Diagnostic Report on the Bus Transport Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Robinsons Land Corporation RLC

The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. Robinsons Land Corporation RLC PSE Disclosure Form 17-11 - List of Stockholders Reference: Section 17.11 of the Revised Disclosure Rules Type of Securities Common Preferred - Others - Record Date of Apr 24, 2019 Stockholders' Meeting Date of Stockholders' May 29, 2019 Meeting Type of Stockholders' Meeting Annual (Annual or Special) Other Relevant Information Please find attached the list of stockholders of Robinsons Land Corporation (RLC) as of April 24, 2019, the record date set by the Board of Directors of RLC to determine the stockholders entitled to notice and to vote at the annual meeting of the stockholders of RLC to be held on May 29, 2019. Filed on behalf by: Name Rosalinda Rivera Designation Corporate Secretary Robinsons Land Corporation April 24, 2019 SH # SH NAME SH ADDRESS NATIONALITY TOTAL NO. OF SHARES PERCENTAGE 0000230766 A & A SECURITIES, INC. 1906 PACIFIC BANK BLDG. AYALA AVENUE, MAKATI CITY FILIPINO 4,000.00 0.00007701 0000230768 A. ANGEL S. TANJANGCO 542 ARQUIZA ST.,ERMITA, MANILA FILIPINO 38,500.00 0.00074126 0000230770 ABOITIZ JEBS EN BULK TRANSPORT CORPORATION CEBU CITY, PHILIPPINES FILIPINO 400.00 0.00000770 0000230771 ABRAHAM T. CO C/O PBU, RCBC 333 SEN GIL PUYAT AVE 1200 MAKATI, METRO MANILA FILIPINO 1,000.00 0.00001925 0000230772 ACRIS CORPORATION 5/F BENPRES BUILDING,MERALCO AVENUE, PASIG CITY FILIPINO 8,900.00 0.00017136 0000230774 ADELINA A. -

Westmont-Pharmaceuti

WESTMONT PHARMACEUTICALS INC., } IPC No. 14-2014-00061 Opposer, } Opposition to: } Appln. Serial No. 4-2013-00001758 } Date Filed: 18 February 2013 -versus- } TM: "ANGIMAX" } } } CATHAY YSS DISTRIBUTORS CO. INC., } Respondent- Applicant. } )(-------------------------------------------------------------------)( NOTICE OF DECISION OCHAVE & ESCALONA Counsel for the Opposer No. 66 United Street Mandaluyong City JIMENEZ GONZALES BELLO VALDEZ CALUYA & FERNANDEZ Counsel for Respondent-Applicant 5 th Floor, SOL Building 112 Amorsolo Street, Legaspi Village Makati City GREETINGS: Please be informed that Decision No. 2016 - ..J::Q_ dated February 18, 2016 (copy enclosed) was promulgated in the above entitled case. Taguig City, February 18, 2016. For the Director: ~o.~9' Atty. EDWIN DANILO A. DATll'l§; Director Ill Bureau of Legal Affairs Republic of the Philippines INTELLECTUAL PROPERTY OFFICE Intellectual Property Center # 28 Upper McKinley Road, McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634 Philippines ewww.ipophil.gov.ph T: +632-2386300 • F: +632-5539480 • [email protected] < • I l. WESTMONT PHARMACEUTICALS IPC No. 14-2014-00061 INC., Opposition to: Opposer, Appln. No. 4-2013-00001758 - versus - Date Filed: 18 February 2013 Trademark: "ANGIMAX" CATHAY YSS DISTRIBUTORS CO. INC., Respondent-Applicant. Decision No. 2016 - ..S'O x --------------------------------------------- x DECISION WESTMONT PHARMACEUTICALS INC. ("Opposer"), 1 filed an oppos1tion to Trademark Application Serial No. 4-2013-00001758. The application, filed by CATHAY YSS DISTRIBUTORS 2 3 CO. INC. ("Respondent-Applicant") , covers the mark "ANGIMAX" for use on goods under class 05 namely: pharmaceutical preparations namely tablet for treatment for ischaemic heart disease, angina pectoris, sequelae of infraction. The Opposer alleges the following among other things: "7. The mark 'ANGIMAX' filed by Respondent-Applicant so resembles the trademark 'AMPIMAX' owned by Opposer and duly registered with the IPO prior to the publication for opposition of the mark 'ANG IMAX'. -

Impact of the Global Financial and Economic Crisis on the Philippines Josef T

Philippine Institute for Development Studies Surian sa mga Pag-aaral Pangkaunlaran ng Pilipinas Impact of the Global Financial and Economic Crisis on the Philippines Josef T. Yap, Celia M. Reyes, and Janet S. Cuenca DISCUSSION PAPER SERIES NO. 2009-30 The PIDS Discussion Paper Series constitutes studies that are preliminary and subject to further revisions. They are be- ing circulated in a limited number of cop- ies only for purposes of soliciting com- ments and suggestions for further refine- ments. The studies under the Series are unedited and unreviewed. The views and opinions expressed are those of the author(s) and do not neces- sarily reflect those of the Institute. Not for quotation without permission from the author(s) and the Institute. October 2009 For comments, suggestions or further inquiries please contact: The Research Information Staff, Philippine Institute for Development Studies 5th Floor, NEDA sa Makati Building, 106 Amorsolo Street, Legaspi Village, Makati City, Philippines Tel Nos: (63-2) 8942584 and 8935705; Fax No: (63-2) 8939589; E-mail: [email protected] Or visit our website at http://www.pids.gov.ph Impact of the Global Financial and Economic Crisis on the Philippines Paper Prepared for the United Nations Development Programme September 26, 2009 Josef T. Yap, Celia M. Reyes, and Janet S. Cuenca∗ ∗ President, Senior Research Fellow, and Supervising Research Specialist, respectively, Philippine Institute for Development Studies (PIDS). Table of Contents Part I Introduction 1 Objectives 1 Overview of the Philippine -

Consular Section

CONSULAR SECTION British Embassy Manila 120 Upper McKinley Road, McKinley Hill, Taguig City 1634 Tel: +63 2 858 2200 / Fax: +63 2 858 2342 Email: [email protected] / Website: www.gov.uk/world/philippines LEGAL PRACTITIONERS IN THE PHILIPPINES July 2014 (All correspond in English) This list of Lawyers is provided by the British Embassy Manila for the convenience of enquirers. Neither the British Government nor any official of the Embassy take responsibility for competence or probity of any firm/advocate on this list or for the consequence of any legal action initiated or advice given. LAW FIRM CONTACT DETAILS SPECIALISATION METRO MANILA ORTEGA, DEL CASTILLO, 5th & 6th Floors, Alpap I Building (Honorary Legal Advisers to the British BACORRO, ODULIO, 140 L.P. Leviste Street (Alfaro) Salcedo Vill., Embassy) CALMA & CARBONELL Makati City 1227 General Practise, Foreign Investments, Tel: 00632.818 2321-25 Corporations, Patents, Trademarks, Fax: 00632.810.3153 / 750 2606 Copyrights and Technology, Transfers, Email: [email protected] Litigation, Taxation, Insurance, Securities, Website: www.ocbocc.com Labour Law, Admiralty Estates, and Trusts, Aviation, Immigration, Banking and Finance, Oil and Mining, Media Law. QUASHA, ANCHETA, 6th Floor, Don Pablo Building Corporate, Taxation, Commercial PENA & NOLASCO 114 Amorsolo Street, Transactions, Investments, Insurance, Banking Legaspi Village, Makati City 1229 and Financial Services, Family Law, Contracts, Tel: 00632.892.3011 Intellectual Property, Labor and Employment, Fax: 00632.817.6423 Immigration, -

A Review of Build-Operate-Transfer for Infrastructure Development: Some Lessons for Policy Reform Gilberto M

Philippine Institute for Development Studies Surian sa mga Pag-aaral Pangkaunlaran ng Pilipinas A Review of Build-Operate-Transfer for Infrastructure Development: Some Lessons for Policy Reform Gilberto M. Llanto DISCUSSION PAPER SERIES NO. 2008-25 The PIDS Discussion Paper Series constitutes studies that are preliminary and subject to further revisions. They are be- ing circulated in a limited number of cop- ies only for purposes of soliciting com- ments and suggestions for further refine- ments. The studies under the Series are unedited and unreviewed. The views and opinions expressed are those of the author(s) and do not neces- sarily reflect those of the Institute. Not for quotation without permission from the author(s) and the Institute. September 2008 For comments, suggestions or further inquiries please contact: The Research Information Staff, Philippine Institute for Development Studies 5th Floor, NEDA sa Makati Building, 106 Amorsolo Street, Legaspi Village, Makati City, Philippines Tel Nos: (63-2) 8942584 and 8935705; Fax No: (63-2) 8939589; E-mail: [email protected] Or visit our website at http://www.pids.gov.ph A Review of Build-Operate-Transfer for Infrastructure Development: Some Lessons for Policy Reform1 Gilberto M. Llanto2 Philippine Institute for Development Studies Summary The Philippines has used the BOT law, as amended to motivate private sector provision of infrastructure. Using examples from selected BOT projects in the country, the paper pointed out key issues constraining the successful implementation of the BOT approach to infrastructure provision. It also indicated several factors that were instrumental in forging an effective public- private partnership in BOT projects. -

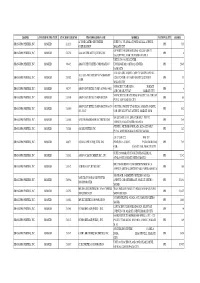

APC GROUP INC. Page : 1 LIST of STOCKHOLDERS Date : 8/7/2014 As of August 7, 2014 Broker

APC GROUP INC. Page : 1 LIST OF STOCKHOLDERS Date : 8/7/2014 As of August 7, 2014 Broker SHARES ISSUED SHARES & OUTSTANDING SUBSCRIBED NO. CTZN NAME ADDRESS RECEIVABLES AB001 PHILIPPINES A & A SECURITIES, INC. #1906 MAKATI BUILDING 60,000 45,000.00 #6776 AYALA AVENUE MAKATI, METRO MANILA AB059 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 20,000 15,000.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB060 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 10,000 7,500.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB061 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 10,000 7,500.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB062 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 10,000 7,500.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB063 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 10,000 7,500.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB064 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 20,000 15,000.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB065 PHILIPPINES AGJ SECURITIES CORP. 10/F TOWER ONE & 10,000 7,500.00 EXCHANGE PLAZA, AYALA TRIANGLE AYALA AVENUE, MAKATI CITY AB020 PHILIPPINES ALAKOR SECURITIES CORP. 9/F QUAD ALPHA CENTRUM 5,000 125 PIONEER STREET, MANDALUYONG CITY AB070 PHILIPPINES AMON SEC. CORP. A/C #002- 10/F PACIFIC STAR BLDG. 20,000 15,000.00 GIL PUYAT AVENUE EXT. COR. MAKATI AVE. MAKATI AB071 PHILIPPINES AMON SEC. CORP. A/C #004- 10/F PACIFIC STAR BLDG. 10,000 7,500.00 GIL PUYAT AVENUE EXT. -

Universal Robina Corporation URC

CR00573-2015 The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. All data contained herein are prepared and submitted by the disclosing party to the Exchange, and are disseminated solely for purposes of information. Any questions on the data contained herein should be addressed directly to the Corporate Information Officer of the disclosing party. Universal Robina Corporation URC PSE Disclosure Form 17-12 - List of Top 100 Stockholders Reference: Section 17.12 of the Revised Disclosure Rules Type of Securities Common Preferred N/A Others N/A For the period ended Dec 31, 2014 Description of the Disclosure Please see attached list of top 100 stockholders and PDTC Participants of Universal Robina Corporation as of December 31, 2014. Filed on behalf by: Name Rosalinda Rivera Designation Corporate Secretary COMPANY NAME : UNIVERSAL ROBINA CORPORATION Page 1 LIST OF TOP 100 STOCKHOLDERS As Of December 31, 2014 OUTSTANDING & OUTSTANDING & TOTAL PERCENTAGE ISSUED SHARES ISSUED SHARES HOLDINGS TO STOCKHOLDER'S NAME (FULLY PAID) (PARTIALLY PAID) (SUBSCRIBED) TOTAL NATIONALITY ADDRESS JG SUMMIT HOLDINGS INC. 1,215,223,061 0 1,215,223,061 54.552 FILIPINO 43/F ROBINSONS EQUITABLE TOWER ADB AVE.,COR.POVEDA ST. PCD NOMINEE CORPORATION (NON-FILIPINO) 720,573,425 0 720,573,425 32.347 OTHERS G/F MAKATI STOCK EXCHANGE BLDG 6767 AYALA AVE., MAKATI CITY PCD NOMINEE CORPORATION (FILIPINO) 233,178,167 0 233,178,167 10.468 FILIPINO G/F MSE BLDG. 6767 AYALA AVE., MAKATI CITY ELIZABETH Y. GOKONGWEI AND/OR JOHN GOKONGWEI JR. -

ERIA Study to Further Improve the ASEAN Economic Community Scorecard: the Philippines Rafaelita M

Philippine Institute for Development Studies Surian sa mga Pag-aaral Pangkaunlaran ng Pilipinas ERIA Study to Further Improve the ASEAN Economic Community Scorecard: the Philippines Rafaelita M. Aldaba et al. DISCUSSION PAPER SERIES NO. 2010-24 The PIDS Discussion Paper Series constitutes studies that are preliminary and subject to further revisions. They are be- ing circulated in a limited number of cop- ies only for purposes of soliciting com- ments and suggestions for further refine- ments. The studies under the Series are unedited and unreviewed. The views and opinions expressed are those of the author(s) and do not neces- sarily reflect those of the Institute. Not for quotation without permission from the author(s) and the Institute. October 2010 For comments, suggestions or further inquiries please contact: The Research Information Staff, Philippine Institute for Development Studies 5th Floor, NEDA sa Makati Building, 106 Amorsolo Street, Legaspi Village, Makati City, Philippines Tel Nos: (63-2) 8942584 and 8935705; Fax No: (63-2) 8939589; E-mail: [email protected] Or visit our website at http://www.pids.gov.ph ERIA Study to Further Improve the ASEAN Economic Community Scorecard: the Philippines Lead Authors Rafaelita M. Aldaba, Dorothea C. Lazaro, Gilberto M. Llanto and Erlinda M. Medalla Secondary Authors Josef T. Yap, Francis Mark A. Quimba, Melalyn C. Mantaring and Larraine C. Zafe Final Draft 13 September 2010 Table of Contents Acknowledgement v List of Acronyms vi List of Tables, Figures and Boxes x Chapter 1 The Philippine Development Experience 1 1.1. The Openness Model of Development 1 1.2. -

JEEP Bus Time Schedule & Line Route

JEEP bus time schedule & line map JEEP Ayala - Mantrade via Pasong Tamo View In Website Mode The JEEP bus line (Ayala - Mantrade via Pasong Tamo) has 2 routes. For regular weekdays, their operation hours are: (1) Paseo De Roxas / Ayala Avenue Intersection, Makati City, Manila →Sabio St / Chino Roces Ave Intersection, Makati City, Manila: 12:00 AM - 11:00 PM (2) Sabio St / Chino Roces Ave Intersection, Makati City, Manila →Paseo De Roxas / Ayala Avenue Intersection, Makati City, Manila: 12:00 AM - 11:00 PM Use the Moovit App to ƒnd the closest JEEP bus station near you and ƒnd out when is the next JEEP bus arriving. Direction: Paseo De Roxas / Ayala Avenue JEEP bus Time Schedule Intersection, Makati City, Manila →Sabio St / Paseo De Roxas / Ayala Avenue Intersection, Makati Chino Roces Ave Intersection, Makati City, Manila City, Manila →Sabio St / Chino Roces Ave Intersection, Makati City, Manila Route Timetable: 11 stops VIEW LINE SCHEDULE Sunday 12:00 AM - 10:00 PM Monday 12:00 AM - 11:00 PM Paseo De Roxas / Ayala Avenue Intersection, Makati City, Manila Tuesday 12:00 AM - 11:00 PM 6768 Ayala Avenue, Philippines Wednesday 12:00 AM - 11:00 PM Makati Ave / Ayala Avenue Intersection, Makati City, Manila Thursday 12:00 AM - 11:00 PM 6752 Ayala Avenue, Philippines Friday 12:00 AM - 11:00 PM Makati Ave / North Dr Intersection, Makati City, Saturday 12:00 AM - 10:00 PM Manila Drop Off, Philippines Makati Ave / A. Arnaiz Ave, Makati City, Manila 926 Antonio S. Arnaiz Avenue, Philippines JEEP bus Info Direction: Paseo De Roxas / Ayala Avenue Paseo De Roxas / Pasay Road Intersection, Intersection, Makati City, Manila →Sabio St / Chino Makati City, Manila Roces Ave Intersection, Makati City, Manila Paseo de Roxas, Philippines Stops: 11 Trip Duration: 17 min A. -

Shang List 052316

ISSUER STOCKHOLDER TYPE STOCKHOLDER NO STOCKHOLDER NAME ADDRESS NATIONALITY SHARES A. T. DE CASTRO SECURITIES SUITE 701, 7/F AYALA TOWER AYALA AVENUE, SHANG PROPERTIES, INC. BROKER 211123 PH 535 CORPORATION MAKATI CITY G/F FORTUNE LIFE BUILDING 162 LEGASPI ST., SHANG PROPERTIES, INC. BROKER 211238 AAA SOUTHEAST EQUITIES, INC. PH 8 LEGASPI VILL. MAKATI, METRO MANILA UNIT E 2904-A PSE CENTER SHANG PROPERTIES, INC. BROKER 80442 ABACUS SECURITIES CORPORATION EXCHANGE RD., ORTIGAS CENTER PH 2,049 PASIG CITY ALL ASIA SEC. MGMT. CORP. 7/F SYCIP-LAW ALL ALL ASIA SECURITIES MANAGEMENT SHANG PROPERTIES, INC. BROKER 211322 ASIA CENTER 105 PASEO DE ROXAS STREET PH 35 CORP. MAKATI CITY 5/F PACIFIC STAR BLDG., MAKATI SHANG PROPERTIES, INC. BROKER 80257 AMON SECURITIES CORP. A/C#001-54011 PH 6 AVE COR GIL PUYAT MAKATI CITY 5/F PACIFIC STAR BUILDING MAKATI AVE. COR. GIL SHANG PROPERTIES, INC. BROKER 211303 AMON SECURITIES CORPORATION PH 98 PUYAT AVE MAKATI CITY AMON SECURITIES CORPORATION A/C # 10TH FLR., PACIFIC STAR BLDG. MAKATI AVENUE, SHANG PROPERTIES, INC. BROKER 211050 PH 982 001-33247 COR. SEN GIL PUYAT AVENUE, MAKATI, M. M. 3/F ASIAN PLAZA 1, SENATOR GIL J. PUYAT SHANG PROPERTIES, INC. BROKER 211014 ANSCOR HAGEDORN SECURITIES INC PH 285 AVENUE, MAKATI METRO MANILA 9TH FLR., METROBANK PLAZA BLDG SEN GIL J. SHANG PROPERTIES, INC. BROKER 211244 ASI SECURITIES, INC. PH 142 PUYAT AVENUE MAKATI, METRO MANILA A/C-CAXN1222 RM. 207 SHANG PROPERTIES, INC. BROKER 80673 ASIAN CAPITAL EQUITIES, INC. PENINSULA COURT, PASEO DE ROXAS PH 785 COR., MAKATI AVE., MAKATI CITY SUITE 210 MAKATI STOCK EXCHANGE BLDG., SHANG PROPERTIES, INC. -

JEEP Bus Time Schedule & Line Route

JEEP bus time schedule & line map JEEP Libertad - Pasay Rd. View In Website Mode The JEEP bus line (Libertad - Pasay Rd.) has 2 routes. For regular weekdays, their operation hours are: (1) Antonio Arnaiz Ave / P.Zamora Intersection, Manila →South Dr / A. Arnaiz Ave Intersection, Makati City, Manila: 12:00 AM - 11:00 PM (2) South Dr / A. Arnaiz Ave Intersection, Makati City, Manila →Antonio Arnaiz Ave / P.Zamora Intersection, Manila: 12:00 AM - 11:00 PM Use the Moovit App to ƒnd the closest JEEP bus station near you and ƒnd out when is the next JEEP bus arriving. Direction: Antonio Arnaiz Ave / P.Zamora JEEP bus Time Schedule Intersection, Manila →South Dr / A. Arnaiz Ave Antonio Arnaiz Ave / P.Zamora Intersection, Intersection, Makati City, Manila Manila →South Dr / A. Arnaiz Ave Intersection, Makati City, Manila Route Timetable: 19 stops VIEW LINE SCHEDULE Sunday 12:00 AM - 10:00 PM Monday 12:00 AM - 11:00 PM Antonio Arnaiz Ave / P.Zamora Intersection, Manila Tuesday 12:00 AM - 11:00 PM Cementina, Philippines Wednesday 12:00 AM - 11:00 PM A. Arnaiz Ave / Hidalgo, Lungsod Ng Pasay, Manila Thursday 12:00 AM - 11:00 PM Friday 12:00 AM - 11:00 PM A. Arnaiz Ave / Batangas, Manila Mayor, Philippines Saturday 12:00 AM - 10:00 PM A. Arnaiz Ave, Makati City Skyway, Makati City, Manila A. Apolinario, Philippines JEEP bus Info Direction: Antonio Arnaiz Ave / P.Zamora Skyway, Makati City, Manila Intersection, Manila →South Dr / A. Arnaiz Ave Intersection, Makati City, Manila A.Apolinario / General Luna Intersection, Makati Stops: 19 City, Manila Trip Duration: 26 min Line Summary: Antonio Arnaiz Ave / P.Zamora A.Apolinario / Gen.P.Garcia Intersection, Makati Intersection, Manila, A. -

At Your Service

AT YOUR SERVICE Owned and Operated by Worldhotel Makati, Inc. [email protected] | www.imhotel.com WHY BOOK DIRECT? Dear Valued Guest, Mabuhay and welcome to I’M Hotel, a place where everything is all about you. I would like to personally welcome you to your address which is the epitome of affordable urban luxury in the heart of Makati. We are very excited that you have chosen to stay with us and will do our best to curate remarkable memories of your stay here. The next pages will allow you to explore more details of the hotel and its facilities. We also invite you to explore I’M Onsen Spa for a serene and calming atmosphere to nourish the mind, body, and spirit. This is the largest urban spa in the country, rated number 1 across Manila and Luzon for the 2nd year running. As HOTEL an exclusive treat to our in-house guests, you will get to avail a discount on our list prices when you visit our spa, quoting your name and room number. FACT SHEET I’M Hotel also caters to a well-travelled and discerning palate. The Common Good Food Playground features nine (9) different concepts under one roof, offering the best of various international cuisines. Antidote, located on our roof deck is the very first jellyfish bar in the country with a 360-degree view. Watch the ambient glow of these creatures accentuate the stunning cityscape with a bespoke cocktail in hand. Last but not least, Mermaid Pool Bar, located by our iconic acrylic-bottomed pool, dishes up exciting bar nibbles inspired from various corners of the world.