Beyond the Asterisk * Adjusting for Performance Inflation In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Visit the Hall of Stats at Hallofstats.Com. Follow the Hall of Stats on Twitter at @Hallofstats

The Hall of Stats is populated by a formula called Hall Rating. A player needs a Hall Rating of 100 to gain induction, so Alan Trammell and his 143 Hall Rating sit comfortably in the Hall of Stats. In fact, Trammell’s Hall Rating is better than 70% of Hall of Famers. For a complete explanation of the Hall Rating formula, similarity scores, and much more, visit: hallofstats.com/about The Hall of Stats The Hall of Stats ranks An alternate Hall of Fame populated by a mathematical formula. every player in history—all 17,941 of them. There are also rankings by position Research and design by Adam Darowski ([email protected]) and by franchise. Built by Adam Darowski, Jeffrey Chupp, and Michael Berkowitz (hallofstats.com) Each player’s value is broken down by franchise. Rather than raw career The Hall of Stats was conceived because the Hall of Fame voting process has statistics, the Hall of Stats become a political nightmare. A massive backlog of worthy candidates is piling displays WAR and WAA up—some because of association with PEDs (or simply suspicion), but some because (before and after voters just don’t realize how good they were. There seems to be a false perception of adjustments). what the Hall of Fame actually is. It’s not all Babe Ruth, Christy Mathewson, Ty Cobb, Each player’s WAR and Honus Wagner. For every Walter Johnson in the Hall of Fame there’s a Jesse components (batting, Haines. For every Hank Aaron there’s a Tommy McCarthy. basrunning, avoiding the double play, fielding, and Should each player better than Haines and McCarthy get in? No. -

Fair Ball! Why Adjustments Are Needed

© Copyright, Princeton University Press. No part of this book may be distributed, posted, or reproduced in any form by digital or mechanical means without prior written permission of the publisher. CHAPTER 1 Fair Ball! Why Adjustments Are Needed King Arthur’s quest for it in the Middle Ages became a large part of his legend. Monty Python and Indiana Jones launched their searches in popular 1974 and 1989 movies. The mythic quest for the Holy Grail, the name given in Western tradition to the chal- ice used by Jesus Christ at his Passover meal the night before his death, is now often a metaphor for a quintessential search. In the illustrious history of baseball, the “holy grail” is a ranking of each player’s overall value on the baseball diamond. Because player skills are multifaceted, it is not clear that such a ranking is possible. In comparing two players, you see that one hits home runs much better, whereas the other gets on base more often, is faster on the base paths, and is a better fielder. So which player should rank higher? In Baseball’s All-Time Best Hitters, I identified which players were best at getting a hit in a given at-bat, calling them the best hitters. Many reviewers either disapproved of or failed to note my definition of “best hitter.” Although frequently used in base- ball writings, the terms “good hitter” or best hitter are rarely defined. In a July 1997 Sports Illustrated article, Tom Verducci called Tony Gwynn “the best hitter since Ted Williams” while considering only batting average. -

2017 Topps Dynasty Baseball Checklist

2017 Topps Dynasty Baseball Team Checklist No Rays - Padres - Royals Player Set Team Print Run Rod Carew Auto Dual Relic + 1/1 Parallel Angels 6 Albert Pujols Auto MLB Logo Patch Angels 1 Mike Trout Auto MLB Logo Patch Angels 1 Albert Pujols Auto Patch + Parallels Angels 16 Mike Trout Auto Patch + Parallels Angels 16 Rod Carew Auto Patch + Parallels Angels 16 Mike Trout Dual Player Auto Patch w/Bryant + 1/1 Parallel Angels 6 Mike Trout Dual Player Auto Patch w/Pujols + 1/1 Parallel Angels 6 Albert Pujols Dual Player Auto Patch w/Trout + 1/1 Parallel Angels 6 Alex Bregman Auto MLB Logo Patch Astros 1 Carlos Correa Auto MLB Logo Patch Astros 1 Craig Biggio Auto MLB Logo Patch Astros 1 Carlos Correa Auto On This Day Patch + 1/1 Parallel Astros 6 Carlos Correa Auto Patch (Puerto Rico) + Parallels Astros 16 Alex Bregman Auto Patch (USA) + Parallels Astros 16 Jose Altuve Auto Patch (Venezuela) + Parallels Astros 16 Alex Bregman Auto Patch + Parallels Astros 16 Andy Pettitte Auto Patch + Parallels Astros 16 Carlos Correa Auto Patch + Parallels Astros 16 Craig Biggio Auto Patch + Parallels Astros 16 George Springer Auto Patch + Parallels Astros 16 Jeff Bagwell Auto Patch + Parallels Astros 16 Jose Altuve Auto Patch + Parallels Astros 16 Nolan Ryan Auto Patch + Parallels Astros 16 Yulieski Gurriel Auto Patch + Parallels Astros 16 Joe Niekro Cut Auto Astros 1 Carlos Correa Dual Player Auto Patch w/Bregman + 1/1 Parallel Astros 6 Alex Bregman Dual Player Auto Patch w/Correa + 1/1 Parallel Astros 6 Mark McGwire Auto Patch + Parallels Athletics 16 -

DONNA LEINWAND: (Sounds Gavel.) Good Afternoon and Welcome to the National Press Club. My Name Is Donna Leinwand. I'm a Repor

NATIONAL PRESS CLUB LUNCHEON WITH JEFF IDELSON SUBJECT: JEFF IDELSON, PRESIDENT OF THE NATIONAL BASEBALL HALL OF FAME, IS SCHEDULED TO SPEAK AT A NATIONAL PRESS CLUB LUNCHEON MAY 11. HALL OF FAME THIRD BASEMAN BROOKS ROBINSON WILL BE A SPECIAL GUEST. MODERATOR: DONNA LEINWAND, PRESIDENT, NATIONAL PRESS CLUB LOCATION: NATIONAL PRESS CLUB BALLROOM, WASHINGTON, D.C. TIME: 1:00 P.M. EDT DATE: MONDAY, MAY 11, 2009 (C) COPYRIGHT 2009, NATIONAL PRESS CLUB, 529 14TH STREET, WASHINGTON, DC - 20045, USA. ALL RIGHTS RESERVED. ANY REPRODUCTION, REDISTRIBUTION OR RETRANSMISSION IS EXPRESSLY PROHIBITED. UNAUTHORIZED REPRODUCTION, REDISTRIBUTION OR RETRANSMISSION CONSTITUTES A MISAPPROPRIATION UNDER APPLICABLE UNFAIR COMPETITION LAW, AND THE NATIONAL PRESS CLUB. RESERVES THE RIGHT TO PURSUE ALL REMEDIES AVAILABLE TO IT IN RESPECT TO SUCH MISAPPROPRIATION. FOR INFORMATION ON BECOMING A MEMBER OF THE NATIONAL PRESS CLUB, PLEASE CALL 202-662-7505. DONNA LEINWAND: (Sounds gavel.) Good afternoon and welcome to the National Press Club. My name is Donna Leinwand. I’m a reporter at USA Today and I’m president of the National Press Club. We’re the world’s leading professional organization for journalists and are committed to a future of journalism by providing informative programming, journalism education and fostering a free press worldwide. For more information about the National Press Club, please visit our website at www.press.org. On behalf of our 3,500 members worldwide, I’d like to welcome our speaker and our guests in the audience today. I’d also like to welcome those of you who are watching us on C-Span. We’re looking forward to today’s speech, and afterwards, I’ll ask as many questions from the audience as time permits. -

Download Preview

DETROIT TIGERS’ 4 GREATEST HITTERS Table of CONTENTS Contents Warm-Up, with a Side of Dedications ....................................................... 1 The Ty Cobb Birthplace Pilgrimage ......................................................... 9 1 Out of the Blocks—Into the Bleachers .............................................. 19 2 Quadruple Crown—Four’s Company, Five’s a Multitude ..................... 29 [Gates] Brown vs. Hot Dog .......................................................................................... 30 Prince Fielder Fields Macho Nacho ............................................................................. 30 Dangerfield Dangers .................................................................................................... 31 #1 Latino Hitters, Bar None ........................................................................................ 32 3 Hitting Prof Ted Williams, and the MACHO-METER ......................... 39 The MACHO-METER ..................................................................... 40 4 Miguel Cabrera, Knothole Kids, and the World’s Prettiest Girls ........... 47 Ty Cobb and the Presidential Passing Lane ................................................................. 49 The First Hammerin’ Hank—The Bronx’s Hank Greenberg ..................................... 50 Baseball and Heightism ............................................................................................... 53 One Amazing Baseball Record That Will Never Be Broken ...................................... -

Tml American - Single Season Leaders 1954-2016

TML AMERICAN - SINGLE SEASON LEADERS 1954-2016 AVERAGE (496 PA MINIMUM) RUNS CREATED HOMERUNS RUNS BATTED IN 57 ♦MICKEY MANTLE .422 57 ♦MICKEY MANTLE 256 98 ♦MARK McGWIRE 75 61 ♦HARMON KILLEBREW 221 57 TED WILLIAMS .411 07 ALEX RODRIGUEZ 235 07 ALEX RODRIGUEZ 73 16 DUKE SNIDER 201 86 WADE BOGGS .406 61 MICKEY MANTLE 233 99 MARK McGWIRE 72 54 DUKE SNIDER 189 80 GEORGE BRETT .401 98 MARK McGWIRE 225 01 BARRY BONDS 72 56 MICKEY MANTLE 188 58 TED WILLIAMS .392 61 HARMON KILLEBREW 220 61 HARMON KILLEBREW 70 57 TED WILLIAMS 187 61 NORM CASH .391 01 JASON GIAMBI 215 61 MICKEY MANTLE 69 98 MARK McGWIRE 185 04 ICHIRO SUZUKI .390 09 ALBERT PUJOLS 214 99 SAMMY SOSA 67 07 ALEX RODRIGUEZ 183 85 WADE BOGGS .389 61 NORM CASH 207 98 KEN GRIFFEY Jr. 67 93 ALBERT BELLE 183 55 RICHIE ASHBURN .388 97 LARRY WALKER 203 3 tied with 66 97 LARRY WALKER 182 85 RICKEY HENDERSON .387 00 JIM EDMONDS 203 94 ALBERT BELLE 182 87 PEDRO GUERRERO .385 71 MERV RETTENMUND .384 SINGLES DOUBLES TRIPLES 10 JOSH HAMILTON .383 04 ♦ICHIRO SUZUKI 230 14♦JONATHAN LUCROY 71 97 ♦DESI RELAFORD 30 94 TONY GWYNN .383 69 MATTY ALOU 206 94 CHUCK KNOBLAUCH 69 94 LANCE JOHNSON 29 64 RICO CARTY .379 07 ICHIRO SUZUKI 205 02 NOMAR GARCIAPARRA 69 56 CHARLIE PEETE 27 07 PLACIDO POLANCO .377 65 MAURY WILLS 200 96 MANNY RAMIREZ 66 79 GEORGE BRETT 26 01 JASON GIAMBI .377 96 LANCE JOHNSON 198 94 JEFF BAGWELL 66 04 CARL CRAWFORD 23 00 DARIN ERSTAD .376 06 ICHIRO SUZUKI 196 94 LARRY WALKER 65 85 WILLIE WILSON 22 54 DON MUELLER .376 58 RICHIE ASHBURN 193 99 ROBIN VENTURA 65 06 GRADY SIZEMORE 22 97 LARRY -

Almost a Pelican

Almost A Pelican By S. Derby Gisclair The winningest pitcher in Cleveland Indians history, in 1962 Feller became the first pitcher since charter member Walter Johnson to be elected to the Hall of Fame in his first year of eligibility. Though regarded as the fastest pitcher of his day, he himself attributed his strikeout records to his curve and slider. Blessed with a strong arm and an encouraging father, young Feller pitched to a makeshift backstop on the family farm near Van Meter, Iowa. Cleveland scout Cy Slapnicka signed him for one dollar and an autographed baseball. His velocity became an immediate legend when he struck out eight Cardinals in a three-inning exhibition stint. He came up as a 17- year-old at the end of 1936 and fanned 15 Browns in his first ML start and 17 Athletics shortly thereafter. But he was extremely wild. In 1938 he became a regular starter for the Indians. He won 17 and led the AL in strikeouts with 240. He also set a ML record with 208 walks. Although he led the AL in walks three more times, his control progressively improved. Meanwhile, he led the AL in both strikeouts and wins from 1939 to 1941. In 1940, he won his personal high with 27, including an Opening Day no-hitter against the White Sox. Yet the year was tarnished, first when Cleveland veterans, including Feller, earned the nickname Crybabies by asking Cleveland owner Alva Bradley to replace stern manager Ossie Vitt. Then Feller lost the season's climactic game and the pennant to Tigers unknown Floyd Giebell, despite pitching a three-hitter. -

Baseball Classics All-Time All-Star Greats Game Team Roster

BASEBALL CLASSICS® ALL-TIME ALL-STAR GREATS GAME TEAM ROSTER Baseball Classics has carefully analyzed and selected the top 400 Major League Baseball players voted to the All-Star team since it's inception in 1933. Incredibly, a total of 20 Cy Young or MVP winners were not voted to the All-Star team, but Baseball Classics included them in this amazing set for you to play. This rare collection of hand-selected superstars player cards are from the finest All-Star season to battle head-to-head across eras featuring 249 position players and 151 pitchers spanning 1933 to 2018! Enjoy endless hours of next generation MLB board game play managing these legendary ballplayers with color-coded player ratings based on years of time-tested algorithms to ensure they perform as they did in their careers. Enjoy Fast, Easy, & Statistically Accurate Baseball Classics next generation game play! Top 400 MLB All-Time All-Star Greats 1933 to present! Season/Team Player Season/Team Player Season/Team Player Season/Team Player 1933 Cincinnati Reds Chick Hafey 1942 St. Louis Cardinals Mort Cooper 1957 Milwaukee Braves Warren Spahn 1969 New York Mets Cleon Jones 1933 New York Giants Carl Hubbell 1942 St. Louis Cardinals Enos Slaughter 1957 Washington Senators Roy Sievers 1969 Oakland Athletics Reggie Jackson 1933 New York Yankees Babe Ruth 1943 New York Yankees Spud Chandler 1958 Boston Red Sox Jackie Jensen 1969 Pittsburgh Pirates Matty Alou 1933 New York Yankees Tony Lazzeri 1944 Boston Red Sox Bobby Doerr 1958 Chicago Cubs Ernie Banks 1969 San Francisco Giants Willie McCovey 1933 Philadelphia Athletics Jimmie Foxx 1944 St. -

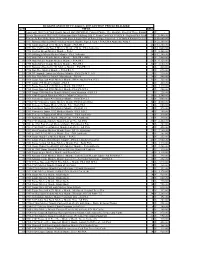

PDF of August 17 Results

HUGGINS AND SCOTT'S August 3, 2017 AUCTION PRICES REALIZED LOT# TITLE BIDS 1 Landmark 1888 New York Giants Joseph Hall IMPERIAL Cabinet Photo - The Absolute Finest of Three Known Examples6 $ [reserve - not met] 2 Newly Discovered 1887 N693 Kalamazoo Bats Pittsburg B.B.C. Team Card PSA VG-EX 4 - Highest PSA Graded &20 One$ 26,400.00of Only Four Known Examples! 3 Extremely Rare Babe Ruth 1939-1943 Signed Sepia Hall of Fame Plaque Postcard - 1 of Only 4 Known! [reserve met]7 $ 60,000.00 4 1951 Bowman Baseball #253 Mickey Mantle Rookie Signed Card – PSA/DNA Authentic Auto 9 57 $ 22,200.00 5 1952 Topps Baseball #311 Mickey Mantle - PSA PR 1 40 $ 12,300.00 6 1952 Star-Cal Decals Type I Mickey Mantle #70-G - PSA Authentic 33 $ 11,640.00 7 1952 Tip Top Bread Mickey Mantle - PSA 1 28 $ 8,400.00 8 1953-54 Briggs Meats Mickey Mantle - PSA Authentic 24 $ 12,300.00 9 1953 Stahl-Meyer Franks Mickey Mantle - PSA PR 1 (MK) 29 $ 3,480.00 10 1954 Stahl-Meyer Franks Mickey Mantle - PSA PR 1 58 $ 9,120.00 11 1955 Stahl-Meyer Franks Mickey Mantle - PSA PR 1 20 $ 3,600.00 12 1952 Bowman Baseball #101 Mickey Mantle - PSA FR 1.5 6 $ 480.00 13 1954 Dan Dee Mickey Mantle - PSA FR 1.5 15 $ 690.00 14 1954 NY Journal-American Mickey Mantle - PSA EX-MT+ 6.5 19 $ 930.00 15 1958 Yoo-Hoo Mickey Mantle Matchbook - PSA 4 18 $ 840.00 16 1956 Topps Baseball #135 Mickey Mantle (White Back) PSA VG 3 11 $ 360.00 17 1957 Topps #95 Mickey Mantle - PSA 5 6 $ 420.00 18 1958 Topps Baseball #150 Mickey Mantle PSA NM 7 19 $ 1,140.00 19 1968 Topps Baseball #280 Mickey Mantle PSA EX-MT -

Atlanta Braves Clippings Wednesday, May 6, 2020 Braves.Com

Atlanta Braves Clippings Wednesday, May 6, 2020 Braves.com Braves' Top 5 center fielders: Bowman's take By Mark Bowman No one loves a good debate quite like baseball fans, and with that in mind, we asked each of our beat reporters to rank the top five players by position in the history of their franchise, based on their career while playing for that club. These rankings are for fun and debate purposes only … if you don’t agree with the order, participate in the Twitter poll to vote for your favorite at this position. Here is Mark Bowman’s ranking of the top 5 center fielders in Braves history. Next week: Right fielders. 1. Andruw Jones, 1996-2007 Key fact: Stands with Roberto Clemente, Willie Mays and Ichiro Suzuki as the only outfielders to win 10 consecutive Gold Glove Awards The 60.9 bWAR (Baseball Reference’s WAR model) Andruw Jones produced during his 11 full seasons (1997-2007) with Atlanta ranked third in the Majors, trailing only Alex Rodriguez (85.7) and Barry Bonds (79.2). Chipper Jones was fourth at 58.9. Within this span, the Braves center fielder led all Major Leaguers with a 26.7 Defensive bWAR. Hall of Fame catcher Ivan Rodriguez ranked second with 16.5. The next closest outfielder was Mike Cameron (9.6). Along with establishing himself as one of the greatest defensive outfielders baseball has ever seen during his time with Atlanta, Jones became one of the best power hitters in Braves history. He ranks fourth in franchise history with 368 homers, and he set the club’s single-season record with 51 homers in 2005. -

July Birthdays Cow Chips KARE-11 to Feature Area Ballparks Arpi

July 2000 Arpi Continues Bibliography Work KARE-11 to Feature Area Ballparks Rich Arpi continues to prepare Current Baseball Following the All-Star Game on Tuesday, July 11, the Publications, the quarterly newsletter of the SABR KARE-TV (Channel 11) news will have a feature on Bibliography Committee. It contains a list of recently Nicollet and Lexington parks, homes of the Minneapolis published books and magazines on baseball. The news- Millers and St. Paul Saints. The talking heads on the letter is free to all committee members, and all issues segment will include Rich Arpi and your scribe. since 1995 can be viewed on the SABR web page at: http://www.sabr.org/cbp.shtml Chapter Profiles Rich Wolf is hoping to come off the 60-day disabled Cow Chips list after a year-and-a-half of being ill and going through Glenn Gostick was featured in an article on Dick two surgeries last summer. Rich has been a lifelong Cassidy in the Saturday, May 13, 2000 Star Tribune, baseball fan. He was batboy for the St. John’s Newspaper of the Twin Cities. “No one knows and University baseball team, for which his brother played, loves the game more than him,” Cassidy said of Gos. when he was nine. Rich later played high school base- . Roger Godin went to Ottawa for the Society for ball and town ball in Long Prairie. His two great thrills in International Hockey Research convention and made a baseball were touring the Hall of Fame and seeing two presentation on the 1915-16 St. -

John E. Allen, Inc. Jea 1B01

JOHN E. ALLEN, INC. JEA 1B01 - BASEBALL <01/95> [u-bit #39015200] 1464-1-4 01:01:09 1) “Baseball - Opening Of Ebbets Field - Brooklyn, N.Y.” (S) Sports: Baseball -01:02:05 - American flag being raised, players in uniforms standing at base -2- of flag, men wearing hats outside stadium with newsboys in foreground, first ball about to be thrown out from stands by VIP wearing overcoat and hat, players warming up by throwing balls with one player in foreground catching balls without glove, HA game action on infield with player hitting double...then hitter making third out leaving runner on third (1913) [Universal Animated Weekly] 01:02:06 2) “The Grand Parade And Flag Raising” (N) Sports: Baseball - -01:02:50 - parade of players walking abreast onto field, U.S. flag Misc. -1- being raised, players walking abreast on field [section] [Kinograms] [also worse transfer below 01:47:38- 01:48:14] 01:02:54 3) Brooklyn Nationals spring training camp in Clearwater, Fl. - (N) Sports: Baseball - -01:04:05 pitcher throwing to batter who pops up, CS manager Robertson 1922-25 in suit and tie behind batting cage, batter hitting grounder to third, [also below 1st baseman throwing ball, coach Ben Egan showing rookies a ball, 02:07:11-02:08:16] Dick Cox catching ball in outfield and throwing it, Jacques Fournier catching and throwing ball, Dazzy Vance posing for photographer with large still camera, players coming off field in through door, owner Ebbets and wife in stands talking to manager Robertson, player hitting ball to line of infielders (1924) [Kinograms] 01:04:09 4) PAN of crowd and players warming up at game in small town (N) Sports: Baseball with autos parked near field, game action with giant wheel for [also see 1B10 fireworks in background, crowd in stands, people waving from on 16:06:10-16:08:37] top of house, boys looking underneath gate through peepholes (Pennsylvania 1912-14? written on leader - may be in Uniontown, PA) 01:06:57 large crowd onto field after game, three Cardinal pitchers warming up -01:07:15 (4th of July) 1B01 -2- JOHN E.