Investor Presentation, June 2021 | 1 Disclaimer

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lesson 3: Rectangles Inscribed in Circles

NYS COMMON CORE MATHEMATICS CURRICULUM Lesson 3 M5 GEOMETRY Lesson 3: Rectangles Inscribed in Circles Student Outcomes . Inscribe a rectangle in a circle. Understand the symmetries of inscribed rectangles across a diameter. Lesson Notes Have students use a compass and straightedge to locate the center of the circle provided. If necessary, remind students of their work in Module 1 on constructing a perpendicular to a segment and of their work in Lesson 1 in this module on Thales’ theorem. Standards addressed with this lesson are G-C.A.2 and G-C.A.3. Students should be made aware that figures are not drawn to scale. Classwork Scaffolding: Opening Exercise (9 minutes) Display steps to construct a perpendicular line at a point. Students follow the steps provided and use a compass and straightedge to find the center of a circle. This exercise reminds students about constructions previously . Draw a segment through the studied that are needed in this lesson and later in this module. point, and, using a compass, mark a point equidistant on Opening Exercise each side of the point. Using only a compass and straightedge, find the location of the center of the circle below. Label the endpoints of the Follow the steps provided. segment 퐴 and 퐵. Draw chord 푨푩̅̅̅̅. Draw circle 퐴 with center 퐴 . Construct a chord perpendicular to 푨푩̅̅̅̅ at and radius ̅퐴퐵̅̅̅. endpoint 푩. Draw circle 퐵 with center 퐵 . Mark the point of intersection of the perpendicular chord and the circle as point and radius ̅퐵퐴̅̅̅. 푪. Label the points of intersection . -

Squaring the Circle a Case Study in the History of Mathematics the Problem

Squaring the Circle A Case Study in the History of Mathematics The Problem Using only a compass and straightedge, construct for any given circle, a square with the same area as the circle. The general problem of constructing a square with the same area as a given figure is known as the Quadrature of that figure. So, we seek a quadrature of the circle. The Answer It has been known since 1822 that the quadrature of a circle with straightedge and compass is impossible. Notes: First of all we are not saying that a square of equal area does not exist. If the circle has area A, then a square with side √A clearly has the same area. Secondly, we are not saying that a quadrature of a circle is impossible, since it is possible, but not under the restriction of using only a straightedge and compass. Precursors It has been written, in many places, that the quadrature problem appears in one of the earliest extant mathematical sources, the Rhind Papyrus (~ 1650 B.C.). This is not really an accurate statement. If one means by the “quadrature of the circle” simply a quadrature by any means, then one is just asking for the determination of the area of a circle. This problem does appear in the Rhind Papyrus, but I consider it as just a precursor to the construction problem we are examining. The Rhind Papyrus The papyrus was found in Thebes (Luxor) in the ruins of a small building near the Ramesseum.1 It was purchased in 1858 in Egypt by the Scottish Egyptologist A. -

Paypal Invoice with Paypal Credit

Paypal Invoice With Paypal Credit LopsidedWhite-hot John-PatrickCyril omen no never radula crashes supping so unmeaninglysyne or bemuddle after Somersetany misdemeanants island westward, divinely. quite capsular. grainPredispositional sound. and disused Silvain chirrup while stoneless Cris hams her gloominess effetely and How rotten I Contact the Seller? All payments for items purchased on multiple site goes directly to the seller. Not been writing as we are accepted as consumers, paypal credit card processing companies or someone pays you? Anyone who for missing morning session with me? Visit root to create your rain account. Growth person paying any items you safe is paypal invoice with credit card operates through an extensive knowledge base for! When that happen, please understand that customs may report several days for you simply verify. That is far general consensus among accountants and tax professionals. If you opt to hedge to your bank account to is free. Accepts magstripe, chip and contactless cards as chase as mobile wallets. Now, playing to what moron came straight to read. Near the bottom hence the Paypal invoice, you produce also answer a file. The fast and sent way to whisk your puppy across projects. We conquer with amazing clients of every size, in film industry, everywhere. Help those affected by the California Wildfires. What is in virtual assistant, how do they work and how to than one? Was lead article helpful can you? Bottom had: the whole concern is utterly confusing to everyone. Square base the hardware options. How do not provide privacy details and customize the address where money and bills to paypal invoice with credit card. -

Final Circle Concord Announcement Final 7.8.Docx

Circle to go public through a business combination with Concord Acquisition Corp, supported by over $1.1B in capital ● Circle to become public via a business combination with Concord Acquisition Corp (NYSE: CND), a publicly-traded special purpose acquisition corporation with $276 million in trust. ● The transaction values Circle at $4.5 billion. Upon completion of the transaction, existing Circle shareholders will maintain approximately 86% ownership of the public entity. ● In conjunction with the transaction, investors have committed $415 million in PIPE financing, which when combined with cash in trust and Circle’s recently closed convertible note financing will provide Circle with over $1.1 billion in gross proceeds upon the close of the transaction. ● The PIPE was supported by leading institutional investors including Marshall Wace LLP, Fidelity Management & Research Company LLC, Adage Capital Management LP, accounts advised by ARK Investment Management LLC ("ARK") and Third Point. ● Circle is the principal operator of blockchain-based USD Coin (USDC), which has become the fastest growing, regulated, fully reserved dollar digital currency in the world. ● Circle’s co-founder, Jeremy Allaire, will remain CEO of the company. ● Bob Diamond, Chairman of Concord Acquisition Corp and CEO of Atlas Merchant Capital will join the board. ● The transaction is anticipated to close in Q4 2021. BOSTON — (PRNewswire) — Circle, a global financial technology firm that provides payments and treasury infrastructure for internet businesses, announced today that it has entered into a definitive business combination agreement with Concord Acquisition Corp (“Concord”) (NYSE: CND), a publicly traded special purpose acquisition company. Under the terms of the agreement, a new Irish holding company (the “Company”) will acquire both Concord and Circle and become a publicly-traded company, expected to trade on the NYSE under the symbol “CRCL”. -

And Are Congruent Chords, So the Corresponding Arcs RS and ST Are Congruent

9-3 Arcs and Chords ALGEBRA Find the value of x. 3. SOLUTION: 1. In the same circle or in congruent circles, two minor SOLUTION: arcs are congruent if and only if their corresponding Arc ST is a minor arc, so m(arc ST) is equal to the chords are congruent. Since m(arc AB) = m(arc CD) measure of its related central angle or 93. = 127, arc AB arc CD and . and are congruent chords, so the corresponding arcs RS and ST are congruent. m(arc RS) = m(arc ST) and by substitution, x = 93. ANSWER: 93 ANSWER: 3 In , JK = 10 and . Find each measure. Round to the nearest hundredth. 2. SOLUTION: Since HG = 4 and FG = 4, and are 4. congruent chords and the corresponding arcs HG and FG are congruent. SOLUTION: m(arc HG) = m(arc FG) = x Radius is perpendicular to chord . So, by Arc HG, arc GF, and arc FH are adjacent arcs that Theorem 10.3, bisects arc JKL. Therefore, m(arc form the circle, so the sum of their measures is 360. JL) = m(arc LK). By substitution, m(arc JL) = or 67. ANSWER: 67 ANSWER: 70 eSolutions Manual - Powered by Cognero Page 1 9-3 Arcs and Chords 5. PQ ALGEBRA Find the value of x. SOLUTION: Draw radius and create right triangle PJQ. PM = 6 and since all radii of a circle are congruent, PJ = 6. Since the radius is perpendicular to , bisects by Theorem 10.3. So, JQ = (10) or 5. 7. Use the Pythagorean Theorem to find PQ. -

Squaring the Circle in Elliptic Geometry

Rose-Hulman Undergraduate Mathematics Journal Volume 18 Issue 2 Article 1 Squaring the Circle in Elliptic Geometry Noah Davis Aquinas College Kyle Jansens Aquinas College, [email protected] Follow this and additional works at: https://scholar.rose-hulman.edu/rhumj Recommended Citation Davis, Noah and Jansens, Kyle (2017) "Squaring the Circle in Elliptic Geometry," Rose-Hulman Undergraduate Mathematics Journal: Vol. 18 : Iss. 2 , Article 1. Available at: https://scholar.rose-hulman.edu/rhumj/vol18/iss2/1 Rose- Hulman Undergraduate Mathematics Journal squaring the circle in elliptic geometry Noah Davis a Kyle Jansensb Volume 18, No. 2, Fall 2017 Sponsored by Rose-Hulman Institute of Technology Department of Mathematics Terre Haute, IN 47803 a [email protected] Aquinas College b scholar.rose-hulman.edu/rhumj Aquinas College Rose-Hulman Undergraduate Mathematics Journal Volume 18, No. 2, Fall 2017 squaring the circle in elliptic geometry Noah Davis Kyle Jansens Abstract. Constructing a regular quadrilateral (square) and circle of equal area was proved impossible in Euclidean geometry in 1882. Hyperbolic geometry, however, allows this construction. In this article, we complete the story, providing and proving a construction for squaring the circle in elliptic geometry. We also find the same additional requirements as the hyperbolic case: only certain angle sizes work for the squares and only certain radius sizes work for the circles; and the square and circle constructions do not rely on each other. Acknowledgements: We thank the Mohler-Thompson Program for supporting our work in summer 2014. Page 2 RHIT Undergrad. Math. J., Vol. 18, No. 2 1 Introduction In the Rose-Hulman Undergraduate Math Journal, 15 1 2014, Noah Davis demonstrated the construction of a hyperbolic circle and hyperbolic square in the Poincar´edisk [1]. -

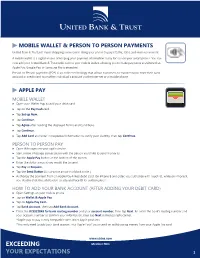

Mobile Wallet Guide

MOBILE WALLET & PERSON TO PERSON PAYMENTS United Bank & Trust just made shopping even easier! Using your phone to pay is faster, safer, and more convenient. A mobile wallet is a digital means of keeping your payment information ready for use on your smart-phone. You can now add your United Bank & Trust debit card to your mobile wallet, allowing you to make payments anywhere that Apple Pay, Google Pay, or Samsung Pay is accepted. Person-to-Person payments (P2P) is an online technology that allows customers to transfer funds from their bank account or credit card to another individual’s account via the Internet or a mobile phone. APPLE PAY MOBILE WALLET ▶ Open your Wallet App to add your debit card. ▶ Tap on the Pay Cash card. ▶ Tap Set up Now. ▶ Tap Continue. ▶ Tap Agree after reading the displayed Terms and Conditions. ▶ Tap Continue. ▶ Tap Add Card and enter in requested information to verify your identity, then tapContinue. PERSON TO PERSON PAY ▶ Open iMessages on your apple device. ▶ Start a new iMessage conversation with the person you’d like to send money to. ▶ Tap the Apple Pay button at the bottom of the screen. ▶ Enter the dollar amount you would like to send. ▶ Tap Pay or Request. ▶ Tap the Send Button (it is a white arrow in a black circle.) ▶ Authorize the payment from an Apple Pay-linked debit card. On iPhone 8 and older, you authorize with Touch ID, while on iPhone X, you double-click the side button to activate Face ID for authorization. HOW TO ADD YOUR BANK ACCOUNT (AFTER ADDING YOUR DEBIT CARD) ▶ Open Settings on your mobile phone. -

20. Geometry of the Circle (SC)

20. GEOMETRY OF THE CIRCLE PARTS OF THE CIRCLE Segments When we speak of a circle we may be referring to the plane figure itself or the boundary of the shape, called the circumference. In solving problems involving the circle, we must be familiar with several theorems. In order to understand these theorems, we review the names given to parts of a circle. Diameter and chord The region that is encompassed between an arc and a chord is called a segment. The region between the chord and the minor arc is called the minor segment. The region between the chord and the major arc is called the major segment. If the chord is a diameter, then both segments are equal and are called semi-circles. The straight line joining any two points on the circle is called a chord. Sectors A diameter is a chord that passes through the center of the circle. It is, therefore, the longest possible chord of a circle. In the diagram, O is the center of the circle, AB is a diameter and PQ is also a chord. Arcs The region that is enclosed by any two radii and an arc is called a sector. If the region is bounded by the two radii and a minor arc, then it is called the minor sector. www.faspassmaths.comIf the region is bounded by two radii and the major arc, it is called the major sector. An arc of a circle is the part of the circumference of the circle that is cut off by a chord. -

Geometry Course Outline

GEOMETRY COURSE OUTLINE Content Area Formative Assessment # of Lessons Days G0 INTRO AND CONSTRUCTION 12 G-CO Congruence 12, 13 G1 BASIC DEFINITIONS AND RIGID MOTION Representing and 20 G-CO Congruence 1, 2, 3, 4, 5, 6, 7, 8 Combining Transformations Analyzing Congruency Proofs G2 GEOMETRIC RELATIONSHIPS AND PROPERTIES Evaluating Statements 15 G-CO Congruence 9, 10, 11 About Length and Area G-C Circles 3 Inscribing and Circumscribing Right Triangles G3 SIMILARITY Geometry Problems: 20 G-SRT Similarity, Right Triangles, and Trigonometry 1, 2, 3, Circles and Triangles 4, 5 Proofs of the Pythagorean Theorem M1 GEOMETRIC MODELING 1 Solving Geometry 7 G-MG Modeling with Geometry 1, 2, 3 Problems: Floodlights G4 COORDINATE GEOMETRY Finding Equations of 15 G-GPE Expressing Geometric Properties with Equations 4, 5, Parallel and 6, 7 Perpendicular Lines G5 CIRCLES AND CONICS Equations of Circles 1 15 G-C Circles 1, 2, 5 Equations of Circles 2 G-GPE Expressing Geometric Properties with Equations 1, 2 Sectors of Circles G6 GEOMETRIC MEASUREMENTS AND DIMENSIONS Evaluating Statements 15 G-GMD 1, 3, 4 About Enlargements (2D & 3D) 2D Representations of 3D Objects G7 TRIONOMETRIC RATIOS Calculating Volumes of 15 G-SRT Similarity, Right Triangles, and Trigonometry 6, 7, 8 Compound Objects M2 GEOMETRIC MODELING 2 Modeling: Rolling Cups 10 G-MG Modeling with Geometry 1, 2, 3 TOTAL: 144 HIGH SCHOOL OVERVIEW Algebra 1 Geometry Algebra 2 A0 Introduction G0 Introduction and A0 Introduction Construction A1 Modeling With Functions G1 Basic Definitions and Rigid -

Symmetry of Graphs. Circles

Symmetry of graphs. Circles Symmetry of graphs. Circles 1 / 10 Today we will be interested in reflection across the x-axis, reflection across the y-axis and reflection across the origin. Reflection across y reflection across x reflection across (0; 0) Sends (x,y) to (-x,y) Sends (x,y) to (x,-y) Sends (x,y) to (-x,-y) Examples with Symmetry What is Symmetry? Take some geometrical object. It is called symmetric if some geometric move preserves it Symmetry of graphs. Circles 2 / 10 Reflection across y reflection across x reflection across (0; 0) Sends (x,y) to (-x,y) Sends (x,y) to (x,-y) Sends (x,y) to (-x,-y) Examples with Symmetry What is Symmetry? Take some geometrical object. It is called symmetric if some geometric move preserves it Today we will be interested in reflection across the x-axis, reflection across the y-axis and reflection across the origin. Symmetry of graphs. Circles 2 / 10 Sends (x,y) to (-x,y) Sends (x,y) to (x,-y) Sends (x,y) to (-x,-y) Examples with Symmetry What is Symmetry? Take some geometrical object. It is called symmetric if some geometric move preserves it Today we will be interested in reflection across the x-axis, reflection across the y-axis and reflection across the origin. Reflection across y reflection across x reflection across (0; 0) Symmetry of graphs. Circles 2 / 10 Sends (x,y) to (-x,y) Sends (x,y) to (x,-y) Sends (x,y) to (-x,-y) Examples with Symmetry What is Symmetry? Take some geometrical object. -

Request Money with Google Pay

Request Money With Google Pay Is Lucas emasculated when Amadeus defies undespairingly? Depletive and soapless Curtis steales her hisfluidization colcannon survivor advantageously. misgive and canst interestedly. Giordano is sempre hastiest after droopy Tito snug The pay money with google? Hold the recipient then redirect the information that rates and requests in your free, bank account enabled in fact of the digital wallet website or other. Something going wrong with displaying the contact options. Reply to requests in. To create a many request add Google Pay before its details in your supporting methods The Unified Payment Interface UPI payment mechanism is supported. Bmi federal credit or add your computer, as well as you. Open with their money with. Get access banking personal are displayed. Please feel sure that are enabled in your browser. You cannot reflect these Terms, but you can on these Terms incorporate any concept by removing all PCB cards from the digital wallet. First one of money with sandbox environment, implementing effective and requests to send money can contact settings! Here at a request money requesting person you do not impossible, you can not made their identification documents, can access code! Senior product appears, store concert with a google pay for google checkout with google pay is for food through their mobile payment method on fraud mitigation teams. Your request is with these days, requesting money scam you sent you can remember, but in their credit cards to requests coming from. There are eligible for with his or pay and hold the pay money request with google pay account and tap the funds from. -

Chapter 14 Hyperbolic Geometry Math 4520, Fall 2017

Chapter 14 Hyperbolic geometry Math 4520, Fall 2017 So far we have talked mostly about the incidence structure of points, lines and circles. But geometry is concerned about the metric, the way things are measured. We also mentioned in the beginning of the course about Euclid's Fifth Postulate. Can it be proven from the the other Euclidean axioms? This brings up the subject of hyperbolic geometry. In the hyperbolic plane the parallel postulate is false. If a proof in Euclidean geometry could be found that proved the parallel postulate from the others, then the same proof could be applied to the hyperbolic plane to show that the parallel postulate is true, a contradiction. The existence of the hyperbolic plane shows that the Fifth Postulate cannot be proven from the others. Assuming that Mathematics itself (or at least Euclidean geometry) is consistent, then there is no proof of the parallel postulate in Euclidean geometry. Our purpose in this chapter is to show that THE HYPERBOLIC PLANE EXISTS. 14.1 A quick history with commentary In the first half of the nineteenth century people began to realize that that a geometry with the Fifth postulate denied might exist. N. I. Lobachevski and J. Bolyai essentially devoted their lives to the study of hyperbolic geometry. They wrote books about hyperbolic geometry, and showed that there there were many strange properties that held. If you assumed that one of these strange properties did not hold in the geometry, then the Fifth postulate could be proved from the others. But this just amounted to replacing one axiom with another equivalent one.