Property Market 2010

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Micare Panel Gp List (Aso) for (October 2020) No

MICARE PANEL GP LIST (ASO) FOR (OCTOBER 2020) NO. STATE TOWN CLINIC ID CLINIC NAME ADDRESS TEL OPERATING HOURS REGION : CENTRAL 1 KUALA LUMPUR JALAN SULTAN EWIKCDK KLINIK CHIN (DATARAN KEWANGAN DARUL GROUND FLOOR, DATARAN KEWANGAN DARUL TAKAFUL, NO. 4, 03-22736349 (MON-FRI): 7.45AM-4.30PM (SAT-SUN & PH): CLOSED SULAIMAN TAKAFUL) JALAN SULTAN SULAIMAN, 50000 KUALA LUMPUR 2 KUALA LUMPUR JALAN TUN TAN EWGKIMED KLINIK INTER-MED (JALAN TUN TAN SIEW SIN, KL) NO. 43, JALAN TUN TAN SIEW SIN, 50050 KUALA LUMPUR 03-20722087 (MON-FRI): 8.00AM-8.30PM (SAT): 8.30AM-7.00PM (SUN/PH): 9.00AM-1.00PM SIEW SIN 3 KUALA LUMPUR WISMA MARAN EWGKPMP KLINIK PEMBANGUNAN (WISMA MARAN) 4TH FLOOR, WISMA MARAN, NO. 28, MEDAN PASAR, 50050 KUALA 03-20222988 (MON-FRI): 9.00AM-5.00PM (SAT-SUN & PH): CLOSED LUMPUR 4 KUALA LUMPUR MEDAN PASAR EWGCDWM DRS. TONG, LEOW, CHIAM & PARTNERS (CHONG SUITE 7.02, 7TH FLOOR WISMA MARAN, NO. 28, MEDAN PASAR, 03-20721408 (MON-FRI): 8.30AM-1.00PM / 2.00PM-4.45PM (SAT): 8.30PM-12.45PM (SUN & PH): DISPENSARY)(WISMA MARAN) 50050 KUALA LUMPUR CLOSED 5 KUALA LUMPUR MEDAN PASAR EWGMAAPG KLINIK MEDICAL ASSOCIATES (LEBUH AMPANG) NO. 22, 3RD FLOOR, MEDAN PASAR, 50050 KUALA LUMPUR 03-20703585 (MON-FRI): 8.30AM-5.00PM (SAT-SUN & PH): CLOSED 6 KUALA LUMPUR MEDAN PASAR EWGKYONGA KLINIK YONG (MEDAN PASAR) 2ND FLOOR, WISMA MARAN, NO. 28, MEDAN PASAR, 50050 KUALA 03-20720808 (MON-FRI): 9.00AM-1.00PM / 2.00PM-5.00PM (SAT): 9.00AM-1.00PM (SUN & PH): LUMPUR CLOSED 7 KUALA LUMPUR JALAN TUN PERAK EWPISRP POLIKLINIK SRI PRIMA (JALAN TUN PERAK) NO. -

Trends in Southeast Asia

ISSN 0219-3213 2017 no. 9 Trends in Southeast Asia PARTI AMANAH NEGARA IN JOHOR: BIRTH, CHALLENGES AND PROSPECTS WAN SAIFUL WAN JAN TRS9/17s ISBN 978-981-4786-44-7 30 Heng Mui Keng Terrace Singapore 119614 http://bookshop.iseas.edu.sg 9 789814 786447 Trends in Southeast Asia 17-J02482 01 Trends_2017-09.indd 1 15/8/17 8:38 AM The ISEAS – Yusof Ishak Institute (formerly Institute of Southeast Asian Studies) is an autonomous organization established in 1968. It is a regional centre dedicated to the study of socio-political, security, and economic trends and developments in Southeast Asia and its wider geostrategic and economic environment. The Institute’s research programmes are grouped under Regional Economic Studies (RES), Regional Strategic and Political Studies (RSPS), and Regional Social and Cultural Studies (RSCS). The Institute is also home to the ASEAN Studies Centre (ASC), the Nalanda-Sriwijaya Centre (NSC) and the Singapore APEC Study Centre. ISEAS Publishing, an established academic press, has issued more than 2,000 books and journals. It is the largest scholarly publisher of research about Southeast Asia from within the region. ISEAS Publishing works with many other academic and trade publishers and distributors to disseminate important research and analyses from and about Southeast Asia to the rest of the world. 17-J02482 01 Trends_2017-09.indd 2 15/8/17 8:38 AM 2017 no. 9 Trends in Southeast Asia PARTI AMANAH NEGARA IN JOHOR: BIRTH, CHALLENGES AND PROSPECTS WAN SAIFUL WAN JAN 17-J02482 01 Trends_2017-09.indd 3 15/8/17 8:38 AM Published by: ISEAS Publishing 30 Heng Mui Keng Terrace Singapore 119614 [email protected] http://bookshop.iseas.edu.sg © 2017 ISEAS – Yusof Ishak Institute, Singapore All rights reserved. -

FGV Supply Base Information.Xlsx

ORGANIZATION: FGV KERNEL PRODUCTS SDN BHD (FKP) FACILITY: PASIR GUDANG, JOHOR, WEST MALAYSIA 2 3 PERCENTAGE 1 RSPO MSPO TRACEABILITY NAME OF COMPANY NAME OF MILL UML ID ADDRESS STATE COORDINATE OF THIRD- CERTIFIED CERTIFIED PERCENTAGE PARTY FFB Kilang Sawit Adela, 1°33’06.9”N FGV Holdings Berhad Adela PO1000000236 Johor √ √ 94% 79% Peti Surat 73, 81907 Kota Tinggi Johor. 104°11’10.9”E Kilang Sawit Air Tawar, 1°40'01.19"N FGV Holdings Berhad Air Tawar PO1000003414 Peti Surat 17, Pejabat Pos Felda Air Tawar 2 81920, Johor √ 100% 95% 104°01'46.67"E Kota Tinggi Johor Kilang Sawit Belitong, 1° 56'19.16" N FGV Holdings Berhad Belitong PO1000001311 Johor √ √ 92% 70% Peti Surat 61, 86007, Kluang, Johor 103° 29'55.03" E Kilang Sawit Bukit Kepayang, 3° 20'46.8" N FGV Holdings Berhad Bukit Kepayang PO1000000898 Pahang √ √ 84% 61% Pejabat Pos Triang, 28300, Triang, Pahang 102° 35'48.7" E Kilang Sawit Bukit Mendi, 3°11'49.45"N FGV Holdings Berhad Bukit Mendi PO1000000576 Pahang √ 100% 44% Pejabat Pos Triang, 28320, Triang, Pahang 102°18'03.43"E Kilang Sawit Chini 2, 3° 23'43" N FGV Holdings Berhad Chini 2 PO1000007489 Pahang √ 95% 100% D/A Bandar Chini 1, 26600, Pekan, Pahang 102° 58' 6" E Kilang Sawit Chini 3, 3° 21'58" N FGV Holdings Berhad Chini 3 PO1000003760 Pahang √ √ 84% 60% D/A Bandar Chini 1, 26600 Pekan Pahang 102° 55' 54" E Kilang Sawit Kahang, 2°04'29.91"N FGV Holdings Berhad Kahang PO1000001314 Johor √ 100% 61% Jln Kilang Sawit, 86000 Kluang, Johor 103°29'41.62"E Kilang Sawit Kemasul, 3°16'23.28"N FGV Holdings Berhad Kemasul PO1000000820 -

Buku Daftar Senarai Nama Jurunikah Kawasan-Kawasan Jurunikah Daerah Johor Bahru Untuk Tempoh 3 Tahun (1 Januari 2016 – 31 Disember 2018)

BUKU DAFTAR SENARAI NAMA JURUNIKAH KAWASAN-KAWASAN JURUNIKAH DAERAH JOHOR BAHRU UNTUK TEMPOH 3 TAHUN (1 JANUARI 2016 – 31 DISEMBER 2018) NAMA JURUNIKAH BI NO KAD PENGENALAN MUKIM KAWASAN L NO TELEFON 1 UST. HAJI MUSA BIN MUDA (710601-01-5539) 019-7545224 BANDAR -Pejabat Kadi Daerah Johor Bahru (ZON 1) 2 UST. FAKHRURAZI BIN YUSOF (791019-01-5805) 013-7270419 3 DATO’ HAJI MAHAT BIN BANDAR -Kg. Tarom -Tmn. Bkt. Saujana MD SAID (ZON 2) -Kg. Bahru -Tmn. Imigresen (360322-01-5539) -Kg. Nong Chik -Tmn. Bakti 07-2240567 -Kg. Mahmodiah -Pangsapuri Sri Murni 019-7254548 -Kg. Mohd Amin -Jln. Petri -Kg. Ngee Heng -Jln. Abd Rahman Andak -Tmn. Nong Chik -Jln. Serama -Tmn. Kolam Air -Menara Tabung Haji -Kolam Air -Dewan Jubli Intan -Jln. Straits View -Jln. Air Molek 4 UST. MOHD SHUKRI BIN BANDAR -Kg. Kurnia -Tmn. Melodies BACHOK (ZON 3) -Kg. Wadi Hana -Tmn. Kebun Teh (780825-01-5275) -Tmn. Perbadanan Islam -Tmn. Century 012-7601408 -Tmn. Suria 5 UST. AYUB BIN YUSOF BANDAR -Kg. Melayu Majidee -Flat Stulang (771228-01-6697) (ZON 4) -Kg. Stulang Baru 017-7286801 1 NAMA JURUNIKAH BI NO KAD PENGENALAN MUKIM KAWASAN L NO TELEFON 6 UST. MOHAMAD BANDAR - Kg. Dato’ Onn Jaafar -Kondo Datin Halimah IZUDDIN BIN HASSAN (ZON 5) - Kg. Aman -Flat Serantau Baru (760601-14-5339) - Kg. Sri Paya -Rumah Pangsa Larkin 013-3352230 - Kg. Kastam -Tmn. Larkin Perdana - Kg. Larkin Jaya -Tmn. Dato’ Onn - Kg. Ungku Mohsin 7 UST. HAJI ABU BAKAR BANDAR -Bandar Baru Uda -Polis Marin BIN WATAK (ZON 6) -Tmn. Skudai Kanan -Kg. -

![Micare Panel Gp List for Amgeneral Insurance Bhd [Fka Kurnia Insurans (M) Bhd] (September 2020) No](https://docslib.b-cdn.net/cover/3706/micare-panel-gp-list-for-amgeneral-insurance-bhd-fka-kurnia-insurans-m-bhd-september-2020-no-383706.webp)

Micare Panel Gp List for Amgeneral Insurance Bhd [Fka Kurnia Insurans (M) Bhd] (September 2020) No

MICARE PANEL GP LIST FOR AMGENERAL INSURANCE BHD [FKA KURNIA INSURANS (M) BHD] (SEPTEMBER 2020) NO. STATE TOWN CLINIC NAME ADDRESS TEL OPERATING HOURS REGION : CENTRAL 1 KUALA LUMPUR JALAN SULTAN KLINIK CHIN (DATARAN KEWANGAN DARUL TAKAFUL) GROUND FLOOR, DATARAN KEWANGAN DARUL TAKAFUL, NO. 4, 03-22736349 (MON-FRI): 7.45AM-4.30PM (SAT-SUN & PH): CLOSED SULAIMAN JALAN SULTAN SULAIMAN, 50000 KUALA LUMPUR 2 KUALA LUMPUR JALAN TUN TAN KLINIK INTER-MED (JALAN TUN TAN SIEW SIN, KL) NO. 43, JALAN TUN TAN SIEW SIN, 50050 KUALA LUMPUR 03-20722087 (MON-FRI): 8.00AM-8.30PM (SAT): 8.30AM-7.00PM (SUN/PH): 9.00AM-1.00PM SIEW SIN 3 KUALA LUMPUR WISMA MARAN KLINIK PEMBANGUNAN (WISMA MARAN) 4TH FLOOR, WISMA MARAN, NO. 28, MEDAN PASAR, 50050 KUALA 03-20222988 (MON-FRI): 9.00AM-5.00PM (SAT-SUN & PH): CLOSED LUMPUR 4 KUALA LUMPUR MEDAN PASAR DRS. TONG, LEOW, CHIAM & PARTNERS (CHONG SUITE 7.02, 7TH FLOOR WISMA MARAN, NO. 28, MEDAN PASAR, 50050 03-20721408 (MON-FRI): 8.30AM-1.00PM / 2.00PM-4.45PM (SAT): 8.30PM-12.45PM (SUN & PH): CLOSED DISPENSARY)(WISMA MARAN) KUALA LUMPUR 5 KUALA LUMPUR MEDAN PASAR KLINIK MEDICAL ASSOCIATES (LEBUH AMPANG) NO. 22, 3RD FLOOR, MEDAN PASAR, 50050 KUALA LUMPUR 03-20703585 (MON-FRI): 8.30AM-5.00PM (SAT-SUN & PH): CLOSED 6 KUALA LUMPUR JALAN TUN PERAK POLIKLINIK SRI PRIMA (JALAN TUN PERAK) NO. 68, JALAN TUN PERAK, 50050 KUALA LUMPUR 03-20222967 (MON-SUN): 9.00AM-9.00PM (PH): CLOSED 7 KUALA LUMPUR MENARA FELDA KLINIK PEMBANGUNAN (MENARA FELDA) RETAIL 2.3, MENARA FELDA, PLATINUM PARK, NO. -

Senarai Pendaftaran Bengkel Pembaikan Kenderaan Kemalangan

SENARAI PENDAFTARAN BENGKEL PEMBAIKAN KENDERAAN KEMALANGAN NEGERI : JOHOR BIL NAMA SYARIKAT ALAMAT NO TEL 10, 12, 14, Jalan Mutiara Emas 7/4, Taman Mount Austin, 81100 1 AH KUM MOTOR WORKSHOP SDN BHD. 07-3535788 Johor Bahru, Johor Darul Takzim. 2 ANG TRADING & MOTOR CREDIT SDN BHD. No. 33, 34 & 35, Jalan Sulaiman, 84000 Muar, Johor Darul Takzim. 06-955525 No. 7, Jalan Permas 9/14, Bandar Baru Permas Jaya, 81750 Masai, 3 AZAM MOTOR SERVICES SDN BHD. 07-3823532 Johor Darul Takzim. BAN SOON ENGINEERING & MOTOR No. 74 (PTD 41568), Jalan Idaman 1/3, Senai Industrial Park, 81400 4 07-5997681 WORKSHOP SDN BHD. Senai, Johor Darul Takzim. BATU PAHAT SIN HUAT MOTOR CAR & CRANE Lot MLO 513, Jalan Kampung Mohd Noor, Tongkang Pecah, 83010 5 07-4152220 SDN BHD. Batu Pahat, Johor Darul Takzim. 6 BENGKEL KENDERAAN SONG LIM SDN BHD. No 1, Pontian Besar, 82000 Pontian, Johor Darul Takzim. 07-6872822 No. 18, Jalan Enau 3, Taman Teratai, 81100 Johor Bahru, Johor Darul 7 BENGKEL LB MOTOR SDN BHD. 07-5207445 Takzim. BENGKEL MEMATERI KENDERAAN TEK YEE PTD 11769, Jalan Industri 2, Taman Perindustrian, 81500 Pekan 8 07-6992207 SDN BHD. Nanas, Johor Darul Takzim. No. 16, Jalan Kemajuan 3, Taman Perindustrian Kota Tinggi, 81900 9 BENGKEL MENGIMPAL KERETA KK SDN BHD. 07-8834123 Kota Tinggi, Johor Darul Takzim. No 22, Jalan Bertam 5, Taman Daya, 81100 Johor Bahru, Johor Darul 10 BOACK CHIEW WELDING SDN BHD. 07-3529262 Takzim. 11 BP AUTO UTAMA SDN BHD. No. 9, Jalan Mohd Salleh, 83000 Batu Pahat, Johor Darul Takzim. -

Colgate Palmolive List of Mills As of June 2018 (H1 2018) Direct

Colgate Palmolive List of Mills as of June 2018 (H1 2018) Direct Supplier Second Refiner First Refinery/Aggregator Information Load Port/ Refinery/Aggregator Address Province/ Direct Supplier Supplier Parent Company Refinery/Aggregator Name Mill Company Name Mill Name Country Latitude Longitude Location Location State AgroAmerica Agrocaribe Guatemala Agrocaribe S.A Extractora La Francia Guatemala Extractora Agroaceite Extractora Agroaceite Finca Pensilvania Aldea Los Encuentros, Coatepeque Quetzaltenango. Coatepeque Guatemala 14°33'19.1"N 92°00'20.3"W AgroAmerica Agrocaribe Guatemala Agrocaribe S.A Extractora del Atlantico Guatemala Extractora del Atlantico Extractora del Atlantico km276.5, carretera al Atlantico,Aldea Champona, Morales, izabal Izabal Guatemala 15°35'29.70"N 88°32'40.70"O AgroAmerica Agrocaribe Guatemala Agrocaribe S.A Extractora La Francia Guatemala Extractora La Francia Extractora La Francia km. 243, carretera al Atlantico,Aldea Buena Vista, Morales, izabal Izabal Guatemala 15°28'48.42"N 88°48'6.45" O Oleofinos Oleofinos Mexico Pasternak - - ASOCIACION AGROINDUSTRIAL DE PALMICULTORES DE SABA C.V.Asociacion (ASAPALSA) Agroindustrial de Palmicutores de Saba (ASAPALSA) ALDEA DE ORICA, SABA, COLON Colon HONDURAS 15.54505 -86.180154 Oleofinos Oleofinos Mexico Pasternak - - Cooperativa Agroindustrial de Productores de Palma AceiteraCoopeagropal R.L. (Coopeagropal El Robel R.L.) EL ROBLE, LAUREL, CORREDORES, PUNTARENAS, COSTA RICA Puntarenas Costa Rica 8.4358333 -82.94469444 Oleofinos Oleofinos Mexico Pasternak - - CORPORACIÓN -

Senarai Bilangan Pemilih Mengikut Dm Sebelum Persempadanan 2016 Johor

SURUHANJAYA PILIHAN RAYA MALAYSIA SENARAI BILANGAN PEMILIH MENGIKUT DAERAH MENGUNDI SEBELUM PERSEMPADANAN 2016 NEGERI : JOHOR SENARAI BILANGAN PEMILIH MENGIKUT DAERAH MENGUNDI SEBELUM PERSEMPADANAN 2016 NEGERI : JOHOR BAHAGIAN PILIHAN RAYA PERSEKUTUAN : SEGAMAT BAHAGIAN PILIHAN RAYA NEGERI : BULOH KASAP KOD BAHAGIAN PILIHAN RAYA NEGERI : 140/01 SENARAI DAERAH MENGUNDI DAERAH MENGUNDI BILANGAN PEMILIH 140/01/01 MENSUDOT LAMA 398 140/01/02 BALAI BADANG 598 140/01/03 PALONG TIMOR 3,793 140/01/04 SEPANG LOI 722 140/01/05 MENSUDOT PINDAH 478 140/01/06 AWAT 425 140/01/07 PEKAN GEMAS BAHRU 2,391 140/01/08 GOMALI 392 140/01/09 TAMBANG 317 140/01/10 PAYA LANG 892 140/01/11 LADANG SUNGAI MUAR 452 140/01/12 KUALA PAYA 807 140/01/13 BANDAR BULOH KASAP UTARA 844 140/01/14 BANDAR BULOH KASAP SELATAN 1,879 140/01/15 BULOH KASAP 3,453 140/01/16 GELANG CHINCHIN 671 140/01/17 SEPINANG 560 JUMLAH PEMILIH 19,072 SENARAI BILANGAN PEMILIH MENGIKUT DAERAH MENGUNDI SEBELUM PERSEMPADANAN 2016 NEGERI : JOHOR BAHAGIAN PILIHAN RAYA PERSEKUTUAN : SEGAMAT BAHAGIAN PILIHAN RAYA NEGERI : JEMENTAH KOD BAHAGIAN PILIHAN RAYA NEGERI : 140/02 SENARAI DAERAH MENGUNDI DAERAH MENGUNDI BILANGAN PEMILIH 140/02/01 GEMAS BARU 248 140/02/02 FORTROSE 143 140/02/03 SUNGAI SENARUT 584 140/02/04 BANDAR BATU ANAM 2,743 140/02/05 BATU ANAM 1,437 140/02/06 BANDAN 421 140/02/07 WELCH 388 140/02/08 PAYA JAKAS 472 140/02/09 BANDAR JEMENTAH BARAT 3,486 140/02/10 BANDAR JEMENTAH TIMOR 2,719 140/02/11 BANDAR JEMENTAH TENGAH 414 140/02/12 BANDAR JEMENTAH SELATAN 865 140/02/13 JEMENTAH 365 140/02/14 -

1380097620-Laporan Tahunan 2003-Bhgn 3

JABATAN ALAM SEKITAR DEPARTMENT OF ENVIRONMENT BAB / CHAPTER 5 JABATAN ALAM SEKITAR http://www.jas.sains.my 35 JABATAN ALAM SEKITAR DEPARTMENT OF ENVIRONMENT LAPORAN TAHUNAN 2003 36 ANNUAL REPORT 2003 JABATAN ALAM SEKITAR DEPARTMENT OF ENVIRONMENT PENGAWASAN KUALITI UDARA AIR QUALITY MONITORING Status Kualiti Udara Air Quality Status Pada tahun 2003, Jabatan Alam Sekitar (JAS) terus In 2003, the Department of Environment (DOE) mengawasi status kualiti udara di dalam negara monitored air quality under the national monitoring melalui rangkaian pengawasan kualiti udara network consisting of 51 automatic and 25 manual kebangsaan yang terdiri dari 51 stesen automatik dan stations (Map 5.1, Map 5.2). Sulphur Dioxide (SO2), 25 stesen manual (Peta 5.1, Peta 5.2). Sulfur Dioksida Carbon Monoxide (CO), Nitrogen Dioxide (NO2), (SO2), Karbon Monoksida (CO), Nitrogen Dioksida Ozone (O3) and Particulate Matter (PM10) were (NO2), Ozon (O3) and Partikulat Terampai (PM10) continuously monitored, while several heavy metals diawasi secara berterusan sementara logam berat including lead (Pb) were measured once in every six termasuk plumbum (Pb) diukur sekali pada setiap days (Table 5.1). enam hari. (Jadual 5.1). Secara keseluruhan, kualiti udara di seluruh negara The overall air quality for Malaysia throughout the pada tahun 2003 meningkat sedikit berbanding tahun 2003 improved slightly compared to 2002, such as sebelumnya terutama bagi parameter Partikulat for PM10, mainly due to more wet weather conditions Terampai (PM10) disebabkan oleh keadaan cuaca -

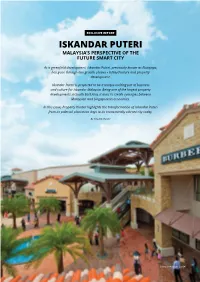

Iskandar-Puteri.Pdf

EXCLUSIVE REPORT ISKANDAR PUTERI MALAYSIA’S PERSPECTIVE OF THE FUTURE SMART CITY As a greenfield development, Iskandar Puteri, previously known as Nusajaya, has gone through two growth phases - infrastructure and property development. Iskandar Puteri is projected to be a unique melting pot of business and culture for Iskandar Malaysia. Being one of the largest property developments in South East Asia, it aims to create synergies between Malaysian and Singaporean economies. In this issue, Property Hunter highlights the transformation of Iskandar Puteri from its palm oil plantation days to its economically vibrant city today. By Property Hunter Johor Premium Outlet www.PropertyHunter.com.my 1 EXCLUSIVE REPORT Pinewood Iskandar Malaysia SiLC (Southern Industrial and and spacious luxury resort homes THE BRIDGING OF OPPORTUNITIES Studios Logistics Clusters) nestled within 7 parks featuring 31 Located on a 49 acres site, Pinewood SiLC is Iskandar Puteri’s premier hidden, intimate and lush gardens. ISKANDAR PUTERI Iskandar Malaysia Studios is a studio industrial and environmentally Covering 275 acres, the lake, forest, complex which targets the Asia-Pacific sustainable development. Spanning wetland and canal themes are Iskandar Puteri, a newly developed planned city in Johor Bahru District, has never been intended to attract region. The state-of-the-art facilities across 1,300 acres of neighbouring combined together with tropical the agriculture or manufacturing industries. Thought to be a signature and catalytic development billed as in the studio include 100,000sqft of development-ready land, SiLC landscaping, celebrating the beauty The World in One City, its convenience to Singapore and lower cost base makes it a primary location for film stages, ranging from 15,000sqft features advanced, innovation-driven of nature. -

BIL NAMA SEKOLAH ALAMAT 1 SA Bandar Kota Tinggi Jalan Sri

SEKOLAH-SEKOLAH AGAMA NEGERI JOHOR KOTA TINGGI BIL NAMA SEKOLAH ALAMAT 1 SA Bandar Kota Tinggi Jalan Sri Lalang,81900 Kota Tinggi 2 SA Sungai Telor Kampung Sungai Telor, 81900 Kota Tinggi 3 SA Ladang Y.P.J Ladang Y.P.J. 81900 Kota Tinggi 4 SA F. Pasir Raja Felda Pasir Raja, 81000 Kulai 5 SA F. Bukit Besar Felda Bukit Besar, 81000 Kulai 6 SA F. Bukit Ramon Felda Bukit Ramon, 81000 Kulai 7 SA Desa Mahkota d/a Sek. Keb. Rantau Panjang, 81900 Kota Tinggi 8 SA F. Sungai Sayong Felda Sg Sayong, 81000 Kulai 9 SA F. Pengeli Timur Felda Pengeli Timur, 81000 Kulai 10 SA F. Sungai Sibol Felda Sg Sibol, 81000 Kulai 11 SA Bakti Bandar Tenggara Bandar Tenggara, 81000 Kulai 12 SA F. Linggiu Felda Linggiu, 81900 Kota Tinggi 13 SA Petri Jaya Bandar Petri Jaya, 81900 Kota Tinggi 14 SA Semanggar Kg Semanggar, 81900 Kota Tinggi 15 SA Bukit Lintang Kg Bukit Lintang, 81900 Kota Tinggi 16 SA Taman Sayong Pinang Tmn Sayong Pinang, 81000 Kulai 17 SA Taman Kota Jaya Jalan Delima, Taman Kota Jaya, 81900 Kota Tinggi 18 SA Ladang Alaf Y.P.J Ladang Alaf Y.P.J. 81900 Kota Tinggi 19 SA Bandar Sri Perani Bandar Sri Perani, 81900 Kota Tinggi 20 SA Mawai Baru Kg Mawai Baru, 81900 Kota Tinggi 21 SA F. Bukit Aping Barat ( Al-Falah ) Felda Bukit Aping Barat, 81900 Kota Tinggi 22 SA F. Bukit Aping Timur ( Al-Nur ) Felda Bukit Aping Timur, 81900 Kota Tinggi 23 SA F. Lok Heng Selatan ( Al-Ansar ) Felda Lok Heng Selatan, 81900 Kota Tinggi 24 SA As Syakirin F. -

68-Avenue-Brochure-Udzqknpt.Pdf

Iskandar Puteri has been earmarked to become the largest fully integrated urban development in Southeast Asia. Being one of the catalyst developments within Iskandar Malaysia, it contributes significant investment, financial and business opportunities to the economic growth and development of the region. Kota Iskandar Newcastle University Medicine Malaysia, EduCity Columbia Asia Hospital Iskandar Puteri’s location, connectivity, and proximity to Singapore is also in part responsible for its surging economic growth. Seen as the economic catalyst and envisioned as Malaysia’s most connected and liveable city, Iskandar Puteri is set on a path for unprecedented growth and is the country’s foremost emerging economic zone. Puteri Harbour International Ferry Terminal IT’S ALL ABOUT LOCATION To Mutiara Rini To Pontian Bio-Xcell Nusaa Sentral Taman Nusantara V3 Hotel SiLC Maybank D Elegance Hotel Tea Garden Jalan Nus Hong Leong Bank a Pe ri M ntis Pizza Hut a l Taman a y s Mas i a - S i n g J a a Taman Nusa p l a Perintis o r n e U Gelang Patah S Masjid Jamik e l u h Balai Petronaset a c Gelang Patah o C t Bomba SJK(C) a n h P Le d o b Ming Terk g u Balai n h L h la Ko r e ta Isk da i Polis Jalan G an n k Gelang CIMB Bank Taman Patah KFC L Gelang Shell SMK Gelang Patah e Emas b Pejabat Pos u To h r a Kotao Iskandar y a Nusa Cemerlang N Restaurant u Industrial Parkk Chua Kee s a j a y Nusa Height a Kampung Melayu Taman Dato Syed Mohd Idrus EduCity Sports Complex ToT Gerbang Nusajaya EduCity Denaiai NusantaraN 0 1.5 KILOMETER Artist’s Impression SiLC Nusajaya Strategically located in Gelang Patah and within 10km of Gerbang Nusajaya, 68° Avenue boasts a prime locale and is surrounded by matured residential and commercial areas.