Prospectus (The “Prospectus”)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Consolidated Financial Statements As of December 31, 2018

Consolidated Financial Statements as of December 31, 2018 We hereby present to you the annual financial report for the fiscal year ended on December 31, 2018, prepared in accordance with the provisions of Articles L. 451-1-2 III of the French Monetary and Financial Code and 222- 4 et seq. of the General Regulations of the French Financial Markets Regulator (AMF). This report shall be shared in accordance with the provisions of Article 221-3 of the General Regulations of the AMF. In particular, it shall be available on the website of our company, www.mediawan.com. Contents 1. Consolidated Income Statement ................................................................................................... 4 2. Consolidated Statement of Comprehensive Income...................................................................... 5 3. Consolidated Financial Position .................................................................................................... 6 4. Table of Consolidated Cash Flow ................................................................................................... 7 5. Consolidated Variation of Equity................................................................................................... 8 6. Mediawan Group .......................................................................................................................... 9 6.1. Activities of the Group ........................................................................................................................ 9 6.2. Significant -

Xavier NIEL, Un Empire Économique Et Médiatique

INFOGRAPHIES OJIM Xavier NIEL, un empire économique et médiatique Mars 2020 1991 Acquisition de FERMIC MULTIMÉDIA, éditeur de services du MINITEL ROSE, rebaptisé ILIAD 1998 1993 Vente du MINITEL ROSE Création de WORLDNET, 1999 premier fournisseur d’accès Création de FREE, internet en France fournisseur d’accès Internet 2004 2008 Introduction en bourse Rachat d’ALICE ADSL. de FREE Devient le N°2 du marché Mise en examen pour des fournisseurs d’accès 2006 recel d’abus de biens internet (26% des parts) sociaux et proxénétisme Condamnation pour recel d’abus de biens sociaux à : • 2 ans de prison avec sursis 2005 Janvier 2008 • 250 000 euros d’amende Capitalisation de 2,3 milliards Création de l’offre • 188 667 euros de dommages d’euros pour FREE/ILIAD FREE Mobile 3G et intérêts Ordonnance de non-lieu INFOGRAPHIES OJIMpour proxénétisme Juillet 2013 Décembre 2013 Inauguration du “42“ FREE annonce la 4G Avril 2014 incluse dans le forfait d’entrée l’école du numérique Rachat de 55% de gamme à 2 € fondée par NIEL de MONACO TELECOM Juillet 2014 ILIAD rachete 56,6% du capital de T-MOBILE US, 4e opérateur américain Mai 2018 Juin 2016 2017 Lancement du réseau mobile Investissement de 5M°€ Décembre 2014 ILIAD en Italie le plaçant Acquisition de 31,6% dans BLACKPILLS, Rachat de ORANGE SUISSE au 4e rang de la téléphonie de EIR, l’opérateur une plate-forme vidéo pour via sa holding NJJ CAPITAL mobile dans la péninsule historique irlandais mobiles, avec Luc BESSON qui devient SALT Xavier NIEL | 1. Du Minitel rose à la téléphonie mobile Mars 2020 FORMATION -

CHALLENGES | Survival Is Success Nicola Bruno and Rasmus Kleis Nielsen

Bruno Neilson cover_Layout 1 04/04/2012 10:28 Page 1 R I S REUTERS J C INSTITUTE for the REUTERS H A STUDY of L INSTITUTE for the L E JOURNALISM N CHALLENGES STUDY of G E JOURNALISM S | S u All around Europe, new journalistic ventures are launched on the internet r Survival is Success v even as legacy media like newspapers and broadcasters are oen struggling to i v adapt to a new communications environment. is report is the first to a l Journalistic Online Start-Ups in systematically assess how they are doing. Based on analysis of nine strategic i s cases from Germany, France, and Italy, it shows that the economics of online S u news today are as challenging for new entrants as they are for industry c Western Europe c incumbents. ough internet use and online advertising is growing rapidly e s across Europe, it is not clear that this alone will provide the basis for new s forms of journalism. Two challenges loom particularly large for all the ventures examined here. First, the market for online news continues to be dominated by legacy media organisations. Second, the market for online advertising is generously supplied and dominated by a few very large players. Nicola Bruno and Rasmus Kleis Nielsen ere are examples of journalistic start-ups that have managed to break even despite these challenges, but they are in a minority. While many new initiatives are inspiring in their journalistic idealism and impressive in their technical inventiveness, most struggle to make ends meet financially. -

Thomas Anargyros Appointed CEO of Mediawan Studio, a New Entity Gathering Mediawan’S French Drama Production Companies

Thomas Anargyros appointed CEO of Mediawan Studio, a new entity gathering Mediawan’s French drama production companies Paris, July 15th, 2020 – Mediawan announces today that Thomas Anargyros (until now CEO of Storia Television, a Mediawan Group company) has been appointed as CEO of Mediawan Studio, a new entity within its Mediawan Originals unit which will bring together the Group’s French drama production companies. He will supervise and coordinate the activities of the Mediawan Studio companies and develop their international coproduction projects, so as to implement an ambitious development strategy of drama production for all broadcasters and SVOD platforms. He will be supported by two COOs: Dominik Schmelck, currently Managing Director of Makever (another Mediawan Group company) and Matthieu Thollin, currently COO of Storia Television. “I am very happy to be able to count on Thomas’ renowned talent and experience to develop and coordinate the activities of our French drama production companies, and lead the Group’s ambition on that segment,” declared Pierre-Antoine Capton, Chairman of the Board of Mediawan. Thanks to an ambitious portfolio of franchises (like “The Red Bracelets”, “Call My Agent”, “The Crimson Rivers”, “Alice Nevers” or “Savages”), Mediawan has been leading the ranking of French prime-time drama producers (published by Ecran Total magazine) since 2017. Thomas Anargyros Thomas Anargyros is CEO of Storia Television which for many years has been developing an ambitious production strategy in terms of French and international prime time drama. Before that, Thomas Anargyros was Chairman of Cipango then of Europacorp Television France and USA where he produced many series including large international projects like “XIII” (with Val Kilmer and Stephen Dorff) for Canal+, M6 and NBC, distributed on over 160 territories, or the 26 episodes of the US series “Taken”, in coproduction with Universal for NBC. -

Matthieu PIGASSE L’Homme De Toutes Les Situations

INFOGRAPHIES OJIM Matthieu PIGASSE l’homme de toutes les situations Mai 2020 SES RELATIONS SES ACTIONS > Re-négociation de la dette de l’Argentine Matthieu > Vente de LIBÉRATION PIGASSE à Édouard de ROTSCHIELD Alain MINC Daniel COHEN > Re-négociation de la dette irakienne • Conseiller politique • Économiste • Ex-Président du • Conseiller de la banque LAZARD > Nationalisation Conseil de Surveillance • Membre du Conseil du gaz bolivien de la Société des de Surveillance du MONDE > Vente du PSG par CANAL+ Lecteurs du MONDE • Président du Conseil • Président d’AM Conseil Scientifique de la FONDATION > Fusion et de SANEF JEAN JAURÈS SUEZ-GAZ DE FRANCE > Vente de l’activité de transmission et de distribution d’AREVA > Vente par ACCOR de sa participation dans le CLUB MED Xavier NIEL Claude PERDRIEL • Propriétaire-AssociéINFOGRAPHIES • Propriétaire de Banque OJIM> Vente d’AB Groupe à TF1 du Groupe LE MONDE RUE89 LAZARD > Conseil auprès de • Propriétaire du groupe • Partenaire dans G. PAPANDREOU de presse MEDIAWAN dans la résolution SOPHIA PUBLICATIONS 2002 • Débuts en tant qu’associé gérant de la crise grecque > Fusion 2010 CAISSE D’ÉPARGNE- • DG de la banque LAZARD France BANQUE POPULAIRE 2015 > Acquisition de DARTY • Responsable mondial par la FNAC Pierre-Antoine CAPTON Bruno ROGER des activités de fusion-acquisition • Président fondateur de Président de LAZARD 2019 TROISIÈME ŒIL Paris à l’origine • Responsable mondial de LAZARD PRODUCTIONS du recrutement • Fin octobre : DÉMISSION ! Membre du CA de PIGASSE • Président du Directoire • Groupe Lucien BARRIÈRE 2020 AUTRES MEDIAWAN, groupe de • Groupe DERICHEBOURG médias créé en 2017 • Prend la direction de l’implantation en • BskyB avec Xavier NIEL France de CENTERVIEW, une banque d’affaires américaine Matthieu PIGASSE | 1. -

Engie : Isabelle Kocher a LE BEC Dans LE Gaz (Liquéfié)

Exemplaire destiné exclusivement à HEBDOMADAIRE PUBLIÉ LE JEUDI DEPUIS 1978 Tous les jours N°1748 sur www.LaLettreA.fr PARIS, LE 20 OCTOBRE 2016 ActionAction publique Stratégies d’entreprises Journalistes & médias Loi VTC : comment Uber assiège Faurecia : les ex-FAE dans les limbes Le budget 2017 de l'AFP prend l'eau NP.8 le Sénat NP.2 de Bruxelles NP.5 céan a depuis été transformé en une société GNL comme carburant maritime, via des ENGIE : de gérance, la propriété de ses navires ayant navires avitailleurs. Le service démarrera Octave été transférée à la maison mère. La vente en 2017, quand le consortium réception- ISABELLE KOCHER du GDF Global porterait aussi un nouveau nera un bateau dédié, acheté avec les coup au pavillon français, déjà délaissé par Japonais et le belge Fluxys. D'autres par- BONNAUD A LE BEC DANS les groupes tricolores ( LLA nº1700) : sur tenariats existent, comme avec Kan- LE gaz (LIQUÉFIé) les quatre navires détenus ou codétenus sai Electric et Mitsui-MOL. par Engie, trois voguaient avec un équipage français, dont le GDF Global. Cette vente Terminaux sur le fil. Entre le réajustement s'inscrit en revanche dans le processus de de sa flotte et la quête de développements cessions d'actifs annoncé, en 2016, par la commerciaux, Engie doit par ailleurs jugu- - Abonné n°AA031838 L'activité transport maritime de gaz natu- direction pour réduire son endettement. ler la crise des terminaux français d'impor- rel liquéfié (GNL) est en plein ajustement Financièrement, le bénéfice de l'opération tation de GNL de sa filiale Elengy. -

Democratic Information in an Age of Corporate Power

14 09/2016 N°14 Democratic Information in an Age of Corporate Power Democratic Information in an Age of Corporate Power The Passerelle Collection The Passerelle Collection, realised in the framework of the Coredem initiative (Communauté des sites de ressources documentaires pour une démocratie mondiale– Community of Sites of Documentary Resources for a Global Democracy), aims at presenting current topics through analyses, propos- als and experiences based both on field work and research. Each issue is an attempt to weave together various contribu- tions on a specific issue by civil society organisations, media, trade unions, social movements, citizens, academics, etc. The publication of new issues of Passerelle is often associated to public conferences, «Coredem’s Wednesdays» which pursue a similar objective: creating space for dialogue, sharing and build- ing common ground between the promoters of social change. All issues are available online at: www.coredem.info Coredem, a Collective Initiative Coredem (Community of Sites of Documentary Resources for a Global Democracy) is a space for exchanging knowl- edge and practices by and for actors of social change. More than 30 activist organisations and networks share informa- tion and analysis online by pooling it thanks to the search engine Scrutari. Coredem is open to any organisation, net- work, social movement or media which consider that the experiences, proposals and analysis they set forth are building blocks for fairer, more sustainable and more responsible societies. Ritimo, the Publisher The organisation Ritimo is in charge of Coredem and of publishing the Passerelle Collection. Ritimo is a network for information and documentation on international solidarity and sustainable development. -

Hub for Entrepreneurs

AUGUST 2018 A Growing (Opportunistic) Hub for Entrepreneurs: A Report on the Innovation Ecosystem in Paris, France Annie Woodbridge Hudson | iDiplomat 2018 Executive Summary As the economic capital of one of Europe’s biggest economies, Paris is a natural location for a strong and vibrant innovation ecosystem. Yet it has historically fallen short of that designation. Rather, much more of the attention with regards to innovation has fallen on other cities such as London and even, increasingly, Berlin. Deeper analysis would indicate that Paris has vast potential to rise in the world of innovation powerhouses, but suffers as a result of an imbalance in its innovation ecosystem. Applying a research structure developed by MIT’s REAP Program, it becomes clear that the city boasts strong and lasting Innovation Capacity (I-Capacity) but has been quite limited historically in its Entrepreneurial Capacity (E-Capacity). And, according to MIT’s research, while each capacity can exist independently, neither I- Capacity of E-Capacity is enough to create a truly dynamic innovation ecosystem. One established, the two reinforce each other and establish a lasting system that is beneficial for all involved. More directly, Paris’ dynamic university system and strong commitment to R&D both on public and private levels create a vibrant landscape for innovation and research to thrive, yet the city remains mired in a complex bureaucratic system (the result of decades of centralization) that limits the agility of entrepreneurs. Nonetheless, the innovation landscape looks to be gradually changing. There are an increasing number of entrepreneurs eager to mentor a younger generation and to offer the resources necessary to establish burgeoning companies; and the government, too, has expressed a bullish willingness to make the bureaucratic changes necessary to make the entrepreneurial landscape of Paris more appealing. -

Media Oligarchs Go Shopping Patrick Drahi Groupe Altice

MEDIA OLIGARCHS GO SHOPPING Patrick Drahi Groupe Altice Jeff Bezos Vincent Bolloré Amazon Groupe Bolloré Delian Peevski Bulgartabak FREEDOM OF THE PRESS WORLDWIDE IN 2016 AND MAJOR OLIGARCHS 2 Ferit Sahenk Dogus group Yildirim Demirören Jack Ma Milliyet Alibaba group Naguib Sawiris Konstantin Malofeïev Li Yanhong Orascom Marshall capital Baidu Anil et Mukesh Ambani Rupert Murdoch Reliance industries ltd Newscorp 3 Summary 7. Money’s invisible prisons 10. The hidden side of the oligarchs New media empires are emerging in Turkey, China, Russia and India, often with the blessing of the political authorities. Their owners exercise strict control over news and opinion, putting them in the service of their governments. 16. Oligarchs who came in from the cold During Russian capitalism’s crazy initial years, a select few were able to take advantage of privatization, including the privatization of news media. But only media empires that are completely loyal to the Kremlin have been able to survive since Vladimir Putin took over. 22. Can a politician be a regular media owner? In public life, how can you be both an actor and an objective observer at the same time? Obviously you cannot, not without conflicts of interest. Nonetheless, politicians who are also media owners are to be found eve- rywhere, even in leading western democracies such as Canada, Brazil and in Europe. And they seem to think that these conflicts of interests are not a problem. 28. The royal whim In the Arab world and India, royal families and industrial dynasties have created or acquired enormous media empires with the sole aim of magnifying their glory and prestige. -

15/02/2021 Argomento: Utilities Pagina 18

15/02/2021 Pagina 18 EAV: € 60.429 Lettori: 724.276 Argomento: Utilities https://pdf.extrapola.com/utilitaliaV/1819671.pdf Riproduzione autorizzata Licenza Promopress ad uso esclusivo del destinatario Vietato qualsiasi altro uso Gli affari d' oro del banchiere rock che alza le barricate su Suez anais ginori "banchiere rock", è editore della rivista Matthieu Pigasse , parigi Dopo 17 anni Inrockuptiblesin oltre che, insieme a Xavier Niel, Lazard ha creato l' hub europeodel dell' gruppo Le Monde. Con il suo stile americana Centerview e in otto mesi trasgressivo,ha Pigasse è un personaggio a seguito undici operazioni di M&A tra cui partela nel mondo ingessato delle banche d' vendita di Tiffany a Lvmh. Oggi con Ardianaffari. «Qui c' è un po' troppa polizia », contrasta Veolia "S iamo arrivati sul mercato scherza mostrando la strada su cui affaccia la ad aprile, in pieno lockdown, ma alla fine èsede di Centerview, davanti all' Eliseo dove stato un vantaggio: eravamo più carichi edrisiede un altro famoso ex banchiere d' affari. entusiasti dei nostri concorrenti ». MatthieuNel 2016 Pigasse non aveva risparmiato le Pigasse si è lanciato in una nuova avventura a critiche sulla scalata al potere di Emmanuel primavera, con il nuovo hub europeo dellaMacron. Qualcuno sospetta che anche lui banca d' affari americana Centerviewcoltivasse il sogno di lanciarsi in politica. Oggi specializzata in M&A. Dopo diciassette anniè molto più cauto nei giudizi su Macron, loda passati in Lazard, sempre alla ribalta lanel risposta del governo alla crisi economica, consigliare dirigenti d' impresa e governi,ovvero il bazooka di sussidi e prestiti alle Pigasse è oggi in una struttura più piccola che imprese. -

Matthieu Pigasse, Plus Dure Serait La Chute

Downloaded from: justpaste.it/3dnpj ÉDITION ABONNÉS Matthieu Pigasse, plus dure serait la chute Même si Lazard conforte son rang, le banquier vedette est fragilisé par ses investissements personnels. Au point de quitter le navire ?Par Marie Bordet Enfin, Matthieu Pigasse entre dans la pièce. Il apparaît, à l'heure dite - matinale, 8 h 30 -, dans le salon de réception à la lumière tamisée. Sur le mur, un tableau du XIXe siècle représente un banquier fondateur de Lazard au regard sévère. Le maître des lieux nous mène vers une table où est dressé un copieux petit déjeuner et prend place en face de nous. Quelques minutes plus tôt, un huissier en complet noir nous avait guidée dans les couloirs du siège de la prestigieuse banque d'affaires sise au 121, boulevard Haussmann, à Paris. Matthieu Pigasse apparaît tel qu'en sa légende. Visage taillé à la serpe, cintré dans un costume Dior sans cravate et teint pâle, à la limite du translucide. On se souvient alors d'une description clinique que nous avait glissée une de ses vieilles connaissances : « Matthieu, c'est le type à qui on a toujours envie d'offrir un pain au chocolat. Il fait pitié, vraiment. Trop maigre. » Le voir ainsi, en chair et en os, face à des croissants et de la brioche qu'il n'effleurera jamais, relève du miracle. Cela faisait dix jours, déjà, que l'on était partie à sa recherche. « Un rendez-vous ? Oui, oui, je vais en parler à Matthieu », nous répétait sa directrice de la communication. Mais voilà, Matthieu est très occupé. -

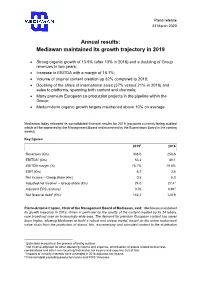

Annual Results: Mediawan Maintained Its Growth Trajectory in 2019

Press release 23 March 2020 Annual results: Mediawan maintained its growth trajectory in 2019 • Strong organic growth of 13.9% (after 13% in 2018) and a doubling of Group revenues in two years; • Increase in EBITDA with a margin of 15.7%; • Volume of original content creation up 32% compared to 2018; • Doubling of the share of international sales (37% versus 21% in 2018) and sales to platforms, spanning both content and channels; • Many premium European co-production projects in the pipeline within the Group; • Medium-term organic growth targets maintained above 10% on average. Mediawan today released its consolidated financial results for 2019 (accounts currently being audited which will be approved by the Management Board and examined by the Supervisory Board in the coming weeks). Key figures 20191 2018 Revenues (€m) 338.0 258.6 EBITDA1 (€m) 53.2 49.1 EBITDA margin (%) 15.7% 19.0% EBIT (€m) 6,7 3,6 Net income – Group share (€m) 0,5 5,0 Adjusted net income2 – Group share (€m) 24.0 27.43 Adjusted EPS (€/share) 0.76 0.943 Net financial debt4 (€m) 142.2 120.9 Pierre-Antoine Capton, Chair of the Management Board of Mediawan, said: “Mediawan maintained its growth trajectory in 2019, driven in particular by the quality of the content created by its 24 labels, now broadcast over an increasingly wide area. The demand for premium European content has never been higher, allowing Mediawan to build a robust and unique model, based on the entire audiovisual value chain from the production of drama, film, documentary and animated content to the distribution 1 Estimated accounts in the process of being audited 2 Net income adjusted for other operating income and expense, amortisation of assets related to business combinations and other non-recurring financial or tax income and expense (net of tax).