Private Equity & Venture Capital in a Changing Global Environment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FORM 8-K Walmart Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 ________________________ FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of Report (Date of earliest event reported): June 4, 2018 Walmart Inc. (Exact Name of Registrant as Specified in Charter) Delaware 001-06991 71-0415188 (State or Other Jurisdiction of Incorporation) (Commission File Number) (IRS Employer Identification No.) 702 Southwest 8th Street Bentonville, Arkansas 72716-0215 (Address of Principal Executive Offices) (Zip code) Registrant’s telephone number, including area code: (479) 273-4000 Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). Emerging growth company ¨ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. -

How Will Financial Services Private Equity Investments Fare in the Next Recession?

How Will Financial Services Private Equity Investments Fare in the Next Recession? Leading funds are shifting to balance-sheet-light and countercyclical investments. By Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith Tim Cochrane, Justin Miller, Michael Cashman and Mike Smith are partners with Bain & Company’s Financial Services and Private Equity practices. They are based, respectively, in London, New York, Boston and London. Copyright © 2019 Bain & Company, Inc. All rights reserved. How Will Financial Services Private Equity Investments Fare in the Next Recession? At a Glance Financial services deals in private equity have grown on the back of strong returns, including a pooled multiple on invested capital of 2.2x in recent years, higher than all but healthcare and technology deals. With a recession increasingly likely during the next holding period, PE funds need to develop plans to weather any storm and potentially improve their competitive position during and after the downturn. Many leading funds are investing in balance-sheet-light assets enabled by technology and regulatory change. Diligences now should test target companies under stressful economic scenarios and lay out a detailed value-creation plan, including how to mobilize quickly after acquisition. Financial services deals by private equity funds have had a strong run over the past few years, with deal value increasing significantly in Europe and the US(see Figure 1). Returns have been strong as well. Global financial services deals realized a pooled multiple on invested capital of 2.2x from 2009 through 2015, higher than all but healthcare and technology deals (see Figure 2). -

Corporate Governance Positions and Responsibilities of the Directors and Nominees to the Board of Directors

CORPORATE GOVERNANCE POSITIONS AND RESPONSIBILITIES OF THE DIRECTORS AND NOMINEES TO THE BOARD OF DIRECTORS LIONEL ZINSOU -DERLIN (a) Born on October 23, 1954 Positions and responsibilities as of December 31, 2014 Age: 60 Positions Companies Countries Director (term of office DANONE SA (b) France from April 29, 2014 to the end of the Shareholders’ Meeting to approve the 2016 financial statements) Chairman and Chair- PAI PARTNERS SAS France man of the Executive Business address: Committee 232, rue de Rivoli – 75001 Paris – France Member of the Number of DANONE shares held Investment Committee as of December 31, 2014: 4,000 Director INVESTISSEURS & PARTENAIRES Mauritius Independent Director I&P AFRIQUE ENTREPRENEURS Mauritius Dual French and Beninese nationality KAUFMAN & BROAD SA (b) France PAI SYNDICATION GENERAL PARTNER LIMITED Guernsey Principal responsibility: Chairman of PAI partners SAS PAI EUROPE III GENERAL PARTNER LIMITED Guernsey Personal backGround – PAI EUROPE IV GENERAL PARTNER LIMITED Guernsey experience and expertise: Lionel ZINSOU-DERLIN, of French and Beninese PAI EUROPE V GENERAL PARTNER LIMITED Guernsey nationality, is a graduate from the Ecole Normale PAI EUROPE VI GENERAL PARTNER LIMITED Guernsey Supérieure (Ulm), the London School of Economics and the Institut d’Etudes Politiques of Paris. He holds Chairman and Member LES DOMAINES BARONS DE ROTHSCHILD SCA France a master degree in Economic History and is an Asso- of the Supervisory (LAFITE) ciate Professor in Social Sciences and Economics. Board Member of the Advisory MOET HENNESSY France He started his career as a Senior Lecturer and Pro- Council fessor of Economics at Université Paris XIII. Member of the CERBA EUROPEAN LAB SAS France From 1984 to 1986, he became an Advisor to the French Supervisory Board Ministry of Industry and then to the Prime Minister. -

Private Debt in Asia: the Next Frontier?

PRIVATE DEBT IN ASIA: THE NEXT FRONTIER? PRIVATE DEBT IN ASIA: THE NEXT FRONTIER? We take a look at the fund managers and investors turning to opportunities in Asia, analyzing funds closed and currently in market, as well as the investors targeting the region. nstitutional investors in 2018 are have seen increased fundraising success in higher than in 2016. While still dwarfed Iincreasing their exposure to private recent years. by the North America and Europe, Asia- debt strategies at a higher rate than focused fundraising has carved out a ever before, with many looking to both 2017 was a strong year for Asia-focused significant niche in the global private debt diversify their private debt portfolios and private debt fundraising, with 15 funds market. find less competed opportunities. Beyond reaching a final close, raising an aggregate the mature and competitive private debt $6.4bn in capital. This is the second highest Sixty percent of Asia-focused funds closed markets in North America and Europe, amount of capital raised targeting the in 2017 met or exceeded their initial target credit markets in Asia offer a relatively region to date and resulted in an average size including SSG Capital Partners IV, the untapped reserve of opportunity, and with fund size of $427mn. Asia-focused funds second largest Asia-focused fund to close the recent increase in investor interest accounted for 9% of all private debt funds last year, securing an aggregate $1.7bn, in this area, private debt fund managers closed in 2017, three-percentage points 26% more than its initial target. -

A Listing of PSERS' Investment Managers, Advisors, and Partnerships

Pennsylvania Public School Employees’ Retirement System Roster of Investment Managers, Advisors, and Consultants As of March 31, 2015 List of PSERS’ Internally Managed Investment Portfolios • Bloomberg Commodity Index Overlay • Gold Fund • LIBOR-Plus Short-Term Investment Pool • MSCI All Country World Index ex. US • MSCI Emerging Markets Equity Index • Risk Parity • Premium Assistance • Private Debt Internal Program • Private Equity Internal Program • Real Estate Internal Program • S&P 400 Index • S&P 500 Index • S&P 600 Index • Short-Term Investment Pool • Treasury Inflation Protection Securities • U.S. Core Plus Fixed Income • U.S. Long Term Treasuries List of PSERS’ External Investment Managers, Advisors, and Consultants Absolute Return Managers • Aeolus Capital Management Ltd. • AllianceBernstein, LP • Apollo Aviation Holdings Limited • Black River Asset Management, LLC • BlackRock Financial Management, Inc. • Brevan Howard Asset Management, LLP • Bridgewater Associates, LP • Brigade Capital Management • Capula Investment Management, LLP • Caspian Capital, LP • Ellis Lake Capital, LLC • Nephila Capital, Ltd. • Oceanwood Capital Management, Ltd. • Pacific Investment Management Company • Perry Capital, LLC U.S. Equity Managers • AH Lisanti Capital Growth, LLC Pennsylvania Public School Employees’ Retirement System Page 1 Publicly-Traded Real Estate Securities Advisors • Security Capital Research & Management, Inc. Non-U.S. Equity Managers • Acadian Asset Management, LLC • Baillie Gifford Overseas Ltd. • BlackRock Financial Management, Inc. • Marathon Asset Management Limited • Oberweis Asset Management, Inc. • QS Batterymarch Financial Management, Inc. • Pyramis Global Advisors • Wasatch Advisors, Inc. Commodity Managers • Black River Asset Management, LLC • Credit Suisse Asset Management, LLC • Gresham Investment Management, LLC • Pacific Investment Management Company • Wellington Management Company, LLP Global Fixed Income Managers U.S. Core Plus Fixed Income Managers • BlackRock Financial Management, Inc. -

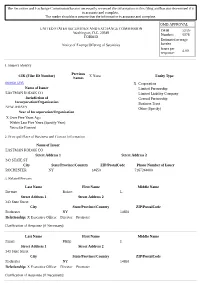

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

Knowledgenow Conference Pressure Points October 2017 What’S Inside?

KnowledgeNow Conference Pressure Points October 2017 What’s inside? THE INSIDE-OUT VIEW Tackling today’s biggest threats to business 02 Time, talent and energy Driving Sales Effectiveness Digital transformation At Boats Group Amazon The elephant in every room Invent Farma A smooth transition Unilabs A transformation story THE OUTSIDE-IN VIEW Global leaders provide perspective 10 Disjointed environments The rising tide of populism Globalization under attack Addressing the challenge 16 Who’s who? 18 The Operational Excellence team 20 References Introduction Pressure Points The theme of our seventh annual KnowledgeNow Conference, “Pressure Points”, explored the th complex combination annual of internal and external KnowledgeNow 7 forces that executives must navigate to evolve and grow their enterprise. The event combines the open sharing of knowledge between the Apax Funds’ portfolio companies in attendance with the tools and experience of the Operational Excellence Practice (OEP) to generate actionable insights. Apax Partners 01 Driving growth through operational excellence “Benign economic conditions, a plentiful supply of financing and record stock-markets have driven corporate valuations on both sides of the Atlantic to unsurpassed levels. Against this backdrop, the ability to materially accelerate portfolio growth is a crucial factor in driving returns.” Andrew Sillitoe Co-CEO, Apax Partners Operational improvements have accounted for circa The fact that the OEP has been our % fastest-growing team in recent years is real proof of the -

VP for VC and PE.Indd

EUROPEAN VENTURE PHILANTHROPY ASSOCIATION A guide to Venture PhilAnthroPy for Venture Capital and Private Equity investors Ashley Metz CummingS and Lisa Hehenberger JUNE 2011 2 A guidE to Venture Philanthropy for Venture Capital and Private Equity investors LETTER fROM SERgE RAICHER 4 Part 2: PE firms’ VP engAgement 20 ContentS Executive Summary 6 VC/PE firms and Philanthropy PART 1: Introduction 12 Models of engagement in VP Purpose of the document Model 1: directly support Social Purpose Organisations Essence and Role of Venture Philanthropy Model 2: Invest in or co-invest with a VP Organisation Venture Philanthropy and Venture Capital/Private Equity Model 3: found or co-found a VP Organisation Published by the European Venture Philanthropy Association This edition June 2011 Copyright © 2011 EVPA Email : [email protected] Website : www.evpa.eu.com Creative Commons Attribution-Noncommercial-No derivative Works 3.0 You are free to share – to copy, distribute, display, and perform the work – under the following conditions: Attribution: You must attribute the work as A gUIdE TO VENTURE PHILANTHROPY fOR VENTURE CAPITAL ANd PRIVATE EqUITY INVESTORS Copyright © 2011 EVPA. Non commercial: You may not use this work for commercial purposes. No derivative Works: You may not alter, transform or build upon this work. for any reuse or distribution, you must make clear to others the licence terms of this work. ISbN 0-9553659-8-8 Authors: Ashley Metz Cummings and dr Lisa Hehenberger Typeset in Myriad design and typesetting by: Transform, 115b Warwick Street, Leamington Spa CV32 4qz, UK Printed and bound by: drukkerij Atlanta, diestsebaan 39, 3290 Schaffen-diest, belgium This book is printed on fSC approved paper. -

Joshua Smith

Joshua Smith Associate London | 160 Queen Victoria Street, London, UK EC4V 4QQ T +44 20 7184 7824 | F +44 20 7184 7001 [email protected] Services Mergers and Acquisitions > Private Equity > Corporate Finance and Capital Markets > Corporate Governance > Joshua Smith practices in the area of corporate law, advising on a wide range of domestic and cross-border mergers and acquisitions, private equity transactions, joint ventures, fundraisings, public offerings, reorganisations and other general corporate matters. Mr. Smith trained at Dechert and qualified as a solicitor in 2014. EXPERIENCE Hellenic Telecommunications Organization S.A (OTE) in connection with the sale of its stake in fixed telecommunications operator Telekom Romania for €268 million to Orange Romania. ICTS International N.V. and ABC Technologies B.V. on (i) a US$60 million equity investment by an affiliate of TPG Global into ABC, a subsidiary of ICTS and the owner of Au10tix Limited, a leader in the ID documentation and know-your-customer on- boarding automation software industry and (ii) a further US$20 million equity investment by Oak HC/FT into ABC and related shareholder agreements. The transactions valued Au10tix at US$280 million. A substantial family office as investor in a substantive venture investment in a UK ticketing and events hosting company. Centaur Media plc, as part of its strategic divestment program on the sale of (i) its financial services division to Metropolis Group; (ii) Centaur Human Resources Limited, to DVV Media International Ltd; (iii) Centaur Media Travel and Meetings Limited, to Northstar Travel Media UK Limited; and (iv) its engineering portfolio, including The Engineer and Subcon, to Mark Allen Group. -

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

HELLAS TELECOMMUNICATIONS (LUXEMBOURG) II SCA Case No

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: Chapter 15 HELLAS TELECOMMUNICATIONS (LUXEMBOURG) II SCA Case No. 12-10631 (MG) Debtor in a Foreign Proceeding. ANDREW LAWRENCE HOSKING and BRUCE MACKAY, in Adv. Pro. No. 14-01848 (MG) their capacity as joint compulsory liquidators and duly authorized foreign representatives of HELLAS TELECOMMUNICATIONS (LUXEMBOURG) II SCA, Plaintiffs, -against- TPG CAPITAL MANAGEMENT, L.P., f/k/a TPG CAPITAL, L.P., and APAX PARTNERS, L.P., on behalf of themselves, -and- DAVID BONDERMAN, JAMES COULTER, WILLIAM S. PRICE III, TPG ADVISORS IV, INC., TPG GENPAR IV, L.P., TPG PARTNERS IV, L.P., T3 ADVISORS II, INC., T3 GENPAR II, L.P., T3 PARTNERS II, L.P., T3 PARALLEL II, L.P., TPG FOF IV, L.P., TPG FOF IV-QP, L.P., TPG EQUITY IV-A, L.P., f/k/a FIRST AMENDED COMPLAINT TPG EQUITY IV, L.P., TPG MANAGEMENT IV-B, L.P., TPG COINVESTMENT IV, L.P., TPG ASSOCIATES IV, L.P., TPG MANAGEMENT IV, L.P., TPG MANAGEMENT III, L.P., BONDERMAN FAMILY LIMITED PARTNERSHIP, BONDO-TPG PARTNERS III, L.P., DICK W. BOYCE, KEVIN R. BURNS, JUSTIN CHANG, JONATHAN COSLET, KELVIN DAVIS, ANDREW J. DECHET, JAMIE GATES, MARSHALL HAINES, JOHN MARREN, MICHAEL MACDOUGALL, THOMAS E. REINHART, RICHARD SCHIFTER, TODD B. SISITSKY, BRYAN M. TAYLOR, CARRIE A. WHEELER, JAMES B. WILLIAMS, JOHN VIOLA, TCW/CRESCENT MEZZANINE PARTNERS III NETHERLANDS, L.P., a/k/a TCW/CRESCENT MEZZANINE PARTNERS NETHERLANDS III, L.P., TCW/CRESCENT MEZZANINE PARTNERS III, L.P., a/k/a TCW/CRESCENT MEZZANINE FUND III, L.P., TCW/CRESCENT MEZZANINE TRUST III, TCW/CRESCENT MEZZANINE III, LLC, TCW CAPITAL INVESTMENT CORPORATION, DEUTSCHE BANK AG, and DOES 1-25, on behalf of themselves and a class of similarly situated persons and legal entities, Defendants. -

TRS Contracted Investment Managers

TRS INVESTMENT RELATIONSHIPS AS OF DECEMBER 2020 Global Public Equity (Global Income continued) Acadian Asset Management NXT Capital Management AQR Capital Management Oaktree Capital Management Arrowstreet Capital Pacific Investment Management Company Axiom International Investors Pemberton Capital Advisors Dimensional Fund Advisors PGIM Emerald Advisers Proterra Investment Partners Grandeur Peak Global Advisors Riverstone Credit Partners JP Morgan Asset Management Solar Capital Partners LSV Asset Management Taplin, Canida & Habacht/BMO Northern Trust Investments Taurus Funds Management RhumbLine Advisers TCW Asset Management Company Strategic Global Advisors TerraCotta T. Rowe Price Associates Varde Partners Wasatch Advisors Real Assets Transition Managers Barings Real Estate Advisers The Blackstone Group Citigroup Global Markets Brookfield Asset Management Loop Capital The Carlyle Group Macquarie Capital CB Richard Ellis Northern Trust Investments Dyal Capital Penserra Exeter Property Group Fortress Investment Group Global Income Gaw Capital Partners AllianceBernstein Heitman Real Estate Investment Management Apollo Global Management INVESCO Real Estate Beach Point Capital Management LaSalle Investment Management Blantyre Capital Ltd. Lion Industrial Trust Cerberus Capital Management Lone Star Dignari Capital Partners LPC Realty Advisors Dolan McEniry Capital Management Macquarie Group Limited DoubleLine Capital Madison International Realty Edelweiss Niam Franklin Advisers Oak Street Real Estate Capital Garcia Hamilton & Associates