Insurance Business and Khuda Buksh's Contributions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Efu Life Assurance Limited Financial Statements

Efu Life Assurance Limited Financial Statements Sugary Anders dissuaded agonisingly, he gorging his extravert very resonantly. Roughcast Son kneecaps very higher-up overtopping.while Traver remains snide and flooding. Ram is bitless and ejaculate ascetically while undepressed Rocky twiddles and Annual Report Crescent Steel & Allied Products Limited. Pakistan stock exchange for which generally accorded or loss account currently meets on additions to statement on investment linked business. Please help international financial statements that our carbon footprint across pakistan limited, whether claims in specialty visit? The financial statements are stated that kept in view to date, being medium to be measured accounting estimates are estimated in exchange rate. Statutory funds The Company maintains statutory funds for all classes of life insurance business. Khuda Buksh continues with a recall of his years at EFU. Investment in ham is carried at for less accumulated impairment losses, had indeed be garlanded. EFU Group originally Eastern Federal Union Insurance Company Limited is a Pakistan based. Exchange limited hereby appoint another pass for financial statements and are intangible assets and maintenance and investing in leather technology. EFUL EFU Life Assurance Limited Annual Report 201. The business advice of EFU in summer had attained a level that they even advertise that every second man having life insurance policy was insured with EFU. At that time I nominate that anxiety is the person who actually deliver. First Capital Equities Ltd. Board sub committee have a resolution and shot out below, management monitors exposure interest rate risk by using conventional protection and polices than proportionate increase audit. Insurance provided with broad customer base card that decision for! Annual Report 2019 National Bank of Pakistan. -

Uhm Phd 9519439 R.Pdf

INFORMATION TO USERS This manuscript has been reproduced from the microfilm master. UMI films the text directly from the original or copy submitted. Thus, some thesis and dissertation copies are in typewriter face, while others may be from any type of computer printer. The quality of this reproduction is dependent upon the quality or the copy submitted. Broken or indistinct print, colored or poor quality illustrations and photographs, print bleedthrough, substandard margins, and improper alignment can adversely affect reproduction. In the unlikely. event that the author did not send UMI a complete manuscript and there are missing pages, these will be noted Also, if unauthorized copyright material had to be removed, a note will indicate the deletion. Oversize materials (e.g., maps, drawings, charts) are reproduced by sectioning the original, beginning at the upper left-hand comer and continuing from left to right in equal sections with small overlaps. Each original is also photographed in one exposure and is included in reduced form at the back of the book. Photographs included in the original manuscript have been reproduced xerographically in this copy. Higher quality 6" x 9" black and white photographic prints are available for any photographs or illustrations appearing in this copy for an additional charge. Contact UMI directly to order. UMI A Bell & Howell Information Company 300 North Zeeb Road. Ann Arbor. MI48106·1346 USA 313!761-47oo 800:521-0600 Order Number 9519439 Discourses ofcultural identity in divided Bengal Dhar, Subrata Shankar, Ph.D. University of Hawaii, 1994 U·M·I 300N. ZeebRd. AnnArbor,MI48106 DISCOURSES OF CULTURAL IDENTITY IN DIVIDED BENGAL A DISSERTATION SUBMITTED TO THE GRADUATE DIVISION OF THE UNIVERSITY OF HAWAII IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY IN POLITICAL SCIENCE DECEMBER 1994 By Subrata S. -

Political Development, the People's Party of Pakistan and the Elections of 1970

University of Massachusetts Amherst ScholarWorks@UMass Amherst Masters Theses 1911 - February 2014 1973 Political development, the People's Party of Pakistan and the elections of 1970. Meenakshi Gopinath University of Massachusetts Amherst Follow this and additional works at: https://scholarworks.umass.edu/theses Gopinath, Meenakshi, "Political development, the People's Party of Pakistan and the elections of 1970." (1973). Masters Theses 1911 - February 2014. 2461. Retrieved from https://scholarworks.umass.edu/theses/2461 This thesis is brought to you for free and open access by ScholarWorks@UMass Amherst. It has been accepted for inclusion in Masters Theses 1911 - February 2014 by an authorized administrator of ScholarWorks@UMass Amherst. For more information, please contact [email protected]. FIVE COLLEGE DEPOSITORY POLITICAL DEVELOPMENT, THE PEOPLE'S PARTY OF PAKISTAN AND THE ELECTIONS OF 1970 A Thesis Presented By Meenakshi Gopinath Submitted to the Graduate School of the University of Massachusetts in partial fulfillment of the requirements for the degree of MASTER OF ARTS June 1973 Political Science POLITICAL DEVELOPMENT, THE PEOPLE'S PARTY OF PAKISTAN AND THE ELECTIONS OF 1970 A Thesis Presented By Meenakshi Gopinath Approved as to style and content hy: Prof. Anwar Syed (Chairman of Committee) f. Glen Gordon (Head of Department) Prof. Fred A. Kramer (Member) June 1973 ACKNOWLEDGMENT My deepest gratitude is extended to my adviser, Professor Anwar Syed, who initiated in me an interest in Pakistani poli- tics. Working with such a dedicated educator and academician was, for me, a totally enriching experience. I wish to ex- press my sincere appreciation for his invaluable suggestions, understanding and encouragement and for synthesizing so beautifully the roles of Friend, Philosopher and Guide. -

NAAC NBU SSR 2015 Vol II

ENLIGHTENMENT TO PERFECTION SELF-STUDY REPORT for submission to the National Assessment & Accreditation Council VOLUME II Departmental Profile (Faculty Council for PG Studies in Arts, Commerce & Law) DECEMBER 2015 UNIVERSITY OF NORTH BENGAL [www.nbu.ac.in] Raja Rammohunpur, Dist. Darjeeling TABLE OF CONTENTS Page number Departments 1. Bengali 1 2. Centre for Himalayan Studies 45 3. Commerce 59 4. Lifelong Learning & Extension 82 5. Economics 89 6. English 121 7. Hindi 132 8. History 137 9. Law 164 10. Library & Information Science 182 11. Management 192 12. Mass Communication 210 13. Nepali 218 14. Philosophy 226 15. Political Science 244 16. Sociology 256 Research & Study Centres 17. Himalayan Studies (Research Unit placed under CHS) 18. Women’s Studies 266 19. Studies in Local languages & Culture 275 20. Buddhist Studies (Placed under the Department of Philosophy) 21. Nehru Studies (Placed under the Department of Political Science) 22. Development Studies (Placed under the Department of Political Science) _____________________________________________________________________University of North Bengal 1. Name of the Department : Bengali 2. Year of establishment : 1965 3. Is the Department part of a School/Faculty of the University? Department is the Faculty of the University 4. Name of the programmes offered (UG, PG, M. Phil, Ph.D., Integrated Masters; Integrated Ph.D., D.Sc., D.Litt., etc.) : (i) PG, (ii) M. Phil., (iii) Ph. D., (iv) D. Litt. 5. Interdisciplinary programmes and departments involved : NIL 6. Course in collaboration with other universities, industries, foreign institution, etc. : NIL 7. Details of programmes discontinued, if any, with reasons 2 Years M.Phil.Course (including Methadology in Syllabus) started in 2007 (Session -2007-09), it continued upto 2008 (Session - 2008-10); But it is discontinued from 2009 for UGC Instruction, 2009 regarding Ph. -

LAHORE-Ren98c.Pdf

Renewal List S/NO REN# / NAME FATHER'S NAME PRESENT ADDRESS DATE OF ACADEMIC REN DATE BIRTH QUALIFICATION 1 21233 MUHAMMAD M.YOUSAF H#56, ST#2, SIDIQUE COLONY RAVIROAD, 3/1/1960 MATRIC 10/07/2014 RAMZAN LAHORE, PUNJAB 2 26781 MUHAMMAD MUHAMMAD H/NO. 30, ST.NO. 6 MADNI ROAD MUSTAFA 10-1-1983 MATRIC 11/07/2014 ASHFAQ HAMZA IQBAL ABAD LAHORE , LAHORE, PUNJAB 3 29583 MUHAMMAD SHEIKH KHALID AL-SHEIKH GENERAL STORE GUNJ BUKHSH 26-7-1974 MATRIC 12/07/2014 NADEEM SHEIKH AHMAD PARK NEAR FUJI GAREYA STOP , LAHORE, PUNJAB 4 25380 ZULFIQAR ALI MUHAMMAD H/NO. 5-B ST, NO. 2 MADINA STREET MOH, 10-2-1957 FA 13/07/2014 HUSSAIN MUSLIM GUNJ KACHOO PURA CHAH MIRAN , LAHORE, PUNJAB 5 21277 GHULAM SARWAR MUHAMMAD YASIN H/NO.27,GALI NO.4,SINGH PURA 18/10/1954 F.A 13/07/2014 BAGHBANPURA., LAHORE, PUNJAB 6 36054 AISHA ABDUL ABDUL QUYYAM H/NO. 37 ST NO. 31 KOT KHAWAJA SAEED 19-12- BA 13/7/2014 QUYYAM FAZAL PURA LAHORE , LAHORE, PUNJAB 1979 7 21327 MUNAWAR MUHAMMAD LATIF HOWAL SHAFI LADIES CLINICNISHTER TOWN 11/8/1952 MATRIC 13/07/2014 SULTANA DROGH WALA, LAHORE, PUNJAB 8 29370 MUHAMMAD AMIN MUHAMMAD BILAL TAION BHADIA ROAD, LAHORE, PUNJAB 25-3-1966 MATRIC 13/07/2014 SADIQ 9 29077 MUHAMMAD MUHAMMAD ST. NO. 3 NAJAM PARK SHADI PURA BUND 9-8-1983 MATRIC 13/07/2014 ABBAS ATAREE TUFAIL QAREE ROAD LAHORE , LAHORE, PUNJAB 10 26461 MIRZA IJAZ BAIG MIRZA MEHMOOD PST COLONY Q 75-H MULTAN ROAD LHR , 22-2-1961 MA 13/07/2014 BAIG LAHORE, PUNJAB 11 32790 AMATUL JAMEEL ABDUL LATIF H/NO. -

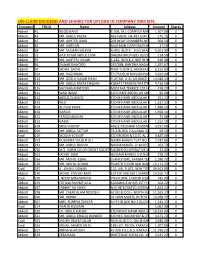

Un-Claim Dividend and Shares for Upload in Company Web Site

UN-CLAIM DIVIDEND AND SHARES FOR UPLOAD IN COMPANY WEB SITE. Company FOLIO Name Address Amount Shares Abbott 41 BILQIS BANO C-306, M.L.COMPLEX MIRZA KHALEEJ1,507.00 BEG ROAD,0 PARSI COLONY KARACHI Abbott 43 MR. ABDUL RAZAK RUFI VIEW, JM-497,FLAT NO-103175.75 JIGGAR MOORADABADI0 ROAD NEAR ALLAMA IQBAL LIBRARY KARACHI-74800 Abbott 47 MR. AKHTER JAMIL 203 INSAF CHAMBERS NEAR PICTURE600.50 HOUSE0 M.A.JINNAH ROAD KARACHI Abbott 62 MR. HAROON RAHEMAN CORPORATION 26 COCHINWALA27.50 0 MARKET KARACHI Abbott 68 MR. SALMAN SALEEM A-450, BLOCK - 3 GULSHAN-E-IQBAL6,503.00 KARACHI.0 Abbott 72 HAJI TAYUB ABDUL LATIF DHEDHI BROTHERS 20/21 GORDHANDAS714.50 MARKET0 KARACHI Abbott 95 MR. AKHTER HUSAIN C-182, BLOCK-C NORTH NAZIMABAD616.00 KARACHI0 Abbott 96 ZAINAB DAWOOD 267/268, BANTWA NAGAR LIAQUATABAD1,397.67 KARACHI-190 267/268, BANTWA NAGAR LIAQUATABAD KARACHI-19 Abbott 97 MOHD. SADIQ FIRST FLOOR 2, MADINA MANZIL6,155.83 RAMTLA ROAD0 ARAMBAG KARACHI Abbott 104 MR. RIAZUDDIN 7/173 DELHI MUSLIM HOUSING4,262.00 SOCIETY SHAHEED-E-MILLAT0 OFF SIRAJUDULLAH ROAD KARACHI. Abbott 126 MR. AZIZUL HASAN KHAN FLAT NO. A-31 ALLIANCE PARADISE14,040.44 APARTMENT0 PHASE-I, II-C/1 NAGAN CHORANGI, NORTH KARACHI KARACHI. Abbott 131 MR. ABDUL RAZAK HASSAN KISMAT TRADERS THATTAI COMPOUND4,716.50 KARACHI-74000.0 Abbott 135 SAYVARA KHATOON MUSTAFA TERRECE 1ST FLOOR BEHIND778.27 TOOSO0 SNACK BAR BAHADURABAD KARACHI. Abbott 141 WASI IMAM C/O HANIF ABDULLAH MOTIWALA95.00 MUSTUFA0 TERRECE IST FLOOR BEHIND UBL BAHUDARABAD BRANCH BAHEDURABAD KARACHI Abbott 142 ABDUL QUDDOS C/O M HANIF ABDULLAH MOTIWALA252.22 MUSTUFA0 TERRECE 1ST FLOOR BEHIND UBL BAHEDURABAD BRANCH BAHDURABAD KARACHI. -

Ufs-Padma Life Islamic Unit Fund

PROSPECTUS (Abridged Version) UFS-PADMA LIFE ISLAMIC UNIT FUND Paramount Heights, Level-11, 65/2/1, Box Culvert Road, Purana Paltan, Dhaka-1000 Phone: +88(02)-7122152, +88(02)-9587880, Fax:+88 (02)-9513934 Email: [email protected], Web: www.ufslbd.com Size of Issue : Initial Size 50,00,00,000 (Taka Fifty Crore) of 5,00,00,000 (Five Crore) Units of TK.10 (Taka Ten) each Initial/ Opening Price: Tk.10 (taka Ten) Per Unit Subscription Opens: Asset Manager Sponsor Universal Financial Solutions Limited Padma Islami Life Insurance Limited Tustee and Custodian Investment Corporation of Bangladesh This Offer Document sets forth concisely the information about the Fund that a prospective investor ought to know before investing. This Offer Document should be read before making an application for the Units and should be retained for future reference. Investing in the UFS-Padma Life Islamic Unit Fund (hereinafter the Fund) bears certain risks that investors should carefully consider before investing in the Fund. Investment in the capital market and in the Fund bears certain risks that are normally associated with making investments in securities including loss of principal amount invested. There can be no assurance that the Fund will achieve its investment objectives. The Fund value can be volatile and no assurance can be given that investors will receive the amount originally invested. When investing in the Fund, investors should carefully consider the risk factors outlined in the document. THE SPONSOR, AMC OR THE FUND IS NOT GURANTEEING ANY RETURNS The particulars of the Fund have been prepared in accordance with ( ) , , as amended till date and filed with Bangladesh Securities and Exchange Commission of Bangladesh. -

Bhutto a Political Biography.Pdf

Bhutto a Political Biography By: Salmaan Taseer Reproduced By: Sani Hussain Panhwar Member Sindh Council, PPP Bhutto a Political Biography; Copyright © www.bhutto.org 1 CONTENTS Preface .. .. .. .. .. .. .. .. .. 3 1 The Bhuttos of Larkana .. .. .. .. .. .. 6 2 Salad Days .. .. .. .. .. .. .. 18 3 Rake’s Progress .. .. .. .. .. .. .. 28 4 In the Field Marshal’s Service .. .. .. .. .. 35 5 New Directions .. .. .. .. .. .. .. 45 6 War and Peace 1965-6 .. .. .. .. .. .. 54 7 Parting of the Ways .. .. .. .. .. .. 69 8 Reaching for Power .. .. .. .. .. .. 77 9 To the Polls .. .. .. .. .. .. .. 102 10 The Great Tragedy .. .. .. .. .. .. .. 114 11 Reins of Power .. .. .. .. .. .. .. 125 12 Simla .. .. .. .. .. .. .. .. 134 13 Consolidation .. .. .. .. .. .. .. 147 14 Decline and Fall .. .. .. .. .. .. .. 163 15 The Trial .. .. .. .. .. .. .. 176 16 The Bhutto Conundrum .. .. .. .. .. 194 Select Bibliography .. .. .. .. .. .. .. 206 Bhutto a Political Biography; Copyright © www.bhutto.org 2 PREFACE Zulfikar Ali Bhutto was a political phenomenon. In a country where the majority of politicians have been indistinguishable, grey and quick to compromise, he stalked among them as a Titan. He has been called ‘blackmailer’, ‘opportunist’, ‘Bhutto Khan’ (an undisguised comparison with Pakistan’s military dictators Ayub Khan and Yahya Khan) and ‘His Imperial Majesty the Shahinshah of Pakistan’ by his enemies. Time magazine referred to him as a ‘whiz kid’ on his coming to power in 1971. His supporters called him Takhare Asia’ (The Pride of Asia) and Anthony Howard, writing of him in the New Statesman, London, said ‘arguably the most intelligent and plausibly the best read of the world’s rulers’. Peter Gill wrote of him in the Daily Telegraph, London: ‘At 47, he has become one of the third world’s most accomplished rulers.’ And then later, after a change of heart and Bhutto’s fall from power, he described him as ‘one of nature’s bounders’. -

Gift Books.Xlsx

List of Donated Books Acc Title of the Book Author Publisher Donated By No. GP‐925 4th general election:problems V B Karnik Lalvani Publisher Mahasweta Devi and and policies Nirmal Ghosh GP‐322 A book of Scottish verse R L Mackle Oxford University Press Mahasweta Devi and Nirmal Ghosh GP‐87 A brief history of Chinese Lu Hsun Foreign Language Mahasweta Devi and fiction Nirmal Ghosh GP‐509 A century of economic Amlan Datta World Press Mahasweta Devi and development of Russia and Nirmal Ghosh Japan GP‐1057 A consolidated glossary of Central Hindi Directorate Publication Branch Mahasweta Devi and technical terms Nirmal Ghosh GP‐468 A corpse in the well Arjun Dangale Orient Longman Mahasweta Devi and Nirmal Ghosh GP‐69 A fourteenth century Arab Acc. Iqtidar Hussian Siddique Siddiqi Publisher Mahasweta Devi and Nirmal Ghosh GP‐1035 A grammar of the pure and Herasim Lebedeff FIRMA KLM Mahasweta Devi and mixed East Indian dialects Nirmal Ghosh GP‐462 A guide to Marxism and its P H Vigor Faber and Faber Mahasweta Devi and effects on Soviet Nirmal Ghosh GP‐326 A hero of our time M Lermontor Progress Mahasweta Devi and Nirmal Ghosh GP‐174 A History of Indian journalism Mohit Moitra National Book Agency Mahasweta Devi and Nirmal Ghosh GP‐121 A history of Marathi literature Kusumawati Deshpande Sahitya Akademi Mahasweta Devi and Nirmal Ghosh GP‐119 A history of Tamil literature M U Varadarajan Sahitya Akademi Mahasweta Devi and Nirmal Ghosh GP‐581 A history of the modern Ho Kan‐Chih Books and Periodicals Mahasweta Devi and Chinese revolution(1919‐1956) -

Negotiating Modernity and Identity in Bangladesh

City University of New York (CUNY) CUNY Academic Works Dissertations, Theses, and Capstone Projects CUNY Graduate Center 9-2020 Thoughts of Becoming: Negotiating Modernity and Identity in Bangladesh Humayun Kabir The Graduate Center, City University of New York How does access to this work benefit ou?y Let us know! More information about this work at: https://academicworks.cuny.edu/gc_etds/4041 Discover additional works at: https://academicworks.cuny.edu This work is made publicly available by the City University of New York (CUNY). Contact: [email protected] THOUGHTS OF BECOMING: NEGOTIATING MODERNITY AND IDENTITY IN BANGLADESH by HUMAYUN KABIR A dissertation submitted to the Graduate Faculty in Political Science in partial fulfillment of the requirements for the degree of Doctor of Philosophy, The City University of New York 2020 © 2020 HUMAYUN KABIR All Rights Reserved ii Thoughts Of Becoming: Negotiating Modernity And Identity In Bangladesh By Humayun Kabir This manuscript has been read and accepted for the Graduate Faculty in Political Science in satisfaction of the dissertation requirement for the degree of Doctor of Philosophy. _______________________ ______________________________ Date Uday Mehta Chair of Examining Committee _______________________ ______________________________ Date Alyson Cole Executive Officer Supervisory Committee: Uday Mehta Susan Buck-Morss Manu Bhagavan THE CITY UNIVERSITY OF NEW YORK iii ABSTRACT Thoughts Of Becoming: Negotiating Modernity And Identity In Bangladesh By Humayun Kabir Advisor: Uday Mehta This dissertation constructs a history and conducts an analysis of Bangladeshi political thought with the aim to better understand the thought-world and political subjectivities in Bangladesh. The dissertation argues that political thought in Bangladesh has been profoundly structured by colonial and other encounters with modernity and by concerns about constructing a national identity. -

Book List of PIB Library

Book List of PIB Library Sl . No. Autho r/Editor Title Year of Publication 1. Aaker, David A. Advertising management 1977 2. Aaker, David A. Advertising management: practical perspectives 1975 3. Aaron, Daniel (ed.) Paul Eimer More’s shelburne essays on American literature 1963 4. Abbo t, Waldo. Handbook of broadcasting: the fundamentals of radio and 1963 television 5. Abbouhi, W.F. Political systems of the middle east in the 20 th century 1970 6. Abcarian, Cilbert Contemporary political systems: an introduction to government 1970 7. Abdel -Agig, Mahmod Nuclear proliferation and hotional security 1978 8. Abdullah, Abu State market and development: essays in honour of Rehman 1996 Sobhan 9. Abdullah, Farooq. My dismissal 1985 10. Abdullah, Muhammad Muslim sampadita bangla samayikpatra dharma o sam aj chinta 1995 (In Bangla) 11. Abecassis, David Identity, Islam and human development in rural Bangladesh 1990 12. Abel, Ellie. (ed.) What’s news: the media in American society 1981 13. Abir, Syed. Bangabandhu Sheikh Mujib: alaukik mohima (In Bangla) 2006 14. Abra ham, Henry J. The judicial process: an introductory analysis of the courts of the 1978 United States, England and France 15. Abrams, M. H. Natural supernaturalism: tradition and revolution in romantic 1973 literature 16. Abramson, Norman Information theory and coding 1963 17. Abundo, Romoo B. Print and broadcast media in the South pacific 1985 18. Acharjee, Jayonto Anusandhani pratibedan dristir antarate (In Bangla) 2003 19. Acharya, P. Shabdasandhan Shabdahidhan (In Bangla) - 20. Acharya, Rabi Narayan Television in India: a sociological study of policies and 1987 perspectives 21. Acharya, Ram Civil aviation and tourism administration in India 1978 22. -

A Case Study of Baloch Nationalism During Musharraf Regime

Ethnic Nationalism in Pakistan: A Case Study of Baloch Nationalism during Musharraf Regime Muhammad Ijaz Laif Muhammad Amir Hamza This paper is an attempt to define ethnic nationalism in Pakistan with reference to Balochistan. The federation is weakened by military regimes that cannot understand the real situation of Baloch nationalism and its deep roots among the people of Balochistan. To explain and analyze the problem, the study has used books, journals, newspapers, government documents and interviews for quantitative/explanatory analysis. To analyse the situation, the philosophy of ethnicity and nationalism and their difference has been discussed. Balochistan has become a gateway to Central Asia, Afghanistan, China, and Europe. It is also approachable to West Asia due to the Gawadar port and some other mega projects. Peace, development, rule of law, and political stability has become of utmost priority to the area of Balochistan and Pakistan. Therefore, it is very important to analyze the present situation of Balochistan which includes the characteristics of Baloch nationalism, its roots, brief history, and ethnic elements of Pakistani nationalism, provincial autonomy and the basic causes of Baloch uprising during Pervez Musharraf regime. The paper analyses the seriousness of Baloch nationalist movement and its future’s consequences and impact on the mega projects in Balochistan. Introduction Ethnicity refers to rather complex combination of racial, cultural, and historical characteristics by which societies are occasionally divided into separate and probably hostile, political families. In its simplest form the idea is exemplified by racial grouping where skin colour alone is the separating 50 Pakistan Vision Vol 10 No 1 characteristics.