Page 1 a S 0

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Familymart Branches

Sheet1 Participating FamilyMart Branches BRANCH ADDRESS CONTACT NUMBER G/F 139 CORPORATE CENTER, VALERO ST. 0917-8129710 139 CORPORATE SALCEDO VILLAGE, MAKATI CITY 978-0109 G/F STALL 21 ELJ COMMUNICATIONS 964-8279 ABS - CBN CENTER, QUEZON CITY 0917-5225533 GF AEON PRIME BUILDING, ALABANG- AEON PRIME ZAPOTE ROAD COR. NORTHGATE 0917-8458988 BRIDGEWAY, MUNTINLUPA CITY G/F UNIT 1-4, AIC GRAND DE TOWER, 0917-846-0651 AIC GRANDE TOWER GARNET ROAD, ORTIGAS CENTER, PASIG 507-6348 CITY G/F ALCO BLDG. 391 SEN. GIL PUYAT ALCO BLDG 954-1585 MAKATI CITY G/F ALPHALAND SOUTHGATE MALL EDSA 0917-5827526 ALPHALAND COR. PASONG TAMO ST. MAKATI CITY 959-0832 LG/F UNIT 7 ANONAS LRT CITY CENTER 978-0131 ANONAS LRT AURORA BLVD. & ANONAS ST. PROJECT 3 0917-8057206 QUEZON CITY AVIDA TOWERS NEW MANILA (TOWER# 5), 0917-8466236 AVIDA NEW MANILA B. SERRANO AVE., BRGY. BAGONG LIPUNAN 964-1352 NG CRAME, QUEZON CITY G/F RETAIL SPACE 2-4, AVIDA TOWERS SAN 0917-8940484 AVIDA SAN LORENZO LORENZO, CHINO ROCES AVE., MAKATI CITY 964-1499 959-1275 AYALA MRT 2/F AYALA MRT STATION 3 MAKATI CITY 09178207217 G/F C1 AYALA TOWER ONE & EXCHANGE AYALA TOWER ONE PLAZA AYALA TRIANGLE AYALA AVE. MAKATI 625 - 0446 CITY AYALA TRIANGLE GARDENS AYALA AVE., AYALA TRIANGLE GARDENS 729-7962 MAKATI CITY 11th AVE COR 30th ST., BONIFACIO GLOBAL 0917-5818190 BGC CORP CITY 978-0138 G/F BLDG K, BLUE BAYWALK MACAPAGAL, 0917-8103789 BLUE BAYWALK EDSA EXT. COR. MACAPAGAL AVE. 218-9335 METROPARK, PASAY CITY G/F SPACE #3 BONIFACIO ONE TECHNOLOGY TOWER RIZAL DRIVE COR. -

18/4/2011 Report

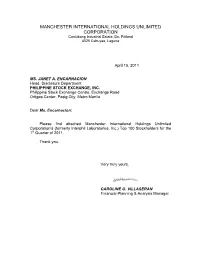

MANCHESTER INTERNATIONAL HOLDINGS UNLIMITED CORPORATION Canlubang Industrial Estate, Bo. Pittland 4025 Cabuyao, Laguna April 15, 2011 MS. JANET A. ENCARNACION Head, Disclosure Department PHILIPPINE STOCK EXCHANGE, INC. Philippine Stock Exchange Centre, Exchange Road Ortigas Center, Pasig City, Metro Manila Dear Ms. Encarnacion: Please find attached Manchester International Holdings Unlimited Corporation’s (formerly Interphil Laboratories, Inc.) Top 100 Stockholders for the 1st Quarter of 2011. Thank you. Very truly yours, CAROLINE O. VILLASERAN Financial Planning & Analysis Manager BPI STOCK TRANSFER OFFICE MANCHESTER INTERNATIONAL HOLDINGS UNLIMITED CORP. TOP 100 STOCKHOLDERS AS OF MARCH 31, 2011 RANK STOCKHOLDER NUMBER STOCKHOLDER NAME NATIONALITY CERTIFICATE CLASS OUTSTANDING SHARES PERCENTAGE TOTAL 1 09002935 INTERPHARMA HOLDINGS & MANAGEMENT CORPORATION FIL A 255,264,483 61.9476% 255,264,483 C/O INTERPHIL LABORATORIES INC KM. 21 SOUTH SUPERHIGHWAY 1702 SUKAT, MUNTINLUPA, M. M. 2 1600000001 PHARMA INDUSTRIES HOLDINGS LIMITED BRT B 128,208,993 31.1138% 128,208,993 C/O ZUELLIG BUILDING, SEN. GIL J. PUYAT AVENUE, MAKATI CITY 3 16015506 PCD NOMINEE CORPORATION (FILIPINO) FIL A 10,913,671 G/F MKSE. BLDG, 6767 AYALA AVE MAKATI CITY B 8,258,342 4.6526% 19,172,013 4 16009811 PAULINO G. PE FIL A 181,250 29 NORTH AVENUE, DILIMAN, QUEZON CITY B 575,000 0.1835% 756,250 5 10002652 KASIGOD V. JAMIAS FIL A 464,517 109 APITONG ST., AYALA ALABANG MUNTINLUPA, METRO MANILA B 106,344 0.1385% 570,861 6 16011629 PCD NOMINEE CORPORATION (NON-FILIPINO) NOF B 393,750 0.0955% 393,750 G/F MKSE BUILDING 6767 AYALA AVENUE MAKATI CITY 7 16010090 PUA YOK BING FIL A 375,000 0.0910% 375,000 509 SEN. -

FTSE Publications

2 FTSE Russell Publications 28 October 2020 FTSE Philippines USD Net Tax Index Indicative Index Weight Data as at Closing on 27 October 2020 Constituent Index weight (%) Country Constituent Index weight (%) Country Constituent Index weight (%) Country Aboitiz Power 1.55 PHILIPPINES JG Summit Holdings 6.55 PHILIPPINES Semirara Mining and Power 0.48 PHILIPPINES Alliance Global 1.11 PHILIPPINES Jollibee Foods 2.48 PHILIPPINES SM Investments 16.27 PHILIPPINES Ayala Corporation 8.63 PHILIPPINES LT Group 1.16 PHILIPPINES SM Prime Hldgs 10.52 PHILIPPINES Ayala Land 9.44 PHILIPPINES Manila Electric 2.7 PHILIPPINES Universal Robina 4.26 PHILIPPINES Bank of The Philippine Islands 4.65 PHILIPPINES Megaworld 1.25 PHILIPPINES BDO Unibank 6.27 PHILIPPINES Metro Pacific Investments 1.97 PHILIPPINES Bloomberry Resorts 0.9 PHILIPPINES Metropolitan Bank & Trust 2.63 PHILIPPINES DMCI Holdings 0.65 PHILIPPINES PLDT 4.32 PHILIPPINES Globe Telecom 2.08 PHILIPPINES Puregold Price Club 1.44 PHILIPPINES GT Capital Holdings 1.51 PHILIPPINES San Miguel 1.28 PHILIPPINES International Container Terminal Service 4.37 PHILIPPINES San Miguel Food and Beverage 1.52 PHILIPPINES Source: FTSE Russell 1 of 2 28 October 2020 Data Explanation Weights Weights data is indicative, as values have been rounded up or down to two decimal points. Where very small values are concerned, which would display as 0.00 using this rounding method, these weights are shown as <0.005. Timing of data Constituents & Weights are generally published in arrears and contain the data as at the most recent quarter-end. However, some spreadsheets are updated on a more frequent basis. -

No. Company Star

Fair Trade Enforcement Bureau-DTI Business Licensing and Accreditation Division LIST OF ACCREDITED SERVICE AND REPAIR SHOPS As of November 30, 2019 No. Star- Expiry Company Classific Address City Contact Person Tel. No. E-mail Category Date ation 1 (FMEI) Fernando Medical Enterprises 1460-1462 E. Rodriguez Sr. Avenue, Quezon City Maria Victoria F. Gutierrez - Managing (02)727 1521; marivicgutierrez@f Medical/Dental 31-Dec-19 Inc. Immculate Concepcion, Quezon City Director (02)727 1532 ernandomedical.co m 2 08 Auto Services 1 Star 4 B. Serrano cor. William Shaw Street, Caloocan City Edson B. Cachuela - Proprietor (02)330 6907 Automotive (Excluding 31-Dec-19 Caloocan City Aircon Servicing) 3 1 Stop Battery Shop, Inc. 1 Star 214 Gen. Luis St., Novaliches, Quezon Quezon City Herminio DC. Castillo - President and (02)9360 2262 419 onestopbattery201 Automotive (Excluding 31-Dec-19 City General Manager 2859 [email protected] Aircon Servicing) 4 1-29 Car Aircon Service Center 1 Star B1 L1 Sheryll Mirra Street, Multinational Parañaque City Ma. Luz M. Reyes - Proprietress (02)821 1202 macuzreyes129@ Automotive (Including 31-Dec-19 Village, Parañaque City gmail.com Aircon Servicing) 5 1st Corinthean's Appliance Services 1 Star 515-B Quintas Street, CAA BF Int'l. Las Piñas City Felvicenso L. Arguelles - Owner (02)463 0229 vinzarguelles@yah Ref and Airconditioning 31-Dec-19 Village, Las Piñas City oo.com (Type A) 6 2539 Cycle Parts Enterprises 1 Star 2539 M-Roxas Street, Sta. Ana, Manila Manila Robert C. Quides - Owner (02)954 4704 iluvurobert@gmail. Automotive 31-Dec-19 com (Motorcycle/Small Engine Servicing) 7 3BMA Refrigeration & Airconditioning 1 Star 2 Don Pepe St., Sto. -

1623400766-2020-Sec17a.Pdf

COVER SHEET 2 0 5 7 3 SEC Registration Number M E T R O P O L I T A N B A N K & T R U S T C O M P A N Y (Company’s Full Name) M e t r o b a n k P l a z a , S e n . G i l P u y a t A v e n u e , U r d a n e t a V i l l a g e , M a k a t i C i t y , M e t r o M a n i l a (Business Address: No. Street City/Town/Province) RENATO K. DE BORJA, JR. 8898-8805 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A 0 4 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) NONE (Secondary License Type, If Applicable) Corporation Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 2,999 as of 12-31-2020 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. 2 SEC Number 20573 File Number______ METROPOLITAN BANK & TRUST COMPANY (Company’s Full Name) Metrobank Plaza, Sen. Gil Puyat Avenue, Urdaneta Village, Makati City, Metro Manila (Company’s Address) 8898-8805 (Telephone Number) December 31 (Fiscal year ending) FORM 17-A (ANNUAL REPORT) (Form Type) (Amendment Designation, if applicable) December 31, 2020 (Period Ended Date) None (Secondary License Type and File Number) 3 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. -

Top 100 Stockholders - Philippine H2O Ventures Corp

Top 100 Stockholders - Philippine H2O Ventures Corp. Count Stockholder # Stockholder Name Address Nationality TIN Number Of Shares Percentage 1 PCD Fil PCD Filipino N/A PH N/A 231,441,320.00 95.15 % 2 PCD Non-Fil PCD Non-Filipino N/A OA N-A 11,676,801.00 4.80 % 3 0000225748 YU KOK SEE 27 TIRAD PASS QUEZON CITY PH 106,272.00 0.04 % 4 0000225735 ASTURIAS, MARCIAL RONALD T. V.V. SOLIVEN COR. FELIX AVE. CAINTA RIZAL PH 7,200.00 0.00 % 5 0000225740 PASCUA, ROGELIO N. 29 DOLLAR MERALCO VILL. TAYTAY RIZAL PH 3,024.00 0.00 % 6 0000227991 MIGUEL DE CASTRO MARANA OR BITUIN DE CASTRO MARANA C/O AVON COSMETICS INC. ZAMBOANGA BRANCH CANELAR STREET,ZAMBOANGA CITY PH 241-338-761 3,000.00 0.00 % 7 0000225738 MORELOS, LILIAN GUISON 946 MA. CRISTINA SAMPALOC MANILA PH 2,160.00 0.00 % 8 1800300492 ERIC O. RECTO 5TH FLOOR PBCOM TOWER 6795, AYALA AVENUE, MAKATI CITY, METRO MANILA PH 108-730-891-000 1,000.00 0.00 % 9 0000225739 PANG, VICENTE LIM 1022 CORTADA STREET ERMITA, MANILA PH 432.00 0.00 % 10 0000240022 LIMGENCO, DONDI RON R. 886B MARQUITOS ST., SAMPALOC MANILA 1008 PHILIPPINES PH 302-242-112 111.00 0.00 % 11 1800300482 SHAREHOLDERS' ASSOCIATION OF THE PHILIPPINES, INC. UNIT 1003, 10TH FLOOR CITYLAND PASONG TAMO TOWER, 2210 DON CHINO ROCES AVE., MAPH 007-553-100 100.00 0.00 % 12 0000226005 AU, OWEN NATHANIEL S. AU ITF: LI MARCUS B9 L5 MT. TABOR ST., MT. VIEW SUBD., MANDALAGAN, BACOLOD CITY PH 197-550-637 75.00 0.00 % 13 0000225720 QUINTANA, DEXTER E. -

Of 31 STOCKHOLDERS NAME NATIONALITY OUTSTANDING SHARES UNION BANK of the PHILIS

National Reinsurance Corporation of the Philippines List of Stockholders as of Record Date, June 23, 2020 STOCKHOLDERS NAME NATIONALITY OUTSTANDING SHARES ALEGAR CORPORATION FILIPINO 32,600 ALPHA INSURANCE & SURETY CO., INC. FILIPINO 1,578,900 AP MADRIGAL STEAMSHIP CO. INC. FILIPINO 3,300 ARAVAL, INC FILIPINO 77,100 ASIA UNITED INSURANCE, INC FILIPINO 1,252,300 BANCOM DEVELOPMENT CORP. FILIPINO 8,300 BENEFICIAL LIFE INSURANCE COMPANY INC. FILIPINO 3,193,500 B.F. GENERAL INSURANCE CO., INC. FILIPINO 36,900 BF LIFE INSURANCE CORP. FILIPINO 397,300 BPI/MS INSURANCE CORP. FILIPINO 3,347,500 CENTENNIAL GUARANTEE ASSURANCE CORP. FILIPINO 14,500 CONSOLIDATED INSURANCE CO., INC. FILIPINO 144,600 COOPERATIVE INSURANCE SYSTEM OF THE PHILS. FILIPINO 72,900 COUNTRY BANKERS INS. CORP. FILIPINO 2,220,300 COUNTRY BANKERS LIFE INSURANCE CORP. FILIPINO 30,000 EASTERN ASSURANCE & SURETY CORPORATION FILIPINO 1,872,400 FEDERAL PHOENIX ASSURANCE COMPANY INC. FILIPINO 3,786,300 FGU INSURANCE CORPORATION FILIPINO 36,126,000 FIDELITY INSURANCE COMPANY INC. FILIPINO 818,800 FIRST INTEGRATED BONDING & INS. CO INC. FILIPINO 275,300 GREAT DOMESTIC INS. CO. OF THE PHILS. FILIPINO 544,700 INSURANCE COMPANY OF NORTH AMERICA FILIPINO 705,600 INSURANCE OF THE PHIL. ISLANDS CO., INC. FILIPINO 59,100 INVESTOR'S ASSURANCE CORP. FILIPINO 99,000 LUZON INSURANCE & SURETY CO., INC. FILIPINO 32,300 MAA GENERAL ASSURANCE PHILS., INC. FILIPINO 271,800 MABASA & COMPANY, INC. FILIPINO 36,500 MALAYAN INSURANCE CO., INC. FILIPINO 21,600 MANILA INSURANCE COMPANY INC. FILIPINO 1,148,400 MANILA SURETY & FIDELITY CO., INC. FILIPINO 3,168,400 MONARCH INSURANCE CO., INC. FILIPINO 1,674,000 THE NEW INDIA ASSURANCE COMPANY, LIMITED FILIPINO 4,168,300 ORIENTAL ASSURANCE CORPORATION FILIPINO 3,560,800 PACIFIC UNION INSURANCE CO. -

ROBINSONS BANK CORPORATION List of Branches As of August 2020

ROBINSONS BANK CORPORATION List of Branches as of August 2020 NO. BRANCH NAME ADDRESS 1 ACACIA LANE - SHAW BLVD. G/F Padilla Bldg. 333 Shaw Boulevard, Brgy. Bagong Silang, Mandaluyong City 2 ADRIACTICO [PADRE RADA] G/F Robinsons Place Manila, Adriatico Street, Ermita, Manila City G/F Unit 4, El Molito Commercial Complex, Madrigal Avenue cor Alabang-Zapote Road, Alabang, 3 ALABANG Muntinlupa City 4 ANGELES Level 1 Robinsons Place Angeles, McArthur Highway, Balibago, Angeles City, Pampanga Unit 169-A, Robinsons Place Antipolo, Sumulong Highway/Circumference Avenue, Dela Paz, 5 ANTIPOLO Antipolo City 6 ANTIQUE Level 1-116, 117 & 118 Robinsons Place Antique, Brgy. Maybato, San Jose de Buenavista, Antique Unit 7A Commercial Space, The Beacon Makati, A. Arnaiz Avenue corner Chino Roces Ave, Makati 7 ARNAIZ AVE City G/F Don Norberto & Doña Salustiana Ty Building, #403 Asuncion Street corner San Nicolas Street, 8 ASUNCION BINONDO Binondo, Manila 9 AYALA 6780 G/F JAKA 1 Building, Ayala Avenue, Makati City 10 BACOLOD CAPITOL R. PERFORMANCE Building A 62-64 Narra Avenue, Capitol Shopping Center, Bacolod City Level 1 C2002, The Central Citywalk, Robinsons Place Bacolod, Lacson Street, Mandalagan, 11 BACOLOD CITY Bacolod City, Negros Occidental 12 BACOOR Units 1 & 2, Apollo Mart Building, #369 Gen. Aguinaldo Highway, Talaba 4, Bacoor, Cavite 13 BACOOR MOLINO BLVD. G/F Main Square Bacoor, Molino Boulevard, Bacoor City, Cavite 14 BAGUIO G/F, ECCO/EDGARDOMCO REALTY CORP. Bldg., #43 Assumption Road, Baguio City 15 BAIS Corner Quezon and Burgos Streets, Bais City, Negros Oriental 16 BALAGTAS G/F 103-1 Balagtas Town Center, McArthur Highway, Borol 1st, Balagtas, Bulacan 17 BALANGA G/F, R & R Building, Don Manuel Banzon Avenue, Doña Francisca, Balanga City, Bataan 18 BALAYAN G/F Stalls Numbers 2, 3 & 4 Balayan Public Market, Plaza Mabini Street, Balayan Batangas 19 BANAWE (FORMERLY PASAY) Store No. -

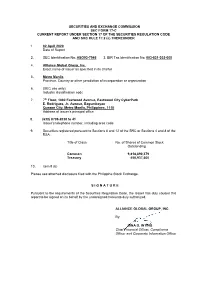

SECURITIES and EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 of the SECURITIES REGULATION CODE and SRC RULE 17.2 (C) THEREUNDER

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2 (c) THEREUNDER 1. 02 April 2020 Date of Report 2. SEC Identification No: ASO93-7946 3. BIR Tax Identification No: 003-831-302-000 4. Alliance Global Group, Inc. Exact name of issuer as specified in its charter 5. Metro Manila Province, Country or other jurisdiction of incorporation or organization 6. (SEC use only) Industry classification code 7. 7th Floor, 1880 Eastwood Avenue, Eastwood City CyberPark E. Rodriguez, Jr. Avenue, Bagumbayan Quezon City, Metro Manila, Philippines, 1110 Address of issuer’s principal office 8. (632) 8709-2038 to 41 Issuer’s telephone number, including area code 9. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA: Title of Class No. of Shares of Common Stock Outstanding Common 9,818,890,379 Treasury 450,937,600 10. Item 9 (b) Please see attached disclosure filed with the Philippine Stock Exchange. S I G N A T U R E Pursuant to the requirements of the Securities Regulation Code, the Issuer has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized. ALLIANCE GLOBAL GROUP, INC. By: DINA D. INTING Chief Financial Officer, Compliance Officer and Corporate Information Officer 4/3/2020 Request for extension to file SEC Form 17-A CR01662-2020 The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. -

PLANNING and DESIGNING for CLIMATE ADAPTIVE and RESILIENT TRANSPORT: EXPERIENCE from PHILIPPINES Engineer ERNESTO V

The Republic of the Philippines DEPARTMENT OF PUBLIC WORKS AND HIGHWAYS PLANNING AND DESIGNING FOR CLIMATE ADAPTIVE AND RESILIENT TRANSPORT: EXPERIENCE FROM PHILIPPINES Engineer ERNESTO V. ALDAY, JR Project Preparation Division, Planning Service Regional Seminar on Safe, Climate Adaptive and Disaster Resilient Transport for Sustainable Development Kathmandu, Nepal 17 November 2015 1 10 Year Disaster Data: 21,381,374 Affected Persons (6,389) (Casualties) 12,250,050 11,253,211 (1,140) (1,165) 9,884,577 6,966,136 (1,557) (1,232) 13,106,133 (294) 7,009,725 8,006,126 (673) (1,386) 2,998,885 2,596,587 1,019,646 (124) (136) (54) Total Cost of Damages Cost Total US $ 1 - P 44 1 Republic of the Philippines Department of Public Works and Highways Effects of Typhoon Ketsana (Ondoy) – September 2009 Total Cost of Damages: P11.0 B ($ 250 M) . Tropical Rainfall Measuring Mission (TRMM) / NASA – Multi Satellite Precipitation Analysis (MPA) showed Typhoon ‘Ketsana’ poured 575 mm of rainfall (6hr Rainfall) . Monthly average (November) rainfall record in Manila was poured over in 1 day. Affected Families 993,227 Total Displaced Families 15,798 Fatalities 464 Injured 529 US $ 1 - P 44 Missing 37 Republic of the Philippines Department of Public Works and Highways Effects of Typhoon Washi (Sendong) – December 2011 Affected Families 131,6 18 Total Cost of Damages: P2.07 B ($ 47 M) Fatalities 1,268 Injured 6,071 Missing 181 US $ 1 - P 44 Republic of the Philippines Department of Public Works and Highways Effects of Magnitude 7.2 Sagbayan, Bohol Earthquake – October 2013 Total Cost of Damages: P2.26 B* ($ 51 M) Affected Families 671,103 Total Displaced 72,521 Families Fatalities 223 Missing 8 Injured 976 Source: NDRRMC Site Report No. -

The Case of the Pasig City Bus Service

Assessing the Implementation Arrangements for a City Bus Transport System through a Hybrid PPP Model: The Case of the Pasig City Bus Service Annelie LONTOCa, German AVENGOZAb, Nelson DOROYc, Giel Sabrine CRUZd, Alpher DE VERAe , Paolo MANUELf , Candice RAMOS g, ClairedeLune VILLANUEVA h a,b,c,d,e,f,g,h School of Urban and Regional Planning, University of the Philippines a E-mail: [email protected] b E-mail: [email protected] c E-mail: [email protected] d E-mail: [email protected] e E-mail: [email protected] f E-mail: [email protected] g E-mail: [email protected] h E-mail: [email protected] Abstract: The Ortigas Center is an important urban center in Metro Manila where its roads are often congested. Pasig City implemented a free bus service within Ortigas to address the need for public transportation. This Study assessed the implementation arrangements for a free bus service in Ortigas. The Study finds that there is a valid demand for the bus service as Ortigas is a key trip generator. However, the present free bus service is not financially viable. The Study shows that a fleet size fitted for demand will be more efficient than the current service. The Study finds that a Hybrid PPP Model for the bus service is more viable than a Pure PPP Model and the current arrangements. Both PPP Models will require the same institutional requirements such as a PPP Ordinance, the setting-up of a PPP Committee, and processes consistent with the awarding of local government contracts. Keywords: Local Public Transport Route Planning, Viability Assessment, PPP Bus Service 1. -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy.