Rate-And-Term Refinance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

AIG Investments Jumbo Underwriting Guidelines

AIG Investments Jumbo Underwriting Guidelines December 20, 2019 These AIG Investments Jumbo Underwriting Guidelines (Exhibit A-2) are dated December 20, 2019. The Underwriting Guidelines may be updated or modified from time to time. AIG Investments believes the information contained in this document relating to state laws and third party requirements to be accurate as of January 1, 2020. However, this information is provided for informational purposes only and may change at any time without notice. AIG Investments is providing this information without any warranties, express or implied. © 2019 AIG Investments. All Rights Reserved. AIG Investments is an affiliate of American International Group, Inc. ("AIG”). AIG Investments is the program administrator for this program and not the purchaser of the loan. Please refer to the AIG Investments Correspondent Seller's Guide for additional information regarding the relationship between the parties. MC-2-A987C-1016 Table of Contents Table of Contents ..................................................................................................................................................................................................................... 1 Jumbo Loan Underwriting Introduction ................................................................................................................................................................................. 5 Chapter One: General ..................................................................................................................................................................................................... -

Good Faith Estimate (GFE)

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Borrower Originator Property Address Address Originator Phone Number Originator Email Date of GFE Purpose This GFE gives you an estimate of your settlement charges and loan terms if you are approved for this loan. For more information, see HUD’s Special Information Booklet on settlement charges, your Truth-in-Lending Disclosures, and other consumer information at www.hud.gov/respa. If you decide you would like to proceed with this loan, contact us. Shopping for Only you can shop for the best loan for you. Compare this GFE with other loan offers, so you can find your loan the best loan. Use the shopping chart on page 3 to compare all the offers you receive. Important dates 1. The interest rate for this GFE is available through . After this time, the interest rate, some of your loan Origination Charges, and the monthly payment shown below can change until you lock your interest rate. 2. This estimate for all other settlement charges is available through . 3. After you lock your interest rate, you must go to settlement within days (your rate lock period) to receive the locked interest rate. 4. You must lock the interest rate at least days before settlement. Summary of Your initial loan amount is $ your loan Your loan term is years Your initial interest rate is % Your initial monthly amount owed for principal, interest, and any mortgage insurance is $ per month Can your interest rate rise? c No c Yes, it can rise to a maximum of %. -

Chapter 3: Escrow, Taxes, and Insurance

HB-2-3550 CHAPTER 3: ESCROW, TAXES, AND INSURANCE 3.1 INTRODUCTION To protect the Agency’s interest in the security property, the Servicing and Asset Management Office (Servicing Office) must ensure that real estate taxes and any other local assessments are paid and that the property remains adequately insured. To ensure that funds are available for these purposes, the Agency requires most borrowers who receive new loans to deposit funds to an escrow account. Borrowers who are not required to establish an escrow account may do so voluntarily. If an escrow account has been established, payments for insurance, taxes, and other assessments are made by the Agency. If an escrow account has not been established, the borrower is responsible for making timely payments. Section 1 of this chapter describes basic requirements for paying taxes and maintaining insurance coverage; Section 2 provides procedure for establishing and maintaining the escrow account; and Section 3 discusses procedures for addressing insured and uninsured losses to the security property. SECTION 1: TAX AND INSURANCE REQUIREMENTS [7 CFR 3550.60 and 3550.61] 3.2 TAXES AND OTHER LOCAL ASSESSMENTS The Agency contracts with a tax service to secure tax information for all borrowers. The tax service obtains tax bills due for payment, determines the optimal time to pay the taxes in order to take advantage of any discounts, and provides delinquent tax status on the portfolio. A. Tax Service Fee All borrowers are charged a tax service fee. Borrowers who obtain a subsequent loan are not required to pay a second tax service fee. -

Contract for Sale of Real State

CONTRACT FOR SALE OF REAL STATE This Contract for Sale is made on , 20 BETWEEN whose address is , referred to as the Seller, AND whose address is , referred to as the Buyer. The words "Buyer" and "Seller" include all buyers and all Sellers listed above. 1. Purchase Agreement. The Seller agrees to sell and the Buyer agrees to buy the property described in this contract. 2. Property. The property to be sold consists of (a) the land and all the buildings, other improvements and fixtures on the land; (b) all of the Seller's rights relating to the land; and (c) all personal property specifically included in this contract. The real property to be sold is commonly known as in the Township of in the County of and State of New Jersey. It is shown on the municipal tax map as lot in block . This property is more fully described in the attached Schedule A. 3. Purchase Price. The purchase price is $ 4. Payment of Purchase Price. The Buyer will pay the purchase price as follows: Previously paid by the Buyer (initial deposit) $ Upon signing of this contract (balance of deposit) $ Amount of mortgage (paragraph 6) $ By assuming the obligation to pay the present mortgage according to its terms, $ this mortgage shall be in good standing at the closing. Either party may cancel this contract if the Lender does not permit the Buyer to assume the mortgage (estimated balance due). By the Seller taking back a note and mortgage for years at % $ interest with monthly payments based on a payment schedule. -

Chicago Association of Realtors® Condominium Real Estate Purchase and Sale Contract

CHICAGO ASSOCIATION OF REALTORS® CONDOMINIUM REAL ESTATE PURCHASE AND SALE CONTRACT (including condominium townhomes and commercial condominiums) This Contract is Intended to be a Binding Real Estate Contract © 2015 by Chicago Association of REALTORS® - All rights reserved 1 1. Contract. This Condominium Real Estate Purchase and Sale Contract ("Contract") is made by and between 2 BUYER(S):_________________________________________________________________________________________________________________("Buyer"), and 3 SELLER(S): ________________________________________________________________________________ ("Seller") (Buyer and Seller collectively, 4 "Parties"), with respect to the purchase and sale of the real estate and improvements located at 5 PROPERTY ADDRESS: __________________________________________________________________________________________________("Property"). 6 (address) (unit #) (city) (state) (zip) 7 The Property P.I.N. # is ____________________________________________. Approximate square feet of Property (excluding parking):________________. 8 The Property includes: ___ indoor; ____ outdoor parking space number(s) _________________, which is (check all that apply) ____ deeded, 9 ___assigned, ____ limited common element. If deeded, the parking P.I.N.#: ______________________________________. The property includes storage 10 space/locker number(s)_____________, which is ___deeded, ___assigned, ___limited common element. If deeded, the storage space/locker 11 P.I.N.#______________________________________. 12 2. Fixtures -

TILA Higher-Priced Mortgage Loans (HPML) Escrow Rule

March 2016 TILA Higher-Priced Mortgage Loans (HPML) Escrow Rule Small entity compliance guide Version Log The Bureau updates this guide on a periodic basis to reflect finalized amendments and clarifications to the rule which impact guide content. Below is a version log noting the history of this document and notable rule changes: Date Version Rule Changes March 28, 1.2 Exemption for Small Creditors that Operate in a Rural 2016 or Underserved Area. The September 2015 Final Rule amends the eligibility criteria for small creditors operating in rural or underserved areas for exemption from the requirement to establish an escrow account for higher-priced mortgage loans (HPMLs). The March 2016 Interim Final Rule further amends the definition of rural areas and replaces the requirement that a small creditor operate predominantly in rural and underserved areas to be eligible for the escrow exemption with a requirement that a small creditor operate in a rural or underserved area. The revised rural-or-underserved test extends eligibility to small creditors that originated at least one covered loan secured by a first lien on a property located in a rural or underserved area in the preceding calendar year. It also amends the conditions for exempting small creditors from the requirement to maintain escrows so that an otherwise eligible small creditor will be able to rely on the exemption if it and its affiliates continue to maintain escrows established for first-lien HPMLs if the application for the HPML was received between April 1, 1 2010 and May 1, 2016. (See “What are the exemptions to the TILA HPML Escrow Rule?”on page 13 and “What are the loan volume and size requirements to qualify for the exemption for creditors operating in a rural or underserved area?” on page 14. -

Avoid Foreclosure: Pre‐Foreclosure Sale & Deed in Lieu to the Rescue!

Avoid Foreclosure: Pre‐Foreclosure Sale & Deed In Lieu to the Rescue! Section 502 Guarantee Loan Program Welcome to “Avoid Foreclosure: Pre‐Foreclosure and Deed in Lieu to the Rescue! This presentation will review more effective ways to leverage the pre‐foreclosure and deed in lieu loss mitigation options to help more USDA guaranteed loan borrowers avoid foreclosure! 1 SFH Guaranteed COST OF FORECLOSURE Survey of FY 2017 paid claims • Average loss claim: $50,990 • Average liquidation costs: $6,168 Foreclosure is certainly not cost effective. Not for the borrower. Not for the lender. Not for the U.S. Government. In a review of over 11,600 loss claims paid due to foreclosure in calendar year 2017: • The average loss claim was over $50,000 and • Average liquidation costs per claim were over $6,000 These figures include loss claims paid for properties sold while in REO, unsold but held in REO, and foreclosures completed through third parties. That’s a lot of money! 2 SFH Guaranteed LOSS MITIGATION OPTION USE Loan Modification 49% Repayment Agreements 45% Pre‐Foreclosure Sales (Less than 1%) Deed In Lieu (Less than 1%) This chart represents over 14,700 lender approved loan servicing plans for calendar year 2017. • 7,166 were loan modifications and Special Loan Servicing modifications • 6,623 were forbearance repayment agreements • 805 are short sales, and only • 121 are deed‐in‐lieu 3 SFH Guaranteed COULD FORECLOSURE BE AVOIDED? The big question we would like to answer is: Could foreclosure have been avoided? 4 SFH Guaranteed EVIDENCE OF HOPE • Less than 3,000 claims • Not due to foreclosure There is evidence that USDA’s loss mitigation strategies, when approved and executed, are halting the breaks on foreclosure activity. -

Commonly Used Real Estate Transaction Terms

Commonly Used Real Estate Transaction Terms The following terms are utilized frequently in real estate transactions that are not used in implementing other NRCS conservation programs. The definitions provided for this list of terms does not supersede definitions provided in the WRP manual or in the Department of Justice title standards, but is intended to clarify frequently used terms. 1. “Exceptions and clouds on title” refers to any evidence that the landowner is not in full control of the property to be encumbered by the Wetlands Restoration Program (WRP) easement or contract or that the property cannot be used for wetland restoration purposes. Exceptions and clouds on title can include mechanics’ liens, mortgages, judgments, divorce decrees, other conservation easements, hazardous waste risks, and squatters’ rights. 2. “Title search documents” refers to the summaries of information regarding the documents obtained by searching the land records, court dockets, and other public records. These summaries are contained in documents entitled “Preliminary Title Report,” “Title Commitment Binder,” “Title Abstract,” and the like. 3. “Underlying documents” refers to the individual documents listed in the title search documents summary that are obtained by searching the land records, court dockets, and other public records. 4. “Closing agent” refers to the person or entity preparing the title search document, providing the underlying documents, or handling the closing and legal transfer of title and ownership from the seller to the buyer. The closing agent is typically not an agent of either party, but simply the person entrusted to carry out all non-conflicting instructions from all parties. In WRP transactions, the closing agent is hired by NRCS and thus is consider a buyer’s agent. -

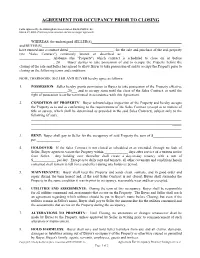

Agreement for Occupancy Prior to Closing

AGREEMENT FOR OCCUPANCY PRIOR TO CLOSING Form approved by the Birmingham Association of REALTORS®, Inc. March 29, 2006 (Previous forms obsolete and are no longer approved) WHEREAS, the undersigned SELLER(S)__________________________________________________ and BUYER(S)_____________________________________________________________________________ have entered into a contract dated , for the sale and purchase of the real property (the "Sales Contract") commonly known or described as ________________________________ _________________, Alabama (the "Property") which contract is scheduled to close on or before ___________________, 20__. Buyer desires to take possession of and to occupy the Property before the closing of the sale and Seller has agreed to allow Buyer to take possession of and to occupy the Property prior to closing on the following terms and conditions: NOW, THEREFORE, SELLER AND BUYER hereby agree as follows: 1. POSSESSION: Seller hereby grants permission to Buyer to take possession of the Property effective ____________________,20___ and to occupy same until the close of the Sales Contract, or until the right of possession is earlier terminated in accordance with this Agreement. 2. CONDITION OF PROPERTY: Buyer acknowledges inspection of the Property and hereby accepts the Property as is and as conforming to the requirements of the Sales Contract (except as to matters of title or survey, which shall be determined as provided in the said Sales Contract), subject only to the following (if any): _____ _____ _____ 3. RENT: Buyer shall pay to Seller for the occupancy of said Property the sum of $________________ per _____________. 4. HOLDOVER: If the Sales Contract is not closed as scheduled or as extended, through no fault of Seller, Buyer agrees to vacate the Property within _____________ days after service of a written notice from Seller. -

Closing Checklist Selling Agent Responsibilities *Be Certain That All Parties Have Copies of Any Documents That They Have Signed Or Initialed, Including the Contract

Closing Checklist Selling Agent Responsibilities *Be certain that all parties have copies of any documents that they have signed or initialed, including the contract. Prepare For Negotiation Date Completed __/__ ___ 1. Pre-qualify Purchaser, get pre-qualification letter. __/__ ___ 2. Prepare cost sheet for purchaser. __/__ ___ 3. Prepare cover letter to Listing Agent personalizing the purchaser. __/__ ___ 4. Prepare the VPAR Settlement Transmittal Form. __/__ ___ 5. Make certain that the purchaser signs the Virginia Residential Property Disclosure or Disclaimer. __/__ ___ 6. Make certain that the purchaser signs the Lead Based Paint Disclosure if applicable. __/__ ___ 7. Return a copy of the ratified contract to the purchaser. Turn the contract in to the sales secretary. __/__ ___ 8. If Power of Attorney is to be used at closing locate original and deliver copy to settlement agent. Week 1 __/__ ___ 1. Deliver the POA/Condo Packet if applicable; have the purchaser sign for proof of receipt. __/__ ___ 2. Get the purchaser to a mortgage company within seven (7) working days of contract ratification for loan application. __/__ ___ 3. Arrange and attend the home inspection; negotiate any deficiency lists. __/__ ___ 4. Deliver a copy of the contract to the attorney and lender with the settlement Transmittal form. Week 2 __/__ ___ 1. Check with the Mortgage Company. Has appraisal been ordered? __/__ ___ 2. Report to the purchaser regarding the status of the loan. __/__ ___ 3. -

Homeservices of America Names Chief Diversity and Inclusion Officer

HomeServices of America Names Chief Diversity and Inclusion Officer Posted on July 16, 2020 at 6:18 pm. MINNEAPOLIS, MN (July 16, 2020) — Gino Blefari, CEO of HomeServices of America, a Berkshire Hathaway affiliate, has appointed Teresa Palacios Smith as Chief Diversity and Inclusion Officer for HomeServices and its subsidiaries, including its family of brokerage, mortgage, insurance, settlement-services, and relocation companies, and HSF Affiliates, which operates the Berkshire Hathaway HomeServices and Real Living franchise networks. In her role, Palacios Smith will lead HomeServices’ employee- and agent-diversity programs, cultivate a culture of equity and inclusion, and champion the company’s goal of increasing minority homeownership. “There’s no place like home. Our home is a place that we associate with acceptance, family, love, safety, and belonging,” said Palacios Smith. “HomeServices eXemplifies this and I’m honored to lead the diversity and inclusion efforts of a company that values its people, promotes diversity, equity, and inclusion, and cherishes homeownership and fair housing for all.” Palacios Smith began her career as a successful real estate agent and served on Berkshire Hathaway HomeServices Georgia Properties’ management team. In 2017, she joined HSF Affiliates as its Vice President of Diversity & Inclusion for the Berkshire Hathaway HomeServices and Real Living franchise networks. During her more than 20 years in the real estate industry, Palacios Smith has been a national speaker and trainer who has focused on emerging markets, unconscious bias, and real estate trends in diverse market segments. She serves on the boards of many of the country’s top housing organizations that focus on supporting people from traditionally underserved communities and is recognized for her dedication to eXpanding and celebrating leadership opportunities in real estate for women. -

Good Faith Estimate (GFE)

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Borrower Originator Property Address Address Originator Phone Number Originator Email Date of GFE Purpose This GFE gives you an estimate of your settlement charges and loan terms if you are approved for this loan. For more information, see HUD’s Special Information Booklet on settlement charges, your Truth-in-Lending Disclosures, and other consumer information at www.hud.gov/respa. If you decide you would like to proceed with this loan, contact us. Shopping for Only you can shop for the best loan for you. Compare this GFE with other loan offers, so you can find your loan the best loan. Use the shopping chart on page 3 to compare all the offers you receive. Important dates 1. The interest rate for this GFE is available through . After this time, the interest rate, some of your loan Origination Charges, and the monthly payment shown below can change until you lock your interest rate. 2. This estimate for all other settlement charges is available through . 3. After you lock your interest rate, you must go to settlement within days (your rate lock period) to receive the locked interest rate. 4. You must lock the interest rate at least days before settlement. Summary of Your initial loan amount is $ your loan Your loan term is years Your initial interest rate is % Your initial monthly amount owed for principal, interest, and any mortgage insurance is $ per month Can your interest rate rise? c No c Yes, it can rise to a maximum of %.