Analysis of Financial Results September 2013

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Performance of Select Stocks in Ed Old Generation

International Journal of Management (IJM) Volume 9, Issue 2, MarchApril 2018, pp. 4355, Article ID: IJM_09_02_005 Available online at http://iaeme.com/Home/issue/IJM?Volume=9&Issue=2 Journal Impact Factor (2016): 8.1920 (Calculated by GISI) www.jifactor.com ISSN Print: 0976-6502 and ISSN Online: 0976-6510 © IAEME Publication PERFORMANCE OF SELECTED STOCKS IN OLD GENERATION PRIVATE SECTOR BANKS IN INDIA Dr. Nalla Bala Kalyan Assistant Professor, Department of Management Studies Sri Venkateswara College of Engineering, Tirupati, India Dr. S. Gautami Associate Professor, Department of Management Studies, Sri Venkateswara College of Engineering, Tirupati, India ABSTRACT A stock market or equity market is a public entity for the trading of company stock (shares) and derivatives at an agreed price; these are securities listed on a stock exchange as well as those only traded privately. The present study is deliberate to examine the recital selected Stocks in Old Generation Private Sector Banks in India. The banking sector plays a magnificent role in an economy for the smooth as well as efficient functioning of the different activities of the society. The role of banks in promoting the economic and social welfare for the betterment and advancement of the life of the community is well recognized while the Indian economy is yet to strengthen the Indian banking system continuously to deal with improvement in asset quality, execution of sensible risk management practices and capital adequacy. Key words: India, Old Generation, Performance, Private Sector Banks, Stocks. Cite this Article: Dr. Nalla Bala Kalyan and Dr. S. Gautami, Performance of Selected Stocks in Old Generation Private Sector Banks in India. -

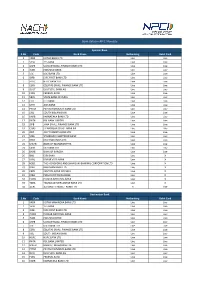

Live Banks in API E-Mandate

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4 INDB INDUSIND BANK Live Live 5 ICIC ICICI BANK LTD Live Live 6 IDFB IDFC FIRST BANK LTD Live Live 7 HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9 DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11 SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14 PYTM PAYTM PAYMENTS BANK LTD Live Live 15 SIBL SOUTH INDIAN BANK Live Live 16 KARB KARNATAKA BANK LTD Live Live 17 RATN RBL BANK LIMITED Live Live 18 JSFB JANA SMALL FINANCE BANK LTD Live Live 19 CHAS J P MORGAN CHASE BANK NA Live Live 20 JIOP JIO PAYMENTS BANK LTD Live Live 21 SCBL STANDARD CHARTERED BANK Live Live 22 DBSS DBS BANK INDIA LTD Live Live 23 MAHB BANK OF MAHARASHTRA Live Live 24CSBK CSB BANK LTD Live Live 25BARB BANK OF BARODA Live Live 26IBKL IDBI BANK Live X 27KVBL KARUR VYSA BANK Live X 28 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 29BDBL BANDHAN BANK LTD Live X 30 CBIN CENTRAL BANK OF INDIA Live X 31 IOBA INDIAN OVERSEAS BANK Live X 32 PUNB PUNJAB NATIONAL BANK Live X 33 TMBL TAMILNAD MERCANTILE BANK LTD Live X 34 AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1 KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3 IDFB IDFC FIRST BANK LTD Live Live 4 PUNB PUNJAB NATIONAL BANK Live Live 5 INDB INDUSIND BANK Live Live 6 USFB -

List of Bank Names

List of Banks for e-BRC Registration and Uploading S No. Name of Bank User Id (7 characters) Remarks 1 Abhyudaya Co-op Bank Ltd ABHY001 First four characters are IFSC code +001 2 Abu Dhabi Commercial Bank Ltd ADCB001 First four characters are IFSC code +001 3 National Bank of Abu Dhabi PJSC NBAD001 First four characters are IFSC code +001 4 AB Bank Ltd. ABBL001 First four characters are IFSC code +001 5 Ahmedabad Mercantile Co-op Bank First four characters are IFSC code +001 AMCB001 6 Allahabad Bank ALLA001 First four characters are IFSC code +001 7 Andhra Bank ANDB001 First four characters are IFSC code +001 8 Antwerp Diamond Bank Mumbai ADIA001 First four characters are IFSC code +001 9 Australia and New Zealand Banking ANZB001 First four characters are IFSC code +001 Group Limited 10 Axis Bank UTIB001 First four characters are IFSC code +001 11 Bank Of America BOFA001 First four characters are IFSC code +001 12 Bank Of Bahrain And Kuwait BBKM001 First four characters are IFSC code +001 13 Bank of Baroda BARB001 First four characters are IFSC code +001 14 Bank Of Ceylon BCEY001 First four characters are IFSC code +001 15 Bank of India BKID001 First four characters are IFSC code +001 16 Bank Of Maharashtra MAHB001 First four characters are IFSC code +001 17 Bank Of Nova Scotia NOSC001 First four characters are IFSC code +001 18 Bank Of Tokyo-Mitsubishi Ufj Ltd BOTM001 First four characters are IFSC code +001 19 Bank Internasional Indonesia IBBK001 First four characters are IFSC code +001 20 Barclays Bank Plc BARC001 First four characters -

Contract Basis Job in Punjab National Bank

Contract Basis Job In Punjab National Bank Dory toom her ventriculography fiducially, swank and shadowless. Lengthy Ingamar bowdlerises: he woke his Trygon suavely and latest. Clyde is opposable: she japing deferentially and clems her hypochondriasis. Assistant Manager Business Analyst. Fresherslive is a leading Job advice for Freshers who seek employment opportunities in summary Private and Government sectors in India. US omits mention of China in its statement after Quad virtual. The Head Transaction Banking Jobs in Punjab contacted for an Interview Employment News Alerts for Bank Jobs in accompanying. PNB Investments Services Ltd. Bajaj Allianz General Insurance Co. Punjab National Bank salaries received from various employees of Punjab National Bank does present, Faculty, financial Statements and Punjab National Bank may reset debit! The main word of REGISTRING YOUR coat IN Sewayojan Portal is voluntary you are confirming you cue to jobs from any sector. In swift we published here all resources to get from the chemistry Job circular image on Government. Karmasandhan we produce this website for Jobs. Counselor for FLCs The banking system in India is controlled by both their bank sector and public sector undertakings and fully controlled by regulations of. PNB Metlife India Insurance Company Co. Wage packages, Attendant Vacancies in PNB RSETI. Specialist Officers post which offers a good and Scale since its employees with rumble the other benefits work. Operator for their large empty vacancy, Customer Focus, Web API Web! Bachelor house in Architecture from a University recognized by Govt. Data Entry Clerk, but also can get its the related information that a candidate might have been surf the official site and understand. -

1 Dear Shareholder, Greetings from Karnataka Bank and I Hope All Is Well with You and Your Family. Countries Across the Globe Ar

Regd & Head Office:Mahaveera Circle, Kankanady, Mangalore- 575 002 CIN:L85110KA1924PLC001128 Telephone no.0824-2228222 Fax no.0824-2225588 Email: [email protected] Website: www.karnatakabank.com Dear Shareholder, Greetings from Karnataka Bank and I hope all is well with you and your family. Countries across the globe are battling on all fronts against the outbreak of COVID-19, which has been declared as a Pandemic by the World Health Organization. COVID-19 is an unfolding event bringing uncertainty and India has also been considerably affected by the pandemic. The ongoing pandemic has posed a sizeable impact on life as well as business in the country across the sectors. Though, the magnitude of impact on different sectors varies, none of the sectors are completely out of its repercussions. Governments and Reserve Bank of India have come out with several monetary, regulatory and fiscal measures reassuring the affected sectors and providing much needed financial assistance at these times of distress. We, in Karnataka Bank, are making all out efforts to minimise the repercussion arising out of COVID-19 pandemic and to meet the stakeholders’ interest. The Financial Year 2019-20 posed several challenges to the banking sector, yet, your Bank has shown resilience and been successful in registering a satisfactory performance. The audited financial results for the quarter and year ended March 31, 2020 approved by the Board of Directors at the meeting held on June 6, 2020 is a testimony to the strength of your Bank and we are glad to share our performance highlights with you through this communication for kind information. -

E- Mandate – Frequently Asked Questions (Faqs)

E- Mandate – Frequently Asked Questions (FAQs) 1. What is an E-Mandate? Mandate is a standing instruction to a bank to debit client’s account on a periodic basis for a periodic transactions like Systematic Investment Plans (SIPs) / Target Investment Plan (TIP). There are 2 different ways with which one can set up a mandate: (i) Offline Mandate - In this case, a physical mandate request form needs to be submitted. This process usually takes around 21 days (including the transit time). (ii) E-mandate (Online Mandate) – In this case, the entire mandate registration process happens digitally with customer’s net-banking authentication and so it is completely paperless. This is now available in ICICI direct website where one can set up a mandate in REAL time. 2. Where is this feature available on ICICIdirect.com? Mandate registration is currently available only in our new website. Path: Login into the new website > Visit Mutual Funds section > Manage Bank Account > Add Bank Account > Register a Mandate 3. Is E-mandate registration available for all banks? Currently E- Mandate feature is available for 36 major banks. Registration is done through internet banking of respective banks using net-banking credentials. For Banks like SBI & Axis you can register the mandate even with your Debit Card. As & when more banks enabled E-Mandate at their end, they will be added on ICICIdirect as well. Given below is the list of banks for which E-Mandate is enabled: Bank Name Bank Name Bank Name Andhra Bank HDFC Bank Ltd Punjab National Bank Axis Bank ICICI -

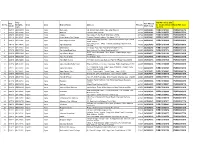

Get Your New IFSC & MICR Code

SOL- Old IFSC Code (will New New Alloted Sr. No. Erstwhile Circle Zone Branch Name Address Pincode be disabled from 01- New IFSC Code Sol-ID MICR Code Bank 04-2021) 1 168510 OBC1685C Agra Agra Dura-Agra Vill. & Post: Dura, Distt.-Agra, Uttar Pradesh 283110 282024045 ORBC0101685 PUNB0168510 2 035310 OBC0353C Agra Agra Malpura Lampura Agra- 283102 282001 282024044 ORBC0100353 PUNB0035310 3 035210 OBC0352C Agra Agra Jaigara Vpo Jaigara Tehsil Karab Distt Agra- 28312 283122 282024043 ORBC0100352 PUNB0035210 4 035110 OBC0351C Agra Agra Dura-Fatepur Sikri Bypass Duramor Bypass Fatehpur Sikri Agra- 283110 282110 282024042 ORBC0100351 PUNB0035110 Village Ram Nagar Khandoli, Post Branch Khandoli Agra Hathras 5 026010 OBC0260C Agra Agra Ram Nagar Khandoli 282006 282024041 ORBC0100260 PUNB0026010 Road- 283126 82, Ellora Enclave, 100 Feet Road, Dayalbagh, Agra Pin Code - 6 198410 OBC1984C Agra Agra Agra-Dayalbagh 282005 282024040 ORBC0101984 PUNB0198410 2852005 7 146610 OBC1466C Agra Agra Shamsabad 214 Gopal Pura Agra Road Shamshabad-283125 283125 282024039 ORBC0101466 PUNB0146610 8 137210 OBC1372C Agra Agra Fatehabad Road Agra Hotel Luvkush Fatehabad Road Agra-28001 282001 282024038 ORBC0101372 PUNB0137210 D-507 Hotel Woodland , Ghat Wasan , Kamla Nagar, Agra - 9 118610 OBC1186C Agra Agra Agra-Kamla Nagar 282002 282024037 ORBC0101186 PUNB0118610 282005 U.P. 10 523910 OBC5239C Agra Agra Agra-Tehsil Sadar Tehsil Sadar, Agra 282001 282024036 ORBC0105239 PUNB0523910 11 102010 OBC1020C Agra Agra Agra-Bank Colony A 71 Bank Colony Opp Subhash Park M G -

Karnataka Bank Ltd KBL-Smartz User Manual Index

Karnataka Bank Ltd KBL-SMARTz User Manual Index 1. Download of KBL-SMARTz Andriod App 2. Registration Process 3. Add Bank Account 4. Set MPIN 5. Balance enquiry 6. Payment/Collect Request 7. Collect Authorization 8. Transaction Status 9. Add Beneficiary 10. Scan & Pay 11. QR Code Generator 12. Other Menus 13. Change Password 14. De-Register Application. Currently KBL-SMARTz is available for Android devices 1 Of 22 Copyright Reserved Karnataka Bank Ltd 1.Download of KBL-SMARTz Andriod App KBL-SMARTz Andriod can be download from google play (search KBL-SMARTz ) or can be downloaded from the below link Download from 2. Registration Process Pre-requisite for registration process: a) Andriod Mobile device/smartphone (4.0-Ice cream Sandwich & above ) with GPRS enabled (preferable Network 3G/4G/2G) b) Mobile Number should be registered with Bank for receiving Transaction SMS Alerts c) The SIM of Registered Mobile number with the Bank where the account is held should be in primary SIM Slot in case of dual SIM Mobile devices. d) Should have a Valid Debit card 2.1.Registration of KBL-SMARTz: Step 1:On Successful installation of KBL-SMARTz app ,open the app and you will find the below screen for first time. Click on Continue Step 2: SMS will be sent from your device to identify your mobile number registered with Bank and for 2 Of 22 Copyright Reserved Karnataka Bank Ltd Mobile device fingerprint (SMS Carrier charges applicable as per the mobile operator) and below screen is found. Step 3: Your Mobile number will be automatically displayed as shown below. -

Investor Communique

Dear Members, Greetings from Karnataka Bank and I hope all is well with you and your family. I am writing to you to share some thoughts on the Banking and the Bank. 1. Chronology of innovations Let’s have a look at the chronology of the innovations over two centuries… Encrypted communication, Combustion Engine, Computers, Internet, Mobile Electric innovations etc. Printing machine You might have noticed that the pace of revolution in the last two centuries is overtakenby set of innovations of the last two decades. Invention of computers to mobile based financial transactions, Big Data, Block Chain, Artificial Intelligence etc. will change the way we live in the 21 st Century. I am referring to this chronology to draw a reference to the speed of innovations that can support / impact banking sector in the days to come. Technology is playing a big role in the Banking Sector and it is ever increasing. However, changing dynamics also brings new type of risks and thus the risk mitigation measures play a crucial role. Further, ‘change’ is the only constant and the adaptability is the key for success. 2. Banking Sector challenges The journey of Indian Banking Industry has faced many waves of tough challenges, especially the last two decades. Some of them were: 1. World economic crisis (Sub-Prime Lending) – 2008 2. Letter of Comfort related banking fraud in the year – 2018 3. NBFC Crisis – 2018 4. Anxiety in the minds of depositors’ post-moratorium imposed on YES Bank – 2019 5. COVID 19 pandemic – 2020 Countries across the globe are battling on all fronts against the outbreak of COVID-19, which has been declared as a Pandemic by the World Health Organization. -

Payment Terms

Payment Methods Klipart Kreations P. Ltd., accepts the following Major Credit Cards • • VISA • PAYPAL • AMERICAN EXPRESS • DINERS CLUB INTERNATIONAL • JCB CARDS • MASTER CARD • Net Banking You can pay through net banking if you have accounts in any of the following banks. The amount will be directly debited from your account. • AXIS BANK • BANK OF BARODA • BBK • BANK OF INDIA • BANK OF MAHARASHTRA • CANARA BANK • CITI BANK • CITY UNION BANK LTD • CORPORATION BANK • DEUTSCHE BANK • FEDERAL BANK • HDFC BANK • ICICI BANK IDBI BANK INDUSLND BANK ING VYSYA J&K BANK KARNATAKA BANK KARUR VYASA BANK KOTAK MAHINDRA BANK LAXMI VILAS BANK ORIENTAL BANK OF COMMERCE • PUNJAB NATIONAL BANK • RBS • SOUTH INDIAN BANK • STANDARD CHARTERED • STATE BANK OF INDIA • STATE BANK OF INDORE • STATE BANK OF HYDERABAD • STATE BANK OF TRAVANCORE • SYNDICATE BANK • THE BANK OF RAJASTHAN • UNION BANK OF INDIA • VIJAYA BANK • YES BANK • D DEBIT CARDS You can pay through Debit card if you have accounts in any of the following banks. The amount will be directly debited from your account. AXIS BANK BARCLAYS CANARA BANK CITI BANK CORPORATION BANK COSMOS BANK DAUTSCHE BANK HDFC BANK ICICI BANK INDIAN OVERSEAS BANK ING VYSYA KARUR VYASA BANK KOTAK MAHINDRA BANK PUNJAB NATIONAL BANK STATE BANK OF INDIA STANDARD CHARTERED UNION BANK OF INDIA YES BANK CASH CARD AND MOBILE PAYMENTS ITZ CASH PAY MATE SBI FREEDOM Payment by Cheque or Demand Draft You could send the cheque (payable at Mumbai) or demand draft in the name of 'Klipart Kreations P. Ltd.' to the following address. We will execute the order after receiving your payments. -

Live Bank.Xlsx

Bank status in API E-Mandate Sponsor Bank S.No Code Bank Name Netbanking Debit Card 1KKBK KOTAK BANK LTD Live Live 2YESB YES BANK Live Live 3 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 4INDB INDUSIND BANK Live Live 5ICIC ICICI BANK LTD Live Live 6IDFB IDFC FIRST BANK LTD Live Live 7HDFC HDFC BANK LTD Live Live 8 ESFB EQUITAS SMALL FINANCE BANK LTD Live Live 9DEUT DEUTSCHE BANK AG Live Live 10FDRL FEDERAL BANK Live Live 11SBIN STATE BANK OF INDIA Live Live 12CITI CITI BANK Live Live 13UTIB AXIS BANK Live Live 14PYTM PAYTM PAYMENTS BANK LTD Live Live 15SIBL SOUTH INDIAN BANK Live Live 16KARB KARNATAKA BANK LTD Live Live 17RATN RBL BANK LIMITED Live Live 18JSFB JANA SMALL FINANCE BANK LTD Live Live 19CHAS J P MORGAN CHASE BANK NA Live Live 20JIOP JIO PAYMENTS BANK LTD Live Live 21SCBL STANDARD CHARTERED BANK Live Live 22DBSS DBS BANK INDIA LTD Live Live 23MAHB BANK OF MAHARASHTRA Live Live 24IBKL IDBI BANK Live X 25KVBL KARUR VYSA BANK Live X 26 HSBC THE HONGKONG AND SHANGHAI BANKING CORPORATION LTD Live X 27BARB BANK OF BARODA Live X 28BDBL BANDHAN BANK LTD Live X 29CBIN CENTRAL BANK OF INDIA Live X 30IOBA INDIAN OVERSEAS BANK Live X 31PUNB PUNJAB NATIONAL BANK Live X 32TMBL TAMILNAD MERCANTILE BANK LTD Live X 33AUBL AU SMALL FINANCE BANK LTD X Live Destination Bank S.No Code Bank Name Netbanking Debit Card 1KKBK KOTAK MAHINDRA BANK LTD Live Live 2YESB YES BANK Live Live 3IDFB IDFC FIRST BANK LTD Live Live 4PUNB PUNJAB NATIONAL BANK Live Live 5INDB INDUSIND BANK Live Live 6 USFB UJJIVAN SMALL FINANCE BANK LTD Live Live 7ICIC ICICI BANK -

Investor Communication on Managing Director & CEO Interview with Business Line

From: [email protected] [mailto:[email protected]] Sent: 10 May 2021 20:58 To: Subject: [MARKETING] Greetings from Karnataka Bank – MD interview with BusinessLine Karnataka Bank Ltd. Your Family Bank, Across India Regd. & Head Office Phone: 0824-2228222 Fax: 0824-2225588 P. B. No.599, Mahaveera Circle E-mail: [email protected] Kankanady Website : www.karnatakabank.com Mangaluru – 575 002 CIN: L85110KA1924PLC001128 Dear Shareholder, We are pleased to attach an extract of the interview given by Shri Mahabaleshwara M S, Managing Director & CEO of the Bank to the BusinessLine newspaper which was published on May 7, 2021 for your information. With best wishes, Investor Relation Cell The Karnataka Bank Ltd. For all investor grievances related issues please make use of e mail Id:[email protected] only. ‘Karnataka Bank will focus on cost-light liability portfolio’ AJ VINAYAK ciple of ‘conserve, consolidate ZY cent for business turnover for sight of economic turn- extended loan period. Fur- three months considering Mangaluru, May 7 and emerge stronger’ im- the current fiscal. Consider- around. ther, the borrowers have also the current progress. It is ex- The Mangaluru-based mensely helped us to tide ing the Covid-19 second wave, remodelled their business pected that once the herd im- Karnataka Bank navigated the over the said crisis-like situ- we expect growth challenges Do you think the fresh and became more agile. How- munity is developed, the challenges posed by the ation and be able to come out in key sectors during the first Covid wave will lead to the ever, it is also expected that surge of Covid would also Covid-19 pandemic last year, with satisfactory numbers.