Corporate Board Governance and Director Compensation in Canada

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

CDP NON-DISCLOSURE CAMPAIGN: 2020 RESULTS Measuring the Impact of Investor Engagement on Corporate Environmental Disclosure

DISCLOSURE INSIGHT ACTION CDP NON-DISCLOSURE CAMPAIGN: 2020 RESULTS Measuring the impact of investor engagement on corporate environmental disclosure WWW.CDP.NET CONTENTS CDP NON-DISCLOSURE CAMPAIGN 2 Introduction In the fight against climate change, 2020 ended with perhaps more 3 Non-Disclosure Campaign overview optimism than it started with. Analysts predict that recent net-zero Good disclosure enables pledges made by several countries, including China and the incoming US 5 2020 campaign disclosure results investors to assess how well administration, could, if achieved, limit global temperature rise to around companies manage their 2.1 degrees by the end of the century - around a degree lower than the 19 Regional focus ESG risks. CDP now reflects trajectory of current policies1. This could bring the world within striking 11 Climate change TCFD requirements and is a distance of the well below 1.5 degree target set out in the Paris Agreement. However, figures recently released from Brazil’s National 13 Forests model disclosure framework Institute for Space Research (INPE) show that deforestation in one of the 5 1 Water security on climate change, one of world’s largest carbon sinks has increased by 9.5% over the past year, the broadest risks facing with 11,088 km2 of Amazonian forest being destroyed. 17 Sectoral focus companies. We encourage all 19 Climate change companies to respond fully to Greater action is needed if the world is to avoid the worst effects of 21 Forests the CDP questionnaire. catastrophic climate change. The capital markets and corporate sector have a vital role to play. -

Power to Do More

2018 2018 Annual Report Annual Report @BoralexInc boralex.com POWER TO DO MORE NOTICE of Annual Meeting of Shareholders Management proxy CIRCULAR 2018 Our thanks to the employees who accepted to appear on the cover page: Van Anh Dang Vu (Kingsey Falls, Québec), Myriam Savage (Thetford Mines, Québec) and Ernani Schnorenberger (Lyon, France). PROFILE Boralex develops, builds and operates renewable energy power facilities in Canada, France, the United Kingdom and the United States. A leader in the Canadian market and France’s largest independent producer of onshore wind power, the Corporation is recognized for its solid experience in optimizing its asset base in four power generation types – wind, hydroelectric, thermal and solar. Boralex has ensured sustained growth by leveraging the expertise and diversification developed for more than 25 years. General HEAD OFFICE WEBSITE www.boralex.com Boralex Inc. Information 36 Lajeunesse Street Kingsey Falls (Québec) Canada J0A 1B0 @BoralexInc Telephone: 819-363-6363 Fax: 819-363-6399 [email protected] BUSINESS OFFICES CANADA UNITED STATES 900 de Maisonneuve Boulevard West 606-1155 Robson Street 39 Hudson Falls Street 24th floor Vancouver, British Columbia South Glens Falls New York Montréal, Québec Canada V6E 1B5 12803 Canada H3A 0A8 Telephone: 1-855-604-6403 United States Telephone: 514-284-9890 Telephone: 518-747-0930 Fax: 514-284-9895 201-174 Mill Street Fax: 518-747-2409 Milton, Ontario Canada L9T 1S2 Telephone: 819-363-6430 | 1-844-363-6430 FRANCE UNITED KINGDOM 71, rue Jean-Jaurès -

STOXX Canada 240 Last Updated: 02.10.2017

STOXX Canada 240 Last Updated: 02.10.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) CA7800871021 2754383 RY.TO RY Royal Bank of Canada CA CAD Y 95.2 1 1 CA8911605092 2897222 TD.TO TDpD Toronto-Dominion Bank CA CAD Y 87.8 2 2 CA0641491075 2076281 BNS.TO BNS Bank of Nova Scotia CA CAD Y 65.0 3 3 CA29250N1050 2466149 ENB.TO IPL Enbridge Inc. CA CAD Y 57.8 4 4 CA8672241079 B3NB1P2 SU.TO T.SU Suncor Energy Inc. CA CAD Y 49.2 5 6 CA1363751027 2180632 CNR.TO TCNR Canadian National Railway Co. CA CAD Y 45.7 6 5 CA0636711016 2076009 BMO.TO BMO Bank of Montreal CA CAD Y 41.6 7 7 CA89353D1078 2665184 TRP.TO TRP TransCanada Corp. CA CAD Y 36.3 8 8 CA05534B7604 B188TH2 BCE.TO B BCE Inc. CA CAD Y 35.6 9 9 CA56501R1064 2492519 MFC.TO 274642 Manulife Financial Corp. CA CAD Y 33.9 10 10 CA1360691010 2170525 CM.TO 217052 Canadian Imperial Bank of Comm CA CAD Y 32.2 11 13 CA1363851017 2171573 CNQ.TO TCNQ Canadian Natural Resources Ltd CA CAD Y 31.6 12 12 CA1125851040 2092599 BAMa.TO TEBC.A BROOKFIELD ASSET MANAGEMENT CA CAD Y 31.5 13 11 CA13645T1003 2793115 CP.TO 279311 Canadian Pacific Railway Ltd. CA CAD Y 20.8 14 15 CA8667961053 2566124 SLF.TO 256612 Sun Life Financial Inc. CA CAD Y 20.6 15 14 CA87971M1032 2381093 T.TO BCT TELUS CA CAD Y 18.0 16 16 CA01626P4033 2011646 ATDb.TO 201164 ALIMENTATION CCH.TARD CA CAD Y 16.2 17 18 CA5592224011 2554475 MG.TO MG.A Magna International Inc. -

Expansion in Full Swing

20 Expansion 20 in full swing Positioning for sustainable growth LE MEILLEUR DE NOS Management FORCES Information CIRCULAR NOTICE of Annual Meeting of Shareholders Notice of Annual Meeting of Shareholders Dear shareholders, We invite you to attend Boralex Inc.’s 2020 annual meeting of shareholders. Items of business When The meeting will be held for the following purposes: May 5, 2021 1. Receive the consolidated financial statements of the 11:00 a.m. (Eastern Daylight Time) Corporation for the financial year ended December 31, 2020 and the independent auditor’s report thereon 2. Elect the directors 3. Appoint the independent auditor Where 4. Adopt a non-binding advisory resolution, the text of which is Virtual meeting via live audio webcast at reproduced on page 15 of the management information circular, https://web.lumiagm.com/262304484 accepting our approach to executive compensation 5. Adopt a resolution, the text of which is reproduced on page 156 of the management information circular, reconfirming and renewing the shareholder rights plan adopted by the board of directors on March 1, 2018 Materials A notice of availability of proxy materials 6. Consider any other business that may properly come before the for our 2020 annual meeting is being meeting or any adjournment thereof. mailed to shareholders on or about March 26, 2021. Notice-and-Access We are providing access to the meeting This year, as permitted by Canadian corporate and securities Materials, the Financial Statements and regulators, Boralex Inc. is using notice-and-access to deliver the annual report to both our registered management information circular of Boralex Inc. -

1 2 March 2021 Flutter Entertainment

2 March 2021 Flutter Entertainment plc - 2020 Preliminary Results Transformational year for Group; Earnings ahead of expectations Flutter Entertainment plc (the “Group”) announces preliminary results for year ended 31 December 2020. Reported1 Pro forma2 2020 2019 2020 2019 CC3 £m £m YoY % £m £m YoY % YoY % Group revenue4 4,398 2,140 +106% 5,264 4,144 +27% +28% Adjusted5 Group EBITDA6 excluding US 1,037 462 +125% 1,401 1,170 +20% +23% Adjusted Group EBITDA 889 425 +109% 1,231 1,089 +13% +16% Profit before tax 1 136 -99% Earnings per share7 29.3p 180.2p -84% Adjusted earnings per share 402.7p 298.4p +35% 496.6p 415.7p +19% Net debt at year end8 2,814 265 Operational highlights • Transformational year for Group - Unparalleled scale and diversification achieved following merger with The Stars Group, Inc (“TSG”) - Accelerated buy-out of minority shareholders in FanDuel at compelling valuation - Reinforced balance sheet to support investment and growth • Excellent momentum with 19% growth in recreational players9 across Group - Acceleration of channel shift from retail to online and increased share of entertainment spend • Further investment in safer gambling initiatives to ensure sustainable growth - Enhanced predictive technology; increase in safer gambling tool usage by customers - Advocating a customer driven approach to affordability • Merger integration progressing well - Australian integration complete, PokerStars strategy in place and core momentum maintained - Annualised cost synergies now expected to be £170m, up from £140m previously -

OSC Bulletin Volume 42, Issue 14 (April 4, 2019)

The Ontario Securities Commission OSC Bulletin April 4, 2019 Volume 42, Issue 14 (2019), 42 OSCB The Ontario Securities Commission administers the Securities Act of Ontario (R.S.O. 1990, c. S.5) and the Commodity Futures Act of Ontario (R.S.O. 1990, c. C.20) The Ontario Securities Commission Published under the authority of the Commission by: Cadillac Fairview Tower Thomson Reuters 22nd Floor, Box 55 One Corporate Plaza 20 Queen Street West 2075 Kennedy Road Toronto, Ontario Toronto, Ontario M5H 3S8 M1T 3V4 416-593-8314 or Toll Free 1-877-785-1555 416-609-3800 or 1-800-387-5164 Contact Centre – Inquiries, Complaints: Fax: 416-593-8122 TTY: 1-866-827-1295 Office of the Secretary: Fax: 416-593-2318 The OSC Bulletin is published weekly by Thomson Reuters Canada, under the authority of the Ontario Securities Commission. Thomson Reuters Canada offers every issue of the Bulletin, from 1994 onwards, fully searchable on SecuritiesSource™, Canada’s pre-eminent web-based securities resource. SecuritiesSource™ also features comprehensive securities legislation, expert analysis, precedents and a weekly Newsletter. For more information on SecuritiesSource™, as well as ordering information, please go to: http://www.westlawecarswell.com/SecuritiesSource/News/default.htm or call Thomson Reuters Canada Customer Support at 1-416-609-3800 (Toronto & International) or 1-800-387-5164 (Toll Free Canada & U.S.). Claims from bona fide subscribers for missing issues will be honoured by Thomson Reuters Canada up to one month from publication date. Space is available in the Ontario Securities Commission Bulletin for advertisements. The publisher will accept advertising aimed at the securities industry or financial community in Canada. -

Frontiers Canadian Equity Pool Interim Management Report of Fund Performance

Frontiers Canadian Equity Pool Interim Management Report of Fund Performance for the period ended February 29, 2016 All figures are reported in Canadian dollars unless otherwise noted. This interim management report of fund performance contains financial highlights but does not contain either the complete interim or annual financial statements of the investment fund. If you have not received a copy of the interim financial reports with this interim management report of fund performance, you can get a copy of the interim financial reports or annual financial statements at your request, and at no cost, by calling us toll-free at 1-888-888-3863, by writing to us at Renaissance Investments, 1500 Robert-Bourassa Boulevard, Suite 800, Montreal, QC, H3A 3S6, by visiting the SEDAR website at sedar.com, or by visiting renaissanceinvestments.ca. Unitholders may also contact us using one of these methods to request a copy of the investment fund’s proxy voting policies and procedures, proxy voting disclosure record, or quarterly portfolio disclosure. Management Discussion of Fund Performance . Results of Operations CIBC Asset Management Inc. (CAMI,theManager, or Portfolio Global economic growth remained slow over the period. Concerns Advisor), Picton Mahoney Asset Management (Picton Mahoney), about China’s economic growth and U.S. Federal Reserve Board Triasima Portfolio Management Inc. (Triasima), Connor, Clark & Lunn policy were the two largest factors weighing on the global economic Investment Management Ltd. (CC&L) and Foyston, Gordon & Payne outlook. Commodity prices continued to fall, worsened by a Inc. (Foyston) provide investment advice and investment management strengthening U.S. dollar. Slow global growth and plunging oil prices services to Frontiers Canadian Equity Pool (the Pool). -

Canada Capital Markets Review

Canada Capital Markets Review FIRST HALF 2019 | MANAGING UNDERWRITERS Canada Capital Markets Review First Half 2019 | Managing Underwriters Global Deals Intelligence Canada Debt Capital Markets Issuance (C$bil) $200 350 Canadian Debt Capital Markets $180 Overall Canadian DCM issuance (excluding self-funded deals) totaled C$91.5 billion in the first half of 300 2019, a 4% decrease from the year prior. On a quarter-over-quarter basis, proceeds fell by 3% and the $160 number of issues fell by 7% and 10% on a year-over-year and quarter-over-quarter basis respectively. $140 250 Government and Agency debt led the market, with a 59% share of overall issuance at the end of the first six months. Financials and Energy & Power followed, with 21% and 10% market shares, $120 respectively. 200 $100 RBC placed first in nearly all Canadian rankings in the first half, including Canadian All Debt (including 150 & excluding self-funded), Canadian Domestic Corporate Debt (including and excluding self-funded), $80 Canadian Domestic Government Debt (True Economics), and Canadian Cross Border transactions. National Bank placed first in Canadian Domestic Government Debt (Full Credit). $60 100 Overall, the top corporate deals list for the first six months, exclusive of self-funded issues, was led by $40 Hydro One with C$1.5 billion of issuance, followed by Enbride Pipelines with $1.2 billion, and 50 Northwestern Hydro with C$1.1 billion. $20 Canadian Equity Capital Markets $0 0 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Canadian Equity & Equity-Related issuance (excluding self-led issuance) totaled C$11.6 billion from Q1 Q2 Q3 Q4 H1 # of Deals 137 issues in the first half, representing a 33% decrease in total proceeds from the previous year, but a 46% climb from the previous quarter. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

The Stars Group and FOX Sports Announce Historic U.S. Media and Sports Wagering Partnership

The Stars Group and FOX Sports Announce Historic U.S. Media and Sports Wagering Partnership May 8, 2019 Toronto and Los Angeles, May 8, 2019 – The Stars Group Inc. (Nasdaq: TSG)(TSX: TSGI) and FOX Sports, a unit of Fox Corporation (Nasdaq: FOXA, FOX), today announced plans to launch FOX Bet, the first-of-its kind national media and sports wagering partnership in the United States. The Stars Group and FOX Sports have entered a long-term commercial agreement through which FOX Sports will provide The Stars Group with an exclusive license to use certain FOX Sports trademarks. The Stars Group and FOX Sports expect to launch two products in the Fall of 2019 under the FOX Bet umbrella. One will be a nationwide free-to-play game, awarding cash prizes to players who correctly predict the outcome of sports games. The second product, which will be named FOX Bet, will give customers in states with regulated betting the opportunity to place real money wagers on the outcome of a wide range of sporting events in accordance with the applicable laws and regulations. In addition to the commercial agreement of up to 25 years and associated product launches, Fox Corporation will acquire 14,352,331 newly issued common shares in The Stars Group, representing 4.99% of The Stars Group’s issued and outstanding common shares, at a price of $16.4408 per share, the prevailing market price leading up to the commencement of exclusive negotiations. The Stars Group currently intends to use the aggregate net proceeds of approximately $236 million for general corporate purposes and to prepay outstanding indebtedness on its first lien term loans. -

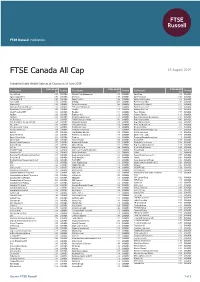

FTSE Publications

2 FTSE Russell Publications 19 August 2019 FTSE Canada All Cap Indicative Index Weight Data as at Closing on 28 June 2019 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Aecon Group 0.05 CANADA Element Fleet Management 0.19 CANADA Onex Corp 0.3 CANADA Agnico Eagle Mines 0.73 CANADA Emera Inc 0.58 CANADA Open Text Corp 0.65 CANADA Air Canada Cl B 0.25 CANADA Empire Co Cl A 0.26 CANADA Osisko Gold Royalties 0.1 CANADA Alacer Gold 0.06 CANADA Enbridge 4.35 CANADA Pan American Silver 0.16 CANADA Alamos Gold 0.14 CANADA Encana Corporation 0.46 CANADA Paramount Res Class A 0.02 CANADA Algonquin Power & Utilities Co 0.36 CANADA Endeavour Mining Corp. 0.07 CANADA Parex Resources Inc 0.14 CANADA Alimentation Couche-Tard B 1.63 CANADA Enerflex 0.07 CANADA Parkland Fuel Corp. 0.28 CANADA Allied Properties REIT 0.24 CANADA Enerplus 0.11 CANADA Pason Systems 0.07 CANADA AltaGas. 0.25 CANADA Enghouse Sys 0.06 CANADA Pembina Pipeline 1.14 CANADA Aphria Inc 0.09 CANADA Ensign Energy Services 0.03 CANADA Peyto Exploration & Development 0.03 CANADA Arc Resources 0.1 CANADA Fairfax Financial Holdings 0.81 CANADA Power Corp Canada 0.46 CANADA Artis Real Estate Investment Trust 0.07 CANADA Finning International 0.18 CANADA Power Financial Corp 0.32 CANADA Atco Class I 0.15 CANADA First Capital Realty 0.16 CANADA PrairieSky Royalty Ltd 0.2 CANADA ATS Automation Tooling 0.07 CANADA First Majestic Silver 0.08 CANADA Precision Drilling 0.03 CANADA Aurora Cannabis Inc 0.38 CANADA First National Financial 0.02 CANADA Premium Brands Holdings Corp 0.12 CANADA B2Gold 0.18 CANADA First Quantum Minerals 0.39 CANADA Pretium Resources 0.1 CANADA Bank of Montreal 2.93 CANADA FirstService Corporation 0.18 CANADA Quebecor Inc.