Dunedin Visitor Strategy 2008 – 2015 July 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Look Inside 10 Days in the Life of Auckland War Memorial Museum CONTENTS

Look inside 10 days in the life of Auckland War Memorial Museum CONTENTS Ka puāwai ngā mahi o tau kē, Year in Review Ka tōia mai ā tātou kaimātaki i ēnei rā, Ka whakatō hoki i te kākano mō āpōpō. Sharing our Highlights 2014/2015 6 Board Chairman, Taumata-ā-Iwi Chairman and Director’s Report 8 Building on our past, 10 Days in the Life of Auckland War Memorial Museum 10 Engaging with our audiences today, Investing for tomorrow. Governance Trust Board 14 We are pleased to present our Taumata-ā-Iwi 16 Annual Report 2014/2015. Executive Team 18 Pacific Advisory Group 20 Youth Advisory Group 21 Governance Statement 22 Board Committees and Terms of Reference 24 Partnerships Auckland Museum Institute 26 Auckland Museum Circle Foundation 28 Funders, Partners and Supporters 30 BioBlitz 2014 Tungaru: The Kiribati project Research Update 32 Performance Te Pahi Medal Statement of Service Performance 38 Auditor’s Report: Statement of Service Performance 49 Entangled Islands Contact Information 51 exhibition Illuminate projections onto the Museum Financial Performance Financial Statements 54 Dissection of Auditor’s Report: Financial Statements 88 Great White Shark Financial Commentary 90 Flying over the Antarctic This page and throughout: Nautilus Shell SECTION SECTION Year in Review 4 5 YEAR IN REVIEW YEAR IN REVIEW Sharing our Highlights 2014/2015 A strong, A compelling Accessible Active sustainable destination ‘beyond participant foundation the walls’ in Auckland 19% 854,177 1 million 8 scholars supported by the Museum to reduction in overall emissions -

Low Cost Food & Transport Maps

Low Cost Food & Transport Maps 1 Fruit & Vegetable Co-ops 2-3 Community Gardens 4 Community Orchards 5 Food Distribution Centres 6 Food Banks 7 Healthy Eating Services 8-9 Transport 10 Water Fountains 11 Food Foraging To view this information on an interactive map go to goo.gl/5LtUoN For further information contact Sophie Carty 03 477 1163 or [email protected] - INFORMATION UPDATED 10 / 2017 - WellSouth Primary Health Network HauoraW MatuaellSouth Ki Te Tonga Primary Health Network Hauora Matua Ki Te Tonga WellSouth Primary Health Network Hauora Matua Ki Te Tonga g f e h a c b d Fruit & Vegetable Co-ops All Saints' Fruit & Veges https://store.buckybox.com/all-saints-fruit-vege Low cost fruit and vegetables ST LUKE’S ANGLICAN CHURCH ALL SAINTS’ ANGLICAN CHURCH a 67 Gordon Rd, Mosgiel 9024 e 786 Cumberland St, North Dunedin 9016 OPEN: Thu 12pm - 1pm and 5pm - 6pm OPEN: Thu 8.45am - 10am and 4pm - 6pm ANGLICAN CHURCH ST MARTIN’S b 1 Howden Street, Green Island, Dunedin 9018, f 194 North Rd, North East Valley, Dunedin 9010 OPEN: Thu 9.30am - 11am OPEN: Thu 4.30pm - 6pm CAVERSHAM PRESBYTERIAN CHURCH ST THOMAS’ ANGLICAN CHURCH c Sidey Hall, 61 Thorn St, Caversham, Dunedin 9012, g 1 Raleigh St, Liberton, Dunedin 9010, OPEN: Thu 10am -11am and 5pm - 6pm OPEN: Thu 5pm - 6pm HOLY CROSS CHURCH HALL KAIKORAI PRESBYTERIAN CHURCH d (Entrance off Bellona St) St Kilda, South h 127 Taieri Road, Kaikorai, Dunedin 9010 Dunedin 9012 OPEN: Thu 4pm - 5.30pm OPEN: Thu 10.30am - 1pm * ORDER 1 WEEK IN ADVANCE WellSouth Primary Health Network Hauora Matua Ki Te Tonga 1 g h f a e Community Gardens Land gardened collectively with the opportunity to exchange labour for produce. -

Implementing Integrated Care 29 Aug 2017 Dunedin, New Zealand

Implementing Integrated Care 29 Aug 2017 Dunedin, New Zealand Symposium Report Table of Contents Introduction .................................................................................................................................. 1 Proceedings ................................................................................................................................... 1 Opening Remarks ...................................................................................................................... 1 Session 1: A Brief Introduction of CHeST .................................................................................... 2 Session 2: Keynote speakers ...................................................................................................... 4 Session 3: Panel discussion ........................................................................................................ 6 Closing remarks ......................................................................................................................... 6 Feedback ....................................................................................................................................... 7 Annex 1: Participants ..................................................................................................................... 8 Annex 2: Symposium Programme ................................................................................................ 12 Introduction The 1st annual symposium of The Centre for Health Systems and Technology -

Flood Hazard of Dunedin's Urban Streams

Flood hazard of Dunedin’s urban streams Review of Dunedin City District Plan: Natural Hazards Otago Regional Council Private Bag 1954, Dunedin 9054 70 Stafford Street, Dunedin 9016 Phone 03 474 0827 Fax 03 479 0015 Freephone 0800 474 082 www.orc.govt.nz © Copyright for this publication is held by the Otago Regional Council. This publication may be reproduced in whole or in part, provided the source is fully and clearly acknowledged. ISBN: 978-0-478-37680-7 Published June 2014 Prepared by: Michael Goldsmith, Manager Natural Hazards Jacob Williams, Natural Hazards Analyst Jean-Luc Payan, Investigations Engineer Hank Stocker (GeoSolve Ltd) Cover image: Lower reaches of the Water of Leith, May 1923 Flood hazard of Dunedin’s urban streams i Contents 1. Introduction ..................................................................................................................... 1 1.1 Overview ............................................................................................................... 1 1.2 Scope .................................................................................................................... 1 2. Describing the flood hazard of Dunedin’s urban streams .................................................. 4 2.1 Characteristics of flood events ............................................................................... 4 2.2 Floodplain mapping ............................................................................................... 4 2.3 Other hazards ...................................................................................................... -

8 Day Southern Scenic Route

8 Day Southern Scenic Route The Journey Few New Zealand road trips rival the Southern Scenic Route for diversity. Sure, it takes in Queenstown, Milford Sound and other landmark attractions on its wiggly ‘U’ through the deep south, but it also travels to quieter corners, with hidden gems just as likely to wow you. The Southern Scenic Route website paints a comprehensive picture, but read on for a hit-list of our favourite stops (often involving home-baking). Highlights of the trip Queenstown Te Anau Milford & Doubtful Sounds Bluff Day 1 Queenstown Frequently lauded as one of the world’s best mountain resorts, Queenstown lives up to the hype with a buzzy centre and beautiful lakeside setting. It also offers a bamboozling array of activities within easy reach including hiking and cycling trails, golf courses, wineries, and iconic must-do’s such as the TSS Earnslaw lake cruise and Skyline Gondola. It’s also campervan heaven, with plenty of holiday parks and reserves near the town centre. Day 2 Queenstown to Te Anau SH6 skirts Lake Wakatipu and meets SH94 to Te Anau. Sitting prettily beside the South Island’s largest lake and boasting seasoned visitor facilities including three top-notch holiday parks, Te Anau is a great base for Fiordland adventures such as world-famous Great Walks and Milford Sound. Attractions close to town include the other-worldly Glowworm Caves, and the conservation-focused Wildlife Centre, accessible by foot or hire-bike along the view-filled Lakeside Track. Reward yourself with a Miles Better Pie. Yum. SIDE TRIP - Milford Sound Pies aside, we’ll eat our hats if you’re not totally wowed by this spectacular drive through the beautiful Eglinton Valley (campsites, sandflies) and rocky narrows around Homer Tunnel. -

Safe Passage for Visitors

SAFE PASSAGE FOR VISITORS Neil Bennett Road Asset Manager, Fulton Hogan Christchurch, New Zealand Abstract Tourism is vitally important to New Zealand’s economy and in the year ended March 2014 over 2.7M visitors arrived in our country. Increasing numbers of tourists are electing to have “self-drive” holidays. In Southland there is a popular tourist route known as the Southern Scenic route, that has an unsealed loop off the sealed road that accesses the popular tourist attractions of Curio Bay and Slope Point (the southernmost point in New Zealand). This paper explains the novel use of a cell phone application, originally developed in Sweden to survey roughness, to accurately monitor driver performance, identify out of context curves particularly from the perspective of a driver who has never seen the road before and often never driven on unsealed roads. The tourists are followed by a survey vehicle through the unsealed road section, photographed every second while driving and the phone data is analysed to enable monitoring of road condition trends at different times of the year. A seal extension would reduce the problem but as a standalone project this has been unable to gain NZ Transport Agency subsidy and so was unaffordable for Council at this time. Unsealed road maintenance strategies are therefore necessary to ensure the safety of our visitors. Key Words Unsealed, Tourist, Gravel, Accident, Crash, Overseas, Self-drive Introduction centres on seeing as much of that landscape as possible in the time available. In most cases In mid-2013 Southland District Council came tourists pre-plan a geographical outline of their under significant pressure from locals about trip, including if they want to see both islands, the condition of the unsealed roads in a what the ‘North Island – South Island’ split will popular diversion off the Southern Scenic be, and some specific tourist destinations, Route through the Catlins. -

Sir Edmund Hillary Explorer 26 March - 7 April 2022 13 Days- Ex Wellington

DISCOVER NZ Sir Edmund Hillary Explorer 26 March - 7 April 2022 13 days- Ex Wellington TOUR OVERVIEW Sir Edmund Hillary epitomised the New Zealand spirit of adventure and he is the inspiration for this unique tour. Learn more about his achievements and humanitarian efforts as you explore the South Island and experience the postcard perfect vistas and dramatic alpine scenery that this part of the world is renowned for. You will travel through Marlborough, where Sir Edmund was trained for the air force during the Second World War and where he made some daring ascents of Mt Tapuae-o-Uenuku. In Christchurch, learn more about his team’s expedition crossing Antarctica using converted farm tractors at the International Antarctic Centre. A special dinner is hosted by Sir Edmund’s son, Peter Hillary - also a keen mountaineer and adventurer - and find out about how he continues to keep his father’s memory alive. At Aoraki/Mt Cook, a visit to the museum dedicated to Sir Edmund’s adventurous spirit and his achievements is a must. On this 13-day journey you will spend the first week travelling the entire length of the South Island by heritage rail, in the comfort of vintage carriages, staying in Marlborough, Kaikoura, Christchurch, Aoraki/Mount Cook (detour inland by luxury coach) & Dunedin. From Marlborough to Kaikoura, you will be hauled under a full head of steam by the historic WW1 memorial steam locomotive Ab608 Passchendaele, named in honour of our fallen soldiers at The Battle of Passchendaele in 1917. South of Kaikoura, your rail journey continues with two magnificent heritage 1950’s DA locomotives in an impressive & powerful double-header formation. -

2013–2014 Annual Report

OTAGO MUSEUM ANNUAL REPORT 2013–2014 TABLE OF CONTENTS Introduction 3 Chairperson’s Foreword 4 Director’s Review of the Year 5 Otago Museum Trust Board 6 Māori Advisory Committee 7 Honorary Curators 7 Association of Friends of the Otago Museum 7 Acknowledgements 8 Otago Museum Staff 9 Goal One – A World-class Collection 12 Goal Two – Engaging Our Community 17 Goal Three – Business Sustainability 21 Goal Four – An Outward-looking and Inclusive Culture 24 Visitor Comments 27 Looking Forward 28 Statement of Service Performance 29 Financial Statements 53 2 INTRODUCTION Leadership at the Otago Museum Each new director builds on the wider community, taking into account is generational, with each Museum legacy of those that have come the many varied functions of the director’s tenure being an average of before. Dr Ian Griffin, trained as a Museum and its obligations to service 18 years. This length of service scientist and physicist, has a passion its stakeholders and communities. invariably defines the culture and for science communication and organisational structure of the informal learning engagement. A strategy planning workshop held institution. Previous directors have He brings a new approach to, and in November 2013 was attended by placed emphasis on building and awareness of, the potential and many sectors of the Museum’s wider inspiring research into the collection, importance of the Museum, not only community, from Museum staff and communicating our region’s history as a visitor attraction but as a centre the Otago Museum Trust Board, to and inspiring our community. for learning. educators and academics, to City, District and Regional Councillors, For the past 20 years, the focus has Our aim is to develop a fit for purpose Kāi Tahu representatives, business been on building the Museum into a repository for the Museum’s collection, operators and community workers major visitor attraction and a strategy address the need to research history in the Otago region. -

H.D. Skinner's Use of Associates Within the Colonial

Tuhinga 26: 20–30 Copyright © Museum of New Zealand Te Papa Tongarewa (2015) H.D.Skinner’s use of associates within the colonial administrative structure of the Cook Islands in the development of Otago Museum’s Cook Islands collections Ian Wards National Military Heritage Charitable Trust, PO Box 6512, Marion Square, Wellington, New Zealand ([email protected]) ABSTRACT: During his tenure at Otago Museum (1919–57), H.D.Skinner assembled the largest Cook Islands collection of any museum in New Zealand. This paper shows that New Zealand’s colonial administrative structure was pivotal in the development of these collections, but that they were also the result of complex human interactions, motivations and emotions. Through an analysis of Skinner’s written correspondence, examples are discussed that show his ability to establish relationships where objects were donated as expressions of personal friendship to Otago Museum. The structure of the resulting collection is also examined. This draws out Skinner’s personal interest in typological study of adzes and objects made of stone and bone, but also highlights the increasing scarcity of traditional material culture in the Cook Islands by the mid-twentieth century, due in part to the activities of other collectors and museums. KEYWORDS: H.D.Skinner, Otago Museum, Cook Islands, colonialism, material culture. Introduction individuals, exchanges with museums, private donations and, significantly, the purchase by the New Zealand government During his tenure as ethnologist (1919–57) and, later, of the Oldman collection in 1948, Otago Museum’s Cook director of Otago Museum, Henry Devenish Skinner Islands collection grew to be the largest in New Zealand. -

Points Statement

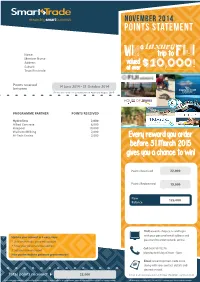

STstatement.pdf 7 10/11/14 2:27 pm NOVEMBER 2014 POINTS STATEMENT a luxury Name win trip to Fiji Member Name Address valued $10 000 Suburb at over , ! Town/Postcode Points received 14 June 2014 - 31 October 2014 between (Points allocated for spend between April and August 2014) FIJI’S CRUISE LINE PROGRAMME PARTNER POINTS RECEIVED Hydroflow 2,000 Allied Concrete 6,000 Hirepool 10,000 Waikato Milking 2,000 Hi-Tech Enviro 2,000 Every reward you order before 31 March 2015 gives you a chance to win! Points Received 22,000 Points Redeemed 15,000 New 125,000 Balance Visit rewards-shop.co.nz and login with your personal email address and Update your account in 3 easy steps: password to order rewards online. 1. Visit smart-trade .co.nz/my-account 2. Enter your personal email address Call 0800 99 76278 3. Set your new password Monday to Friday 8:30am - 5pm. Now you’re ready to get more great rewards! Email [email protected] along with your contact details and desired reward. * Total points received 22,000 Smart Trade International Ltd, PO Box 370, WMC, Hamilton 3240 *If your total points received does not add up, it may be a result of a reward cash top up, points transfer or manual points issue. Please call us if you have any queries. All information is correct as at 31 October 2014. Conditions apply. Go online for more details. GIVE YOUR POINTS A BOOST! Over 300 businesses offering Smart-Trade reward points. To earn points from any of the companies listed below, contact the business, express your desire to earn points and discuss opening an account. -

2014–2015 Annual Report

OTAGO MUSEUM ANNUAL REPORT 2014–2015 TABLE OF CONTENTS Chairperson’s Foreword 3 Director’s Review of the Year 3 Otago Museum Trust Board 4 Māori Advisory Committee 5 Honorary Curators 5 Association of Friends of the Otago Museum 5 Acknowledgements 6 Otago Museum Staff 7 Goal One: A World-class Collection 10 Goal Two: Engaging Our Community 15 Goal Three: Business Sustainability 21 Goal Four: An Outward-looking and Inclusive Culture 23 Giving Back 25 Appendix A: Statement of Service Performance 26 Appendix B: Financial Statements 57 Appendix C: Independent Auditor’s Report 92 2 CHAIRPERSON’S FOREWORD OTAGO MUSEUM TRUST BOARD completed reorganisations within our teams December 2015 is very exciting. It marks to reflect our key areas of focus. We have the start of a major advance in our ability continued to invest in highly-skilled staff to to connect with our communities. This empower these areas. Our financial results development comes on the back of several reflect a successful balance of investment very successful exhibitions staged this year. and sensible management, allowing The great thing about these exhibitions has investment in our key development areas. been the use of our own collection and the leadership and creativity shown by our staff As an institution, we have worked hard at in bringing them to life. building partnership relationships with a large number of organisations. This report I would like to reflect my thanks for the work It is my pleasure as Chairperson to report demonstrates the success of these efforts of the management team and all staff at on behalf of the Board on another very and positions the Museum strongly for future the Otago Museum. -

Invercargill the Catlins Itinerary

Welcome to SOUTHLAND Invercargill & The Catlins 4 days, 3 nights #MySouthland Welcome to Invercargill Day 1 Time Activity Notes Breakfast Breakfast in Dunedin 0800 Drive Dunedin to Invercargill Following SH1 1030 Arrive in Invercargill 1035 Visit Bill Richardson Transport The largest private collection of its World type in the World, Bill Richardson Transport World has literally hundreds of vehicles and petrol pumps on display throughout 15,000sqm there is a lot to take in. 491 Tay St, Hawthorndale Invercargill 9810, New Zealand 1235 Suggested lunch: The Grille Cafe Located at Bill Richardson Transport World, The Grille Cafe serves delicious food and is a big part of the experiences at Transport World. Their flavours strive to include the very best of New Zealand and Southland cuisine. 1330 Drive to Riverton the ‘Riviera Follow the Southern Scenic Route of the South’ to the popular seaside village of Riverton, which is rich in Maori history and is one of the earliest European settlements in New Zealand. Visit the Te Hikoi Southern Journey Heritage Museum and take a photo with the infamous paua shell on the main road. 1400 Arrive in Riverton Suggested places to visit Colac Bay For surfers, food lovers, history buffs or those simply contemplating the power of the great Southern Ocean, Colac Bay and its surrounds offer a great place to slow down and take a break. Riverton Local Organic The Riverton Organic Food Coop is a nonprofit group run by volunteers enabling people to buy organic food at cost price and in doing so supporting natural and sustainable practices Visit Te Hikoi Southern Journey Take an interactive journey Heritage Museum through 'Te Hikoi', featuring authentic displays, adventurous characters and engaging stories.