The Gathering Storm in the Virtual World

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Laureate List 2011 3 27.Indd

THE LAUREATE THE COMPUTERWORLD HONORS PROGRAM | 2011 SYBASE CONGRATULATES OUR 2011 COMPUTERWORLD HONORS LAUREATES Bulgarian Electricity System Operator Cherry Creek School District Citizens Financial Group Everything Everywhere Limited JAGTAG Kodak Imaging Network Korea Ministry of Public Administration and Security (MOPAS) Matrix Systems and Solutions Medihelp Mobikash Afrika Congratulations Municipality of Aarhus 2011 Computerworld Honors Program New York State Division of Homeland Security and Emergency Laureates, Finalists, and Services — NY-ALERT 21st Century Achievement Award Recipients Oasis Medical Solutions Philippine Social Security System (SSS) Rafael Belloso Chacin University (URBE) Royal Netherlands Institute for Sea Research State of Maine Department of Health and Human Services Ready for what’s next. Swiss Medical Group, Argentina The desire to make a difference is the fi rst step that leads to success. Booz Allen Hamilton, a leading strategy and technology consulting fi rm, is proud Turkish Derivatives Exchange, Inc. (TurkDEX) to recognize the 2011 Computerworld Honors Program honorees. Thanks to your vision, commitment, and innovative use of IT, you’re making the world a better place. www.boozallen.com Copyright © 2011 Sybase, Inc. All rights reserved. Unpublished rights reserved under U.S. copyright laws. Sybase, and the Sybase logo, are trademarks of Sybase, Inc. or its subsidiaries. ® indicates registration in the United States of America. SAP, and the SAP logo, are the trademarks or registered trademarks of SAP AG in Germany and in several other countries. All other trademarks are the property of their respective owners. BA11-157_Computerworld Ad_052011Final.indd 1 5/20/11 8:32 AM . THE JOURNAL OF THE COMPUTERWORLD INFORMATION TECHNOLOGY AWARDS FOUNDATION . -

The Man Behind the Cloud an Interview with Vmware’S Paul Maritz

fear, greed and fairy tales • p.j. o’rourke is out off wworkrk It Pays to Be Lucky Where Have the Leaders Gone? Formula One’s Benign Despot The Buck Starts Here The Man Behind the Cloud An Interview with VMware’s Paul Maritz Q1.2012.2012 chief executive officer Gary Burnison chief marketing officer Michael Distefano editor-in-chief Joel Kurtzman creative director Joannah Ralston circulation director Peter Pearsall marketing operations manager Reonna Johnson board of advisors Sergio Averbach Cheryl Buxton Joe Griesedieck Byrne Mulrooney Kristen Badgley Dennis Carey Robert Hallagan Indranil Roy Michael Bekins Bob Damon Katie Lahey Jane Stevenson Stephen Bruyant-Langer Ana Dutra Robert McNabb Anthony Vardy contributing editors Chris Bergonzi Stephanie Mitchell David Berreby P.J. O’Rourke Lawrence M. Fisher Glenn Rifkin Victoria Griffi th Adrian Wooldridge Cover photo of Paul Maritz: The Korn/Ferry International Briefi ngs on Talent and Leadership is published Jeff Singer quarterly by the Korn/Ferry Institute. The Korn/Ferry Institute was founded to serve Cover illustration: as a premier global voice on a range of talent management and leadership issues. The Zé Otavio Institute commissions, originates and publishes groundbreaking research utilizing Korn/ Ferry’s unparalleled expertise in executive recruitment and talent development combined with its preeminent behavioral research library. The Institute is dedicated to improving the state of global human capital for businesses of all sizes around the world. ISSN 1949-8365 Copyright 2012, Korn/Ferry International Requests for additional copies should be sent directly to: Briefi ngs Magazine 1900 Avenue of the Stars, Suite 2600, Los Angeles, CA 90067 briefi [email protected] Briefi ngs is produced with solar power, FSC-certifi ed Advertising Sales Representative: paper, and soy-based inks, Erica Springer + Associates, LLC in a fully sustainable and 1355 S. -

![Implementing and Developing Cloud Computing Applications [2011]](https://docslib.b-cdn.net/cover/0117/implementing-and-developing-cloud-computing-applications-2011-3220117.webp)

Implementing and Developing Cloud Computing Applications [2011]

Implementing and Developing Cloud Computing Applications K11513_C000.indd 1 10/18/10 2:47 PM Implementing and Developing Cloud Computing Applications DAVID E.Y. SARNA K11513_C000.indd 3 10/18/10 2:47 PM Auerbach Publications Taylor & Francis Group 6000 Broken Sound Parkway NW, Suite 300 Boca Raton, FL 33487-2742 © 2011 by Taylor and Francis Group, LLC Auerbach Publications is an imprint of Taylor & Francis Group, an Informa business No claim to original U.S. Government works Printed in the United States of America on acid-free paper 10 9 8 7 6 5 4 3 2 1 International Standard Book Number: 978-1-4398-3082-6 (Hardback) This book contains information obtained from authentic and highly regarded sources. Reasonable efforts have been made to publish reliable data and information, but the author and publisher cannot assume responsibility for the validity of all materials or the consequences of their use. The authors and publishers have attempted to trace the copyright holders of all material reproduced in this publication and apologize to copyright holders if permission to publish in this form has not been obtained. If any copyright material has not been acknowledged please write and let us know so we may rectify in any future reprint. Except as permitted under U.S. Copyright Law, no part of this book may be reprinted, reproduced, transmitted, or utilized in any form by any electronic, mechanical, or other means, now known or hereafter invented, including photocopying, micro- filming, and recording, or in any information storage or retrieval system, without written permission from the publishers. -

The Essential Guide to Legacy-Free Disaster Recovery

The Essential Guide to Legacy-Free Disaster Recovery Sponsored by The Essential Guide to Legacy-Free Disaster Recovery Drop the baggage and simplify your Disaster Recovery strategy Sean Clark VCP 2, 3, 4 and VMware vExpert 2009 white paper / page 1 The Essential Guide to Legacy-Free Disaster Recovery The Essential Guide to Legacy-Free Disaster Recovery Executive summary The benefits of VMware virtualization for servers are unmistakable. The last five years have seen a relentless march towards virtual being the deployment option of choice. At the VMworld 2010 keynote in San Francisco, VMware CEO Paul Maritz even quoted statistics from IDC that 2010 was the first year that servers shipped with a virtualization platform outnumbered common physical servers. This shift is due to the well-known benefits of server consolidation: lower server hardware costs, reduced datacenter power consumption, and increased efficiency of operations. But availability, disaster recovery (DR), and disaster avoidance benefits are also drivers for increased virtualization and key enablers for bringing Tier 1 business-critical workloads onto VMware platforms. Legacy technologies are a drag on the efficiency of IT operations. The need for cautiously adopting new technology and “dipping a toe” before jumping in are well understood. But when it comes to DR planning for VMware environments, we’ve been a little too conservative in leaving legacy technologies and designs behind. It’s like the first automobile engineers who continued the practice of placing whip holders on the frame of new automobiles (horseless carriages). It’s now time to stop engineering new DR plans with their version of “whip holders.” It’s time to drop the legacy processes, technology, and thinking. -

Microsoft's Monopoly Power Is Also Demonstrated by a Structural Analysis

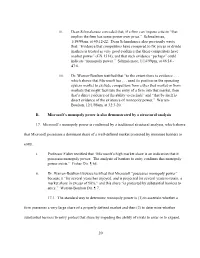

ii. Dean Schmalensee conceded that, if a firm can impose a tie-in “that implies the firm has some power over price.” Schmalensee, 1/19/99am, at 40:12-22. Dean Schmalensee also previously wrote that: “Evidence that competitors have conspired to fix prices or divide markets is treated as very good evidence that these competitors have market power” (GX 1514), and that such evidence “perhaps” could indicate “monopoly power.” Schmalensee, 1/14/99pm, at 46:14 - 47:6. iii. Dr. Warren-Boulton testified that “to the extent there is evidence . which shows that Microsoft has . used its position in the operating system market to exclude competitors from either that market or from markets that might facilitate the entry of a firm into that market, then that’s direct evidence of the ability to exclude” and “that by itself is direct evidence of the existence of monopoly power.” Warren- Boulton, 12/1/98am, at 32:3-20. B. Microsoft’s monopoly power is also demonstrated by a structural analysis 17. Microsoft’s monopoly power is confirmed by a traditional structural analysis, which shows that Microsoft possesses a dominant share of a well-defined market protected by immense barriers to entry. i. Professor Fisher testified that “Microsoft’s high market share is an indication that it possesses monopoly power. The analysis of barriers to entry confirms that monopoly power exists.” Fisher Dir. ¶ 65. ii. Dr. Warren-Boulton likewise testified that Microsoft “possesses monopoly power” because it “for several years has enjoyed, and is projected for several years to retain, a market share in excess of 90%,” and this share “is protected by substantial barriers to entry.” Warren-Boulton Dir. -

Oral History of Pat Gelsinger, Part 2

Oral History of Pat Gelsinger, part 2 Interviewed by: David C. Brock Doug Fairbairn Recorded March 21, 2019 Mountain View, CA CHM Reference number: X8899.2019 © 2019 Computer History Museum Oral History of Pat Gelsinger, part 2 Fairbairn: So the thing I’d like to start out with is just get your observations on Intel’s ability to identify future trends and really capitalize on them before they had become obvious movements within the industry versus being able to jump on a bandwagon that has already started and out executing somebody who may have already established a lead there. So I’d be interested in your observations as to whether that was an accurate perception and to the extent that it was. What within the Intel culture or whatever might contribute to that? Gelsinger: Yeah, I’ll give three different observations on that. One is I actually give Intel a little bit more credit on the PC situation in the sense that, the Crush campaign as it was described at the time was go get design wins everywhere. We know we’re not going be able to necessarily predict the future, so plant as many seeds as possible, right, and one of them just happened to be the PC, , the IBM design win. But maybe all these other designs actually came to fruition and became embedded in this and other things associated with it. So I think there was actually a deep realization that we’re on to something big and we’re not going to be able to predict necessarily what circuitous route it may or not play in the marketplace. -

Implementing and Developing Cloud Computing Applications

Implementing and Developing Cloud Computing Applications DAVID E.Y. SARNA K11513_C000.indd 3 10/18/10 2:47 PM Auerbach Publications Taylor & Francis Group 6000 Broken Sound Parkway NW, Suite 300 Boca Raton, FL 33487-2742 © 2011 by Taylor and Francis Group, LLC Auerbach Publications is an imprint of Taylor & Francis Group, an Informa business No claim to original U.S. Government works Printed in the United States of America on acid-free paper 10 9 8 7 6 5 4 3 2 1 International Standard Book Number: 978-1-4398-3082-6 (Hardback) This book contains information obtained from authentic and highly regarded sources. Reasonable efforts have been made to publish reliable data and information, but the author and publisher cannot assume responsibility for the validity of all materials or the consequences of their use. The authors and publishers have attempted to trace the copyright holders of all material reproduced in this publication and apologize to copyright holders if permission to publish in this form has not been obtained. If any copyright material has not been acknowledged please write and let us know so we may rectify in any future reprint. Except as permitted under U.S. Copyright Law, no part of this book may be reprinted, reproduced, transmitted, or utilized in any form by any electronic, mechanical, or other means, now known or hereafter invented, including photocopying, micro- filming, and recording, or in any information storage or retrieval system, without written permission from the publishers. For permission to photocopy or use material electronically from this work, please access www.copyright.com (http://www. -

Managing Virtual Machines

25-31 October 2011 | computerweekly.com Why IT projects fail WE ASK THE EXPERTS WHY TECHNOLOGY PROGRAMMES ARE PLAGUED WITH PROBLEMS PAGe 13 Managing virtual machines VMWARE CEO PAUL MARITZ SETS OUT HIS VISION FOR VIRTUALISATION PAGe 4 Getting NHS IT into shape HEALTH SERVICE INTERIM IT CHIEF KATIE DAVIS ON MANAGING THE TECHNOLOGY TO SUPPORT CHANGE PAGe 5 COMSTOCK IMAGES Highlights from the week online MOST POPULAR PHOTO STORY PREMIUM CONTENT Samsung sues to block > The reality behind government 1 Apple iPhone 4S cloud computing hype: Gartner computerweekly.com/248167.htm Cloud computing remains an important trend and, in the long run, RIM offers free technical will have a transformational impact 2 support after outages on the way government organisa- computerweekly.com/248173.htm tions access and leverage IT. However, the path to the cloud is Military-grade cyber attacks: definitely slower and more tortuous 3 How businesses can be safe than many wish to think. computerweekly.com/248174.htm computerweekly.com/248039.htm Data warehouse suppliers > Research: Do CIOs have more 4 will integrate Hadoop clarity about cloud computing? computerweekly.com/248169.htm Xantus surveyed a panel of 50 CIOs from organisations across a range CESG approves first of public and private sectors and 5 encrypted USB flash drive > Business apps for the iPhone sizes. The results show that, while computerweekly.com/248170.htm In this photo story we look at the applications, including GoodReader and there is still a reluctance to fully 1Password Pro, that make the iPhone a smartphone for business. commit to the cloud, there is a Microsoft will disrupt computerweekly.com/48151-1.htm general acceptance of the benefits 6 developer community and a growing commitment to computerweekly.com/248163.htm develop those benefits as far as VIDEOS practicable. -

UNITED STATES DISTRICT COURT for the District of Utah Central Division ______Novell, Inc., * NOVELL’S OPPOSITION to Plaintiff, * JUDGMENT AS a MATTER of LAW * V

Case 2:04-cv-01045-JFM Document 302 Filed 11/18/11 Page 1 of 114 MAX D. WHEELER (3439) MARALYN M. ENGLISH (8468) SNOW, CHRISTENSEN & MARTINEAU 10 Exchange Place, 11th Floor P.O. Box 45000 Salt Lake City, Utah 84145-5000 Telephone (801) 521-9000 Facsimile: (801) 363-0400 JEFFREY M. JOHNSON (admitted pro hac vice) PAUL R. TASKIER (admitted pro hac vice) ADAM PROUJANSKY (admitted pro hac vice) JAMES R. MARTIN (admitted pro hac vice) DICKSTEIN SHAPIRO LLP 1825 Eye Street, NW Washington, DC 20006-5403 Telephone: (202) 420-2200 Facsimile: (202) 420-2201 R. BRUCE HOLCOMB (admitted pro hac vice) ADAMS HOLCOMB LLP 1875 Eye Street, NW, Suite 810 Washington, DC 20006-5403 Telephone: (202) 580-8820 Facsimile: (202) 580-8821 JOHN E. SCHMIDTLEIN (admitted pro hac vice) WILLIAMS & CONNOLLY LLP 725 Twelfth Street, NW Washington, DC 20005 Telephone: (202) 434-5901 Facsimile: (202) 434-5029 Attorneys for Novell, Inc. ______________________________________________________________________________ UNITED STATES DISTRICT COURT for the District of Utah Central Division __________________________________________________________________ Novell, Inc., * NOVELL’S OPPOSITION TO Plaintiff, * JUDGMENT AS A MATTER OF LAW * v. * * Microsoft Corporation, * Case No. 2:04-cv-01045-JFM Defendant. * Hon. J. Frederick Motz _____________________________________________________________________________ Case 2:04-cv-01045-JFM Document 302 Filed 11/18/11 Page 2 of 114 Table of Contents Page TABLE OF AUTHORITIES ........................................................................................................ -

The Rise of Virtualization

VMware’s Past, Containerware Today, and All the Clouds for the Future VMware’s Past, Containerware Today, and All the Clouds for the Future by, Stuart Miniman August 24th, 2019 2019 is the tenth year of theCUBE at VMworld (see theCUBE.net for this year’s event)! I’ve had the pleasure of working with VMware since 2002: when their most popular product was Workstation; when they were starting to offer server virtualization, but before vMotion; and well before we were talking about cloud computing. In this article […] © 2019 Wikibon Research | Page 1 VMware’s Past, Containerware Today, and All the Clouds for the Future 2019 is the tenth year of theCUBE at VMworld (see theCUBE.net for this year’s event)! I’ve had the pleasure of working with VMware since 2002: when their most popular product was Workstation; when they were starting to offer server virtualization, but before vMotion; and well before we were talking about cloud computing. In this article I’m going to take a look at the ebb and flow of VMware’s role in the waves of change in the technology industry. See some companion coverage on SiliconANGLE: ● Focus on multicloud: Analyzing VMware’s history and challenges ahead of VMworld ● The 5 best predictions we got right about VMware, and one we got totally wrong ● VMworld preview show: John Furrier, Dave Vellante analysis with special appearances from VMware’s Sanjay Poonen and Robin Matlock: The Rise of Virtualization Server virtualization is pervasive today, but in the early days, it took a lot of time to educate and sort out the details of what would and wouldn’t work. -

EMC Overview

CW+ a whitepaper from ComputerWeekly EMC overview EMC was incorporated in Massachusetts in 1979, and is headquartered in Hopkinton, Massachusetts (pictured left). It operates in two broad categories: its information infrastructure business, and its VMware virtual infrastructure operation, represented by its majority stake in VMware. The company is divided into several segments. Information Storage handles its core storage products, and EMC Global Services helps customer to design and EMC: From storage deploy storage systems in their organisa- tions. RSA Information Security handles its security presence, while the Information Intelligence Group helps customers to use to big data their information more effectively in areas such as governance and records manage- ment. VMware focuses on virtual and by Danny Bradbury cloud-based offerings. EMC has expanded rapidly from a simple storage company to a firm that supports several of IT’s major pillars, but to fulfil its potential it must integrate its many acquisitions and overcome the challenges of commoditisation and increasing competition in the storage market Back in the good old days of computing, when the industry was awash with money, blockbuster product launches were a regular thing. Analysts and journalists would be flown across oceans to participate in rock concert-style roll-outs of unremarkable products. Post-crash, transatlantic flights have been replaced with product launches in Bracknell and sandwiches. So when EMC crammed 26 dancers into the back of a Mini Cooper in New York in January 2011, it seemed like old times. The stunt set a Guinness World Record to mark EMC’s launch of 41 storage products. -

Aileen Black VP, Public Sector

Aileen Black VP, Public Sector Aileen Black leads VMware's sales and strategy for the Public Sector. With more than 23 years in the high tech industry supporting the government market, Aileen has worked at Data General, EMC, Ontos Corporation and Oracle. Aileen earned a Bachelor of Science from the University of Tampa and her MBA from Marymount University. Andrea Eubanks Sr. Director, Enterprise and Technical Marketing Andrea Eubanks is responsible for enterprise and technical marketing at VMware. Andrea has more than 18 years of experience in enterprise information systems. Prior to VMware, Andrea worked for several enterprise software companies, namely BEA,Macromedia/Adobe, Oracle and TIBCO. Andrea has an MBA from Columbia University and has been an advisor to the board of Xis Inc (acquired by Silicon Valley Bank) and other small start-ups. Ben Matheson Senior Director Global Partner Marketing and Campaigns Ben leads the team responsible for VMware’s global marketing campaigns as well as global channel and alliance partner marketing activities including partners such as AMD, Cisco, Dell, EMC, HP, IBM, Intel, Netapp, SAP and Symantec. Ben has been at VMware since March, 2006 working in a variety of product management and marketing leadership roles. Prior to VMware, Ben was at Microsoft for ten years where most recently he directed product management and marketing for their management products including System Center Data protection Manager, System Management Server, Windows Server Update Services, System Center Virtual Machine Manager and a variety of other management products. Bogomil Balkansky VP, Product Marketing, Server Business Unit Bogomil leads the product marketing team for VMware’s market leading datacenter virtualization product portfolio, including the vSphere and vCenter product lines.