Report REP 444 ASIC Enforcement Outcomes: January to June 2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Federal Court of Australia

FEDERAL COURT OF AUSTRALIA Trilogy Funds Management Limited v Sullivan (No 2) [2015] FCA 1452 Citation: Trilogy Funds Management Limited v Sullivan (No 2) [2015] FCA 1452 Parties: TRILOGY FUNDS MANAGEMENT LIMITED (ACN 080 383 679) AS THE RESPONSIBLE ENTITY FOR THE PACIFIC FIRST MORTGAGE FUND (ARSN 088 139 477) v PHILIP KEITH SULLIVAN, THOMAS WILLIAM SWAN, STEPHEN ANTHONY MCCORMICK and IAN WILLIAM DONALDSON File number: NSD 604 of 2012 Judge: WIGNEY J Date of judgment: 18 December 2015 Catchwords: CORPORATIONS – directors – officers – statutory duties of directors – duty of care and diligence – duties of a responsible entity of a registered managed investment scheme pursuant to s 601FC of the Corporations Act 2001 (Cth) – duties of directors and officers of a responsible entity pursuant to s 601FD of the Corporations Act 2001 (Cth) – standard of care and diligence for directors and officers of a responsible entity acting as a professional trustee – duty of officers of a responsible entity to act in the best interests of scheme members – duty of officers to take steps to ensure responsible entity complies with Corporations Act 2001 (Cth), scheme constitution and compliance plan – where the directors and officers of a responsible entity of a registered managed investment scheme approved or purportedly approved the increase of a loan facility in circumstances where scheme constitution and compliance plan not complied with – whether directors and officers of a responsible entity of a managed investment scheme acted with care and diligence -

Finally Doing Something About Climate Change

PROOF ISSN 1322-0330 RECORD OF PROCEEDINGS Hansard Home Page: http://www.parliament.qld.gov.au/hansard/ E-mail: [email protected] Phone: (07) 3406 7314 Fax: (07) 3210 0182 Subject FIRST SESSION OF THE FIFTY-SECOND PARLIAMENT Page Thursday, 6 September 2007 ABSENCE OF SPEAKER .............................................................................................................................................................. 3113 PETITIONS ..................................................................................................................................................................................... 3113 MINISTERIAL STATEMENTS ........................................................................................................................................................ 3113 Peacekeepers .................................................................................................................................................................... 3113 Council for the Australian Federation, Appointment of Director ......................................................................................... 3113 Clean Coal .......................................................................................................................................................................... 3114 Queensland Economy ........................................................................................................................................................ 3114 Rugby League World Cup ................................................................................................................................................. -

![The Queen V Gore [2020] QDC 264 | DISTRICT COURT of QUEENSLAND](https://docslib.b-cdn.net/cover/5111/the-queen-v-gore-2020-qdc-264-district-court-of-queensland-1885111.webp)

The Queen V Gore [2020] QDC 264 | DISTRICT COURT of QUEENSLAND

DISTRICT COURT OF QUEENSLAND CITATION: The Queen v Gore [2020] QDC 264 PARTIES: The Queen v Craig Kirrin Gore (Defendant) FILE NO: 2413/18 DIVISION: Criminal PROCEEDING: Judge alone trial. ORIGINATING Brisbane District Court COURT: DELIVERED ON: 27 October 2020 DELIVERED AT: Brisbane HEARING DATE: 27, 28, 30, 31 July 2020, 4 August 2020. JUDGE: Byrne QC DCJ ORDERS: Special Verdicts: Count 11: I find that the jurisdiction of this Court to try the charge has not been established on the balance of probabilities. I therefore find the defendant not guilty on count 11. All other counts: I find that the jurisdiction of this Court to try the charges has been established on the balance of probabilities. General Verdicts: Count 1: Not guilty Count 2: Not guilty Count 3: Guilty Count 4: Not guilty Count 5: Not guilty Count 6: Not guilty Count 7: Guilty Count 8: Guilty 2 Count 9: Guilty Count 10: Guilty Count 12: Guilty CATCHWORDS: CRIMINAL LAW – GENERAL MATTERS – PROCEDURE – TRIAL HAD BEFORE JUDGE WITHOUT JURY – where the defendant applied for a judge alone trial under s 614 of the Criminal Code Act 1899 (Qld) – where no jury trial orders were made under s 615 of the Criminal Code (Qld) – where the accused was tried by a judge sitting without jury. CRIMINAL LAW – PARTICULAR OFFENCES –– FRAUD – VERDICT – where the defendant is charged with 11 counts of fraud to the value of $30,000 or more and 1 count of fraud – where the defendant has pleaded not guilty to all charges – whether the defendant is guilty or not guilty. -

1144 05/16 Issue One Thousand One Hundred Forty-Four Thursday, May Sixteen, Mmxix

#1144 05/16 issue one thousand one hundred forty-four thursday, may sixteen, mmxix “9-1-1: LONE STAR” Series / FOX TWENTIETH CENTURY FOX TELEVISION 10201 W. Pico Blvd, Bldg. 1, Los Angeles, CA 90064 [email protected] PHONE: 310-969-5511 FAX: 310-969-4886 STATUS: Summer 2019 PRODUCER: Ryan Murphy - Brad Falchuk - Tim Minear CAST: Rob Lowe RYAN MURPHY PRODUCTIONS 10201 W. Pico Blvd., Bldg. 12, The Loft, Los Angeles, CA 90035 310-369-3970 Follows a sophisticated New York cop (Lowe) who, along with his son, re-locates to Austin, and must try to balance saving those who are at their most vulnerable with solving the problems in his own life. “355” Feature Film 05-09-19 ê GENRE FILMS 10201 West Pico Boulevard Building 49, Los Angeles, CA 90035 PHONE: 310-369-2842 STATUS: July 8 LOCATION: Paris - London - Morocco PRODUCER: Kelly Carmichael WRITER: Theresa Rebeck DIRECTOR: Simon Kinberg LP: Richard Hewitt PM: Jennifer Wynne DP: Roger Deakins CAST: Jessica Chastain - Penelope Cruz - Lupita Nyong’o - Fan Bingbing - Sebastian Stan - Edgar Ramirez FRECKLE FILMS 205 West 57th St., New York, NY 10019 646-830-3365 [email protected] FILMNATION ENTERTAINMENT 150 W. 22nd Street, Suite 1025, New York, NY 10011 917-484-8900 [email protected] GOLDEN TITLE 29 Austin Road, 11/F, Tsim Sha Tsui, Kowloon, Hong Kong, China UNIVERSAL PICTURES 100 Universal City Plaza Universal City, CA 91608 818-777-1000 A large-scale espionage film about international agents in a grounded, edgy action thriller. The film involves these top agents from organizations around the world uniting to stop a global organization from acquiring a weapon that could plunge an already unstable world into total chaos. -

Record of Proceedings

PROOF ISSN 1322-0330 RECORD OF PROCEEDINGS Hansard Home Page: http://www.parliament.qld.gov.au/hansard/ E-mail: [email protected] Phone: (07) 3406 7314 Fax: (07) 3210 0182 Subject FIRST SESSION OF THE FIFTY-THIRD PARLIAMENT Page Tuesday, 24 November 2009 ASSENT TO BILLS ........................................................................................................................................................................ 3433 Tabled paper: Letter, dated 19 November 2009, from Governor to the Speaker advising of assent to bills.......................................................................................................................................................... 3433 PRIVILEGE ..................................................................................................................................................................................... 3433 Comments by Member for Moggill ..................................................................................................................................... 3433 SPEAKER’S STATEMENTS .......................................................................................................................................................... 3434 Christmas Tree Appeal ....................................................................................................................................................... 3434 Parliamentary Crime and Misconduct Commissioner, Appointments ............................................................................... -

ASIC Annual Report 2014-2015

ANNUAL REPORT 2014–2015 investor and financial consumer trust and confidence fair, orderly, transparent and efficient markets efficient and accessible registration Contents Letter of transmittal 1 3. People, community Chairman’s report 2 and the environment 83 3.1 ASIC’s people 84 Key outcomes 2014–15 6 3.2 Diversity at ASIC 90 Government priorities and parliamentary inquiries 12 3.3 ASIC in the community 94 Commissioners 15 3.4 Indigenous awareness and action at ASIC 96 1. About ASIC 17 1.1 ASIC’s role 18 3.5 Environmental performance 97 1.2 Corporate structure 4. Financial statements 99 at 30 June 2015 23 5. Appendices 153 1.3 Regulated populations and 5.1 The role of Commissioners 154 key responsibilities 25 5.2 Audit Committee and audit, 1.4 ASIC’s surveillance coverage assurance and compliance of regulated populations 28 services 155 1.5 ASIC for all Australians 30 5.3 External committees and panels 156 1.6 Financial summary 5.4 Portfolio budget and expenditure 32 statement outcomes 161 2. Outcomes in detail 33 5.5 Six-year summary of 2.1 Priority 1 – Investor and financial key stakeholder data 167 consumer trust and confidence 34 5.6 Reports required under statute 2.2 Priority 2 – Fair, orderly, transparent and other reporting requirements 169 and efficient markets 50 5.7 Consultancies and expenditure 2.3 Priority 3 – Efficient and on advertising 172 accessible registration 64 5.8 ASIC’s use of its 2.4 Unclaimed money and managing significant compulsory property vested in ASIC 70 information-gathering powers 175 2.5 Assessing -

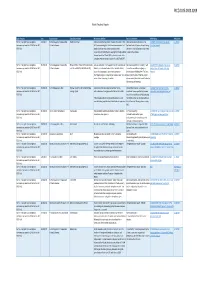

Rcd.0015.0003.0208

RCD.0015.0003.0208 Public Results & Reports Type of Inquiry Date Industry Sector Entity/Subject Name Misconduct identified Actions or outcomes MR Heading MR number Formal investigation (an investigation 2/11/2011 Funds Management - Responsible Equititrust Limited ASIC concerned that Equititrust in breach of a condition of its Obtained various interim orders in the 11-238AD ASIC obtains orders against 11-238AD commenced pursuant to s13 ASIC Act or s247 Entities & schemes AFS licence requiring that it hold a minimum amount of net Supreme Court of Queensland constraining Equititrust Limited NCCP Act) tangible assets and has breached provisions of the the manner in which Equititrust is permitted Corporations Act 2001 (the Act) requiring that it lodge audited to operate the schemes. financial reports for EIF and EPCIF and audited reports of its compliance with the compliance plans for both EIF and EPCIF. Formal investigation (an investigation 31/07/2015 Funds management - Responsible Mr David Anthony Ross, Mr Richard Albarran ASIC was concerned that the appointment of Messrs Ross and ASIC was successful in its proceeding, with 15-203MR ASIC takes action to remove 15-203MR commenced pursuant to s13 ASIC Act or s247 Entities & schemes and Midland HWY Pty Ltd (Midland HWY) Albarran, as replacement administrators to Midland HWY, Messrs Ross and Albaran resigning as administrators of failed land banking NCCP Act) occurred in circumstances where many investors in administrators of Midland HWY. The Court company Hermitage Bendigo, who may also be creditors, were not given made orders by consent that the original notice of the first meeting of creditors. -

Federal Court of Australia

FEDERAL COURT OF AUSTRALIA Australian Securities and Investments Commission v ActiveSuper Pty Ltd (No 2) [2013] FCA 234 Citation: Australian Securities and Investments Commission v ActiveSuper Pty Ltd (No 2) [2013] FCA 234 Parties: AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION v ACTIVESUPER PTY LTD (ACN 125 423 574), ACN 143 832 053 PTY LTD (ACN 143 832 053), JASON GRANT BURROWS, JUSTIN LUKE GIBSON, U.S. REALTY INVESTMENTS #1, LLC (L-1666059-6), U.S. REALTY INVESTMENTS #2, LLC (L-1666058-5), U.S. REALTY INVESTMENTS #3, LLC (L- 1668734- 4), U.S. REALTY INVESTMENTS #4, LLC (L- 1668736-6), SYNDICATED PROPERTY GROUP LTD (BVI COMPANY NUMBER 1678711), WORLDWIDE PROPERTY OPPORTUNITIES LTD (BVI COMPANY NUMBER 1678279), CAYCO MANAGEMENT (REGISTRATION NUMBER CR- 265977), MOGS PTY LTD (ACN 136 499 360), JEFFREY GEORGE, GRAEME SYDNEY STONEHOUSE, MARINA ULRIKA LOVISA GORE, MARK GORDON ADAMSON and CRAIG KIRRIN GORE File number: VID 426 of 2012 Judge: GORDON J Date of judgment: 19 March 2013 Catchwords: CORPORATIONS – application to appoint provisional liquidator – discretionary considerations for appointment of provisional liquidator – whether appropriate to appoint a provisional liquidator to a trustee company – company automatically removed as trustee Legislation: Corporations Act 2001 (Cth) Trusts Act 1973 (Qld) Cases cited: Allstate Exploration NL v Batepro Australia Pty Ltd [2004] NSWSC 261 Australian Securities Commission v AS Nominees Limited (1995) 62 FCR 504 Australian Securities Commission v Solomon (1996) 19 - 2 - ACSR 73 Australian Securities -

1 GOLD COAST WATERWAYS AUTHORITY Executive Summary of Board Personnel the Gold Coast Waterways Authority (GCWA) Was Established

GOLD COAST WATERWAYS AUTHORITY Executive Summary of Board Personnel The Gold Coast Waterways Authority (GCWA) was established ‘to manage the sustainable use and development of the Gold Coast waterways… A board made up of local community and industry representatives will be responsible for overseeing the better management of the Gold Coast waterways…[and] report directly to the Transport and Main Roads Minister’. (www.tmr.qld.gov.au/gcwa accessed 30/09/2012) Russell Witt was the original Administrator and CEO of the GWCA appointed in late 2012. He also served as the Regional Director – Gold Coast for Maritime Safety Queensland (MSQ). Witt previously served under MSQ General Manager, Captain John Watkinson, until Watkinson retired from that position to enter private enterprise in 2009. Watkinson’s Meridian Maritime Services conducted the November 2012 ‘investigation into the feasibility of piloting large cruise ships to and from a proposed terminal within the Gold Coast Broadwater’ at the Smartship Australia simulators, Brisbane. The GWCA will, as a part of its responsibilities, assess and respond to Watkinson’s report on the ship simulations. (see http://www.saveourspit.com/No_Terminal/news/NewsArticle.jsp?News_ID=180 ) In mid-2012, the former Gold Coast Mayor, Gary Baildon, was appointed to the position of Chair of the GCWA by the Queensland State Government. In December 2012, GCWA board members were appointed following public advertisements for nominations. The appointments to the GCWA board consisted of three Queensland Liberal National Party members: - Tom Tate, Gold Coast Mayor and LNP Member (Local Government, Register of Interests 26/06/12) - Steve Minnikin, LNP, Assistant Transport Minister, Qld. -

Queensland's Richest 100

Queensland's richest 100 Article from: • Font size: Decrease Increase • Email article: Email • Print article: Print • Submit comment: Submit comment August 30, 2008 11:00pm • No 1: Clive Palmer • Wealth: $6.5 billion • What: Iron ore mining • Where: Gold Coast EVEN when you are Queensland's richest person and a multibillionaire, sometimes the most important lessons are learned from life itself. Clive Palmer lost his wife of 22 years, Sue, to cancer three years ago. For a time, he managed his grief by immersing himself in his work. Then he began spending time with Anna. "I've known Anna for 20 years. She was married to one of my good friends and he died a month after my wife," Mr Palmer, 54, said. That shared experience brought the couple closer together. They married last year and, in February, he became a father for the third time with the birth of daughter Mary. That new chapter of his life has helped highlight what the billionaire says is part of his successful strategy. It may be coincidental, or a reflection of the renewed joy in his life, but the past 12 months have been productive and profitable for the Gold Coast-based go-getter who puts his active wealth at $6.5 billion. Mr Palmer owns a massive iron ore deposit in Western Australia estimated at 160 billion tonnes. • No 2: Ken Talbot • Wealth: $1.4 billion • What: Coal mining • Where: Brisbane THE state's king of coal is now cashed up after selling the majority of his stake inmining powerhouse Macarthur Coal for $636 million. -

Tabled Paper: Letter from Her Excellency the Governor to the Speaker, Dated 5 November 2008, Advising of Bills Assented To

PROOF ISSN 1322-0330 RECORD OF PROCEEDINGS Hansard Home Page: http://www.parliament.qld.gov.au/hansard/ E-mail: [email protected] Phone: (07) 3406 7314 Fax: (07) 3210 0182 Subject FIRST SESSION OF THE FIFTY-SECOND PARLIAMENT Page Tuesday, 11 November 2008 ASSENT TO BILLS ........................................................................................................................................................................ 3327 Tabled paper: Letter from Her Excellency the Governor to the Speaker, dated 5 November 2008, advising of bills assented to.................................................................................................................................... 3327 REPORT ......................................................................................................................................................................................... 3327 Members’ Daily Travelling Allowance Claims ..................................................................................................................... 3327 Tabled paper: Annual report of the daily travelling allowance claims by members of the Legislative Assembly for 2007-08, prepared pursuant to section 1.3.1 of the Members’ Entitlements Handbook................... 3327 SPEAKER’S STATEMENT ............................................................................................................................................................ 3327 Queensland Parliament Employee of the Year .................................................................................................................