AVAYA INC Form 10-K Annual Report Filed 2012-12-12

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Symbian OS As a Research Platform – Present and Future

Symbian OS as a Research Platform Present and Future Lawrence Simpson Research Department Symbian Copyright © 2008 Symbian Software Ltd. Symbian Platform Symbian OS is a separate platform, specifically designed for mobile & convergent devices. Not an adaptation of Unix or Windows or .... Symbian OS has facilities to support • Small (memory) footprint • Low power consumption • High reliability • “Always on”, but must deal with unplanned shutdown • Diverse range of hardware • Diverse manufacturers – multiple UIs and multiple brands Different UIs on the same underlying system Series 60 (S60) • Provided by Nokia. • Used by Nokia & S60 licensees. • Originally a keypad-based UI ... now supporting touch-screen variants. UIQ • Provided by UIQ – company has sometimes been owned by Symbian, sometimes by Sony Ericsson/Motorola. • Used by Sony Ericsson & Motorola. • Originally mainly a touch-screen UI ... now supporting keypad-only variants. MOAP(S) • Provided through NTT DOCOMO. • Used by several Symbian licensees in Japan. Software in a Symbian Phone – “Habitats of the Symbian Eco-System” User-Installed Applications “In-the-box” Applications (commissioned/written by the phone-maker, built into the phone ROM) User Interface (S60 or UIQ or MOAP) Symbian OS Hardware Adaptation Software (usually from chip-vendors or 3rd parties) Symbian OS component level view developer.symbian.com/main/documentation/technologies/system_models OS designed for Smartphones & Media Phones Core OS Technologies Other Smartphone Technologies • Telephony Services • PIM (calendars, agenda, etc.) • Shortlink (BT, USB) Services • Messaging • Networking (IP) Services • Remote Management • Multimedia (audio & video) • Java / J2ME • Graphics • Security Management • Location-Based Services (LBS) • Multimedia Middleware • Base Services: (Database Utilities, • Application Protocols Localisation, etc.) • GUI Framework • Kernel Symbian programming paradigms • Several paradigms to support mobility, reliability, security, including.. -

Avaya 1120E IP Deskphone User Guide

Avaya 1120E IP Deskphone User Guide Avaya Communication Server 1000 Document Status: Standard Document Version: 07.02 Part Code: NN43112-103 Date: March 2013 Licenses THE SOFTWARE LICENSE TERMS AVAILABLE ON © 2013 Avaya Inc. All Rights Reserved. THE AVAYA WEBSITE, HTTP:// Notice SUPPORT.AVAYA.COM/LICENSEINFO ARE APPLICABLE TO ANYONE WHO DOWNLOADS, While reasonable efforts have been made to ensure USES AND/OR INSTALLS AVAYA SOFTWARE, that the information in this document is complete and PURCHASED FROM AVAYA INC., ANY AVAYA accurate at the time of printing, Avaya assumes no AFFILIATE, OR AN AUTHORIZED AVAYA liability for any errors. Avaya reserves the right to RESELLER (AS APPLICABLE) UNDER A make changes and corrections to the information in COMMERCIAL AGREEMENT WITH AVAYA OR AN this document without the obligation to notify any AUTHORIZED AVAYA RESELLER. UNLESS person or organization of such changes. OTHERWISE AGREED TO BY AVAYA IN WRITING, Documentation disclaimer AVAYA DOES NOT EXTEND THIS LICENSE IF THE SOFTWARE WAS OBTAINED FROM ANYONE “Documentation” means information published by OTHER THAN AVAYA, AN AVAYA AFFILIATE OR AN Avaya in varying mediums which may include product AVAYA AUTHORIZED RESELLER; AVAYA information, operating instructions and performance RESERVES THE RIGHT TO TAKE LEGAL ACTION specifications that Avaya generally makes available to AGAINST YOU AND ANYONE ELSE USING OR users of its products. Documentation does not include SELLING THE SOFTWARE WITHOUT A LICENSE. marketing materials. Avaya shall not be responsible BY INSTALLING, DOWNLOADING OR USING THE for any modifications, additions, or deletions to the SOFTWARE, OR AUTHORIZING OTHERS TO DO original published version of documentation unless SO, YOU, ON BEHALF OF YOURSELF AND THE such modifications, additions, or deletions were ENTITY FOR WHOM YOU ARE INSTALLING, performed by Avaya. -

Symbian Foundation Press Conference

Symbian Foundation Press conference M/C – Merran Wrigley Exciting Internet experiences for the aspirations of billions 2 © 2008 Symbian Foundation Mobile software set free Symbian Foundation Kai Öistämö Executive Vice President, Nokia Shared vision for an unparalleled open mobile software platform 4 © 2008 Symbian Foundation That unites Symbian OS, S60, UIQ and MOAP(S) 5 © 2008 Symbian Foundation Creating the most proven, open, complete mobile software platform 6 © 2008 Symbian Foundation With over 200 million devices already shipped 7 © 2008 Symbian Foundation For free. 8 © 2008 Symbian Foundation Creating one platform, royalty-free Foundation Differentiated Member experience MOAP(S) 9 © 2008 Symbian Foundation Creating one platform, royalty-free Foundation Differentiated Member experience Symbian Foundation Platform Applications suite Runtimes UI framework Middleware Operating system Tools & SDK 10 © 2008 Symbian Foundation The first step to our goal • Acquiring Symbian Ltd • Closing expected in Q4 2008 • Symbian Ltd to be part of Nokia • Nokia will contribute Symbian OS and S60 to Symbian Foundation 11 © 2008 Symbian Foundation Fulfilling the Symbian mission Symbian Foundation Nigel Clifford CEO, Symbian Symbian Ltd Mission To become the most widely used software platform on the planet 13 © 2008 Symbian Foundation The leading global open platform 12% Symbian Linux 11% Microsoft RIM 60% Apple 11% Other Source Canalys – Cumulative 4% 12 month period to Q1 2008 2% 14 © 2008 Symbian Foundation The choice for the top vendors Samsung MOTO -

Federal Communications Commission FCC 15-35 Before the Federal

Federal Communications Commission FCC 15-35 Before the Federal Communications Commission Washington, D.C. 20554 In the Matters of ) ) Telcordia Technologies, Inc. Petition to Reform ) WC Docket No. 07-149 Amendment 57 and to Order a Competitive ) Bidding Process for Number Portability ) Administration ) ) Petition of Telcordia Technologies, Inc. to Reform ) WC Docket No. 09-109 or Strike Amendment 70, to Institute Competitive ) Bidding for Number Portability ) Administration, and to End the NAPM LLC’s ) Interim Role in Number Portability ) Administration Contract Management ) ) Telephone Number Portability ) CC Docket No. 95-116 ) ORDER Adopted: March 26, 2015 Released: March 27, 2015 By the Commission: Chairman Wheeler and Commissioners Clyburn and Pai issuing separate statements; Commissioner O’Rielly approving in part, concurring in part, and issuing a statement. TABLE OF CONTENTS Heading Paragraph # I. INTRODUCTION .................................................................................................................................. 1 II. BACKGROUND .................................................................................................................................... 4 A. First LNPA Selection ....................................................................................................................... 5 B. Current LNPA Selection .................................................................................................................. 8 III. DISCUSSION ..................................................................................................................................... -

DEFINITY ECS Network Call Redirection

'(),1,7< (QWHUSULVH&RPPXQLFDWLRQV6HUYHU Network Call Redirection 555-233-759 Comcode 700156342 Issue 2.0 July 2001 Copyright 2001, Avaya Inc. To prevent intrusions to your telecommunications equipment, you and All Rights Reserved, Printed in U.S.A. your peers should carefully program and configure your: Notice • Lucent-provided telecommunications systems and their interfaces Every effort was made to ensure that the information in this book was com- • Lucent-provided software applications, as well as their underlying plete and accurate at the time of printing. However, information is subject hardware/software platforms and interfaces to change. • Any other equipment networked to your Lucent products Avaya Inc. Web Page Avaya Inc. does not warrant that this product or any of its networked equip- The world wide web home page for Avaya Inc. is: ment is either immune from or will prevent either unauthorized or mali- http://www.avaya.com cious intrusions. Avaya Inc.Avaya Inc. will not be responsible for any Preventing Toll Fraud charges, losses, or damages that result from such intrusions. “Toll fraud” is the unauthorized use of your telecommunications system by Federal Communications Commission Statement an unauthorized party (for example, a person who is not a corporate Part 15: Class A Statement. This equipment has been tested and found to employee, agent, subcontractor, or working on your company’s behalf). Be comply with the limits for a Class A digital device, pursuant to Part 15 of aware that there may be a risk of toll fraud associated with your system and the FCC Rules. These limits are designed to provide reasonable protection that, if toll fraud occurs, it can result in substantial additional charges for against harmful interference when the equipment is operated in a commer- your telecommunications services. -

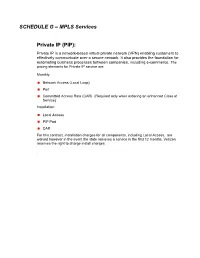

SCHEDULE G – MPLS Services Private IP (PIP)

SCHEDULE G – MPLS Services Private IP (PIP): Private IP is a network-based virtual private network (VPN) enabling customers to effectively communicate over a secure network. It also provides the foundation for automating business processes between companies, including e-commerce, The pricing elements for Private IP service are: Monthly: Network Access (Local Loop) Port Committed Access Rate (CAR) (Required only when ordering an enhanced Class of Service) Installation: Local Access PIP Port CAR For this contract, installation charges for all components, including Local Access, are waived however in the event the state removes a service in the first 12 months, Verizon reserves the right to charge install charges. Private IP Service Local Access pricing is as per the table in Schedule F2 INSTALLATION WAIVER Verizon will not charge Installation up front. If the State disconnects the service prior to 12 months, Verizon reserves the right to charge the standard installtion fee. This applies to PIP Ports only. Features and Optional services are not included PORT CHARGES Port Speed MRC NRC Port Speed MRC NRC 64 Kbps $ 36.75 $ 50.00 600M Sub-Rate OC12 $ 8,433.81 $ 600.00 256 Kbps $ 78.33 $ 100.00 1M Ethernet $ 162.12 $ 600.00 512 Kbps $ 123.69 $ 100.00 2M Ethernet $ 124.00 $ 600.00 1.024 Mbps $ 162.12 $ 100.00 3M Ethernet $ 149.00 $ 600.00 T1 $ 155.00 $ 200.00 4M Ethernet $ 175.00 $ 600.00 3.072 Mbps $ 269.00 $ 600.00 6M Ethernet $ 229.00 $ 600.00 4.608 Mbps $ 350.00 $ 600.00 8M Ethernet $ 268.00 $ 600.00 6.144 Mbps $ 402.00 $ 600.00 10M -

Avaya Definity ECS Whats New in R9.0.Pdf

DEFINITY® Enterprise Communications Server What’s New for Release 9 555-233-766 Issue 2 February 2001 Copyright 2001 Avaya Inc. All rights reserved. For trademark, regulatory compliance, and related legal information, see the copyright and legal notices section of this document. Copyright and legal notices Copyright Copyright 2001 by Avaya Inc. All rights reserved. This material is protected by the copyright laws of the United States and other countries. It may not be reproduced, distributed, or altered in any fashion by any entity (either internal or external to Avaya), except in accordance with applicable agreements, contracts or licensing, without the express written consent of the BCS Product Publications organization and the business management owner of the material. This document was prepared by the Product Publications department of the Business Communications Systems division of Avaya. Offices are located in Denver CO, Columbus OH, Middletown NJ, and Basking Ridge NJ, USA. DEFINITY ECS What’s New for Release 9 555-233-766 Issue 2 February 2001 iii Copyright and legal notices Trademarks DEFINITY, AUDIX, CONVERSANT, elemedia, SABLIME, Talkbak, Terranova, WaveLAN, MERLIN, MERLIN LEGEND and GuestWorks are registered trademarks and 4ESS, 5ESS, Intuity, OneMeeting, OneVision, PacketStar, PathStar, ProLogix, Lucent, Lucent Technologies, and the Lucent Technologies logo are trademarks of Lucent Technologies. Pentium is a registered trademark of Intel Corporation. Microsoft, Windows, and Windows NT are registered trademarks and Video for Windows is a trademark of Microsoft Corporation. UNIX is a registered trademark of UNIX System Laboratories, Inc., a wholly-owned subsidiary of Novell, Inc. X Window System is a trademark and product of the Massachusetts Institute of Technology. -

Matching Gift Programs * Please Note, This List Is Not All Inclusive

Companies With Matching Gift Programs * Please note, this list is not all inclusive. If your employer is not listed, please check with human resources to see if your company matches and the guidelines for matches. A AlliedSignal Inc. Archer Daniels Midland 3Com Corporation Allstate Foundation, Allstate Giving ARCO Chemical Co. 3M Company Altera Corp. Contributions Program Ares Advanced Technology AAA Altria Employee Involvement Ares Management LLC Abacus Capital Investments Altria Group Argonaut Group Inc. Abbot Laboratories AMB Group Aristokraft Inc. Accenture Foundation, Inc. Ambac Arkansas Best Corporation Access Group, Inc. AMD Corporate Giving Arkwright Mutual Insurance Co. ACE INA Foundation American Express Co. Armco Inc. Acsiom Corp. American Express Foundation Armstrong Foundation Adams Harkness and Hill Inc. American Fidelity Corp. Arrow Electronics Adaptec Foundation American General Corp. Arthur J. Gallagher ADC Foundation American Honda Motor Co. Inc. Ashland Oil Foundation, Inc. ADC Telecommunications American Inter Group Aspect Global Giving Program Adobe Systems Inc. American International Group, Inc. Aspect Telecommunications Associates ADP Foundation American National Bank and Trust Co. Corp. of North America A & E Television Networks of Chicago Assurant Health AEGON TRANSAMERICA American Standard Foundation Astra Merck Inc. AEP American Stock Exchange AstraZeneca Pharmaceutical LP AES Corporation Ameriprise Financial Atapco A.E. Staley Manufacturing Co. Ameritech Corp. ATK Foundation Aetna Foundation, Inc. Amgen Center Atlantic Data Services Inc. AG Communications Systems Amgen Foundation Atochem North America Foundation Agilent Technologies Amgen Inc. ATOFINA Chemicals, Inc. Aid Association for Lutherans AMN Healthcare Services, Inc. ATO FINA Pharmaceutical Foundation AIG Matching Grants Program Corporate Giving Program AT&T Aileen S. Andrew Foundation AmSouth BanCorp. -

Application Notes for SIP Trunking Using Verizon Business IP Trunking

Avaya Solution & Interoperability Test Lab Application Notes for SIP Trunking Using Verizon Business IP Trunking Service with Avaya IP Office Release 11.1 and Avaya Session Border Controller for Enterprise Release 8.1 – Issue 1.0 Abstract These Application Notes describe a reference configuration using Session Initiation Protocol (SIP) trunking between the Verizon Business IP Trunking service offer and an Avaya IP Office solution. In the reference configuration, the Avaya IP Office solution consists of Avaya IP Office Server Edition Release 11.1, Avaya Session Border Controller for Enterprise Release 8.1 and Avaya SIP, H.323, digital, and analog endpoints. These Application Notes complement previously published Application Notes by illustrating the configuration screens and Avaya testing of IP Office Release 11.1 and Avaya Session Border Controller for Enterprise Release 8.1. The Verizon Business IP Trunking service offer referenced within these Application Notes is designed for business customers. The service enables local and long distance PSTN calling via standards-based SIP trunks directly, without the need for additional TDM enterprise gateways or TDM cards and the associated maintenance costs. Readers should pay attention to Section 2, in particular the scope of testing as outlined in Section 2.1 as well as the observations noted in Section 2.2, to ensure that their own use cases are adequately covered by this scope and results. Information in these Application Notes has been obtained through DevConnect compliance testing and additional technical discussions. Testing was conducted in the Avaya Solution & Interoperability Test Lab, utilizing a Verizon Business Private IP (PIP) circuit connection to the production Verizon Business IP Trunking service. -

Detection of Smartphone Malware

Detection of Smartphone Malware Eingereicht von Diplom-Informatiker Aubrey-Derrick Schmidt Von der Fakult¨atIV { Elektrotechnik und Informatik der Technischen Universit¨atBerlin zur Erlangung des akademischen Grades Doktor der Ingenieurwissenschaften { Dr.-Ing. { genehmigte Dissertation Promotionsausschuß: Vorsitzender: Prof. Dr. Jean-Pierre Seifert Berichter: Prof. Dr.-Ing. Sahin Albayrak Berichter: Prof. Dr. Fernando C. Colon Osorio Tag der wissenschaftlichen Aussprache: 28.06.2011 Berlin 2011 D 83 ii Acknowledgements On completion of my Ph.D. thesis I would like to sincerely thank all those who supported me in realizing and finishing my work. First of all, I am heartily thankful to my supervisors and Ph.D. Com- mittee spending time and effort on me. Prof. Dr.-Ing. Sahin Albayrak and Ph.D. Ahmet Camtepe always were a shining example for scientific success to me. Throughout all of the stages of my thesis, they helped me to keep track on the right research direction, seriously revised all of my work, and patiently discussed and resolved issues not only related to my work. I am also deeply moved by their serious and honest attitude towards academic work. Additionally, I really appreciate their will for hosting and motivating me all the time while working at DAI-Laboratory at Technische Univer- sit¨atBerlin. I want to honestly thank them for their friendly, personal, and self-sacrificing will to help me in any situation throughout my time at the DAI-Laboratory. When meeting Prof. Dr. Fernando C. Colon Osorio on Malware Conference 2009 in Montreal the first time, I was really impressed by his will to put scientific discussion into the focus of the conference. -

Avaya Call Management System Software Installation, Maintenance, and Troubleshooting for Linux®

Avaya Call Management System Software Installation, Maintenance, and Troubleshooting for Linux® Release 18.0.2 February 2018 © 2018 Avaya Inc. All Rights Reserved. CHANNEL PARTNER; AVAYA RESERVES THE RIGHT TO TAKE LEGAL ACTION AGAINST YOU AND ANYONE ELSE USING OR SELLING THE Notice SOFTWARE WITHOUT A LICENSE. BY INSTALLING, DOWNLOADING OR While reasonable efforts have been made to ensure that the information in this USING THE SOFTWARE, OR AUTHORIZING OTHERS TO DO SO, YOU, ON document is complete and accurate at the time of printing, Avaya assumes no BEHALF OF YOURSELF AND THE ENTITY FOR WHOM YOU ARE liability for any errors. Avaya reserves the right to make changes and INSTALLING, DOWNLOADING OR USING THE SOFTWARE corrections to the information in this document without the obligation to notify (HEREINAFTER REFERRED TO INTERCHANGEABLY AS "YOU" AND "END any person or organization of such changes. USER"), AGREE TO THESE TERMS AND CONDITIONS AND CREATE A BINDING CONTRACT BETWEEN YOU AND AVAYA INC. OR THE Documentation disclaimer APPLICABLE AVAYA AFFILIATE ("AVAYA"). "Documentation" means information published in varying mediums which may Avaya grants You a license within the scope of the license types described include product information, operating instructions and performance below, with the exception of Heritage Nortel Software, for which the scope of specifications that are generally made available to users of products. the license is detailed below. Where the order documentation does not Documentation does not include marketing materials. Avaya shall not be expressly identify a license type, the applicable license will be a Designated responsible for any modifications, additions, or deletions to the original System License. -

Copyrighted Material

1 Introduction 1.1 The Convergence Device Convergence has been one of the major technology trends of the last decade. Like all trends, its roots go back much further; in this case you would probably trace them back to the first combination of computing and communications technologies that led to the birth of the Internet. Human interactions that had previously taken place via the physical transportation of paper could now occur almost instantaneously to any connected computer in the world. Increases in computing power, digital storage capacity and communications bandwidth then enabled more complex media – such as voice, music, high resolution images and video – to enter this digital world. Today, near instant global communications are available in multiple media, or multimedia, as they’re commonly described. At the same time this was happening, communications were shifting from fixed wires to mobile radio technologies, allowing people to connect with one another from anywhere. Computing has become increasingly portable, freeing users to work and play on the move. Imaging and video converged with computing to give us digital cameras and camcorders. Music and video distribution and storage have gone first digital and then portable. Global positioning technology combined with portable computingCOPYRIGHTED has brought us personal MATERIAL navigation devices. Almost inevitably, miniaturization and integration have led to the development of the ultimate convergence device – the multimedia smartphone. The term ‘smartphone’ was first applied to devices which combined the features of a mobile phone and a Personal Digital Assistant (PDA). As technology has advanced, that functionality is now available in some fairly low-end models.