96-369 May 2015 Fiscal Notes

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2021-22 Schedule (.Pdf)

KANSAS STATE MEN’S BASKETBALL 2021-22 SCHEDULE DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Wednesday Nov. 10 Florida A&M [8-12] Manhattan [Bramlage Coliseum] — / — — K-State leads 4-0 Wednesday Nov. 17 Omaha [5-20] Manhattan [Bramlage Coliseum] — / — W, 60-58 K-State leads 3-0 HALL OF FAME CLASSIC The field includes Arkansas, Cincinnati, Illinois and K-State DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Monday Nov. 22 vs. TBD [—] Kansas City, Mo. [T-Mobile Center] — / — — — Tuesday Nov. 23 vs. TBD [—] Kansas City, Mo. [T-Mobile Center] — / — — — DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Sunday Nov. 28 North Dakota [9-17] Manhattan [Bramlage Coliseum] — / — — K-State leads 2-0 Wednesday Dec. 1 Albany [7-9] Manhattan [Bramlage Coliseum] — / — — First meeting Sunday Dec. 5 vs. Wichita State [16-6] Wichita, Kan. [INTRUST Bank Arena] — / — — K-State leads 20-11 BIG EAST / BIG 12 BATTLE DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Wednesday Dec. 8 Marquette [13-14] Manhattan [Bramlage Coliseum] — / — — K-State leads 7-5 DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Sunday Dec. 12 Green Bay [8-17] Manhattan [Bramlage Coliseum] — / — — K-State leads 2-1 DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Sunday Dec. 19 @Nebraska [7-20] Lincoln, Neb. [Pinnacle Bank Arena] — / — — K-State leads 126-93 DAY DATE OPPONENT [2020-21 RECORD] LOCATION TIME / TV 2020-21 RESULT SERIES Tuesday Dec. -

Texas Tech Red Raiders

TEXAS TECH RED RAIDERS MAC MCCLUNG TERRENCE SHANNON, JR. JAMARIUS BURTON CLARENCE NADOLNY 0 6-2 • Junior • Guard 1 6-6 • Sophomore • Guard 2 6-4 • Junior • Guard 3 6-3 • Sophomore • Guard Gate City, Virginia Chicago, Illinois Charlotte, North Carolina Montreuil, France MICAH PEAVY TYREEK SMITH KYLER EDWARDS MARCUS SANTOS-SILVA 5 6-7 • Freshman • Guard 10 6-8 • R-Freshman • Forward 11 6-4 • Junior • Guard 14 6-8 • Senior • Forward Duncanville, Texas Baton Rouge, La. Arlington, Texas Taunton, Massachusetts KEVIN MCCULLAR AVERY BENSON CHIBUZO AGBO VLADISLAV GOLDIN 15 6-6 • R-Sophomore • Guard 21 6-3 • Junior • Guard 23 6-7 • Freshman • Guard 50 7-1 • Freshman • Center San Antonio, Texas Springdale, Arkansas San Diego, California Nalchick, Russia CHRIS BEARD MARK ADAMS ULRIC MALIGI BOB DONEWALD SEAN SUTTON CASEY PERRIN JOHN REILLY MIKE NEAL Head Coach Associate Head Coach Assistant Coach Assistant Coach Advisor/Player Development Chief of Staff Strength & Conditioning Athletic Trainer KHRISTIAN SMITH MIKE FALLONE ROGER WOODS DREW BRYSON DRAKE LAMONT OLIVER HOUSTON JAMAAL SCOTT BROCK BERENATO Graduate Manager Graduate Manager Graduate Manager Graduate Manager Graduate Manager S&C Assistant Academic Advisor Video Coordinator TEXASTECH.COM 2020-21 Schedule DATE [DAY] OPPONENT LOCATION TIME TELEVISION NOV. 25 [WEDNESDAY] NORTHWESTERN STATE LUBBOCK - UNITED SUPERMARKETS ARENA 6 P.M. ESPN+ NOV. 27 [FRIDAY] SAM HOUSTON STATE LUBBOCK - UNITED SUPERMARKETS ARENA 1 P.M. ESPNU Nov. 29 [Sunday] vs. Houston Fort Worth - Dickies Arena 4:30 p.m. ESPN DEC. 3 [THURSDAY] TROY LUBBOCK - UNITED SUPERMARKETS ARENA 8 P.M. ESPN/ESPN2 DEC. 6 [SUNDAY] GRAMBLING LUBBOCK - UNITED SUPERMARKETS ARENA 1 P.M. -

Newsletter Colorado New Mexico Oklahoma Arkansas Texas Kansas Mexico February 2019

Newsletter Colorado New Mexico Oklahoma Arkansas Texas Kansas Mexico February 2019 The 2019 IAVM Region 6 Future Leaders Conference took place on January 14-16 at the Amarillo Civic Center Complex! Educational sessions were designed by the planning committee based on feedback from attendees in 2017 and included topics such as the challenges of young leadership, time management and self-care for future leaders, emergency action plan development, ticketed events from booking to settlement, different types of professional development available through IAVM, emergency preparedness, and a live Trained Crowd Manager course. Attendees also visited the world-famous Cadillac Ranch site and Big Texan Steak Ranch in addition to touring the Amarillo MPEV “Hodgetown” and the Globe-News Center for the Performing Arts. The goals of this conference were to provide helpful tools and information to attendees for their own growth and to take back to their respective venues and organizations, in addition to raising funds for Future Leaders Conference attendee stipends to attend the upcoming IAVM Region 6 Biennial Conference in spring 2020 in Fayetteville, AR. The conference succeeded in their goals by raising over $7,000 in funds for these stipends. The Co-Chairs of the Planning Committee, Ashley Peacock and Melinda Landry, would like to thank the Region 6 Board, our conference registrants and sponsors, and all those who assisted the planning committee and volunteered their time to help make sure this conference was a success. We hope to see everyone in Fayetteville, AR next year! Don’t forget to follow IAVM Region 6 on social media! Facebook Page Facebook Group Instagram LinkedIn Group Twitter @IAVMRegion6 IAVM Region 6 @IAVMRegion6 IAVM Region 6 @IAVMRegion6 Newsletter 1 Warning: Region 6 2020 Biennial Conference Shameless Plug Alert! Region 6 Has a New Scholarship Chair As Meredith Imes moves up to accept the Region 6 Assistant/Vice-Director position, it is with pleasure the Region 6 Board announces a new Scholarship Committee chair, Kelly K. -

Explore Fort Worth Tms & Alliance

So Many Districts. So Much to See. So Much to Do! VISITORS GUIDE EXPLORE FORT WORTH TMS & ALLIANCE Shopping, Dining Museum Mecca STOCKYARDS & Entertainment D/FW INTL AIRPORT PANTHER ISLAND RIVER DISTRICT WEST 7TH SUNDANCE SQUARE & DOWNTOWN CULTURAL DISTRICT NEAR SOUTHSIDE CAMP BOWIE CULTURAL DISTRICT WESTBEND The Cultural District features five internationally- SUNDANCE SQUARE & DOWNTOWN recognized museums: Kimbell Art Museum, Modern Art CLEARFORK Fort Worth’s city center buzzes day and night. It’s one of the cleanest Museum of Fort Worth, Amon Carter Museum most walkable urban areas you’ll find anywhere. The heart of downtown of American Art, National Cowgirl Museum and Hall of TCU & ZOO is Sundance Square, a 35-block shopping and entertainment district Fame and Fort Worth Museum of Science and History. Stroll where twinkling lights line sidewalks around beautifully restored through tree-lined streets while admiring the architecture For more information, including hotels, dining, events, buildings. Come meet the locals among restaurants, shops, galleries, Bass of the museums and the adjacent, art deco Will Rogers WATERSIDE coupons and more, please visit: FORTWORTH.COM Performance Hall and live theatre. FortWorth.com/SundanceSquare Memorial Center. FortWorth.com/CulturalDistrict TEXAS MOTOR SPEEDWAY & Boutiques on the Bricks Start Your Engines ALLIANCE African Savanna This growing area just north of downtown BILLY BOB'S TEXAS offers high-speed thrills at Texas Motor Speedway, one of the best and largest sports stadiums in the U.S. and home to the world’s largest HD video screen, nicknamed “Big Hoss.” Enjoy shopping at nearby Tanger Outlets. See YEAR-ROUND FUN IN THE CITY WHERE THE WEST BEGINS millions of dollars made before your eyes at the Dates available at time of printing. -

YEAR in REVIEW 2019 Event at Web- Ster Hall After Its Reopening

BACK IN BUSI- NESS: Bishop Briggs plays an YEAR IN REVIEW 2019 event at Web- ster Hall after its reopening. (Getty Images) CONTINUED FROM PAGE 51 our expectations. From show count, Verizon launching in 14 venues during the audience reaction, 2019 football season, while AT&T rolled it economic impact out at the Dallas Cowboys’ AT&T Stadium in the neighbor- in Arlington, Texas. In the digital realm, the hood, it has been a $1.1 billion esports sector made a deeper truly rewarding and move into traditional venues such as newly humbling experience renovated TD Garden in Boston, and the for our team,” says Overwatch League is developing a network Geoff Gordon, re- of buildings to host events around the world, gional president for even as it eyes building custom arenas for its Live Nation Philadel- events in the next year. phia. “The Met has Check out some of the year’s other top really been about the stories: convergence of the growth of the city with an amazing building — 94 feet across, 65 deep and 80 high — OPENING ACTS that deserved this.” rivals the dimensions of New York’s Radio THE MET PHILADELPHIA — The latest The revamped venue includes a spa- City Music Hall. The building hosted 164 addition to the city’s live music scene opened cious lobby, plus velour theater seating, 25 shows in its inaugural season and as of with a bang on Dec. 3, 2018, with a Bob bars, a ring of deluxe box seats, wrap- October had donated more than $74,337 Dylan show at the reclaimed historic hall around balconies, gently sloped upper to the School District of Philadelphia, part on the northern fringe of Philly’s Center decks and a surprisingly intimate show- of a pledge to give 25 cents of every ticket City. -

EBBY-PRESENTATION.Pdf

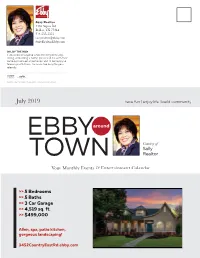

GayleneSuzy Realtor Anders Ebby4455 Sigma Halliday, Rd REALTORS® 157Dallas,5 E. TX Southlake 75244 Blvd #100 Southlake,214-555-5555 TX 76092 [email protected] [email protected] ebby.com OH, BY THE WAY Ifyouknowofanyone who’s thinking of buying, selling, or building a home, please call me with their name and contact information and I’ll be happy to follow up with them. I’m never too busy for your referrals. Equal Housing Opportunity. Not intended to solicit property already listed. have fun | enjoy life | build community EBBYaround Courtesy of TOWN Gaylene Anders Your Monthly Events & Entertainment Calendar >> 5 Bedrooms >> 5 Baths >> 3 Car Garage >> 4,519 sq. ft. >> $499,000 Allen, spa, patio kitchen, gorgeous landscaping! 3452CountryEastRd.ebby.com GayleneSuzy Anders Realtor around 214-673-9622214-555-5555 EBBY [email protected]@ebby.com SuzyRealtor.Ebby.com TOWN SPOTLIGHT around town THROUGHOUT THE METROPLEX music theatre DIOR: FROM PARIS TO THE OUTLAW MUSIC FESTIVAL WITH KING ARTHUR AND THE WORLD WILLIE NELSON SHOPPES AT CAMELOT Dallas Museum of Art Dos Equis Pavilion McKinney Performing Arts Center 214-922-1200 Shakespeare in 214-421-1111 972-547-2650 dma.org fairpark.org mckinneyperformingartscenter.org Through Sep. 1 Jul 3 Jul 11-13 Love at Samuell MONET: THE LATE YEARS THROUGH JULY 21 JULY THROUGH Grand Park CONCERTS IN THE GARDEN: HELLO, DOLLY! Kimbell Art Museum STARS WARS AND BEYOND Music Hall at Fair Park 817-332-8451 Young Will Shakespeare has writer’s Fort Worth Botanic Garden 214-413-3964 kimbellart.org 817-392-5510 dallassummermusicals.org Through Sep. -

July 2020 Newsletter

Newsletter Colorado New Mexico Oklahoma Arkansas Texas Kansas Mexico July 2020 Mark Your Calendar: IAVM Region 6 Business Meeting on July 28 Jeff Davis, CVE, Region 6 Director Hello, Region 6! 2020 has proven to be a year unlike any other! Live events came to a screeching halt nearly four months ago, and now we are all navigating uncharted waters as we work toward reopening venues in a safe manner. In any other year, we would come together at the annual IAVM VenueConnect conference to network, share experiences and learn from each other. However, with the COVID-19 pandemic, our summer plans have changed. This year, we’re taking our annual IAVM Region 6 Business Meeting online. Yes, one more Zoom meeting to add to your calendar. However, this is one you will not want to miss! We have a few business items and IAVM updates to address early on in the meeting. But after that, we’ll spend time visiting with some of our colleagues who are in the early stages of reopening, hear what’s working… and what’s not, ask questions, and share ideas that can help us all as we work toward safely reopening our venues. Mark your calendars now: IAVM Region 6 Business Meeting Tuesday, July 28 10:00 – 11:15 AM (Central) And register online here: https://us02web.zoom.us/meeting/register/tZ0ldeuuqD8sGtXFlnfEDlsz_P1Jcz6YgtgA We’ll see you online in a few weeks! Jeff Davis, CVE Region 6 Director Newsletter 1 The Tobin Center Uses State of the Art Technology to Maintain 6 Feet of Row Separation Article Courtesy of Broadway World: https://www.broadwayworld.com/san-antonio/article/The-Tobin-Center-Uses-State-of-the-Art- Technology-to-Maintain-Six-Feet-of-Separation-Between-its-Rows-20200616 San Antonio Express-News has reported that The Tobin Center is using one of a kind technology to maintain six feet of separation between its rows. -

Newsletter Colorado New Mexico Oklahoma Arkansas Texas Kansas Mexico July 2018 Walton Arts Center Employee Earns Arkansas Volunteer Certification

Newsletter Colorado New Mexico Oklahoma Arkansas Texas Kansas Mexico July 2018 Walton Arts Center Employee Earns Arkansas Volunteer Certification Beth Hopkins, administrative assistant for volunteer programs at Walton Arts Center, is now a Certified Volunteer Manager (CVM) by the Arkansas Public Administration Consortium. CVM is a nationally recognized certification designed for administrators, directors, managers and coordinators of volunteers and volunteer programs. To earn the certification more than 60 hours of study is required in topics that include recruitment and retention strategies, trends in volunteer programs, volunteer screening, placement, training and supervision. Hopkins has been in her role working with volunteers at Walton Arts Center since 2004. More than 200 volunteers fill a variety of roles during shows and events and in the administrative offices. These volunteers donate more than 25,000 hours to the organization, or the equivalent of 13 full-time paid positions. Plano City Council Reviews, Approves Proposal to Build 4-Star Radisson Hotel at Plano Event Center The Plano Event Center could have a new 4-star neighbor by the spring of 2020, adding a key partner to the popular meeting and events venue. At their June 25 meeting, the Plano City Council authorized the City Manager to enter into a lease agreement with Tirgo, LLC for approximately 5 acres of land adjacent to Plano Event Center for the purpose of building a Radisson Hotel. The convention center hotel would connect to Plano Event Center, complete with 175 rooms, a full-service restaurant, business center, exercise facilities, meeting space and the latest hotelier technology. The hotel would operate on a cooperative agreement with Plano Event Center, coordinating with one another for bookings and use of its facilities. -

Want to Get Out?

BRAVO GUIDE TO ENTERTAINMENT MARCH 11, 2021 WANT TO GET OUT? S afety is our priority. We are working hard to keep our senior care Artist needs help communities safe. Our team is ready to answer with Minden origami any questions you have about ongoing location project. — Page 5 availability and safety precautions. Call (308) 234-1888 to learn more. All faiths or beliefs are welcome. © 2020 The Evangelical Lutheran Good Samaritan Society. All rights reserved. 201870 Linda Stephen, courtesy “THE PATH Through the Corn Maze,” by Linda Stephen, origami. “Some“ “SS oomm ee adviseaa dd vviiss ee -- IfIIff losllooss tt iniinn aa W h ic h w ill f foororreeste ss tt,, ffoollowollllooww aa ppospooss s s u umumm . ........ lead you to EEvent Evvee nn ttuuauaa l llylllyy hh e e ww i illillll eende nn dd uupupp iin inn tthheh ee mmiddlem iidd dd llee oofoff tthheh ee rrooad”oaa dd ”” 2109 CENTRAL AVE DOWNTOWN KEARNEY 308-236-5031 2 DIVERSIONS KEARNEY HUB — THURSDAY, MARCH 11, 2021 McCollum means the country he sings KEARNEY — A singer/song- respectful, and to outwork every- writer, multi-instrumentalist, and body.” dedicated road warrior, Parker WHEN AND WHERE McCollum just released his new McCollum began building a What: Red Dirt on the EP, “Hollywood Gold,” which following in his native Texas with River 7 with headliner the singer named after a horse his his 2015 release, “The Limestone Parker McCollum grandfather owned decades ago. Kid.” When: 7 p.m. Friday “Hollywood Gold” includes The album track, “Meet You Where: Viaero Center, McCollum’s debut single, “Pretty 609 Platte Road in the Middle,” became a hit on Admission: $30-$65 Heart,” which already has cracked Texas’ regional radio chart — no Contact: 308-338-8011; Top 10 on the country radio small feat for an independent, KearneyEvents.net chart averaging almost 4 million 22-year-old musician — but it streams a week and recently was was the album’s widely acclaimed certifi ed Gold. -

December 2019 Newsletter

Newsletter Colorado New Mexico Oklahoma Arkansas Texas Kansas Mexico December 2019 Registration is officially open for the 2020 IAVM Region 6 Biennial Conference! When: April 5-8, 2020 Where: Walton Arts Center in Fayetteville, AR Click here to register NOW! Professional development Networking opportunities Educational sessions Local arts and culture Venue tours And more! Thank you to our sponsors who are making this conference possible: Walton Arts Walmart Experience Faulkner Performing Center AMP Fayetteville Arts Center Crystal Bridges Museum The Momentary University of Arkansas of American Art Athletics Be sure to follow IAVM Region 6 on social media! Facebook Instagram LinkedIn Twitter @IAVMRegion6 @IAVMRegion6 IAVM Region 6 @IAVMRegion6 Newsletter 1 Venue Management School Scholarships Available! Our region actively works to engage our membership in educational opportunities. To meet this goal, Region 6 is providing two scholarships for the 2020 sessions. VMS Scholarship Applications are due Friday, January 17, 2020. Region 6 funds a two-year scholarship for the Venue Management School (VMS) at Saddlebrook Resort in Tampa, FL. It is scheduled for June 6-12, 2020. First year students are eligible for the scholarship which fully funds tuition, housing and taxes for both years of the program. Those interested in attending the school and in need of scholarship assistance are encouraged to apply Year 1 & 2 Scholarship. In addition, Region 6 offers a Graduate Institute scholarship for those venue professionals looking for advanced education. The Graduate Institute is also scheduled for June 6-12, 2020 in Tampa, FL. The scholarship will cover the cost of tuition, housing and taxes. If you are interested in attending the Graduate Institute and in need of scholarship assistance please apply Graduate Institute Scholarship. -

Attendance and Sites

ATTENDANCE AND SITES Attendance History 192 Attendance Records 194 All-Time Site and Arena History 196 Tournament Game Arenas By Site 197 Future Dates and Sites 213 ATTENDANCE HISTORY BY TOURNAMENT Year Final Final *Total Sess. Avg. Final Site Final Facility No. of Date Crowd Atten. Atten. Teams 1939 3-27 5,500 15,025 5 3,005 Evanston, IL Patten Gymnasium 8 1940 3-30 10,000 36,880 5 7,376 Kansas City, MO Municipal Auditorium 8 1941 3-29 7,219 48,055 5 9,611 Kansas City, MO Municipal Auditorium 8 1942 3-28 6,500 24,372 5 4,874 Kansas City, MO Municipal Auditorium 8 1943 3-30 13,300 56,876 5 11,375 New York Madison Square Garden 8 1944 3-28 15,000 59,369 5 11,874 New York Madison Square Garden 8 1945 3-27 18,035 67,780 5 13,556 New York Madison Square Garden 8 1946 3-26 18,479 73,116 5 14,623 New York Madison Square Garden 8 1947 3-25 18,445 72,959 5 14,592 New York Madison Square Garden 8 1948 3-23 16,174 72,523 5 14,505 New York Madison Square Garden 8 1949 3-26 10,600 66,077 5 13,215 Seattle Edmundson Pavilion 8 1950 3-28 18,142 75,464 5 15,093 New York Madison Square Garden 8 1951 3-27 15,348 110,645 9 12,294 Minneapolis Williams Arena 16 1952 3-26 10,700 115,712 10 11,571 Seattle Edmundson Pavilion 16 1953 3-18 10,500 127,149 14 9,082 Kansas City, MO Municipal Auditorium 22 1954 3-20 10,500 115,391 15 7,693 Kansas City, MO Municipal Auditorium 24 1955 3-19 10,500 116,983 15 7,799 Kansas City, MO Municipal Auditorium 24 1956 3-23 10,600 132,513 15 8,834 Evanston, IL McGaw Hall 25 1957 3-23 10,500 108,891 14 7,778 Kansas City, MO Municipal -

TCC Arena Floor & Ice Machine Design Build Contract

DESIGN – BUILD AGREEMENT BETWEEN RIO NUEVO MULTIPURPOSE FACILITIES DISTRICT AND LLOYD CONSTRUCTION COMPANY, INC. THIS DESIGN - BUILD AGREEMENT (this “Agreement”) is made February __, 2019, by and between the Rio Nuevo Multipurpose Facilities District, an Arizona tax levying public improvement district (the “District”), and Lloyd Construction Company, Inc., an Arizona corporation (the “Contractor”), for complete design and construction services related to the renovation of the Tucson Convention Center ice rink refrigeration system and other items as deemed necessary by the District (the “Project”). The District and the Contractor are referred to herein individually as a “Party” and collectively as the “Parties.” ARTICLE 1 GENERAL 1.1 Project Summary. The Contractor shall perform all pre-construction services set forth in Article 2 below (the “Pre-Construction Services”) and, subject to Section 1.2 below, management and construction services set forth in Article 4 below (the “Construction Services”) (the Pre-Construction Services and the Construction Services are collectively referred to as the “Services”), including providing all material, equipment, tools and labor necessary to complete the Work (as defined below) described herein and reasonably inferable from the Contract Documents (as defined below), including the upgrades and improvements to be encompassed in the Project. The Contractor will also take the necessary steps to ensure that the Project design is constructible within the established budget. 1.2 Phased Agreement. The Services contemplated by this Agreement shall be carried out in several distinct phases. The initial Services shall be to provide Pre-Construction Services including (A) such environmental investigation services as applicable pursuant to Section 2.1 below, (B) creating all design documents including the Construction Documents pursuant to Section 2.2 below and (C) the Pre-Construction Phase General Services, pursuant to Section 2.3 below (the “Pre-Construction Phase General Services”).