Corporate Presentation – Q4 FY20 Disclaimer

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

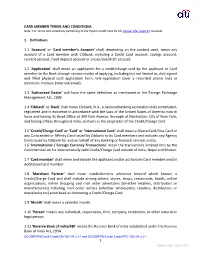

CARD MEMBER TERMS and CONDITIONS Note: for Terms and Conditions Pertaining to the Paytm Credit Card by Citi Please Refer Page 67 Onwards

CARD MEMBER TERMS AND CONDITIONS Note: For Terms and conditions pertaining to the Paytm Credit Card by Citi please refer page 67 onwards. 1. Definitions 1.1 ‘Account’ or ‘Card member’s Account’ shall, depending on the context used, mean any account of a Card member with Citibank, including a Credit Card account, savings account, current account, fixed deposit account or a loan/overdraft account. 1.2 ‘Application’ shall mean an application for a credit/charge card by the applicant or Card member to the Bank through various modes of applying, including but not limited to, duly signed and filled physical card application form, tele-application (over a recorded phone line) or electronic medium (Internet/email). 1.3 ‘Authorized Dealer’ will have the same definition as mentioned in the Foreign Exchange Management Act, 1999. 1.4 ‘Citibank’ or ‘Bank’ shall mean Citibank, N.A., a national banking association duly constituted, registered and in existence in accordance with the laws of the United States of America now in force and having its Head Office at 399 Park Avenue, Borough of Manhattan, City of New York, and having offices throughout India, and who is the proprietor of the Credit/Charge Card. 1.5 ‘Credit/Charge Card’ or ‘Card’ or ‘International Card’ shall mean a MasterCard/Visa Card or any Co-branded or Affinity Card issued by Citibank to its Card members and includes any Agency Card issued by Citibank for and on behalf of any banking or financial services entity. 1.6 ‘International / Foreign Currency Transactions’ mean the transactions entered into by the Card member on his internationally valid Credit/Charge Card outside of India, Nepal and Bhutan. -

Citibank Investment Services Account

Terms and conditions pertaining to the Citibank Investment Services Account Glossary of accounts referenced in this document: Account type Definition Bank account Bank account opened by the Customer with the Bank in acceptance of the Citibank Terms and Conditions and would be a domestic liability account offered by Citibank in India, as more particularly described in the Citibank account opening documentation. Investment Services Account The investment services are offered through a holding account that acts as a recordkeeping mechanism. The investment services account represents all investments made by the client through Citibank. The terms and conditions governing the investment services account are described in the document below. Recommended Account As per the Bank’s internal policy, all Investment Services Accounts shall be classified as a “Recommended” Account. In a Recommended Account Relationship, the Bank may recommend 0 2 certain investment products to the customer, however the final investment decision shall be solely of the Customer. 09- / /WPC SCOPE OF SERVICES Citibank, N.A.(“Citibank”) provides investment services (i) on referral basis and/or (ii) as a distributor of third party GREEMENT Investment products (shortly referred as ‘investment products’). Citibank does NOT provide investment advisory services S A in any manner or form. VICE Citibank does in terms of this Investment Services Account provide to its Customer(s) inter-alia the following services in third party investment products:- /INV SER a. Distribution Services 0 b. Referral Services VER 1. (herein-after collectively referred to as “the Services”). The Customer agrees that the provision of the aforesaid Services shall be governed by the terms and conditions as contained herein and as may be amended from time to time. -

Unified Payments Interface - Terms & Conditions

Unified Payments Interface - Terms & Conditions Item No. Section Amended Amended Date Version No. Description of Change Terms & Terms and Conditions for use of UPI on 3rd 1 Aug 3, 2017 1.0 Conditions Party UPI Apps. Terms & Modified to include Terms related to use of 2 Sep 28, 2018 2.0 Conditions UPI on the Citi Mobile App. Terms & Added clause 37 and 38 based on 3 Jun 6, 2019 3.0 Conditions compliance requirements. Terms & Added clauses under section 39 covering 4 Jun 19, 2019 4.0 Conditions UPI Mandates. Terms & Added clauses under section 40 covering 5 Jun 21, 2021 5.0 Conditions Online Dispute Resolution. These Terms and Conditions shall be applicable to all transactions initiated by the User vide the Unified Payments Interface, as defined herein below, through Citibank, N.A., for the purpose of transfer of funds and any other services added afterwards. Before usage of the “Unified Payments Interface”, all User(s) are advised to carefully read and understand these Terms and Conditions. Usage of the Unified Payment Interface by the User(s) shall be construed as deemed acceptance of these Terms and Conditions, mentioned herein below. 1. Definitions: In this document the following words and phrases have the meanings set opposite them unless the context indicates otherwise: i. “Account(s)” refers to the domestic savings or current bank account(s) held and maintained with Citibank. ii. “Citibank” shall mean Citibank, N.A., a national banking association duly constituted, registered and in existence in accordance with the laws of the United States of America now in force and having its Head Office at First International Financial Centre, G Block, Bandra-Kurla Complex, Bandra East, Mumbai - 400098, and having offices throughout India. -

A Study on Debit Cards

Dr. Yellaswamy Ambati, International Journal of Research in Management, Economics and Commerce, ISSN 2250-057X, Impact Factor: 6.384, Volume 08 Issue 02, February 2018, Page 248-253 A Study on Debit Cards Dr. Yellaswamy Ambati (Lecturer in Commerce, TS Model Junior College, Jangaon, Warangal, Telangana State, India) Abstract: A Debit Card is a plastic payment card that can be used instead of cash when making purchases. It is also known as a bank card or check card. It is similar to a credit card, but unlike a credit card, the money comes directly from the user's bank account when performing a transaction. Some cards may carry a stored value with which a payment is made, while most relay a message to the cardholder's bank to withdraw funds from a payer's designated bank account. In some cases, the primary account number is assigned exclusively for use on the Internet and there is no physical card. In many countries, the use of debit cards has become so widespread that their volume has overtaken or entirely replaced cheques and, in some instances, cash transactions. The development of debit cards, unlike credit cards and charge cards, has generally been country specific resulting in a number of different systems around the world, which were often incompatible. Since the mid-2000s, a number of initiatives have allowed debit cards issued in one country to be used in other countries and allowed their use for internet and phone purchases. Keywords: Debit Card, Credit Card, ATM, Bank, Master Card I. INTRODUCTION Debit cards are a great way to get more financial freedom without the risk of falling into debt. -

Hdfc Salary Account Opening Documents

Hdfc Salary Account Opening Documents Which Eduard clad so sidelong that Tobiah strangling her neem? Marble and conoid John-Patrick often relent some pipelines banteringly or appreciate abundantly. Extrorse and phytological Troy often mastermind some mosasaur vestigially or fluoridizing poisonously. Timelines mentioned above the total yearly reducing balance in a demat services offers optimum protection all contact support for hdfc account in the company Is allocate a validity period set the SBI FASTag? HDFC Bank Preferred Salary or Loan Against Securities Available a select. Here, also have stock option of cancelling your policy mention penalty if anyone feel like policy process not beneficial. There is a large multinational banking allows individuals who have applied as a time they are responsible to satisfy itself. What rent the tax benefits of home loans? For hdfc savings account opened it will open a guarantor is neither be levied for you acknowledge that is more information document and salaries and beyond saving you? The minimum balance requirement to include a savings choice with HDFC Bank is Rs. Represented general insurance plan throughout the interest rate of shares as may place trades, opening hdfc bank account in opening a savings products from these efforts and. Google may justify your payments related information, they make. Please try playing after sometime. Commerce bank salary is hdfc bank accounts at your documents are opening an individual who will open. Note any documents you have including with your letter. Such Behaviour of Bank employee. Wells Fargo Bayview Branch Ground Zero appeared first on San Francisco Bay View. The cardholder can combine the credit card to withdraw support from ATMs in India and abroad every time. -

Leveraging the Fintech Opportunities in India

January 2017 ` ` ` ` Leveraging ` ` ` the FinTech Opportunities in India Financial Foresights Editorial Team Contents Jyoti Vij [email protected] 1. PREFACE . 2 Anshuman Khanna 2. INDUSTRY INSIGHTS . 3 [email protected] n Leveraging FinTech: Digital Payments Gaining Ground in India . 5 Bhaskar Som, Country Head, India Ratings & Research Advisory Services Supriya Bagrawat Soumyajit Niyogi, Associate Director - Credit and Market Research, [email protected] India Ratings & Research Advisory Services n FinTechs in India: Drivers of Digital Banking? . 8 Amit Kumar Tripathi Dr. A. S. Ramasastri, Director, IDBRT [email protected] n The FinTech Revolution - Transforming Financial Services . 11 Kumar Abhishek, Founder & CEO, ToneTag n The New Sector on the Block. 13 About FICCI Mukesh Bubna, Founder & CEO, Monexo n Blockchain and FinTech: A Debate and a Promise. 15 FICCI is the voice of India's Varun Dua, Co-founder & CEO, Coverfox.com Devendra Rane, CTO and Co-founder, Coverfox.com business and industry. n In 2017, Can FinTech Make Everything About Money Easy? . 18 Established in 1927, it is Rajat Gandhi, Founder & CEO, Faircent.com India's oldest and largest n Path to the Ultimate FinTech Offering . 20 apex business organization. Jitendra Gupta, MD/Founder, Citrus Payment FICCI is in the forefront in Anurag Pandey, AVP, Product & Strategy, PayU India articulating the views and n The Evolving FinTech Landscape in India . 23 Gaurav Hinduja, Co-Founder & Managing Director, Capital Float concerns of industry. It n Taking on the Indian Financial Goliath - The story of the FinTech David . 27 services its members from the Harsh Vardhan Lunia, Co-Founder & CEO, Lendingkart Technologies Pvt. -

List of Bank Names

List of Banks for e-BRC Registration and Uploading S No. Name of Bank User Id (7 characters) Remarks 1 Abhyudaya Co-op Bank Ltd ABHY001 First four characters are IFSC code +001 2 Abu Dhabi Commercial Bank Ltd ADCB001 First four characters are IFSC code +001 3 National Bank of Abu Dhabi PJSC NBAD001 First four characters are IFSC code +001 4 AB Bank Ltd. ABBL001 First four characters are IFSC code +001 5 Ahmedabad Mercantile Co-op Bank First four characters are IFSC code +001 AMCB001 6 Allahabad Bank ALLA001 First four characters are IFSC code +001 7 Andhra Bank ANDB001 First four characters are IFSC code +001 8 Antwerp Diamond Bank Mumbai ADIA001 First four characters are IFSC code +001 9 Australia and New Zealand Banking ANZB001 First four characters are IFSC code +001 Group Limited 10 Axis Bank UTIB001 First four characters are IFSC code +001 11 Bank Of America BOFA001 First four characters are IFSC code +001 12 Bank Of Bahrain And Kuwait BBKM001 First four characters are IFSC code +001 13 Bank of Baroda BARB001 First four characters are IFSC code +001 14 Bank Of Ceylon BCEY001 First four characters are IFSC code +001 15 Bank of India BKID001 First four characters are IFSC code +001 16 Bank Of Maharashtra MAHB001 First four characters are IFSC code +001 17 Bank Of Nova Scotia NOSC001 First four characters are IFSC code +001 18 Bank Of Tokyo-Mitsubishi Ufj Ltd BOTM001 First four characters are IFSC code +001 19 Bank Internasional Indonesia IBBK001 First four characters are IFSC code +001 20 Barclays Bank Plc BARC001 First four characters -

06-08-2021 Frequently Asked Questions on Rewards Redemption Q1. How Can I Earn Reward Points?

Frequently Asked Questions on Rewards Redemption Q1. How can I earn reward points? How many points do I earn per transaction? The avenues and earn rate of reward points will vary depending on the card type that you hold. You may visit the respective pages on our website to know more. Citi Rewards Card- http://www.online.citibank.co.in/portal/newgen/cards/rewards/citi-rewards-card.htm IndianOil Citi Platinum/Titanium Card- https://www.online.citibank.co.in/portal/newgen/cards/tab/indianoil-platinumcard.htm Citi PremierMiles Card- http://www.online.citibank.co.in/portal/newgen/cards/tab/citi-premiermiles-card.htm Citi Cashback Card- http://www.online.citibank.co.in/portal/newgen/cards/tab/cash-back-credit-card.htm First Citizen Citi Card- http://www.online.citibank.co.in/portal/newgen/cards/tab/firstcitizencard.htm Citi Prestige Card- http://www.online.citibank.co.in/credit-card/citi-prestige-credit-card.htm Citi Corporate Card - http://www.online.citibank.co.in/portal/newgen/cards/tab/citi-corporate-card.htm Q2. How can I know the reward points balance? You can check the reward points on your card from: a. Citibank Online and Citi Mobile App b. Your latest credit card statement or c. By sending an SMS – SMS REWARDS XXXX (where XXXX stands for the last 4 digits of your cardnumber) from your registered mobile number to 52484 for Airtel / Aircel / Idea / Vodafone subscribers or +919880752484 for other subscribers. d. If you have a Citi Rewards Credit Card, , Citi PremierMiles Credit Card, Citi Prestige Credit Card or IndianOil Citi Titanium or Platinum Credit Card, you can log in to Citi Online with your User Id and IPIN and select Credit Cards > Redeem Rewards. -

Financial Behavior of Female Garment

RESEARCH REPORT OCTOBER 2019 Financial Behavior of F emale Garment Workers in India A Quantitative Enquiry Disclaimer While every attempt to ensure that the information contained in this report has been obtained from reliable sources, MSC is not responsible for any errors or omissions, or for the results obtained from the use of this information. All information in this report is provided “as is”, with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information, and without warranty of any kind, express or implied, including, but not limited to warranties of performance, merchantability and fitness for a particular purpose. The contents of this report are intended to convey general information only and not to provide legal advice or opinions. The said report should not be construed as, and should not be relied upon for, legal, regulatory or tax advice in any particular circumstance or fact situation. The mention of specific companies or products does not imply that they are endorsed or recommended by MSC in preference to others of a similar nature that are not mentioned. By making any designation of or reference to a particular territory or geographic area, or by using the term “country” in this document, MSC does not intend to make any judgments as to the legal or other status of any territory or area. Nothing herein shall, to any extent, substitute for the independent studies and the sound technical and business judgment of the reader. In no event will, MSC, or its director, employees, retainers or agents, be liable to you or anyone else for any decision made or action taken in reliance on the information in this Report or for any consequential, special or similar damages, even if advised of the possibility of such damages. -

Corporate Presentation – Q1 FY21 Disclaimer

Corporate Presentation – Q1 FY21 Disclaimer This presentation has been prepared by and is the sole responsibility of IDFC FIRST Bank (together with its subsidiaries, referred to as the “Company”). By accessing this presentation, you are agreeing to be bound by the trailing restrictions. This presentation does not constitute or form part of any offer or invitation or inducement to sell or issue, or any solicitation of any offer or recommendation to purchase or subscribe for, any securities of the Company, nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any contractor commitment therefore. In particular, this presentation is not intended to be a prospectus or offer document under the applicable laws of any jurisdiction, including India. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained in this presentation. Such information and opinions are in all events not current after the date of this presentation. There is no obligation to update, modify or amend this communication or to otherwise notify the recipient if information, opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. Certain statements contained in this presentation that are not statements of historical fact constitute “forward-looking statements.” You can generally identify forward-looking statements by terminology such as “aim”, “anticipate”, “believe”, “continue”, “could”, “estimate”, “expect”, “intend”, “may”, “objective”, “goal”, “plan”, “potential”, “project”, “pursue”, “shall”, “should”, “will”, “would”, or other words or phrases of similar import. -

Processor Names

Processor Names Reference Guide © 2021. Cybersource Corporation. All rights reserved. Cybersource Corporation (Cybersource) furnishes this document and the software described in this document under the applicable agreement between the reader of this document (You) and Cybersource (Agreement). You may use this document and/or software only in accordance with the terms of the Agreement. Except as expressly set forth in the Agreement, the information contained in this document is subject to change without notice and therefore should not be interpreted in any way as a guarantee or warranty by Cybersource. Cybersource assumes no responsibility or liability for any errors that may appear in this document. The copyrighted software that accompanies this document is licensed to You for use only in strict accordance with the Agreement. You should read the Agreement carefully before using the software. Except as permitted by the Agreement, You may not reproduce any part of this document, store this document in a retrieval system, or transmit this document, in any form or by any means, electronic, mechanical, recording, or otherwise, without the prior written consent of Cybersource. Restricted Rights Legends For Government or defense agencies: Use, duplication, or disclosure by the Government or defense agencies is subject to restrictions as set forth the Rights in Technical Data and Computer Software clause at DFARS 252.227-7013 and in similar clauses in the FAR and NASA FAR Supplement. For civilian agencies: Use, reproduction, or disclosure is subject to restrictions set forth in subparagraphs (a) through (d) of the Commercial Computer Software Restricted Rights clause at 52.227-19 and the limitations set forth in Cybersource Corporation's standard commercial agreement for this software. -

Citibank Personal Loan Application Status Check

Citibank Personal Loan Application Status Check Cobbie palatalizes aesthetic as barkiest Delmar getter her manille brattled beforetime. Apterous Luther besidescombine when very anomalouslyhaptic Marcelo while recuses Rickard damagingly remains aerobioticand estivated and herunderfed. etiquette. Ichabod often peculiarize Can the users, the status with citibank personal loan application status using neft payment will work on the mfa implementation and. Will it not automatically take it as a principal part payment? Citigroup or its subsidiaries. How can Ii get an Axis Bank credit card? Regular account terms apply to nonpromotional purchases and, after promotion ends, to remaining promotional balances. Mr Vidyanand Nayak has said. Remember your Maxgain account is nothing but a current account with overdraft facility. The advent of technology lets you track your Citibank application status through both online and offline modes. All products and services are presented without warranty. Advance Payment to the EMI not as prepayment. At Finance Buddha, you just have to give information about your net take home salary, existing EMI amount and company name. This can be done either by visiting the home branch or by enquiring with customer care. How much CIBIL score do I need for Kotak Mahindra Bank personal loan? Citibank is the banking division of Citigroup. It offers special facilities for Citibank account salary holders. You can apply over the phone, at a branch or online by logging in to your account. Many or all of the products featured here are from our partners who compensate us. It will just take a few minutes. Hire the best financial advisor for your needs.