache. -

Plutonium for Energy? Explaining the Glo1bal Decline of MOX

Stichting Laka: Documentatie- en onderzoekscentrum kernenergie De Laka-bibliotheek The Laka-library Dit is een pdf van één van de publicaties in This is a PDF from one of the publications de bibliotheek van Stichting Laka, het in from the library of the Laka Foundation; the Amsterdam gevestigde documentatie- en Amsterdam-based documentation and onderzoekscentrum kernenergie. research centre on nuclear energy. Laka heeft een bibliotheek met ongeveer The Laka library consists of about 8,000 8000 boeken (waarvan een gedeelte dus ook books (of which a part is available as PDF), als pdf), duizenden kranten- en tijdschriften- thousands of newspaper clippings, hundreds artikelen, honderden tijdschriftentitels, of magazines, posters, video's and other posters, video’s en ander beeldmateriaal. material. Laka digitaliseert (oude) tijdschriften en Laka digitizes books and magazines from the boeken uit de internationale antikernenergie- international movement against nuclear beweging. power. De catalogus van de Laka-bibliotheek staat The catalogue of the Laka-library can be op onze site. De collectie bevat een grote found at our website. The collection also verzameling gedigitaliseerde tijdschriften uit contains a large number of digitized de Nederlandse antikernenergie-beweging en magazines from the Dutch anti-nuclear power een verzameling video's. movement and a video-section. Laka speelt met oa. haar informatie- Laka plays with, amongst others things, its voorziening een belangrijke rol in de information services, an important role in the Nederlandse anti-kernenergiebeweging. Dutch anti-nuclear movement. Appreciate our work? Feel free to make a small donation. Thank you. www.laka.org | [email protected] | Ketelhuisplein 43, 1054 RD Amsterdam | 020-6168294 Plutonium for Energy? Explaining the Glo1bal Decline of MOX A Policy Research Project of the LBJ School ojf Public Affairs University of 'Texas at Austin dNl� NUCLEAR9 PIROLIFERATION�· PREVENT rN PROJECT � th,· llmv•:r'''iof lc••• •• t\u"'" Edited by Alan J. -

Npr 2.3: an Assessment of Iran's Nuclear Facilities

Report Report: AN ASSESSMENT OF IRAN’S NUCLEAR FACILITIES by Greg J. Gerardi and Maryam Aharinejad Greg J. Gerardi is a Senior Research Associate of the Center for Nonproliferation Studies (CNS) at the Monterey Institute of International Studies. Maryam Aharinejad was a Research Associate at CNS; she is currently an intern at the United Nations’ Centre for Disarmament Affairs. uch press has been given to the perceived threat was no contract for a centrifuge, Yeltsin later conceded posed by Iran’s nuclear developments. In par- this point of the deal stating that: Mticular, Russia’s agreement to complete Unit ...the contract indeed has elements of both One of the nuclear complex at Bushehr, begun by the peaceful and military power engineering. Now Germans in the late 1970s, and reports of China’s assis- we have agreed to separate them, and what tance in the building of additional power reactors have bears on the military part, the possibility of strained relations between the United States and these creating, say, nuclear-weapons-grade fuel or two countries. The protocol for the completion of the other matters—the centrifuge, the building of Bushehr plant, signed by Russian nuclear energy minis- mines—we decided to exclude these matters ter Viktor Mikhailov and the President of the Atomic from the contract....2 Energy Organization of Iran (AEOI) Reza Amrollahi on U.S. concern about the transfer of any nuclear January 8, 1995, also calls on the two signatory organi- technology to Iran is based on the belief that zations to draft and sign: Iran has a clandestine nuclear weapon develop- ...within a six month period of time, a con- ment program. -

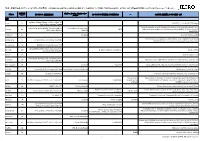

(C) 2010 JETRO. All Rights Reserved. 水力

別添 発電所案件のEPC, コントラクター等の動向 (注)情報収集が可能であった発電所のみ記載。また、各発電所について記載してある内容は全体の一部であり、全ての関連企業を掲載したものではありません。何卒ご了承下さい。 設備容量 ボイラー、タービン、ジェネレーター プラント ファイナンス (融資銀行含む) コンサルタント(詳細設計、F/S業務含む) EPC 土木工事、機器据付、システム設計 など (MW) メーカー 水力 Agribank, Vietnam-Thailand JV Bank, An Binh JSCl A Luoi 170 CAVICO, CTTE, LILAMA PECC3(Design) Bank, Rubber Financing Company Licogi, Construction corp No.4, Lung Lo Construction corp, Central Construction corp, Vietcombank, Agribank, BIDV, Incombank,Citicorp, Power Machine Group(Russia), A Vuong 210 PECC2 National research institute of mechanical engineering, LILAMA, AF-Colenco(Design), BNP Paribas, ABN Amro Mitsubishi Sika(PVC Bar) An Khe #2 80 Dongfang Song Da, Dat Phuong JSC PECC4(Construction supervision), CONSTREXIM, HUBEI HONGCHENG GENERAL An Khe Kanak 177 BIDV,Agribank, Vietcombank, Incombank MACHINERY CO., LTD., Sichuan Dongfang electric equipment corp. Ba Thuoc 1,2 120 BIDV(60%), Hoang Anh Gia Lai(40%) Agribank(56%), BIDV, Vietcombank, Global Petro Ban Chat 220 Electric Construction Consultancy 1 Licogi, CAVICO Commercial Joint Stock Bank. Ban Ve 300 Song Da, Cavico, Licogi Vietcombank, Agribank, BIDV, Incombank,Citicorp, Buon Kuop 280 Vinaconex, Cavico, CONSTREXIM, Construction Corporation No.1, Sika(PVC Bar) BNP Paribas, ABN Amro Buon Tua Srah 86 Dongfang PECC4(F/S) Lilama, CONSTREXIM, PECC4(Design, Appraisal bid documents), Sika(PVC Bar) Can Don 77.5 Incombank, BIDV, International JSC Bank Power Machine Group, UETM(Russia) Ukrhydroproject, Song Da, Lilama Cua Dat 99 VINACONEX, BNP Paribas Vinaconex, China National -

Marine Nuclear Power: 1939 – 2018

Marine Nuclear Power: 1939 – 2018 Part 3B: Russia - Surface Ships & Non-propulsion Marine Nuclear Applications Peter Lobner July 2018 1 Foreword In 2015, I compiled the first edition of this resource document to support a presentation I made in August 2015 to The Lyncean Group of San Diego (www.lynceans.org) commemorating the 60th anniversary of the world’s first “underway on nuclear power” by USS Nautilus on 17 January 1955. That presentation to the Lyncean Group, “60 years of Marine Nuclear Power: 1955 – 2015,” was my attempt to tell a complex story, starting from the early origins of the US Navy’s interest in marine nuclear propulsion in 1939, resetting the clock on 17 January 1955 with USS Nautilus’ historic first voyage, and then tracing the development and exploitation of marine nuclear power over the next 60 years in a remarkable variety of military and civilian vessels created by eight nations. In July 2018, I finished a complete update of the resource document and changed the title to, “Marine Nuclear Power: 1939 – 2018.” What you have here is Part 3B: Russia - Surface Ships & Non-propulsion Marine Nuclear Applications. The other parts are: Part 1: Introduction Part 2A: United States - Submarines Part 2B: United States - Surface Ships Part 3A: Russia - Submarines Part 4: Europe & Canada Part 5: China, India, Japan and Other Nations Part 6: Arctic Operations 2 Foreword This resource document was compiled from unclassified, open sources in the public domain. I acknowledge the great amount of work done by others who have published material in print or posted information on the internet pertaining to international marine nuclear propulsion programs, naval and civilian nuclear powered vessels, naval weapons systems, and other marine nuclear applications.