Who Shops Downtown, and Why?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

Monroeville Active Transportation Plan DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT Table of Contents CONTENTS Project Team / Acknowledgements

Monroeville Active Transportation Plan Draft DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT ii This plan was prepared by Pashek+MTR, a certifi ed Bike-Friendly Employer since 2012. The fi rm, based on Pittsburgh’s North Side, has two “offi ce bikes” for daily use by the staff . This photo shows employees who rode their bikes on 2019 Bike To Work Day. Monroeville Active Transportation Plan DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT DRAFT Table of Contents CONTENTS Project Team / Acknowledgements ............................................................v Report Summary ..................................................RS-1 Introduction ............................................................1 Our Chosen Path Forward ...........................................................................1 A Glance Backward ......................................................................................2 Challenges to Walking and Biking ...............................................................3 What’s in the Plan ........................................................................................4 What’s Ahead ...............................................................................................6 Mapping Monroeville ...................................................................................7 Pedestrian & Cyclist Connections Analysis .................................................24 Safe Routes to Schools Analysis ..................................................................25 Existing Plans, -

Miller Promo Flyer

2016/2017 Gift & Craft Expo show dates & locations 2016/2017 Gift & Craft Expo show dates & locations 2016/2017 Gift & Craft Expo show dates & locations March 16-20 - Johnstown Galleria, Johnstown, Pa. March 16-20 - Johnstown Galleria, Johnstown, Pa. March 16-20 - Johnstown Galleria, Johnstown, Pa. April 6-10 - Shenango Valley Mall, Hermitage, Pa. April 6-10 - Shenango Valley Mall, Hermitage, Pa. April 6-10 - Shenango Valley Mall, Hermitage, Pa. April 13-17 - Monroeville Mall, Monroeville, Pa. April 13-17 - Monroeville Mall, Monroeville, Pa. April 13-17 - Monroeville Mall, Monroeville, Pa. April 22-24 - Washington Crown Center, Washington, Pa. April 22-24 - Washington Crown Center, Washington, Pa. April 22-24 - Washington Crown Center, Washington, Pa. April 29-May 1 - Pittsburgh Mills, Tarentum, Pa. April 29-May 1 - Pittsburgh Mills, Tarentum, Pa. April 29-May 1 - Pittsburgh Mills, Tarentum, Pa. May 6-7,- 7th annual Pamperfest - Airport Embassy Suites, May 6-7,- 7th annual Pamperfest - Airport Embassy Suites, May 6-7,- 7th annual Pamperfest - Airport Embassy Suites, Robinson, Pa. www.Pamperfest.com Robinson, Pa. www.Pamperfest.com Robinson, Pa. www.Pamperfest.com May 4-8 - Johnstown Galleria, Johnstown, Pa. May 4-8 - Johnstown Galleria, Johnstown, Pa. May 4-8 - Johnstown Galleria, Johnstown, Pa. June 1-5 - Westmoreland Mall, Greensburg, Pa. June 1-5 - Westmoreland Mall, Greensburg, Pa. June 1-5 - Westmoreland Mall, Greensburg, Pa. Aug. 13- Summer Daze Festival, Castle Shannon, Pa. Aug. 13- Summer Daze Festival, Castle Shannon, Pa. Aug. 13- Summer Daze Festival, Castle Shannon, Pa. Sept. 9-11 - Pittsburgh Mills, Tarentum, PA Sept. 9-11 - Pittsburgh Mills, Tarentum, PA Sept. -

Property Alert!

Property Alert! Innovative Solutions for the Retail Industry For more information, Spence J. Mehl Or visit please contact: T: 212.300.5375 www.rcsrealestate.com E: [email protected] Bankruptcy Sale of Leases (Subject to Bankruptcy Court approval) # Property Address City State Sq. Ft # Property Address City State Sq. Ft 233 Colonial Mall Gadsden Gadsden AL 3,165 1138 Savannah Outlets Pooler GA 3,500 577 Parkway Place Huntsville AL 3,545 926 Ave Webb Gin Snellville GA 3,467 444 Central Mall Fort Smith AR 2,920 576 Colonial Mall Valdosta Valdosta GA 3,371 828 Turtle Creek Aeropostale Jonesboro AR 3,500 757 Lindale Mall Cedar Rapids IA 3,668 612 Superstition Springs Mesa AZ 3,310 41 River Oaks Center Calumet City IL 2,778 3383 Mariposa PS Nogales AZ 5,047 1071 Outlet Shoppes At Fremont Fremont IN 4,026 1059 Outlets at Anthem Phoenix AZ 4,733 804 Metropolis Mall Plainfield IN 3,300 788 Santa Anita Aeropostale Arcadia CA 3,335 238 Honey Creek Terre Haute IN 3,640 880 Topanga Plaza Canoga Park CA 3,907 558 Towne West Square Wichita KS 3,180 855 Capitola Aeropostale Capitola CA 3,415 334 Ashland Town Center Ashland KY 3,308 1022 The Shoppes At Chino Hill Chino Hills CA 3,859 933 Hamburg Pavilion Lexington KY 4,000 909 Puente Hills Aeropostale Industry CA 3,419 1129 The Outlet Shoppes Of the Blue Simpsonville KY 3,960 Grass 1108 South Bay Galleria Redondo CA 3,601 1109 Riverwalk New Orleans LA 6,000 Beach 1102 Promenade at Temecula Temecula CA 3,433 339 The Mall at Whitney Field Leominster MA 3,548 169 Sangertown Mall New Hartford CT 4,069 -

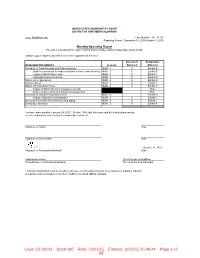

Silicon Valley Bank) 1\ M~Mt>Tr of SVB L'lrw~W Crwp Account Details Requested Date: From: 09/10/2015 To: 10/03/2015 Generated On: 10/15/2015

UNITED STATES BANKRUPTCY COURT DISTRICT OF NORTHERN CALIFORNIA In re: NewZoom, Inc. Case Number: 15 - 31141 Reporting Period: September 10, 2015-October 3, 2015 Monthly Operating Report File with Court and submit copy to United States Trustee within 20 days after end of month Submit copy of report to any official committee appointed in the case. Document Explanation REQUIRED DOCUMENTS Form No. Attached Attached Schedule of Cash Receipts and Disbursements MOR - 1 X Exhibit A Bank Reconciliation (or copies of debtor's bank reconciliation's) MOR - 1 X Exhibit B Copies of Bank Statements MOR - 1 X Exhibit C Cash disbursements journal MOR - 1 X Exhibit D Statement of Operations MOR - 2 X Exhibit E Balance Sheet MOR - 3 X Exhibit F Status of Postpetition Taxes MOR - 4 X Exhibit G Copies of IRS Form 6123 or payment receipt None Copies of tax returns filed during reporting period None Summary of Unpaid Postpetition Debts MOR - 4 Exhibit H Listing of aged accounts payable MOR - 4 X Exhibit I Accounts Receivable Reconciliation and Aging MOR - 5 X Exhibit J Debtor Questionnaire MOR - 5 X Exhibit K I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief. Signature of Debtor Date Signature of Joint Debtor Date October 21, 2015 Signature of Authorized Individual* Date Andrew Hinkelman Chief Restructuring Officer Printed Name of Authorized Individual Title of Authorized Individual * Authorized individual must be an officer, director, or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company. -

Llght Rall Translt Statlon Deslgn Guldellnes

PORT AUTHORITY OF ALLEGHENY COUNTY LIGHT RAIL TRANSIT V.4.0 7/20/18 STATION DESIGN GUIDELINES ACKNOWLEDGEMENTS Port Authority of Allegheny County (PAAC) provides public transportation throughout Pittsburgh and Allegheny County. The Authority’s 2,600 employees operate, maintain, and support bus, light rail, incline, and paratransit services for approximately 200,000 daily riders. Port Authority is currently focused on enacting several improvements to make service more efficient and easier to use. Numerous projects are either underway or in the planning stages, including implementation of smart card technology, real-time vehicle tracking, and on-street bus rapid transit. Port Authority is governed by an 11-member Board of Directors – unpaid volunteers who are appointed by the Allegheny County Executive, leaders from both parties in the Pennsylvania House of Representatives and Senate, and the Governor of Pennsylvania. The Board holds monthly public meetings. Port Authority’s budget is funded by fare and advertising revenue, along with money from county, state, and federal sources. The Authority’s finances and operations are audited on a regular basis, both internally and by external agencies. Port Authority began serving the community in March 1964. The Authority was created in 1959 when the Pennsylvania Legislature authorized the consolidation of 33 private transit carriers, many of which were failing financially. The consolidation included the Pittsburgh Railways Company, along with 32 independent bus and inclined plane companies. By combining fare structures and centralizing operations, Port Authority established the first unified transit system in Allegheny County. Participants Port Authority of Allegheny County would like to thank agency partners for supporting the Light Rail Transportation Station Guidelines, as well as those who participated by dedicating their time and expertise. -

Allderdice 2409 Shady Avenue Pittsburgh, PA 15217 412-422-4851 • Go Through Oakmont And/Or Verona to Washington Boulevard •

Allderdice 2409 Shady Avenue Pittsburgh, PA 15217 412-422-4851 • Go through Oakmont and/or Verona to Washington Boulevard • Right turn onto Washington Boulevard • Follow onto 5 th Avenue at Penn Avenue • Left onto Shady Avenue at Pittsburgh Center for the ARTS • Turn left onto Forward Avenue • Turn left onto Beechwood Avenue • Turn right onto English Lane • Follow to parking lot – field at top of stairs Apollo-Ridge 1825 State Route 56 Spring Church, PA 15685 724-478-6000 – 724-478-9775 (Fax) From Route 28: • Get of 366 Tarentum Bridge • Cross the bridge following 366 • Take Route 56 East towards Leechburg • Follow Route 56 East through Vandergrift • Cross Vandergrift Bridge, follow Route 56 East into Apollo (after crossing the bridge, turn right) • Turn left at light in Apollo, football stadium is ½ mile on the left Aquinas Academy 2308 West Hardies Road Gibsonia, PA 15044 724-444-0722 Aquinas Academy (Dolan Field) From Turnpike Exit 39: • Exit I-76, Pennsylvania Turnpike via ramp at Exit 30 PA 8 to Pittsburgh/Butler • Keep right at the fork in the ramp • Bear right on PA-8, William Flynn Hwy and go north for 500 feet staying in the left lane (there will be alight and a BP station on your left) • Turn left at the light onto West Hardies Road and go west for 2.0 miles (the school will be on your left just past St. Catherine of Sweden Church • The field is behind the school Avonworth 304 Josephs Lane Pittsburgh, PA 15237 412-847-0942 / 412-366-7603 (Fax) High School Gym – Girls’ JV & Varsity Volleyball Middle School Gym – 7/8th Grade Girls’ Basketball Lenzner Field – Varsity, JV, 7/8 th Football; Varsity, JV Girls’ & Boys’ Soccer High School Field (behind building) – 7/8 Soccer, Boys & Girls Ohio Township Community Park – Varsity Cross Country High School Gym, Middle School Gym, Lenzner Field and High School Field From the North: Take 79 South to 279S exiting at the Camp Horne Road Exit. -

Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20

Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 1 of 54 Fill in this information to identify the case: United States Bankruptcy Court for the Southern District of Texas Case number (if known): Chapter 11 Check if this is an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 04/20 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor’s name and the case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor’s name Laredo Outlet Shoppes, LLC 2. All other names debtor used N/A in the last 8 years Include any assumed names, trade names, and doing business as names 3. Debtor’s federal Employer Identification Number (EIN) 81-1563566 4. Debtor’s address Principal place of business Mailing address, if different from principal place of business 2030 Hamilton Place Blvd. Number Street Number Street CBL Center, Suite 500 P.O. Box Chattanooga Tennessee 37421 City State ZIP Code City State ZIP Code Location of principal assets, if different from principal place of business Hamilton County County 1600 Water Street Number Street Laredo Texas 78040 City State ZIP Code 5. Debtor’s website (URL) www.cblproperties.com 6. Type of debtor ☒ Corporation (including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) ☐ Partnership (excluding LLP) ☐ Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy Page 1 WEIL:\97969900\8\32626.0004 Case 21-31717 Document 1 Filed in TXSB on 05/26/21 Page 2 of 54 Debtor Laredo Outlet Shoppes, LLC Case number (if known) 21-_____ ( ) Name A. -

State City Shopping Center Address

State City Shopping Center Address AK ANCHORAGE 5TH AVENUE MALL SUR 406 W 5TH AVE AL FULTONDALE PROMENADE FULTONDALE 3363 LOWERY PKWY AL HOOVER RIVERCHASE GALLERIA 2300 RIVERCHASE GALLERIA AL MOBILE BEL AIR MALL 3400 BELL AIR MALL AR FAYETTEVILLE NW ARKANSAS MALL 4201 N SHILOH DR AR FORT SMITH CENTRAL MALL 5111 ROGERS AVE AR JONESBORO MALL @ TURTLE CREEK 3000 E HIGHLAND DR STE 516 AR LITTLE ROCK SHACKLEFORD CROSSING 2600 S SHACKLEFORD RD AR NORTH LITTLE ROCK MC CAIN SHOPG CNTR 3929 MCCAIN BLVD STE 500 AR ROGERS PINNACLE HLLS PROMDE 2202 BELLVIEW RD AZ CHANDLER MILL CROSSING 2180 S GILBERT RD AZ FLAGSTAFF FLAGSTAFF MALL 4600 N US HWY 89 AZ GLENDALE ARROWHEAD TOWNE CTR 7750 W ARROWHEAD TOWNE CENTER AZ GOODYEAR PALM VALLEY CORNERST 13333 W MCDOWELL RD AZ LAKE HAVASU CITY SHOPS @ LAKE HAVASU 5651 HWY 95 N AZ MESA SUPERST'N SPRINGS ML 6525 E SOUTHERN AVE AZ NOGALES MARIPOSA WEST PLAZA 220 W MARIPOSA RD AZ PHOENIX AHWATUKEE FOOTHILLS 5050 E RAY RD AZ PHOENIX CHRISTOWN SPECTRUM 1727 W BETHANY HOME RD AZ PHOENIX PARADISE VALLEY MALL 4510 E CACTUS RD AZ TEMPE TEMPE MARKETPLACE 1900 E RIO SALADO PKWY STE 140 AZ TUCSON EL CON SHPG CNTR 3501 E BROADWAY AZ TUCSON TUCSON MALL 4530 N ORACLE RD AZ TUCSON TUCSON SPECTRUM 5265 S CALLE SANTA CRUZ AZ YUMA YUMA PALMS S C 1375 S YUMA PALMS PKWY CA ANTIOCH ORCHARD @SLATTEN RCH 4951 SLATTEN RANCH RD CA ARCADIA WESTFLD SANTA ANITA 400 S BALDWIN AVE CA BAKERSFIELD VALLEY PLAZA 2501 MING AVE CA BREA BREA MALL 400 BREA MALL CA CARLSBAD PLAZA CAMINO REAL 2555 EL CAMINO REAL CA CARSON SOUTHBAY PAV @CARSON 20700 AVALON -

Station Square Station Area Plan Executive Summary

STATION SQUARE STATION AREA PLAN EXECUTIVE SUMMARY STATION ACCESS STATION DESIGN PORT AUTHORITY OF ALLEGHENY COUNTY PLANNING AND EVALUATION DEPARTMENT PURPOSE CONTEXT The Port Authority’s Planning and Evaluation Department has initiated The Station Square transit center is home to four bus stops, a light rail a Station Improvement Program (SIP) that is focused on promoting station, and an incline station and occupies a critical location within the Transit-Oriented Development (TOD), improving operations, and Pittsburgh region; it is separated from the central business district by enhancing customer amenities at select fixed-guideway stations, with the Monongahela River, is directly adjacent to a destination mixed-use the ultimate goal of growing ridership and revenue for the agency. development (Station Square), and lies along Carson Street – a major Ideally, new capital investment at transit stations will in turn leverage commercial corridor of South Side neighborhoods. In 1976, Station new development adjacent to Port Authority transit. Stations were Square was developed as a historic adaptive reuse project by the prioritized for the SIP based on a detailed evaluation of factors Pittsburgh History and Landmarks Foundation (it is currently owned by contributing to TOD, with Station Square rated as one of the high priority Forest City Enterprises). locations. Relevant external and internal stakeholders were engaged to A new mixed-use development, Glasshouse, recently broke ground at ensure that proposed initiatives reflect common goals and objectives. the northeast corner of East Carson Street and Smithfield Street. The first phase of the new development by the Trammell Crow Company will have 320 multi-family units, with additional phases planned to include a mix of commercial uses. -

Student Handbook

SSTTUUDDEENNTT HHAANNDDBBOOOOKK Pittsburgh Theological Seminary Student Handbook Students are responsible for knowing and understanding its contents. Revised: September 10, 2019 1 STUDENT HANDBOOK PTS PURPOSE ...................................................................................... 5 PTS COMMUNITY .............................................................................. 5 PTS MISSION ....................................................................................... 6 PTS VISION .......................................................................................... 6 PTS COMMUNITY STANDARDS OF COMMUNICATION AND CONDUCT .................................................................................. 7 PTS HOURS .......................................................................................... 8 COUNSELING SUPPORT…………………………………………….8 MENTAL HEALTH SUPPORT……………………………………….8 I. ACADEMIC REGULATIONS AND PROCEDURES ................. 9 A. Residency Requirement .......................................................... 9 B. Student Classifications ........................................................... 9 C. Faculty Advisor ...................................................................... .9 D. Student Files ............................................................................ 9 E. Registration ............................................................................. 9 F. Types of Courses .................................................................. 10 G. Field Education .................................................................... -

Radio Shack Closing Locations

Radio Shack Closing Locations Address Address2 City State Zip Gadsden Mall Shop Ctr 1001 Rainbow Dr Ste 42b Gadsden AL 35901 John T Reid Pkwy Ste C 24765 John T Reid Pkwy #C Scottsboro AL 35768 1906 Glenn Blvd Sw #200 - Ft Payne AL 35968 3288 Bel Air Mall - Mobile AL 36606 2498 Government Blvd - Mobile AL 36606 Ambassador Plaza 312 Schillinger Rd Ste G Mobile AL 36608 3913 Airport Blvd - Mobile AL 36608 1097 Industrial Pkwy #A - Saraland AL 36571 2254 Bessemer Rd Ste 104 - Birmingham AL 35208 Festival Center 7001 Crestwood Blvd #116 Birmingham AL 35210 700 Quintard Mall Ste 20 - Oxford AL 36203 Legacy Marketplace Ste C 2785 Carl T Jones Dr Se Huntsville AL 35802 Jasper Mall 300 Hwy 78 E Ste 264 Jasper AL 35501 Centerpoint S C 2338 Center Point Rd Center Point AL 35215 Town Square S C 1652 Town Sq Shpg Ctr Sw Cullman AL 35055 Riverchase Galleria #292 2000 Riverchase Galleria Hoover AL 35244 Huntsville Commons 2250 Sparkman Dr Huntsville AL 35810 Leeds Village 8525 Whitfield Ave #121 Leeds AL 35094 760 Academy Dr Ste 104 - Bessemer AL 35022 2798 John Hawkins Pky 104 - Hoover AL 35244 University Mall 1701 Mcfarland Blvd #162 Tuscaloosa AL 35404 4618 Hwy 280 Ste 110 - Birmingham AL 35243 Calera Crossing 297 Supercenter Dr Calera AL 35040 Wildwood North Shop Ctr 220 State Farm Pkwy # B2 Birmingham AL 35209 Center Troy Shopping Ctr 1412 Hwy 231 South Troy AL 36081 965 Ann St - Montgomery AL 36107 3897 Eastern Blvd - Montgomery AL 36116 Premier Place 1931 Cobbs Ford Rd Prattville AL 36066 2516 Berryhill Rd - Montgomery AL 36117 2017 280 Bypass