The Best Business Writing 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Marshall Project/California Sunday Magazine

ANNUAL REPORT 2018 2019 Carroll Bogert PRESIDENT Susan Chira EDITOR-IN-CHIEF Neil Barsky FOUNDER AND CHAIRMAN BOARD OF DIRECTORS Fred Cummings Nicholas Goldberg Jeffrey Halis Laurie Hays Bill Keller James Leitner William L. McComb Jonathan Moses Ben Reiter Topeka Sam Liz Simons (Vice-Chair) William J. Snipes Anil Soni ADVISORY BOARD Soffiyah Elijah Nicole Gordon Andrew Jarecki Marc Levin Joan Petersilia David Simon Bryan Stevenson CREDITS Cover: Young men pray at Pine Grove Youth Conservation Camp—California’s first and only remaining rehabilitative prison camp for offenders sentenced as teens. Photo by Brian Frank for The Marshall Project/California Sunday Magazine. Back cover: Photo credits from top down: WILLIAM WIDMER for The Marshall Project, Associated Press ELI REED for The Marshall Project. From Our President and Board Chair Criminal justice is a bigger part of our national political conversation than at any time in decades. That’s what journalism has the power to do: raise the issues, and get people talking. In 2013, when trying to raise funds for The Marshall Proj- more than 1,350 articles with more than 140 media part- ect’s launch, we told prospective supporters that one ners. Netflix has turned our Pulitzer-winning story, “An of our ambitious goals was for criminal justice reform to Unbelievable Story of Rape,” into an eight-part miniseries. be an integral issue in the presidential debates one day. We’ve reached millions of Americans, helped change “I would hope that by 2016, no matter who the candidates laws and regulations and won pretty much every major are… that criminal justice would be one of the more press- journalism prize out there. -

I:\28947 Ind Law Rev 47-1\47Masthead.Wpd

CITIGROUP: A CASE STUDY IN MANAGERIAL AND REGULATORY FAILURES ARTHUR E. WILMARTH, JR.* “I don’t think [Citigroup is] too big to manage or govern at all . [W]hen you look at the results of what happened, you have to say it was a great success.” Sanford “Sandy” Weill, chairman of Citigroup, 1998-20061 “Our job is to set a tone at the top to incent people to do the right thing and to set up safety nets to catch people who make mistakes or do the wrong thing and correct those as quickly as possible. And it is working. It is working.” Charles O. “Chuck” Prince III, CEO of Citigroup, 2003-20072 “People know I was concerned about the markets. Clearly, there were things wrong. But I don’t know of anyone who foresaw a perfect storm, and that’s what we’ve had here.” Robert Rubin, chairman of Citigroup’s executive committee, 1999- 20093 “I do not think we did enough as [regulators] with the authority we had to help contain the risks that ultimately emerged in [Citigroup].” Timothy Geithner, President of the Federal Reserve Bank of New York, 2003-2009; Secretary of the Treasury, 2009-20134 * Professor of Law and Executive Director of the Center for Law, Economics & Finance, George Washington University Law School. I wish to thank GW Law School and Dean Greg Maggs for a summer research grant that supported my work on this Article. I am indebted to Eric Klein, a member of GW Law’s Class of 2015, and Germaine Leahy, Head of Reference in the Jacob Burns Law Library, for their superb research assistance. -

Turning a Blind Eye: Why Washington Keeps Giving in to Wall Street

GW Law Faculty Publications & Other Works Faculty Scholarship 2013 Turning a Blind Eye: Why Washington Keeps Giving In to Wall Street Arthur E. Wilmarth Jr. George Washington University Law School, [email protected] Follow this and additional works at: https://scholarship.law.gwu.edu/faculty_publications Part of the Law Commons Recommended Citation Arthur E. Wilmarth, Jr., Turning a Blind Eye: Why Washington Keeps Giving In to Wall Street, 81 University of Cincinnati Law Review 1283-1446 (2013). This Article is brought to you for free and open access by the Faculty Scholarship at Scholarly Commons. It has been accepted for inclusion in GW Law Faculty Publications & Other Works by an authorized administrator of Scholarly Commons. For more information, please contact [email protected]. GW Law School Public Law and Legal Theory Paper No. 2013‐117 GW Legal Studies Research Paper No. 2013‐117 Turning a Blind Eye: Why Washington Keeps Giving In to Wall Street Arthur E. Wilmarth, Jr. 2013 81 U. CIN. L. REV. 1283-1446 This paper can be downloaded free of charge from the Social Science Research Network: http://ssrn.com/abstract=2327872 TURNING A BLIND EYE: WHY WASHINGTON KEEPS GIVING IN TO WALL STREET Arthur E. Wilmarth, Jr.* As the Dodd–Frank Act approaches its third anniversary in mid-2013, federal regulators have missed deadlines for more than 60% of the required implementing rules. The financial industry has undermined Dodd–Frank by lobbying regulators to delay or weaken rules, by suing to overturn completed rules, and by pushing for legislation to freeze agency budgets and repeal Dodd–Frank’s key mandates. -

The Dynamics of Secondaries

AVCJ Private Equity & Venture Forum 2010 India Summit 2010 New Delhi 26 - 27 August Hong Kong 9 -12 November 2010 ASIAN VENTURE CAPITAL JOURNAL Asia’s Private Equity News Source avcj.com July 27 2010 Volume 23 Number 28 EDITOR’S VIEWPOINT It’s a wrap Page 3 NEWS PRIVATE EQUITY ASIA Private equity and VC news of the week, with Actis, Blackstone, Carlyle, CHAMP, CVCI, Evolvence, IDG, Khazanah, Sequoia, Starr, TPG Page 5 DEALS OF THE WEEK Gung-ho for Kyobo as M&A ASIA buyout firms assess stake Page 13 Bain goes for Mr. China’s ASIMCO Page 13 FUNDRAISING NEWS Navis VI nears $1.2 billion close Page 15 INDUSTRY Q&A The dynamics of Industry Q&A: Hu Zhanghong, CEO, CCB International Page 17 Limited Partner Q&A: secondaries International Finance Once-owned LP positions for Asia Pacific and elsewhere Page 8 Corporation Page 19 DEALS OF THE WEEK FUNDRAISING NEWS Yellow Pages auction Greene’s Diamond Dragon up a gum tree? Page 11 takes flight Page 15 Anything is possible... There are many barriers to liquidity in private equity: complexity, transaction size, deadlines, disparate assets, confidentiality, alignment, tax, shareholder sensitivities – the list goes on. European Secondaries Firm of the Year But with creativity, experience and determination ... anything is possible. for the 6th consecutive year www.collercapital.com London New York 33 Cavendish Square 410 Park Avenue London New York Liquidity for private equity investors worldwide Contact: [email protected] EDITOR’S VIEWPOINT [email protected] ASIAN VENTURE CAPITAL -

Infrastructure-2008/07/25 1

INFRASTRUCTURE-2008/07/25 1 THE HAMILTON PROJECT THE BROOKINGS INSTITUTION INVESTING IN AMERICA’S INFRASTRUCTURE: FROM BRIDGES TO BROADBAND Washington, D.C. Friday, July 25, 2008 ANDERSON COURT REPORTING 706 Duke Street, Suite 100 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 INFRASTRUCTURE-2008/07/25 2 Opening Session ROBERT E. RUBIN, Citigroup Inc. LAWRENCE H. SUMMERS, Harvard University Special Guest: GOVERNOR TIM KAINE, Commonwealth of Virginia Overview of Strategy Paper DOUGLAS W. ELMENDORF, The Hamilton Project, The Brookings Institution Roundtable on Telecommunications Infrastructure Moderator: GLENN HUTCHINS, Silver Lake Panelists: BLAIR LEVIN, Stifel Nicolaus JON M. PEHA, Carnegie Mellon University PHILIP J. WEISER, University of Colorado Roundtable on Physical Infrastructure Moderator: NANCY CORDES, CBS News Panelists: RONALD BLACKWELL, AFL-CIO JASON BORDOFF, The Hamilton Project, The Brookings Institution DAVID LEWIS, HDR Decision Economics DOROTHY ROBYN, The Brattle Group ANDERSON COURT REPORTING 706 Duke Street, Suite 100 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 INFRASTRUCTURE-2008/07/25 3 * * * * * ANDERSON COURT REPORTING 706 Duke Street, Suite 100 Alexandria, VA 22314 Phone (703) 519-7180 Fax (703) 519-7190 INFRASTRUCTURE-2008/07/25 4 P R O C E E D I N G S MR. RUBIN: Good morning. Welcome. I’m Bob Rubin. On behalf of all my colleagues at The Hamilton Project, let me welcome you this morning to our program on infrastructure, from bridges to broadband. As most of you know, The Hamilton Project was begun about three years ago. Our objective was to set forth, which we did in the form of a paper, an economic strategy for the country in the face of a period of change of truly historic proportions, transformational change. -

CELEBRATING WOMEN's VOICES a FILM FESTIVAL for the FEMALE MAJORITY FESTIVAL GUIDE 51Fest.Org & @51Fest JULY 18–21 @

A FILM FESTIVAL FOR THE FEMALE MAJORITY CELEBRATING WOMEN’s VOICES JULY 18–21 @ IFC CENTER & SVA THEATRE FESTIVAL GUIDE 51fest.org & @51fest POWERHOUSE ContentS & Guests LINEUP Staff 2 MAYOR’s & COMMISSIONER’S LETTERS 3 Welcome 5 Sponsors 6 Special Events & Premieres 7 Schedule, Tickets & Venues 21 GUESTS AND MODERATORS, IN ORDER OF APPEARANCE Kathy Griffin: A Hell of a Story After the Wedding Kathy Griffin, Actor & Comedian Julianne Moore, Producer & Actor THE WALKING DOCTOR KILLING BARONESS VON Moderator Tina Brown Moderator Tina Brown DEAD WHO EVE SKETCH SHOW Women in the World Spotlight: Supermajority For Sama AMC BBC AMERICA BBC AMERICA IFC Cecile Richards, Supermajority Co-founder Waad al-Kateab, Director Ai-jen Poo, Supermajority Co-founder Edward Watts, Director Yoruba Richen, Filmmaker of And She Could Be Next Dr. Hamza al-Kateab, Subject Moderator Tina Brown Moderator Anne Barnard, former New York Times Beirut Bureau Chief Unbelievable Susannah Grant, Showrunner & Executive Producer Otherhood Sarah Timberman, Executive Producer Cindy Chupack, Director Lisa Cholodenko, Executive Producer & Episode Director Cathy Schulman, Producer Kaitlyn Dever, Actor Jason Michael Berman, Producer Danielle Macdonald, Actor Moderator Mario Cantone, Actor & Comedian Merritt Wever, Actor A Girl from Mogadishu Raise Hell: The Life & Times of Molly Ivins Mary McGuckian, Writer & Director Janice Engel, Director Ifrah Ahmed, Real-life Subject Moderator Rachel Dry, Deputy Politics Editor Barkhad Abdi, Actor for Enterprise at The New York Times Moderator -

Investing in Equitable News and Media Projects

Investing in Equitable News and Media Projects Photo credit from Left to Right: Artwork: “Infinite Essence-James” by Mikael Owunna #Atthecenter; Luz Collective; Media Development Investment Fund. INVESTING IN EQUITABLE NEWS AND MEDIA PROJECTS AUTHORS Andrea Armeni, Executive Director, Transform Finance Dr. Wilneida Negrón, Project Manager, Capital, Media, and Technology, Transform Finance ACKNOWLEDGMENTS Farai Chideya, Ford Foundation Jessica Clark, Dot Connector Studio This work benefited from participation in and conversations at the Media Impact Funders and Knight Media Forum events. The authors express their gratitude to the organizers of these events. ABOUT TRANSFORM FINANCE Transform Finance is a nonprofit organization working at the intersection of social justice and capital. We support investors committed to aligning their impact investment practice with social justice values through education and research, the development of innovative investment strategies and tools, and overall guidance. Through training and advisory support, we empower activists and community leaders to shape how capital flows affect them – both in terms of holding capital accountable and having a say in its deployment. Reach out at [email protected] for more information. THIS REPORT WAS PRODUCED WITH SUPPORT FROM THE FORD FOUNDATION. Questions about this report in general? Email [email protected] or [email protected]. Read something in this report that you’d like to share? Find us on Twitter @TransformFin Table of Contents 05 I. INTRODUCTION 08 II. LANDSCAPE AND KEY CONSIDERATIONS 13 III. RECOMMENDATIONS 22 IV. PRIMER: DIFFERENT TYPES OF INVESTMENTS IN EARLY-STAGE ENTERPRISES 27 V. CONCLUSION APPENDIX: 28 A. ACKNOWLEDGMENTS 29 B. LANDSCAPE OF EQUITABLE MEDIA INVESTORS AND ADJACENT INVESTORS I. -

April 2011 Quarterly Program Topic Report Category: Abortion NOLA: MLNH 010002 Series Title: PBS Newshour Length

April 2011 Quarterly Program Topic Report Category: Abortion NOLA: MLNH 010002 Series Title: PBS NewsHour Length: 60 minutes Airdate: 4/8/2011 6:00:00 PM Service: PBS Format: News Segment Length: 00:10:09 Budget Battle Lines Drawn Over Spending, Planned Parenthood as Shutdown Nears: Federal agencies prepared for a shutdown as negotiators struggled to reach a budget compromise. Jeffrey Brown discusses the latest on the budget talks with Todd Zwillich, Washington correspondent for WNYC radio. Category: Abortion NOLA: MLNH 010015 Series Title: PBS NewsHour Length: 60 minutes Airdate: 4/27/2011 6:00:00 PM Service: PBS Format: News Segment Length: 00:07:47 Budget Battles Reignite Animosity Between Congress, D.C. Government: Kwame Holman reports on the historically tense relations between Congress and the District of Columbia's residents and local politicians. The two worlds collided recently when Congress and President Obama reached a budget agreement in part through provisions affecting abortion services and private- school voucher programs in D.C. Category: Aging NOLA: MLNH 010000 Series Title: PBS NewsHour Length: 60 minutes Airdate: 4/6/2011 6:00:00 PM Service: PBS Format: News Segment Length: 00:06:55 Estrogen Study Lead Researcher on Risks, Benefits of Hormone-Replacement Therapy: Once a popular treatment for menopause symptoms, hormone- replacement therapy had come under scrutiny for raising the risk of certain diseases, but a new study found a reduced risk of breast cancer and other benefits for some women. Jeffrey Brown discusses the latest findings with Dr. Andrea LaCroix, the study's lead author. Category: Aging NOLA: NBRT 030214 Series Title: Nightly Business Report Length: 30 minutes Airdate: 4/28/2011 5:30:00 PM Service: PBS Format: Magazine Segment Length: 00:00:00 Baby Boomers are Working Longer; Baby Boomers, Retirement, and Inheritance; NYSE Says No to Merger Bids; Demand for Nuclear Energy Rises; Preview of Berkshire Hathaway Shareholder Meeting; US Economy Slows in First Quarter; Market Focus with Tom Hudson; Market Stats for April 28, 2011. -

Citizens Commission Submission Time: February 28, 2019 9:19 Am

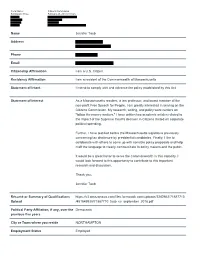

Form Name: Citizens Commission Submission Time: February 28, 2019 9:19 am Name Jennifer Taub Address Phone Email Citizenship Affirmation I am a U.S. Citizen Residency Affirmation I am a resident of the Commonwealth of Massachusetts Statement of Intent I intend to comply with and advance the policy established by this Act. Statement of Interest As a Massachusetts resident, a law professor, and board member of the non-profit Free Speech for People, I am greatly interested in serving on the Citizens Commission. My research, writing, and policy work centers on "follow the money matters." I have written two academic articles related to the impact of the Supreme Court's decision in Citizens United on corporate political spending. Further, I have testified before the Massachusetts legislature previously concerning tax disclosure by presidential candidates. Finally, I like to collaborate with others to come up with sensible policy proposals and help craft the language to clearly communicate to policy makers and the public. It would be a great honor to serve the Commonwealth in this capacity. I would look forward to this opportunity to contribute to this important research and discussion. Thank you, Jennifer Taub Résumé or Summary of Qualifications https://s3.amazonaws.com/files.formstack.com/uploads/3282862/71887710 Upload /481849938/71887710_taub_cv_september_2018.pdf Political Party Affiliation, if any, over the Democratic previous five years CIty or Town where you reside NORTHAMPTON Employment Status Employed Occupation Law Professor Employer Vermont Law School JENNIFER TAUB EDUCATION Harvard Law School, Cambridge, MA J.D. 1993, cum laude Recent Developments Editor of the Harvard Women’s Law Journal Yale University, New Haven, CT B.A. -

Major League Baseball Team Bankruptcies: Who Wins? Who Loses?

Loyola of Los Angeles Entertainment Law Review Volume 32 Number 3 Article 2 6-1-2012 Major League Baseball Team Bankruptcies: Who Wins? Who Loses? John Dillon Loyola Law School Los Angeles Follow this and additional works at: https://digitalcommons.lmu.edu/elr Part of the Law Commons Recommended Citation John Dillon, Major League Baseball Team Bankruptcies: Who Wins? Who Loses?, 32 Loy. L.A. Ent. L. Rev. 297 (2012). Available at: https://digitalcommons.lmu.edu/elr/vol32/iss3/2 This Notes and Comments is brought to you for free and open access by the Law Reviews at Digital Commons @ Loyola Marymount University and Loyola Law School. It has been accepted for inclusion in Loyola of Los Angeles Entertainment Law Review by an authorized administrator of Digital Commons@Loyola Marymount University and Loyola Law School. For more information, please contact [email protected]. 07. DILLON (DO NOT DELETE) 12/30/2012 2:03 AM MAJOR LEAGUE BASEBALL TEAM BANKRUPTCIES: WHO WINS? WHO LOSES? John Dillon* Baseball is America’s sport. It evokes a sense of tradition and a love for the home team. Like all professional sports teams, however, baseball teams are part of a league, which restricts team ownership through contrac- tual “constitutional” provisions and agreements and limits the number of teams that exist. In this limited and restricted entertainment market, profes- sional sports teams operate highly lucrative businesses that sometimes seek bankruptcy protection through Chapter 11 reorganization. Bankruptcy gen- erally allows the debtor to alter existing contractual rights and restructure its operations to avert the financial crisis that precipitated the bankruptcy filing. -

Federal Communications Commission FCC 07-220 Before the Federal

Federal Communications Commission FCC 07-220 Before the Federal Communications Commission Washington, D.C. 20554 In the Matter of ) IB Docket No. 07-181 ) SAT-T/C-20070810-00113 Intelsat Holdings, Ltd., Transferor, ) SAT-T/C-20070810-00111 ) SAT-T/C-20070810-00112 and ) SES-T/C-20070815-01100 ) SES-T/C-20070815-01090 Serafina Holdings Limited, Transferee ) SES-T/C-20070815-01091 ) SES-T/C-20070815-01098 Consolidated Application for Consent to Transfer ) SES-T/C-20070815-01097 Control of Holders of Title II and Title III ) SES-T/C-20070815-01099 Authorizations ) SES-T/C-20070815-01093 ) 0003125329 ) 0026-EX-TC-2007 ) ITC-T/C-20070815-00336 ) ITC-T/C-20070815-00331 MEMORANDUM OPINION AND ORDER Adopted: December 18, 2007 Released: December 19, 2007 By the Commission: Commissioner Copps concurring and issuing a statement. I. INTRODUCTION 1. In this Order, we consider a series of applications (“Applications”) filed by Intelsat Holdings, Ltd. (“Intelsat” or “Transferor”) and Serafina Holdings Limited (“Serafina” or “Transferee” and, together with Intelsat, the “Applicants”) pursuant to sections 214 and 310(d) of the Communications Act of 1934, as amended (the “Communications Act” or “Act”) and sections 1.948(a), 5.79, 25.119, and 63.24 of the Commission’s rules.1 In these unopposed Applications, Intelsat and Serafina seek consent to the transfer of control of Intelsat and six subsidiaries of Intelsat – Intelsat LLC, Intelsat North America LLC, Intelsat General Corporation, Intelsat USA License Corp., PanAmSat Licensee Corp., and PanAmSat H-2 Licensee Corp. (together, the “Intelsat Licensees”) – from Intelsat’s existing control group of four private equity firms (“Existing Control Group” or “Existing Shareholders”) to Serafina, a newly- formed Bermuda company indirectly controlled by BC Partners Holdings Limited (“BCP”), a U.K.-based 1 47 U.S.C. -

Annual Report 2014

14070219_Cover_Layout 1 8/14/14 10:18 AM Page 1 A N N Annual Report U A L R 2014 E P O R T 2 0 1 4 H U T C H I N S C E N T E R F O R A F R I C A N & A F R I C A N A M E R I C A N R E S E A R C H 104 Mount Auburn Street, 3R Cambridge, MA 02138 H A 617.495.8508 Phone R V 617.495.8511 Fax A R D U hutchinscente r@ fas.harvard.edu N I V hutchinscenter.fas.harvard.edu E R S facebook.com/hutchinscenter I T twitter.com/hutchinscenter Y 14070219_Text_Layout 1 8/14/14 9:48 AM Page 1 Understanding our history, as Americans and as African Americans, is essential to re-imagining the future of our country. How black people endured and thrived, how they created a universal culture that is uniquely American, how they helped write the story of this great nation, is one of the most stirring sagas of the modern era. Henry Louis Gates, Jr. Alphonse Fletcher University Professor Director, Hutchins Center for African & African American Research, Harvard University 1 14070219_Text_Layout 1 8/14/14 9:48 AM Page 2 Annual Report 2014 4 13 Letter from the Director 18 Featured Events 28–45 Flagships of the Hutchins Center 46 A Synergistic Hub of Intellectual Fellowship 56 Annual Lecture Series 58 Archives, Manuscripts, and Collections 59 Biographical Dictionary Projects 60 Research Projects and Outreach 66 Hutchins Center Special Events 70 Staff 72 Come and Visit Us Harvard University 14070219_Text_Layout 1 8/14/14 9:48 AM Page 3 28 34 36 38 40 42 43 44 45 3 14070219_Text_Layout 1 8/14/14 9:49 AM Page 4 Director Henry Louis Gates, Jr.