Taipei Exchange Principles for Financial Market Infrastructure Disclosure Report (TR)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Incoming Letter: Taipei Exchange Main Board and Taipei Exchange

New York Paris Northern California Madrid Washington DC Tokyo São Paulo Beijing London Hong Kong James C. Lin Partner Resident Hong Kong Partners Davis Polk & Wardwell 852 2533 3368 tel William F. Barron* Gerhard Radtke* Hong Kong Solicitors 852 2533 1768 fax Bonnie Chan* Martin Rogers † The Hong Kong Club Building [email protected] Karen Chan † Patrick S. Sinclair* 3A Chater Road Paul K. Y. Chow* † Miranda So* Hong Kong James C. Lin* James Wadham † Hong Kong Solicitors * Also Admitted in New York † Also Admitted in England and Wales August 29, 2019 Re: Application for Designation of the Taipei Exchange Main Board and Taipei Exchange Bond Market as a “Designated Offshore Securities Market” Michael Coco, Chief Office of International Corporate Finance Division of Corporation Finance United States Securities and Exchange Commission 450 Fifth Street. N.W. Washington, DC 20549 Dear Mr. Coco: We are writing to the United States Securities and Exchange Commission (the “SEC” or the “Commission”) on behalf of the Taipei Exchange (the “TPEx”) to apply for the classification of a “designated offshore securities market” for purposes of Regulation S (“Regulation S”) under the U.S. Securities Act of 1933, as amended, for (i) the portion of the TPEx known as the Taipei Exchange Main Board (the “TPEx Main Board”) and (ii) the portion of the TPEx known as the Taipei Exchange Bond Market (the “TPEx Bond Market” and together with the TPEx Main Board, the “TPEx Platforms”). Designation is being sought in order to assist market participants to the TPEx Platforms who are eligible for the safe harbor provision provided by Rule 904 of Regulation S to satisfy the requirements specified in that rule when reselling securities “in, on or through the facilities of” the TPEx Platforms. -

IOSCO Members Ordinary Members (129)

IOSCO Members Ordinary Members (129) AGENCY COUNTRY Albanian Financial Supervisory Authority ALBANIA Alberta Securities Commission ALBERTA, CANADA Commission d’Organisation et de Surveillance des Opérations de Bourse ALGERIA Autoritat Financera Andorrana ANDORRA, PRINCIPALITY OF Comissão do Mercado de Capitais ANGOLA Comisión Nacional de Valores* ARGENTINA Central Bank of Armenia ARMENIA Australian Securities and Investments Commission* AUSTRALIA Financial Market Authority AUSTRIA Securities Commission of The Bahamas* BAHAMAS, THE Central Bank of Bahrain BAHRAIN, KINGDOM OF Bangladesh Securities and Exchange Commission BANGLADESH Financial Services Commission BARBADOS Financial Services and Markets Authority* BELGIUM Bermuda Monetary Authority BERMUDA Autoridad de Supervisión del Sistema Financiero BOLIVIA Securities Commission of the Federation of Bosnia and Herzegovina BOSNIA AND HERZEGOVINA, FEDERATION OF Comissão de Valores Mobiliários* BRAZIL British Columbia Securities Commission CANADA British Virgin Islands Financial Services Commission BRITISH VIRGIN ISLANDS Autoriti Monetari Brunei Darussalam BRUNEI Financial Supervision Commission BULGARIA Auditoria Geral do Mercado de Valores Mobiliários, Banco Central of Cabo Verde CABO VERDE Cayman Islands Monetary Authority CAYMAN ISLANDS Commission de Surveillance du Marché Financier de l’Afrique Centrale CENTRAL AFRICA Comisión para el Mercado Financiero (Financial Market Commission) CHILE China Securities Regulatory Commission* CHINA Financial Supervisory Commission CHINESE TAIPEI Superintendencia -

Enhancing Liquidity in Emerging Market Exchanges

ENHANCING LIQUIDITY IN EMERGING MARKET EXCHANGES ENHANCING LIQUIDITY IN EMERGING MARKET EXCHANGES OLIVER WYMAN | WORLD FEDERATION OF EXCHANGES 1 CONTENTS 1 2 THE IMPORTANCE OF EXECUTIVE SUMMARY GROWING LIQUIDITY page 2 page 5 3 PROMOTING THE DEVELOPMENT OF A DIVERSE INVESTOR BASE page 10 AUTHORS Daniela Peterhoff, Partner Siobhan Cleary Head of Market Infrastructure Practice Head of Research & Public Policy [email protected] [email protected] Paul Calvey, Partner Stefano Alderighi Market Infrastructure Practice Senior Economist-Researcher [email protected] [email protected] Quinton Goddard, Principal Market Infrastructure Practice [email protected] 4 5 INCREASING THE INVESTING IN THE POOL OF SECURITIES CREATION OF AN AND ASSOCIATED ENABLING MARKET FINANCIAL PRODUCTS ENVIRONMENT page 18 page 28 6 SUMMARY page 36 1 EXECUTIVE SUMMARY Trading venue liquidity is the fundamental enabler of the rapid and fair exchange of securities and derivatives contracts between capital market participants. Liquidity enables investors and issuers to meet their requirements in capital markets, be it an investment, financing, or hedging, as well as reducing investment costs and the cost of capital. Through this, liquidity has a lasting and positive impact on economies. While liquidity across many products remains high in developed markets, many emerging markets suffer from significantly low levels of trading venue liquidity, effectively placing a constraint on economic and market development. We believe that exchanges, regulators, and capital market participants can take action to grow liquidity, improve the efficiency of trading, and better service issuers and investors in their markets. The indirect benefits to emerging market economies could be significant. -

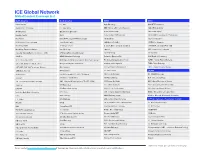

ICE Global Network Global Content Coverage List

ICE Global Network Global Content Coverage List North America North America EMEA APAC Activ Financial ICE TMC Aquis Exchange ASX (NTP Derivatives) Aequitas NEO Exchange ICE Swap Trade BME - Bolsas y Mercados Españoles CXA (CHI-X Australia) ATG Americas IEX (Investors Exchange) Borsa Italiana Group CXJ (CHI-X Japan) Barclays Capital IIROC Börse Stuttgart (SID platform) HKEX (OMD C Securities & D Derivatives) BGC Fenics Itiviti (NYFIX, ULLink PTRMS (Canada)) CBOE Europe ICE Clear Singapore BOX (Boston Stock Exchange) Jane Street Capital CME (BrokerTech EU) ICE Futures Singapore Broadridge (ADP) JP Morgan Chase Deutsche Börse Group (Xetra, Eurex) JPX (TSE Flex Standard/Full, OSE) Broadridge Financial Solutions Lime Brokerage Equiduct KRX - Korea Stock Exchange Canadian Imperial Bank of Commerce - CIBC LTSE (Long Term Stock Exchange) Euronext Group SBI Japanext CBOE US MEMX (Members Exchange) Fastmatch (Euronext FX) SGX (Equities, Derivatives) CBOE FX (Hotspot NY4) MIAX Options, MIAX Pearl Options, Miax Pearl Equities FIS Global (Sungard London-Paris) TAIFEX – Taiwan Futures Exchange CME (CME, NYMEX, COMEX, CBOT) Morgan Stanley Unicast Services Goldman Sachs Sigma-X TPEX – Taipei Exchange CME (BME, DME, MGEX, Indexes, Bitcoin) MSCI Indexes ICE Benchmark Administration TWSE - Taiwan Stock Exchange CME (BrokerTec US) MT Newswires ICE Clear Europe LATAM Credit Suisse NASDAQ Canada (CXC, CX2, CXD, Basic) ICE Clear Netherlands B3 - BM&F & Bovespa Creditex NASDAQ US (All Markets) ICE Futures Europe BCS - Bolsa de Santiago CSE - Canadian Securities -

Doing Data Differently

General Company Overview Doing data differently V.14.9. Company Overview Helping the global financial community make informed decisions through the provision of fast, accurate, timely and affordable reference data services With more than 20 years of experience, we offer comprehensive and complete securities reference and pricing data for equities, fixed income and derivative instruments around the globe. Our customers can rely on our successful track record to efficiently deliver high quality data sets including: § Worldwide Corporate Actions § Worldwide Fixed Income § Security Reference File § Worldwide End-of-Day Prices Exchange Data International has recently expanded its data coverage to include economic data. Currently it has three products: § African Economic Data www.africadata.com § Economic Indicator Service (EIS) § Global Economic Data Our professional sales, support and data/research teams deliver the lowest cost of ownership whilst at the same time being the most responsive to client requests. As a result of our on-going commitment to providing cost effective and innovative data solutions, whilst at the same time ensuring the highest standards, we have been awarded the internationally recognized symbol of quality ISO 9001. Headquartered in United Kingdom, we have staff in Canada, India, Morocco, South Africa and United States. www.exchange-data.com 2 Company Overview Contents Reference Data ............................................................................................................................................ -

Over 100 Exchanges Worldwide 'Ring the Bell for Gender Equality in 2021' with Women in Etfs and Five Partner Organizations

OVER 100 EXCHANGES WORLDWIDE 'RING THE BELL FOR GENDER EQUALITY IN 2021’ WITH WOMEN IN ETFS AND FIVE PARTNER ORGANIZATIONS Wednesday March 3, 2021, London – For the seventh consecutive year, a global collaboration across over 100 exchanges around the world plan to hold a bell ringing event to celebrate International Women’s Day 2021 (8 March 2020). The events - which start on Monday 1 March, and will last for two weeks - are a partnership between IFC, Sustainable Stock Exchanges (SSE) Initiative, UN Global Compact, UN Women, the World Federation of Exchanges and Women in ETFs, The UN Women’s theme for International Women’s Day 2021 - “Women in leadership: Achieving an equal future in a COVID-19 world ” celebrates the tremendous efforts by women and girls around the world in shaping a more equal future and recovery from the COVID-19 pandemic. Women leaders and women’s organizations have demonstrated their skills, knowledge and networks to effectively lead in COVID-19 response and recovery efforts. Today there is more recognition than ever before that women bring different experiences, perspectives and skills to the table, and make irreplaceable contributions to decisions, policies and laws that work better for all. Women in ETFs leadership globally are united in the view that “There is a natural synergy for Women in ETFs to celebrate International Women’s Day with bell ringings. Gender equality is central to driving the global economy and the private sector has an important role to play. Our mission is to create opportunities for professional development and advancement of women by expanding connections among women and men in the financial industry.” The list of exchanges and organisations that have registered to hold an in person or virtual bell ringing event are shown on the following pages. -

Index Methodology Guide for the Factset Global E-Business Indextm

Index Methodology Guide for the FactSet Global e-Business IndexTM Version 1.2 – August 17, 2020 Copyright © 2019 FactSet Research Systems Inc. All rights reserved Table of Contents Index Methodology Guide for the FactSet Global e-Business IndexTM ......................................................... 1 Table of Contents .......................................................................................................................................... 2 Index Introduction and Objective ................................................................................................................. 3 Index Construction ........................................................................................................................................ 4 Index Maintenance ..................................................................................................................................... 10 Index Calculation and Data Correction ....................................................................................................... 11 Additional Information................................................................................................................................ 12 Copyright © 2019 FactSet Research Systems Inc. All rights reserved Index Introduction and Objective 1.1 Index Overview The FactSet Global e-Business Index is an equity benchmark designed to track the performance of companies engaged in electronic business activities. By using the Internet and other cloud and software technologies, -

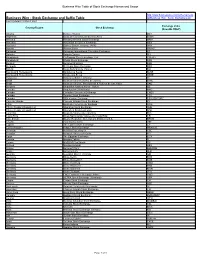

Stock Exchange and Suffix Table Ml/Business Wire Stock Exchanges.Pdf Last Updated 12 March 2021

Business Wire Table of Stock Exchange Names and Usage http://www.businesswire.com/schema/news Business Wire - Stock Exchange and Suffix Table ml/Business_Wire_Stock_Exchanges.pdf Last Updated 12 March 2021 Exchange Value Country/Region Stock Exchange (NewsML ONLY) Albania Bursa e Tiranës BET Argentina Bolsa de Comercio de Buenos Aires BCBA Armenia Nasdaq Armenia Stock Exchange ARM Australia Australian Securities Exchange ASX Australia Sydney Stock Exchange (APX) APX Austria Wiener Börse WBAG Bahamas Bahamas International Securities Exchange BS Bahrain Bahrain Bourse BH Bangladesh Chittagong Stock Exchange, Ltd. CSEBD Bangladesh Dhaka Stock Exchange DSE Belgium Euronext Brussels BSE Bermuda Bermuda Stock Exchange BSX Bolivia Bolsa Boliviana de Valores BO Bosnia and Herzegovina Banjalucka Berza BLSE Bosnia and Herzegovina Sarajevska Berza SASE Botswana Botswana Stock Exchange BT Brazil Bolsa de Valores do Rio de Janeiro BVRJ Brazil Bolsa de Valores, Mercadorias & Futuros de Sao Paulo SAO Bulgaria Balgarska fondova borsa - Sofiya BB Canada Aequitas NEO Exchange NEO Canada Canadian Securities Exchange CNSX Canada Toronto Stock Exchange TSX Canada TSX Venture Exchange TSX VENTURE Cayman Islands Cayman Islands Stock Exchange KY Chile Bolsa de Comercio de Santiago SGO China, People's Republic of Shanghai Stock Exchange SHH China, People's Republic of Shenzhen Stock Exchange SHZ Colombia Bolsa de Valores de Colombia BVC Costa Rica Bolsa Nacional de Valores de Costa Rica CR Cote d'Ivoire Bourse Regionale Des Valeurs Mobilieres S.A. BRVM Croatia -

Northern Trust Emea Order Execution Policy

NORTHERN TRUST EMEA ORDER EXECUTION POLICY For Professional Clients of the following Northern Trust entities: • Northern Trust Global Services SE, and its branches • Northern Trust Securities LLP, and its branches • The Northern Trust Company, London branch Publication date: 1 January 2021 Contents INTRODUCTION .................................................................................................................................................................... 3 A. Purpose of this policy .................................................................................................................................................................................... 3 B. What is Best Execution? ............................................................................................................................................................................... 3 POLICY SCOPE ..................................................................................................................................................................... 4 A. Northern Trust entities subject to this Policy ................................................................................................................................................. 4 B. Types of Clients ............................................................................................................................................................................................. 4 C. Activities ....................................................................................................................................................................................................... -

List of Asian Stock Exchanges

List of Asian stock exchanges This is a list of Asian stock exchanges. In the Asian region, there are multiple stock exchanges. As per data from World Federation of Exchanges, below are top 10 selected in 2019:[1][2] Tokyo Stock Exchange, Japan Shanghai Stock Exchange, China Hong Kong Stock Exchange, Hong Kong Shenzhen Stock Exchange, China Bombay Stock Exchange, India National Stock Exchange, India Korea Exchange, South Korea Taiwan Exchange, Taiwan Singapore Exchange, Singapore The Stock Exchange of Thailand, Thailand Asia Contents Stock exchanges Central Asian East Asian North Asia South Asian Southeast Asian West Asian See also References External links Stock exchanges Central Asian Operating Economy Exchange Location Founded Listings Link Technology MIC KASE (http Kazakhstan Stock Almaty 1993 127 s://kase.k Exchange z/en/) Kazakhstan Astana AIX (http Nasdaq Nur- International 2018 25 s://www.ai Matching AIXK Sultan Exchange x.kz/) Engine[3] KSE (htt Kyrgyz Stock Bishkek 1994 p://www.ks Kyrgyzstan Exchange (KSE) e.kg/) CASE (http Central Asian s://www.ca Dushanbe 2015 Tajikistan Stock Exchange se.com.tj/e n/) SRCMET State Commodity (https://ww and Raw Material Ashgabat 1994 w.exchang Exchange of Turkmenistan e.gov.tm/?l Turkmenistan ang=en) UZSE (http Tashkent Stock Tashkent 1994 104 s://uzse.u Uzbekistan Exchange z/) East Asian Economy Exchange Location Founded Listings Link Shanghai Stock SSE (http://www.sse.com. Shanghai 1990 Exchange cn) Shenzhen Stock SZSE (http://www.szse.cn/ Shenzhen 1991 2,375 (Jan 2021) Mainland Exchange main/) China Dalian Commodity DCE (http://www.dce.com. Dalian 1993 Exchange cn/DCE/) SEHK (https://web.archive. -

IOSCO Members Ordinary Members (126)

IOSCO Members Ordinary Members (126) AGENCY COUNTRY Albanian Financial Supervisory Authority ALBANIA Alberta Securities Commission CANADA Commission d’Organisation et de Surveillance des Opérations de Bourse ALGERIA Institut Nacional Andorra de Finances ANDORRA, PRINCIPALITY OF Comisión Nacional de Valores* ARGENTINA Central Bank of Armenia ARMENIA Australian Securities and Investments Commission* AUSTRALIA Financial Market Authority AUSTRIA Securities Commission of The Bahamas BAHAMAS, THE Central Bank of Bahrain BAHRAIN, KINGDOM OF Bangladesh Securities and Exchange Commission BANGLADESH Financial Services Commission BARBADOS Financial Services and Markets Authority* BELGIUM Bermuda Monetary Authority BERMUDA Autoridad de Supervisión del Sistema Financiero BOLIVIA Securities Commission of the Federation of Bosnia and Herzegovina BOSNIA AND HERZEGOVINA, FEDERATION OF Comissão de Valores Mobiliários* BRAZIL British Columbia Securities Commission CANADA British Virgin Islands Financial Services Commission BRITISH VIRGIN ISLANDS Autoriti Monetari Brunei Darussalam BRUNEI Financial Supervision Commission BULGARIA Cayman Islands Monetary Authority CAYMAN ISLANDS Commission de Surveillance du Marché Financier de l’Afrique Centrale CENTRAL AFRICA Superintendencia de Valores y Seguros CHILE China Securities Regulatory Commission* CHINA Financial Supervisory Commission CHINESE TAIPEI Superintendencia Financiera de Colombia COLOMBIA Superintendencia General de Valores COSTA RICA Croatian Financial Services Supervisory Agency CROATIA Cyprus Securities -

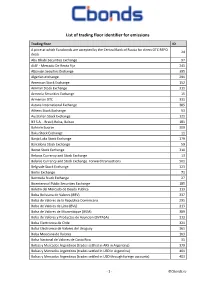

List of Trading Floor Identifier for Emissions

List of trading floor identifier for emissions Trading floor ID A price at which Eurobonds are accepted by the Central Bank of Russia for direct OTC REPO 24 deals Abu Dhabi Securities Exchange 97 AIAF - Mercado De Renta Fija 241 Albanian Secuities Exchange 395 Algerian exchange 291 American Stock Exchange 152 Amman Stock Exchange 311 Armenia Securities Exchange 15 Armenian OTC 331 Astana International Exchange 385 Athens Stock Exchange 53 Australian Stock Exchange 121 B3 S.A. - Brasil, Bolsa, Balcao 181 Bahrain Bourse 309 Baku Stock Exchange 11 Banja Luka Stock Exchange 179 Barcelona Stock Exchange 59 Beirut Stock Exchange 310 Belarus Currency and Stock Exchange 13 Belarus Currency and Stock Exchange. Forward transactions 501 Belgrade Stock Exchange 123 Berlin Exchange 71 Bermuda Stock Exchange 27 Bicentennial Public Securities Exchange 185 Boletin del Mercado de Deuda Publica 113 Bolsa Boliviana de Valores (BBV) 337 Bolsa de Valores de la Republica Dominicana 295 Bolsa de Valores de Lima (BVL) 213 Bolsa de Valores de Mozambique (BVM) 389 Bolsa de Valores y Productos de Asuncion (BVPASA) 313 Bolsa Electronica de Chile 321 Bolsa Electronica de Valores del Uruguay 361 Bolsa Mexicana de Valores 103 Bolsa Nacional de Valores de Costa Rica 31 Bolsas y Mercados Argentinos (trades settled in ARS in Argentina) 379 Bolsas y Mercados Argentinos (trades settled in USD in Argentina) 401 Bolsas y Mercados Argentinos (trades settled in USD through foreign accounts) 403 - 1 - ©Cbonds.ru Trading floor ID BondSpot 69 Borsa Istanbul (International Bonds