Dismiss Modern Monetary Theory at Your Peril

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Former Fed Chiefs Weigh In

JULY 17 2020 Former Fed chiefs weigh in Ben Bernanke and Janet Yellen have hardly been quiet since they left their positions as heads of the Federal Reserve. Whether in media, articles or, recently, as part of a group of 150 economists who wrote a letter to Congress, the two have remained public figures. It has been some time since they testified before lawmakers, however. Appearing twice a year to committees in both the House and the Senate was part of the job back then; Friday marked the first required appearances for each since they left their posts. Paige Wilhelm Given Yellen and Bernanke’s support for Jerome Powell, the current Fed Senior Vice President Senior Portfolio Manager chair, it is no surprise they praised the Fed’s actions so far in the crisis or Federated Investment Counseling that they echoed his call for Congress to provide more fiscal support to the economy. The overarching message for lawmakers was do not worry about the deficit at this time—the economy needs assistance now. One thing is certain, the Fed is not worried about its own balance sheet. This week it revealed that figure now stands at more than $7 trillion. Interestingly, the special purpose vehicles it created in the height of the crisis in March are hardly being used now. These include the Primary Dealer Credit Facility and the Money Market Liquidity Facility. This is a good sign, as it means the liquidity markets are functioning well on their own. But the greater economy probably will require Congress’s assistance to do the same. -

Is the Fed Too Active?

OPINION BY KARTIK ATHREYA Is the Fed Too Active? ome observers have recently voiced concern that Fed So the goal of redressing at least some aspects of activities in the areas of climate change and inequal- economic inequality has long been a Fed concern. Indeed, Sity may put the institution at risk. In a forthcoming the Richmond Fed strives to understand the full range of Duke Law Journal article, for instance, Christina Parajon economic outcomes of Fifth District residents, including Skinner of the University of Pennsylvania’s Wharton School inequities, and among them, those that occur along racial argues that the Fed must avoid the temptation to engage in lines. To fail here would hinder our ability to fulfill our “central bank activism” by pushing its powers beyond the mandate under the CRA and to provide better informa- text and purpose of its legal mandate to address “imme- tion via the Beige Book and other means to guide mone - diate public policy problems” such as climate change tary policy. As Richmond Fed President Tom Barkin and economic inequality. She cautions, “Activism under- has pointed out, “The regional Fed banks are charged mines the legitimacy of central bank authority, with understanding the dynamics within our erodes its political independence, and ultimately “We should districts. In pursuit of that goal, we have been renders a weaker central bank.” In a recent Wall investing in research that addresses these Street Journal op-ed, Michael Belongia of the always strive to issues and the racial inequities that result.” University of Mississippi and Peter Ireland of understand forces Lately, the connection between mone- Boston College voiced similar concerns about Fed that plausibly tary policy and economic inclusion has drawn activities in the area of income inequality. -

The Impact of Capital Market on the Economic Growth in Oman

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Alam, Md. Shabbir; Hussein, Muawya Ahmed Article The impact of capital market on the economic growth in Oman Financial Studies Provided in Cooperation with: "Victor Slăvescu" Centre for Financial and Monetary Research, National Institute of Economic Research (INCE), Romanian Academy Suggested Citation: Alam, Md. Shabbir; Hussein, Muawya Ahmed (2019) : The impact of capital market on the economic growth in Oman, Financial Studies, ISSN 2066-6071, Romanian Academy, National Institute of Economic Research (INCE), "Victor Slăvescu" Centre for Financial and Monetary Research, Bucharest, Vol. 23, Iss. 2 (84), pp. 117-129 This Version is available at: http://hdl.handle.net/10419/231680 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. -

A REVIEW of IRANIAN STAGFLATION by Hossein Salehi

THE HISTORY OF STAGFLATION: A REVIEW OF IRANIAN STAGFLATION by Hossein Salehi, M. Sc. A Thesis In ECONOMICS Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Requirements for the Degree of MASTER OF ARTS Approved Dr. Masha Rahnama Chair of Committee Dr. Eleanor Von Ende Dr. Mark Sheridan Dean of the Graduate School August, 2015 Copyright 2015, Hossein Salehi Texas Tech University, Hossein Salehi, August, 2015 ACKNOWLEDGMENTS First and foremost, I wish to thank my wonderful parents who have been endlessly supporting me along the way, and I would like to thank my sister for her unlimited love. Next, I would like to show my deep gratitude to Dr. Masha Rahnama, my thesis advisor, for his patient guidance and encouragement throughout my thesis and graduate studies at Texas Tech University. My sincerest appreciation goes to, Dr. Von Ende, for joining my thesis committee, providing valuable assistance, and devoting her invaluable time to complete this thesis. I also would like to thank Brian Spreng for his positive input and guidance. You all have my sincerest respect. ii Texas Tech University, Hossein Salehi, August, 2015 TABLE OF CONTENTS ACKNOWLEDGMENTS .................................................................................................. ii ABSTRACT ........................................................................................................................ v LIST OF FIGURES .......................................................................................................... -

A Primer on Modern Monetary Theory

2021 A Primer on Modern Monetary Theory Steven Globerman fraserinstitute.org Contents Executive Summary / i 1. Introducing Modern Monetary Theory / 1 2. Implementing MMT / 4 3. Has Canada Adopted MMT? / 10 4. Proposed Economic and Social Justifications for MMT / 17 5. MMT and Inflation / 23 Concluding Comments / 27 References / 29 About the author / 33 Acknowledgments / 33 Publishing information / 34 Supporting the Fraser Institute / 35 Purpose, funding, and independence / 35 About the Fraser Institute / 36 Editorial Advisory Board / 37 fraserinstitute.org fraserinstitute.org Executive Summary Modern Monetary Theory (MMT) is a policy model for funding govern- ment spending. While MMT is not new, it has recently received wide- spread attention, particularly as government spending has increased dramatically in response to the ongoing COVID-19 crisis and concerns grow about how to pay for this increased spending. The essential message of MMT is that there is no financial constraint on government spending as long as a country is a sovereign issuer of cur- rency and does not tie the value of its currency to another currency. Both Canada and the US are examples of countries that are sovereign issuers of currency. In principle, being a sovereign issuer of currency endows the government with the ability to borrow money from the country’s cen- tral bank. The central bank can effectively credit the government’s bank account at the central bank for an unlimited amount of money without either charging the government interest or, indeed, demanding repayment of the government bonds the central bank has acquired. In 2020, the cen- tral banks in both Canada and the US bought a disproportionately large share of government bonds compared to previous years, which has led some observers to argue that the governments of Canada and the United States are practicing MMT. -

Neo-Liberalism As Financialisation1 Engaging Neo-Liberalism When It

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by SOAS Research Online Neo-liberalism as Financialisation 1 Engaging Neo-liberalism When it first emerged, neo-liberalism seemed to be able to be defined relatively easily and uncontroversially. In the economic arena, the contrast could be made with Keynesianism and emphasis placed on perfectly working markets. A correspondingly distinctive stance could be made over the role of the state as corrupt, rent-seeking and inefficient as opposed to benevolent and progressive. Ideologically, the individual pursuit of self-interest as the means to freedom was offered in contrast to collectivism. And, politically, Reaganism and Thatcherism came to the fore. It is also significant that neo-liberalism should emerge soon after the post-war boom came to an end, together with the collapse of the Bretton Woods system of fixed exchange rates. This is all thirty or more years ago and, whilst neo-liberalism has entered the scholarly if not popular lexicon, it is now debatable whether it is now or, indeed, ever was clearly defined. How does it fair alongside globalisation, the new world order, and the new imperialism, for example, as descriptors of contemporary capitalism. Does each of these refer to a similar understanding but with different terms and emphasis? And how do we situate neo-liberalism in relation to Third Wayism, the social market, and so on, whose politicians, theorists and ideologues would pride themselves as departing from neo- liberalism but who, in their politics and policies, seem at least in part to have been captured by it (and even vice-versa in some instances)? These conundrums in the understanding and nature of neo-liberalism have been highlighted by James Ferguson (2007) who reveals how what would traditionally be termed progressive policies (a basic income grant for example) have been rationalised through neo-liberal discourse. -

Scope and Function of the Capital Market in the American Economy

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: The Flow of Capital Funds in the Postwar Economy Volume Author/Editor: Raymond W. Goldsmith Volume Publisher: NBER Volume ISBN: 0-870-14112-0 Volume URL: http://www.nber.org/books/gold65-1 Publication Date: 1965 Chapter Title: Scope and Function of the Capital Market in the American Economy Chapter Author: Raymond W. Goldsmith Chapter URL: http://www.nber.org/chapters/c1680 Chapter pages in book: (p. 22 - 42) CHAPTER 1 Scope and Function of the Capital Market in the American Economy Origin of the Capital Market in the Separation of Saving and Investment A MARKET for new capital, apart from transactions in existing finan- cial and real assets, exists because in a modern economy saving (the excess of current income over current expenditures on consumption) is to a large extent separated from investment, i.e., expenditures on durable assets usually defined as new construction, equipment, and additionstoinventories and excluding education,research, and health.1 In any given period every economic unit either saves or dissaves— if we ignore the relatively few units whose current expenditures ex- actly balance their current income; and most units make capital expenditures, which usually involve payments to other units for fin- ished durable goods, materials, or labor, but which may also be internal and imputed (e.g., Crusoe building his boat). Both saving and investment may be calculated gross or net of capital consumption allowances or retirements. Since these diminish saving and investment equally, the difference between saving and investment is the same whether calculated on a gross or net basis. -

Modern Monetary Theory: a Marxist Critique

Class, Race and Corporate Power Volume 7 Issue 1 Article 1 2019 Modern Monetary Theory: A Marxist Critique Michael Roberts [email protected] Follow this and additional works at: https://digitalcommons.fiu.edu/classracecorporatepower Part of the Economics Commons Recommended Citation Roberts, Michael (2019) "Modern Monetary Theory: A Marxist Critique," Class, Race and Corporate Power: Vol. 7 : Iss. 1 , Article 1. DOI: 10.25148/CRCP.7.1.008316 Available at: https://digitalcommons.fiu.edu/classracecorporatepower/vol7/iss1/1 This work is brought to you for free and open access by the College of Arts, Sciences & Education at FIU Digital Commons. It has been accepted for inclusion in Class, Race and Corporate Power by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. Modern Monetary Theory: A Marxist Critique Abstract Compiled from a series of blog posts which can be found at "The Next Recession." Modern monetary theory (MMT) has become flavor of the time among many leftist economic views in recent years. MMT has some traction in the left as it appears to offer theoretical support for policies of fiscal spending funded yb central bank money and running up budget deficits and public debt without earf of crises – and thus backing policies of government spending on infrastructure projects, job creation and industry in direct contrast to neoliberal mainstream policies of austerity and minimal government intervention. Here I will offer my view on the worth of MMT and its policy implications for the labor movement. First, I’ll try and give broad outline to bring out the similarities and difference with Marx’s monetary theory. -

Transcript of Chair Powell's Press Conference -- January 29, 2020

January 29, 2020 Chair Powell’s Press Conference FINAL Transcript of Chair Powell’s Press Conference January 29, 2020 CHAIR POWELL. Good afternoon, everyone. Thanks for being here. At today’s meeting, my colleagues and I decided to leave our policy rate unchanged. As always, we base our decisions on our judgment of how best to achieve the goals Congress has given us: maximum employment and price stability. We believe monetary policy is well positioned to serve the American people by supporting continued economic growth, a strong job market, and a return of inflation to our symmetric 2 percent goal. The expansion is in its 11th year, the longest on record. Growth in household spending moderated toward the end of last year, but with a healthy job market, rising incomes, and upbeat consumer confidence, the fundamentals supporting household spending are solid. In contrast, business investment and exports remain weak, and manufacturing output has declined over the past year. Sluggish growth abroad and trade developments have been weighing on activity in these sectors. However, some of the uncertainties around trade have diminished recently, and there are some signs that global growth may be stabilizing after declining since mid-2018. Nonetheless, uncertainties about the outlook remain, including those posed by the new coronavirus. Overall, with monetary and financial conditions supportive, we expect moderate economic growth to continue. The unemployment rate has been near half-century lows for well more than a year, and the pace of job gains remains solid. Participation in the labor force by people in their prime working years, ages 25 to 54, is at its highest level in more than a decade. -

Meet the New Boss, Same As the Old Boss (Part II)

Samuel Miller CFA, CAIA Senior Analyst Deron T. McCoy CFA, CFP®, CAIA, AIF® Chief Investment Officer Meet the New Boss, Same as the Old Boss (Part II) Four years ago in our December 2013 SEIA Report titled, “The Federal Reserve: Meet the New Boss, Same as the Old Boss”, we offered reasons why analyzing the human makeup of the Board is so important (hint: they more or less set monetary policy for the world, affecting global capital markets everywhere). We opined that the new incoming Federal Reserve Chair Janet Yellen was very much in line with her predecessor and that her appointment was a “signal to all investors that easy monetary policy will be the policy of choice for the foreseeable future” and “short-term interest rates might be low for another three years extending through 2016.” We concluded by stating “Yellen’s policies should support ‘risk assets’ (Equities, High Yield Bonds, etc.) in the near term with her hopeful goal of higher inflation and economic overheating (not a typo) four years out which will in turn convolute her reappointment process (in 2017).” Four years have now passed and while we can claim victory on our assessment of the stock market, our view of an overheated economy came up a bit short. As such, the reappointment process caused nary a ripple in global markets as the new-new boss is the same as the old-old boss. Who is Jerome Powell? On November 2, 2017, President Trump nominated Jerome “Jay” Powell to be the next Fed chair, providing clarification for the market and lessening monetary policy uncertainty in the near and intermediate term. -

Regime Change Q2 2018 COMMENTARY

Chief Market Strategist, Dr. Quincy Krosby Prudential Financial Regime Change Q2 2018 COMMENTARY The second quarter— Highlights which statistically • Federal Reserve chairman Jerome Powell takes the helm is not the most • A brief history of recent regime changes at the Federal Reserve • The market enters a period of crosscurrents hospitable in terms of returns—should enjoy Q2 OPENING BELL solid growth here The term “regime change” is currently trending in the headlines, from “More expect Venezuela will collapse and have regime change within 12 months” to “Pushing back against Iran: Is it time and abroad; solid, if for regime change?” As we enter the second quarter of 2018, however, the term is increasingly not stellar, earnings; used to describe a subtle but equally important shift in economic policy. Monetary policy stands out as a significant economic catalyst, and with the departure of Federal Reserve Chair Janet the fiscal stimulus Yellen, we’ve seen headlines blare: “How to survive the regime change in markets.” beginning to filter into Referring to February’s market correction, triggered by fears that inflation was beginning to assert itself, the Financial Times succinctly stated: “Whether correction turns into regime the real economy; and change is down to the Fed.” But do members of the Federal Open Market Committee (FOMC) a Federal Reserve of the Federal Reserve view their job as protectors of stock market performance, the way they seemingly did coming out of the financial crisis? that wants to maintain Newly installed Fed Chairman Jerome Powell, greeted on his first official day with a 4 percent the “middle ground” market sell-off, appeared upbeat about prospects for the economy. -

Apresentação Do Powerpoint

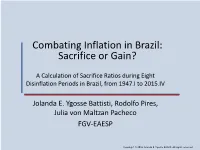

Combating Inflation in Brazil: Sacrifice or Gain? A Calculation of Sacrifice Ratios during Eight Disinflation Periods in Brazil, from 1947.I to 2015.IV Jolanda E. Ygosse Battisti, Rodolfo Pires, Julia von Maltzan Pacheco FGV-EAESP Copyright © 2016 Jolanda E. Ygosse Battisti. All rights reserved Introduction Objective of the paper … to calculate sacrifice ratios for policy-induced inflationary and disinflationary periods, using data on the Brazilian economy from 1947 to 2015. Why do we care? … inflation is costly for society. However, actively combating inflation can also be costly, especially in the short run, resulting in a policy dilemma. Main result … perhaps surprisingly, combating inflation does not necessarily imply a loss of output and jobs in Brazil. Especially when inflation is a fiscal phenomenon, the sacrifice ratio is inverted. This is good news for policy makers 4000 CONTEXT 3750 Consumer Price Index (IPC) 3500 in Brazil, 1912(1)-2015(1) (in log x 100; 1912=0) 3250 Real Plan 3000 2750 IPC (1939=100) 2500 Average annual inflation rate of 2250 54% before the Real Plan, and 2000 6,4% since the Real Plan 1750 1500 in ln, normalized for 1912=0 (x100) 1912=0 fornormalized in ln, 1250 1000 750 500 250 0 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 Source: Data from Mitchell (1998); IPEADATA, IPC-FIPE; and author´s calculations. Year Copyright © 2014 Jolanda E. Ygosse Battisti. All rights reserved 200 CONTEXT 175 Monthly Inflation Rate in Brazil 1912-1980, annualized 150 Crisis of the in %, annualizedin %, Sixties Monthly Inflation Monthly 125 WWII 100 High inflation was 75 common, since the 1940s … 50 25 0 -25 (for comparison, current IT 4,5% p.y.) Deflation -50 (Great Depression USA) 1920 1930 1940 1950 1960 1970 1980 Source: Data from Mitchell (1998); IPEADATA, IPC-FIPE; author´s calculations.