Screen Density – Key to Unlocking the Hidden Box Office Potential December 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Bollywood Talkies

INDIA Bollywood Talkies ©Vanessa Vettorello Rahul Bose, actor, at the premiere of “Margarita with a straw” at the Inox multiplex in Nariman Point (Mumbay) The historic single screen cinemas are recently experiencing a deep identity and economic crisis, leading them to a fast disappearance. Simultaneously, multiple modern screen centers are at the peak of their development and success. As well as the entire Indian film industry. The videos parlour instead - big rooms without any comfort and equipped only with a projector - were born in provincial areas where the old cinemas were closing down, trying to keep alive the traditional movie theaters market in a cheaper way. But today, due to growing piracy, the spread of new technologies (smartphones, tablets, laptops) - and last but not least because of their intrinsic illegality (very few video rooms are fully licensed) – they are experiencing themselves also a major crisis. Thus in a few years the world of cinemas in the country could change radically. Even in India then, in rural areas as in large cities, small theaters are being replaced constantly by more advanced but anonymous video centers. Today these three types of theaters - video parlour, single screen halls and modern multiplex - are still attended by different kind of people in a very exclusive way: each one in fact has its own typical goer that identifies it under a social and economic category. Today they represent a perfect picture of India social complexity to be studied and considered under a light-blue Bollywood twilight. Waiters of the Inox multiplex located inside the Amanora Town Centre mall (Hadapsar - Pune) Matinee show at the New Roshan (Grant Road - Mumbai) Maratha Mandir cinema entrance. -

ENTERTAINMENT November 2010 ENTERTAINMENT November 2010

ENTERTAINMENT November 2010 ENTERTAINMENT November 2010 Contents Advantage India Market overview Industry Infrastructure Investments Policy and regulatory framework Opportunities Industry associations 2 ADVANTAGE INDIA Entertainment November 2010 Advantage India - capital Increasing investments by the private sector and foreign media and entertainment (M&E) majors have enhanced India‘s entertainment infrastructure such as new multiplexes and digitization of TV distribution and theatre infrastructure. • Digitisation and technological advancements Improving across the value chain are improving the quality • Producing more than 1,000 films entertainment of content and reach, and also leading to new annually, India is the largest infrastructure business models. For example rural DTH producer of films in the world. penetration is three times higher than in urban Digital High • There are more than 500 TV areas, with digital TV penetration rate of 34% in revolution production channels in the country, requiring rural areas as compared to 12% in urban areas volumes 30 hours of fresh programming per week. • A liberalised foreign investment regime Advantage and other regulatory initiatives are resulting in a conducive business India environment for Indian M&E. Large and under • FDI upto 100 per cent is allowed in film Liberal penetrated • In 2008, there were as many as 3.3 billion and advertising, TV broadcasting (except government consumer theatre admissions in India. news) and 26 per cent in newspaper policies base • With the TV segment reaching as many as publishing. Favourable 134 million households in the country, • Migration from fixed to revenue sharing demographics India is one of the largest TV markets in license fee regime in radio segment and the world. -

TDI Agra Jabalpur Samdareeya Era Cinema Agra SARV Multip

SubRegion Name Cinema Name SubRegion Name Cinema Name Agra BIG Cinemas: TDI Agra Jabalpur Samdareeya Era Cinema Agra SARV Multiplex: Agra Jabalpur Movie Magic: South Avenue Mall, Jabalpur Agra Pacific Cinema: Agra Jaipur Big Cinemas: Cinestar Ahmedabad BIG Cinemas: Himalaya Jaipur BIG Cinemas: Galaxy Ahmedabad CineMAX: Dev Arc Mall Jaipur Fun Cinemas: Jhotwara Ahmedabad Cinemax: Red Carpet Jaipur Fun Cinemas: Vidyadhar Nagar Ahmedabad CineMAX: Shiv, Ashram Road Jaipur INOX: City Plaza Mall, Bani Park Ahmedabad Fun Cinemas: Ahmedabad Jaipur INOX: Crystal Palm,C Scheme Ahmedabad PVR Acropolis, SG Rd Jaipur INOX: Entertainment Paradise Ahmedabad Rupan Cinema : Relief Road Jaipur INOX: Pink Square, Govind Mark Ahmedabad 5D Bonzai Adventure: Ahmedabad Jaipur INOX: Vaibhav, Amarapali Circle Ahmedabad Cine Pride: Krishna Nagar Jaipur Laxmi Mandir Ahmedabad Devi Multiplex: Naroda Jaipur Suryamandir Ajmer Glitz Cinemas: Ajmer Jalandhar BIG Cinemas: Viva Collage, Jalandhar Akola BIG Cinemas: Radhakrishna, Akola Jalandhar PVR MBD Mall Akola Vasant Talkies Jammu Movietime Aligarh BIG Cinemas Vadra Jamnagar BIG Cinemas Mehul Allahabad BIG Cinemas: Sangeet, Allahabad Jamnagar Review Cinemas: Jamnagar Allahabad Payal and Jhankar BIG Cinemas Jodhpur Bioscope: Jodhpur Allahabad PVR Vinayak city, Jodhpur Glitz Cinemas : Blue City Malll Ambala Fun Cinemas: Galaxy Mall Jodhpur Satyam Cineplexes: Ansal Royal Plaza Amravati Prabhat Theatre Kalyan Cinemax: Kalyan Amritsar BIG Cinemas: Suraj Chand Tara Kalyan Fame Metro Mall Junction: Kalyan (E) Amritsar Cinepolis -

Tushar Dhingra

Consultant Biography TUSHAR DHINGRA Tushar Dhingra serves as an executive vice president for DHR International, based in the New Delhi COMPANY FACTS office. Mr. Dhingra brings nearly 20 years of experience in the retail, media, hospitality and entertainment industries to DHR and has strong background in corporate strategy, real estate, LEADERSHIP operations, branding and identity, and people management. In addition to his time with David Hoffmann internationally acclaimed firms, Mr. Dhingra also has experience working with family owned Chief Executive Officer groups as well as establishing start-ups in India and across the region in the media, real estate, technology and retail business. CHRISTINE GREYBE Managing Director, Asia-Pacific Prior to joining DHR International, Mr. Dhingra had been a successful business leader for nearly seven years with India’s largest cinema group, BIG Cinemas. As their COO, he oversaw the P&L SERVICES responsibility of nearly 40 locations across India and Nepal. During his tenure there, his focus Global retained executive-level covered business functions such as real estate, retail, branding and marketing, and under his and Board Director searches operational leadership, the firm increased 10 times in size. Mr. Dhingra is also well recognized by the industry for his contributions; some of the international awards and acclaims he has received LOCATIONSTushar Dhingra include “Exhibitor of the Year CineAsia” and “Best Retailer in Entertainment” for two successive 49Executive offices Viceproviding President global search years. Prior to joining BIG Cinemas, Mr. Dhingra served as the Vice President - Marketing and Sales services:DHR International a domestic presence for PVR Cinemas, India’s largest multiplex chain. -

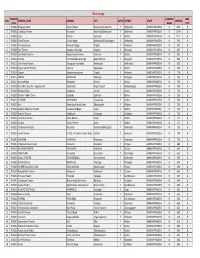

Real Image THEATRE COMPANY WEB S.No

Real Image THEATRE COMPANY WEB S.No. THEATRE_NAME ADDRESS CITY ACTIVE DISTRICT STATE SEATING CODE NAME CODE 1 TH0001 Bhujanga 70mm Shapure Nagar Hyderabad (Jedimetla) Y Hyderabad ANDHRA PRADESH RI 1311 0 2 TH0002 Laxmikala Theatre Moosapet Hyderabad(Moosapet) Y Hyderabad ANDHRA PRADESH RI 1189 0 3 TH0003 Sarat Krishna Gudivada Y Krishna ANDHRA PRADESH RI 1112 0 4 TH0006 Geeta Theatre Chanda Nagar Hyderabad (Chandanagar) Y Hyderabad ANDHRA PRADESH RI 962 0 5 TH0007 Srinivasa Deluxe Mahendra Nagar Ongole Y Prakasam ANDHRA PRADESH RI 900 0 6 TH0009 Devi Theatre Janagoan, Warangal Jangaon Y Warangal ANDHRA PRADESH RI 837 0 7 TH0010 Sree Balaji Theatres Satyanarayana Puram Gudivada Y Krishna ANDHRA PRADESH RI 833 0 8 TH0011 Ashoka Hanumakonda, Warangal Hanumakonda Y Warangal ANDHRA PRADESH RI 830 0 9 TH0012 Sree Prema Theatre Tukkuguda Hyderabad Hyderabad Y Hyderabad ANDHRA PRADESH RI 800 0 10 TH0013 Vijaya Lakshmi Theatre Kaanuru Vijayawada Y Krishna ANDHRA PRADESH RI 786 0 11 TH0014 Satyam Satyanarayanapuram Ongole Y Prakasam ANDHRA PRADESH RI 779 0 12 TH0015 NATRAJ WARANGAL Warangal Y Warangal ANDHRA PRADESH RI 766 0 13 TH0017 Krishna Mahal Kothapeta Guntur Y Guntur ANDHRA PRADESH RI 750 0 14 TH0018 Ravi 70mm A/c DTS - Nagarkarnool Sripur Road Nagarkarnool Y Mehboobnagar ANDHRA PRADESH RI 750 0 15 TH0019 Bhaskar Palace Kothapeta Guntur Y Guntur ANDHRA PRADESH RI 740 0 16 TH0020 Bhaskar Talkies 70mm Gudivada Gudivada Y Krishna ANDHRA PRADESH RI 738 0 17 TH0021 ALANKAR VIJAYAWADA Vijayawada Y Krishna ANDHRA PRADESH RI 738 0 18 TH0022 Ravi -

Annual Report of 2015

BOARD OF DIRECTORS Mr. Subhash Ghai Executive Chairman DIN: 00019803 Mr. Rahul Puri Managing Director DIN: 01925045 Mr. Parvez A. Farooqui Executive Director DIN: 00019853 Mr. Kewal Handa Independent Director DIN: 00056826 Mrs. Paulomi Dhawan Independent Director DIN: 01574580 Mr. Manmohan Shetty Independent Director DIN: 00013961 Chief Financial Offi cer Mr. Prabuddha Dasgupta Company Secretary & Compliance Offi cer Mr. Ravi B. Poplai Statutory Auditors M/s B S R & Co. LLP Internal Auditors M/s Garg Devendra & Associates Secretarial Auditors M/s. K. C. Nevatia & Associates Bankers Kotak Mahindra Bank Limited HDFC Bank Limited CONTENTS Registrar & Transfer Agents Link Intime India Private Limited Performance at a glance 2 C-13, Pannalal Silk Mills Compound Chairman’s Statement 3 L.B.S. Marg, Bhandup (W) Management Discussion & Analysis 5 Mumbai – 400 078 Telephone No. - (022) 2596 3838 Notice 8 Route Map 17 Registered Offi ce Mukta House, Board’s Report 18 Behind Whistling Woods Institute, Corporate Governance Report 43 Filmcity Complex, Goregaon (East), Mumbai- 400065 FINANCIALS Telephone No. - (022) 33649400 Mukta Arts Limited 57 Fax No. - (022) 33649401 Consolidated Financials of Mukta Arts Limited 93 Website: www.muktaarts.com & it’s Subsidiaries CIN : L92110MH1982PLC028180 1 Note: Shareholders are requested to avail services of the Company’s bus outside Goregaon (East) Station near Bus Depot up to 3.30 p.m. to reach the AGM Venue. PERFORMANCE Performance at a glance Rupees in millions Year ended Year ended Year ended Year ended Year -

Carnival Cinemas Is the Largest Multiplex Chain Spread Across Cities with a Presence in 90 Cities with Over 346 Screens Including Small Towns

C arnival Cinemas CARNIVAL MEDIA Carnival Media was founded in 2011 and is a Mumbai-based company and a part of diversified corporate group. It focuses on creating, producing, and developing media properties in live events and also manages shows and concerts in India and abroad. The company works in multiple areas that include television shows, Bollywood movies and music, corporate seminars and training, education workshops, and various promotional and entertainment events in India and overseas. In India, Carnival Cinemas is the largest multiplex chain spread across cities with a presence in 90 cities with over 346 screens including small towns. HISTORY In 2014 Carnival Cinemas acquired HDIL’s Broadway Cinema chain, which had screens across Mumbai, Delhi and Indore. They also acquired Anil Ambani’s Big Cinemas, which made them one of the top three exhibition companies in India. The following year the company purchased the commercial real estate projects Larsen and Toubro Ltd for Rs.1,785 crore. Bhasi and Carnival’s next major step was the acquisition of Anil Ambani owned Big Cinemas with 250 screens across the country for around Rs 700 crore. During this time Bhasi also took over Mukesh Ambani’s Network 18 Media and Investments Ltd owned Glitz Cinema He then went on to add many other verticals to the Carnival Group, which includes hospitality, media, real estate, IT park, event management & food courts along with multiplexes. “Carnival Cinemas” is the largest multiplex chain spread across cities in India. Having its presence in 85 cities with 121 operational locations, it pledges to accord its patrons an absolute movie viewing experience. -

Bhawani Complex

https://www.propertywala.com/bhawani-complex-nagpur Bhawani Complex - Wardhaman Nagar, Nagpur 2/3 Bhk Flats, Bhawani Complex, East Nagpur This apartment is set at a prime and well connected location featuring maximum internal usage area with excellent natural light & air ventilation. Set close to key destinations like schools, hospitals, market, etc. Project ID : J290532111 Builder: Devsar Projects Properties: Apartments / Flats, Multipurpose Buildings Location: Bhawani Complex,Beside New Swaminarayan Mandir & School, Near to Nandanwan, Wardhaman Nagar, Nagpur - 440009 (Maharashtra) Completion Date: Sep, 2013 Status: Started Description A major dream in anybody's life is a home of his own, a place that reflects him, and an area that acknowledges his achievements in his life. A nesting place that makes him secure and encourage him to dream more...and bigger. Your home is heaven for you and it reflects your sense of pride & dignity.As a celebration of this space, we bring you an affordable quality living space called 'Bhawani Complex' especially crafted for you. Our excellent team, quality development and clear transactions will bring your much awaited dream of buying a home come true. Area : 2BHK / 3BHK Specifications Structure & Plasters: RCC Frame structure of superior quality as per structural designer Outer walls of 6” thick & inner wall 4” thick RCC Chajja for storage in kitchen Bathroom, toilet & plumbing: Concealed plumbing with standard quality & beautiful CP fittings One wash basin in each bathroom Provision for hot and cold water -

The Growth of Inox Leisure

International Journal of Grid and Distributed Computing Vol. 13, No. 1s, (2020), pp. 298-308 Indian Multiplex Market: The Growth of Inox Leisure. Mr. Monojit Dutta1, Ms. Sayani Sen2 1Assistant Professor, Department of Commerce and Management, St Xavier’s University Kolkata, India Email id: [email protected] 2Independent Researcher, Kolkata, India, Email id: [email protected] Abstract: Cinemas have always been an integral part of people’s life. As our society has progressed so has the cinema industry. Similarly, the medium of watching movies has also change with the introduction of new technologies. During the 70s and the 80s, there were mainly single screen movie theatres where people had to stand in long queue to buy tickets, whereas, now there are movie multiplexes, where it is no longer necessary to stand in queue to get a ticket, it can be done easily from the comforts of home through online tickets booking apps. In this paper, we have discussed about the different multiplexes in the Indian market, mainly emphasizing on the two main players of this industry i.e. PVR Ltd and INOX Leisure Limited. The paper mainly aims at showing how INOX inspite of not being in the market for as long as PVR is still giving PVR a tough competition on various aspects. It was rightly found that PVR Ltd holds the maximum share in the market but the growth of Inox Leisure Ltd is impeccable and in certain area; Inox outperforms PVR in terms of return on share, ticket prices and revenue. Keywords: Cinema, Inox Leisure, Multiplex, PVR Ltd. -

Address 95 Rashbihari Road Kolkata-700029 RDB

Address 95 Rashbihari Road kolkata-700029 57, Rashbihari Avenue Kolkata-700026 3rd Floor, Lake Mall, Inside Big Baazar, RashBehari Avenue, Kalighat, Kolkata-700029 Jawaharlal Nehru Rd, Dharmatala, Taltala, Kolkata-700087 RDB Boulevard, K-1, big cinemas saltlake, Plot- EP & GP Block, Sector V, Kolkata-700091 Sector v (Block EPGP SDF Buliding ground floor kolkata 700091 city Center Saltlake, D.C block sec-1 saltlake, kolkata-700064 Ecospace Business Park, Block 4B,, Premises No. IIF/11,, Kolkata, Newtown Kolkata-700156 Near Spencer\'s, Upohar, Near Garia Metro Station, New Garia, Garia, Kolkata-700094 6/A Kinaran Sankar Road Road Kolkata-700001 138/2 next to citi mart, Bidhan Sarani, Hati Bagan, Kolkata-700004 244, Chittranjan Avenue, Kolkata-700006 Forum Rangoli Mall Food Court, Belur, Howrah-711202 Action Area IID City Centre 2, Rajarhat Ground Floor, New Town, Nowapara, po- Gopalpur, Kolkata-700157 Inside 6 No Gate, Eco Park New Town, Major Arterial Road(South-East), Action Area II, Kolkata, West Bengal 700156 355, Diamond Harbour Road, Near Behala Police Station, Behala, Kolkata-700034 Behala-492 Diamond harber Road (near Tram Depot) Kolkata-700034 76 Raja S.C. Mullick Road, Near KPC Medical College & Hospital, Jadavpur, Kolkata-700032 217 Near hanuman mandir lake Town Block B Kolkata-700089 965 Cal Jessore Road, Dumdum Kolkata-700055 Near Sitala Mandir,P/a 32 ,B BOSE Pukur road shop No-8 kolkata-700042 Acropolis Mall, 1858, Purba Abason, 1582/1, Rajdanga Main Rd, Sector B, East Kolkata-700107 10, wood Street kolkata-700016 (Near Ballygunge Phari) 53/5A HAZRA ROAD 1, Ashutosh Chowdary Ave, Sector 1 Kolkata-700019 Golpark, 19 Gariyahat Road, kolkata-700020 1/1 Ashutosh Chowdhury avenew kolkata 700019 1 Achariya jagadish ch Bose Rd, Kolkata-700024 34/2 N.S.C. -

Back in the Spotlight

INFORMATION, COMMUNICATIONS & ENTERTAINMENT Back in the Spotlight FICCI-KPMG Indian Media & Entertainment Industry Report KPMG IN INDIA Back in the Spotlight FICCI-KPMG Indian Media & Entertainment Industry Report © 2010 KPMG, an Indian Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. FOREWORD Welcome to the 2010 annual edition of the Indian Media and The improved market sentiment in 2010 has set the tone for a Entertainment (M&E) industry report. FICCI takes this opportunity to promising year ahead. The power to convert this sentiment into a thank KPMG, our Knowledge Partner, for having devoted precious reality will rest with the industry players and their ability to attract time and resources to prepare this report at our behest. greater media consumption. Amidst the uncertain economic environment that was prevalent last FICCI acknowledges the valuable inputs provided by the Media & year, the Indian M&E industry has weathered the storm and is Entertainment industry players who have graciously devoted time to showing signs of accelerating its growth. share their views in helping KPMG put this report together. The industry performance in 2009 was a consequence of not only the slowdown, but also several internal factors that lowered the pace of growth for the otherwise flourishing media and entertainment business in India. The multiplex strike, lack of quality content, delay in auctions for phase 3 FM radio and 3G mobile telecom licenses were some of the unexpected events that further impeded the development of this industry. -

Globalizing Pakistani Identity Across the Border: the Politics of Crossover Stardom in the Hindi Film Industry

DePaul University Via Sapientiae College of Communication Master of Arts Theses College of Communication Winter 3-19-2018 Globalizing Pakistani Identity Across The Border: The Politics of Crossover Stardom in the Hindi Film Industry Dina Khdair DePaul University, [email protected] Follow this and additional works at: https://via.library.depaul.edu/cmnt Part of the Communication Commons Recommended Citation Khdair, Dina, "Globalizing Pakistani Identity Across The Border: The Politics of Crossover Stardom in the Hindi Film Industry" (2018). College of Communication Master of Arts Theses. 31. https://via.library.depaul.edu/cmnt/31 This Thesis is brought to you for free and open access by the College of Communication at Via Sapientiae. It has been accepted for inclusion in College of Communication Master of Arts Theses by an authorized administrator of Via Sapientiae. For more information, please contact [email protected]. GLOBALIZING PAKISTANI IDENTITY ACROSS THE BORDER: THE POLITICS OF CROSSOVER STARDOM IN THE HINDI FILM INDUSTRY INTRODUCTION In 2010, Pakistani musician and actor Ali Zafar noted how “films and music are one of the greatest tools of bringing in peace and harmony between India and Pakistan. As both countries share a common passion – films and music can bridge the difference between the two.”1 In a more recent interview from May 2016, Zafar reflects on the unprecedented success of his career in India, celebrating his work in cinema as groundbreaking and forecasting a bright future for Indo-Pak collaborations in entertainment and culture.2 His optimism is signaled by a wish to reach an even larger global fan base, as he mentions his dream of working in Hollywood and joining other Indian émigré stars like Priyanka Chopra.