قetal Brochure 3 4.Indd

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prince Saud Is Mourned

VOL XXXVIII No. 112 (GGDN 024) FRIDAY, 10th JULY 2015 200 Fils/2 Riyals ABC Ad new QRcode 6cm x 4col.pdf 1 2/19/15 3:48 PM Visit us at www.gdnonline.com WhatsApp us on 39451177 Millions hit Basma Ad.indd4m 1 have7/8/15 4:13 PM by London ed Syria Tube strike says UN 14 15 King hails spirit of unity MANAMA: Difficult times can always be over- the royal directives, support of the government come by reinforcing cohesion and social unity, led by His Royal Highness Prime Minister His Majesty King Hamad said last night. Prince Khalifa bin Salman Al Khalifa and fol- He was speaking as he received, at the low-up of His Royal Highness Prince Salman Muharraq Sports Club, Ramadan well-wishers. bin Hamad Al Khalifa, Crown Prince, Deputy The visit was part of the King’s meetings with Supreme Commander and First Deputy Premier. citizens of Bahrain. Dr Al Mudhahka welcomed the royal reforms He ordered that a multi-purpose hall be built and decisions made aimed at protecting the for the benefit of Muharraq citizens. homeland and citizens. His Majesty exchanged Ramadan greetings The King was presented with commemorative with the well-wishers. gifts by Muharraq Governor Salman Bin Hindi Dr Jawahir Shaheen Al Mudhahka, after recit- and Muharraq Sports Club chairman Shaikh ing verses from the Quran, hailed the develop- Ahmed bin Ali Al Khalifa. ment projects witnessed by Muharraq, thanks to More pictures – Page 2 n The King visits the Muharraq Sports Club Prince Saud is mourned RIYADH: Former Saudi Even before the 2011 MANAMA:RENTS Bahrain’s business- “This -

The Amwaj Islander

ISSUE 78 | APRIL 2017 THE AMWAJ ISLANDER Amwaj Updates New! The Islander Insider, page 5 Discover Explore our new website www.amwaj.bh WWW.AMWAJ.BH 1 THE AMWAJ ISLANDER Letter from the Editor Dear Islanders, It’s April, and spring has finally remember you are eligible to sprung! win for all following issues and not just the upcoming This month, we have launched one. a brand new column, The Finally, Amwaj Islands Islander Insider, courtesy of is staying true to its the Amwaj team, where we quintessence as we have a tell you what’s hot and what’s lot of new and upcoming not around the islands, in projects popping up around entertainment, food and the islands. Amwaj continues retails. Turn to page 5 to find to be a pioneer in real estate out more! in the Kingdom of Bahrain Don’t forget to check out page with lots of benefits in store 4 for exciting new events for our residents. Stay posted for more in our next issue! during April in celebration of Easter. For those of you who Happy reading! continue to submit photos, keep them coming and The Amwaj Team AMWAJ CLASSIFIEDS MAGAZINE is available for bookings For rates and bookings, email [email protected] 2 THE AMWAJ ISLANDER 60 Seconds With.. sea views and access to the canal. At the same time, I’m running the Lagoon Heights project located near Zawia 1 and The Lagoon available for sale as well as for investment. Lagoon Heights, a modern high luxury residence project, is currently under construction and is due to be completed first quarter of next year. -

Summary of Projects

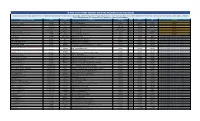

SUMMARY OF PROJECTS Completed Projects Project Sl. # Project Nature of Project Client Consultant Period Shopping Mall with The Private Hypermarket, Office of HRH Kingdom Mall Arabian East 20 1 supermarket, food Prince Khalifa at Janabiya Bureau Months courts, etc. with built Bin Salman Al up area of 81000m2 Khalifa Nawab Office G+3 Office Building Ansari 14 2 (Parliament with built up area of Ministry of Works Engineering Months Building) 5130m2 Dana Mall Lulu Bahrain Refurbishment Refurbishment & ID United 5 3 Hypermarket Works – Phase Works Engineering Months SPC 2 Al Nasseriya Construction of Al Adel Ahmadi 8 4 Accommodati Nasseriya Royal Court Associates S.P.C. Months ons – NBH Accommodations Marassi 11-Storey Beach Shores at front Residential Eagle Hills Diyar Gulf House 24 5 Marassi Al Dev. with 6 food & Company WLL Engineering Months Bahrain beverages outlet Construction of 11- Hilton Staff storey Al Sorouh Accommodati 14 6 accommodation Hospitality Real Arab Architects on at Months with 113 flats for Estate S.P.C. Muharraq Hilton staff Interior Fit-out works for Ramez Interior Fit-out 5 7 Ramez Group Ramez Group Hypermarket works Months at Kingdom Mall Janabiya Marassi Al Bahrain, Address Hotel & Serviced Raft foundation for Eagle Hills Diyar 3 8 Parsons Apartments Address Hotel Company WLL Months Foundation Works GHG Crowne Plaza Phase 2 – Boundary Wall, Refurbishment Gulf Hotels 5 9 MACE Car Park & works Group Months Refurbishment of Block A, E, F & G Marassi Al Bahrain, Landscape Hard & Soft Eagle Hills Diyar Eagle Hills Diyar 5 10 Phase 1 (Areas landscape works Company WLL Company WLL Months 1B2, 1C, 1D1, 1D2 & 1J) Project Sl. -

Bahrain Real Estate Market Report

BAHRAIN REAL ESTATE MARKET REPORT CONTENTS IN THIS ISSUE ISSUE 1 - MAY 2018 12 Property Trends TRENDS 15 Long Term Price Trends 1 16 Performance Review 28 New Developments in Bahrain’s Real Estate Market 2 CONTRIBUTORS 29 How is the Bahrain Real Estate Market Changing? CONSUMER 32 Top Searched Areas SEARCHES 34 Top Searched Keywords 3 EXPLAINED 35 User Behaviour 38 What Sets Us Apart WE ARE 40 Our Performance 4 PROPERTYFINDER 41 Awesome Agent Winners CONTRIBUTORS Maytham Alhayki Ali AlShuwaikh Owner Founder and CEO Maytham Alhayki Real Estate HomeSeekers BACKGROUND With over 14 years of experience across BACKGROUND With over a decade in the real estate and multiple sectors, including real estate and financial services, property development business, Ali is the CEO and Founder Maytham has been instrumental in providing clients with of HomeSeekers. He began his career in the Dubai market, comprehensive professional consultation on all matters which allowed him to grow and experience the industry. Ten relating to real estate, investing, and finance. Maytham’s vast years later, he moved the company to Bahrain, and through experience has helped him create a wide and invaluable his years in the industry has gained valuable experience and a network of clients, contacts, and business associates in deep knowledge about the regional market. Bahrain, Saudi Arabia, and across the Gulf region. IN HIS WORDS Considering that today we operate in the age IN HIS WORDS We believe that it’s our approach to customer of transparency, our platform is based on transparency, ethics, service that really sets us apart. -

INVESTING in BAHRAIN Property Tax & Market Insight

INVESTING IN BAHRAIN Property tax & market insight Autumn 2017 Investing in Bahrain – Property tax & market insight Contents 3 Introduction 4 Bahrain residential property market snapshot 5 Bahrain commercial property market snapshot 6 Considerations for investing in Bahrain Introduction Cluttons has partnered with Trowers & Hamlins to produce a guide to investing in the property market in Bahrain. This has been a cross team effort, working with Trowers & Hamlins in Bahrain to simplify the obligations for those investing in the Kingdom’s residential and commercial markets. The document also includes an update on the residential and office markets in Bahrain and aims to provide a quick and easily digestible resource for all investors and purchasers. Undoubtedly, as we enter the fourth year since the shock collapse in oil values, Bahrain is still working its way through a challenging period, with positive Government intervention programmes being rolled out across the Kingdom. The benefits of this intervention are being dampened somewhat by a slight widening in the country’s GDP-to-debt ratio, however there are some encouraging signs emerging. The Government is putting the pieces of its vision for Bahrain into place and we are already seeing this in many segments of the economy. For instance, with the aid of the GCC Support Fund, the non-oil sector has remained buoyant, growing by 3.7% last year, lifted by wide-ranging infrastructure and construction projects around Bahrain (Oxford Economics). In fact, in early August, the Economic Development Board (EDB) announced that some USD 80 billion worth of construction and infrastructure projects are currently underway or planned for Bahrain, which is expected to help underpin economic growth over the short to medium term. -

King Patronizes Bahrain First Fest Quartet

FAST, SAFE AND SECURE ONLINE MONEY TRANSFER NOW AVAILABLE ON THE BFC APP Thursday, March 1, 2018 Issue No. 7672 200 Fils Tel: 1722 8888 www.newsofbahrain.com www.facebook.com/nobonline newsofbahrain 38444680 nob_bh www.bfc.com.bh JO3639_Smart_Money_App_Launch_DT_Hamper_6.7cmX8.5cm.indd 1 9/26/17 3:39 PM FREE PICK! Issue No.264 DT Supplement www.weekenderbahrain.com March 1-7, 2018 Page 3 King patronizes Bahrain First Fest Arnaud Rothfuss A Verdant Date! Become a rt is able to grab your attention- be it any kind, take a look at something created majestically and you’ll be left in awe. Weekender Probably knowing the kind of effect it gives, Athe owner of a piece of land in Sanabis wanted to have his fence painted creatively as he paved the way for the construction of his new football field Winner! and coffee shop. Deciding to grab the attention of passersby’s with something unique and fetching, he contacted five artists, Arnaud Rothfuss , Mustafa Halwachi, Kojak ,Marylou Hebert and Sarah Redha , who came together to create something which is Page 5 certainly attention-worthy. The graffiti and street art members of ‘Dirty Hands Crew’ have showcased the collaborative results of their individual styles. One of the participants, artist ‘Arnaud Rothfuss’ spoke to Weekender on the project and its success: “It is sort of like a mini open-air museum, consisting of English and Arabic graffiti with realistic human faces as well as cartoonish Get Your Favourite characters.” Speaking on how it is such an interesting and unique concept, that is to have art embedded at a construction site in Bahrain, Arnaud pointed it to Celeb’s Autograph be a win-win situation for the artists and the land owner. -

Bahrain Bay,Riffa Views,Amwaj Islands,The Grove

Bahrain Bay Designed by world-class architect firm Skidmore Owings & Merrill (SOM), Bahrain Bay master planned waterfront development designed around vibrant neighborhoods of residential, commercial, and retail spaces, all based upon the unique concept of an island connected by bridges forming an inner harbour. It has total area of 1.45 million m2 and is expected to have around 40 properties. Owner / Developer: Arcapita Value ($bn): NA Area: Manama Seafront Address: Block 346, Bahrain Riffa Views With three unique residential Estates-The Lagoons, The Oasis and The Park, each individually themed and including multiple amenities and wide open spaces, Riffa Views offers a luxurious lifestyle, and all the benefits of living in a flourishing suburban area. Riffa Views offers nearly a thousand villas with unique lifestyle of Golf Course living. Owner / Developer: Riffa Views BSC Value ($bn):NA Area: Riffa Address: Block 943, Bahrain Amwaj Islands Amwaj Islands Project is the pioneers of waterside living in Bahrain, creating a perfectly balanced community development with individual beach villas / condominiums, providing a relaxing lifestyle for residents while still being conveniently located close to the bustling city of Manama. The islands boast of popular hospitality places such as Rotana Resort, Grove Resort, Grove Hotel and Ramada Apartments. The master plan has more than 2.2 million m2 of developable land area with plenty of prime investment opportunities for savvy developers. Owner / Developer: Ossis Property Developers BSC Value ($bn):2.0 Area: Amwaj Address: Block 257, Amwaj, Bahrain The Grove Hotel & Conference Centre The Grove Hotel & Conference centre, introducing a luxury family oriented hotel and contemporary, upscale 5 stars Hotel in Amwaj Island, Bahrain. -

Big Story Muharraq Sea Link a Fourth Bridge to Muharraq Will Be Ready by End 2019

03 FRIDAY, OCTOBER 12, 2018 big story Muharraq sea link A fourth bridge to Muharraq will be ready by end 2019 The project will be implemented• by a joint Bahraini-Saudi company One of the biggest projects• in the Kingdom Costs around BD100• million Provides easy access to• several vital areas in the Kingdom Expected to ease• traffic flow towards Airport Ahmed Al Khayat Mohammed Al Sinan TDT | Manama fairly new investment projects in Muharraq with the existing An artist’s rendering of the bridge Thamer Taifoor commercial areas in Manama, he fourth bridge linking such as the Diplomatic Area, The bridge will Khayat lately revealed that the the biggest in Bahrain and will and it connects the Al Sayah area Muharraq and Bahrain Bahrain Bay and Bahrain Finan- consist of four to construction works of the bridge be implemented by a joint Bah- in Muharraq with the north - Tislands will be ready by cial Harbour. This would be an five lanes in each will begin within the next few raini-Saudi company. eastern shores of the Capital. the end of 2019, says Muharraq effective boost to the Kingdom’s direction. This will weeks. Al Khayat said: “The width of It’s around 90 meters above sea Municipal Council Chairman economic movement. The pro- have a big impact He said the project is one of the bridge is around 150 meters, level.” Mohammed Al Sinan. ject would also serve the res - on the traffic jams Al Sinan said in an exclusive idential areas in the northern in Muharraq and statement to Tribune that all en- parts of Muharraq island and trances and exits of the cause- also ease the traffic flow towards Manama, and would way are completed. -

Meet Nabil, the Bee Whisperer

Sunday, March 26, 2017 Issue No. 7332 Meet Nabil, the 200 Fils www.newsofbahrain.com www.facebook.com/nobonline newsofbahrain 38444680 nob_bh bee whisperer 8P 02 Muhannad Mansour/DTNN Dr Lombard said this during a Our victory in defeating KARBABAD DISCOVERIES REVEAL [email protected] recent lecture at Bahrain National the disastrous Trump- stone tablet found near Qal’at Museum to announce the new set Al Bahrain archaeological site of discoveries in Bahrain last year. Ryan health care plan is inA Karbabad recently is reported “The agreement carved on one the result of millions of to carry a loan agreement, which side of the tablet shows it was Americans standing up is said to be the first ever in the written in 19th year of King Darius human history carved on stone. I, who ruled Babylon during the and fighting back. Archaeologists say the stone time (around 503-504 BC), in tablet with the loan agreement was Akkadian language, used to be @SenSanders probably the first in history and popular during the time,” he said. was made between two individuals He said that based on the Today’s Weather who lived on the island 2500 years inscription, it is assumed that the ago. borrower had returned the dates Max Min 1st ever The agreement, according to next year during the month of 24°C 18°C the archaeologists, was about one Tashrit (September or October). of them borrowing some dates And when it was returned, the from the other on the promise of names of the witnesses were returning one year later. -

In and Out-Patient Mednet Network Providers List in Bahrain

IN AND OUT-PATIENT MEDNET NETWORK PROVIDERS LIST IN BAHRAIN This list is provided by MedNet UAE to present information only regarding Participating Network Providers. All decisions about the type of care are the responsibility of the patient and the selected Physician. While every effort is made to maintain accurate and correct information, MedNet UAE reserves the right to periodically conduct modifications as Provider Participation is updated. We request that Provider Participation be confirmed prior to hospitalization. NAME OF THE PROVIDER TYPE CITY ADDRESS SPECIALTY Country TEL FAX NETWORK Awali Hospital Hospital Awali P.O. Box 25555, Awali General +973 17753333 17753598 Gold Only Doctor Haifa Eye Hospital Hospital Tubli Tubli -main Road.Manama General +973 17252573 17252110 Gold Only German Orthopaedic Hospital Hospital Manama Building 99, Road 29, Block 329, Manama General +973 17239980 17239980 Gold Only Dr. Saeed Al-Saeed Cardiology Zinj Street No. 3017, Flat14, Bldg 976, Block 330, Zinj, Manama Cardiology +973 17251500 17251507 Gold Only Dr. Farzana Al-Sayed (Affiliated with Joslin) Neurology Manama Gulf Diabetes Center Neurology +973 17239239 Gold Only Dr. Wiam Ebrahim Hussein (Affiliated with Joslin) Endocrionology Manama Gulf Diabetes Center Endocrionology +973 17239239 Gold Only Dental Specialist center Dental Muharraq 1535,Bil. 1197 falt 17 Dental +973 17341234 17344919 Gold Only Dr. Ammar Jaffar Al-Ekri Dental Tubli Flat 22 , Building 589 , Road 111 Dental +973 17131010 17822270 Gold Only Al-Haffadh Specialised Dental Hospital -

Marina,Water Bay,Diyar Al Muharraq,Durrat Al Bahra

Bahrain Bay Designed by world-class architect firm Skidmore Owings & Merrill (SOM), Bahrain Bay master planned waterfront development designed around vibrant neighborhoods of residential, commercial, and retail spaces, all based upon the unique concept of an island connected by bridges forming an inner harbour. It has total area of 1.45 million m2 and is expected to have around 40 properties. Owner / Developer: Arcapita Value ($bn): NA Area: Manama Seafront Address: Block 346, Bahrain Riffa Views With three unique residential Estates-The Lagoons, The Oasis and The Park, each individually themed and including multiple amenities and wide open spaces, Riffa Views offers a luxurious lifestyle, and all the benefits of living in a flourishing suburban area. Riffa Views offers nearly a thousand villas with unique lifestyle of Golf Course living. Owner / Developer: Riffa Views BSC Value ($bn):NA Area: Riffa Address: Block 943, Bahrain Amwaj Islands Amwaj Islands Project is the pioneers of waterside living in Bahrain, creating a perfectly balanced community development with individual beach villas / condominiums, providing a relaxing lifestyle for residents while still being conveniently located close to the bustling city of Manama. The islands boast of popular hospitality places such as Rotana Resort, Grove Resort, Grove Hotel and Ramada Apartments. The master plan has more than 2.2 million m2 of developable land area with plenty of prime investment opportunities for savvy developers. Owner / Developer: Ossis Property Developers BSC Value ($bn):2.0 Area: Amwaj Address: Block 257, Amwaj, Bahrain Dilmunia A mixed-use development with high end wellness facilities, themed luxury hospitality, lifestyle attractions and unique residences. -

Amwaj Islands,IKEA,Dilmunia Shopping Mall

Amwaj Islands Amwaj Islands Project is the pioneers of waterside living in Bahrain, creating a perfectly balanced community development with individual beach villas / condominiums, providing a relaxing lifestyle for residents while still being conveniently located close to the bustling city of Manama. The islands boast of popular hospitality places such as Rotana Resort, Grove Resort, Grove Hotel and Ramada Apartments. The master plan has more than 2.2 million m2 of developable land area with plenty of prime investment opportunities for savvy developers. Owner / Developer: Ossis Property Developers BSC Value ($bn):2.0 Area: Amwaj Address: Block 257, Amwaj, Bahrain IKEA The biggest IKEA store in the GCC with a built-up area in excess of 30,000 sqm. Owner: IKEA Saudi Developer: IKEA Saudi Value: BD 47 mn Status: Under construction Area: 45,000 sqm Purpose: Enhance the tourism infrastructure in the Kingdom and support the national economy Type of Developments (with details) : ( residential? Hotels? Commercial? Etc…): Retail Upcoming developments/ expansions: N/A Any other information you find relevant for Investors: N/A High resolution images of existing project and upcoming project (CGI drawings): N/A Dilmunia Shopping Mall (signed contract with Palm Capital) Temara – retail plots Sultan Mall Sultan Mall is located in Zayed Town area and has shopping, leisure, restaurants and services all under one roof. Size: Small Classification: Neighborhood Centre Gross Leasing rea: 6,550 m2 Area: Zayed Town Address: Building 121, Road 20, Block 720, Zayed Town, Bahrain The Lagoon The one-kilometre long waterside destination has been inspired by lively cultural centres like London’s Covent Garden and Cockle Wharf in Sydney.