DEVELOPMENTS in AUDIT 2019 November 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FTSE Factsheet

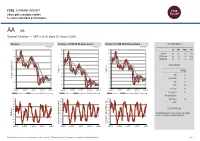

FTSE COMPANY REPORT Share price analysis relative to sector and index performance AA AA. General Retailers — GBP 0.25 at close 03 August 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 03-Aug-2020 03-Aug-2020 03-Aug-2020 0.7 140 140 1D WTD MTD YTD 130 130 Absolute 4.6 4.6 4.6 -57.0 0.6 Rel.Sector 2.4 2.4 2.4 -48.8 120 120 Rel.Market 2.5 2.5 2.5 -46.1 110 110 0.5 100 100 VALUATION 90 0.4 90 80 Trailing Relative Price Relative Relative Price Relative 80 70 0.3 PE 1.6 70 Absolute Price (local currency) (local Price Absolute 60 EV/EBITDA 8.0 60 50 0.2 PB -ve 50 40 PCF 0.7 0.1 40 30 Div Yield 2.6 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Price/Sales 0.1 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity - 100 90 90 Div Payout 4.6 90 80 80 ROE - 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 The principal activity of the Company is providing 40 RSI RSI (Absolute) service of consumer roadside assistance. -

BMW & Mini, 501 Dunstable Road, Luton, LU4

HIGH QUALITY PRIME CAR SHOWROOM INVESTMENT SHOWROOM CAR PRIME HIGH QUALITY BMW & Mini 501 DUNSTABLE ROAD � LUTON � LU4 8QN A14 Northampton A428 CAMBRIDGE Investment Summary. Location.A5 A11 Bedford M1 A1 A421 Excellently positioned fronting A43 Situated on the Madford onto the A505, the main arterial Retail Park, 2 miles north west Milton Keynes route which leads directly from of Luton Town Centre, 20 miles the M1 (J11), 1 mile to the west, to south east of Milton Keynes A6 the centre of Luton M11 A5 A10 Two adjoining modern glazed showrooms, refurbished in 2016 Floor Area: 37,400 sq ft Stevenage Luton 80 display bays (293 in total) Site Area: 2.3 acres A41 A418 11 Workshops and large parking (29% site coverage) provisions Aylesbury A1(M) M1 Single let to Ivor Holmes Limited A41 Harlow Guaranteed by Specialist Cars 21 21a Holdings Limited (D&B Rating AWULT: 17.8 yrs (to expiry) 4A1) M40 AGA from Pendragon PLC until Watford M25 Dec 2031 M25 Marketing Rent: RPI-linked annual rent reviews £ £310,277 pa (£7.85 psf) capped at 2.77% pa Refurbished in 2016 by the Tenure: Freehold tenant at a cost of £2 million Proposal We are instructed to seek offers for the freehold interest in excess of £5,550,000 subject to contract and exclusive of VAT. A purchase at this level would refl ect an attractiveNet Initial Yield of 5.25% and a low capital value of £148 per sq ft, after deducting purchasers costs of 6.61%. Site Plan. Site *boundary for indicative purposes only 2 BMW & MINI � 501 DUNSTABLE ROAD, LUTON, LU4 8QN 17 16 TO LONDON M1 LUTON STATION 15 J11 14 TO LONDON Sovereign Park 12 13 Bilton Way 9 Industrial Estate 10 11 Local 7 8 Occupiers. -

NOTICE: This Is an Unofficial Transcript of the Public Company Accounting

NOTICE: This is an unofficial transcript of the Public Company Accounting Oversight Board’s June 28, 2012 Public Meeting on Auditor Independence and Audit Firm Rotation. The Public Company Accounting Oversight Board does not certify the accuracy of this unofficial transcript, which may contain typographical or other errors or omissions. An archive of the webcast of the meeting can be found on the Public Company Accounting Oversight Board’s website at: http://pcaobus.org/News/Webcasts/Pages/06282012_PublicMeeting.aspx 1 PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD + + + + + AUDITOR INDEPENDENCE AND AUDIT FIRM ROTATION PCAOB RULEMAKING DOCKET MATTER NO. 37 + + + + + PUBLIC MEETING + + + + + THURSDAY JUNE 28, 2012 + + + + + The Public Meeting convened at the Hilton San Francisco Financial District, 750 Kearny Street, San Francisco, California, at 8:00 a.m., Jim Doty, PCAOB Chairman, presiding. THE BOARD JAMES R. DOTY, Chairman LEWIS H. FERGUSON, Board Member JEANETTE M. FRANZEL, Board Member JAY D. HANSON, Board Member STEVEN B. HARRIS, Board Member PCAOB STAFF MARTIN F. BAUMANN, PCAOB, Chief Auditor and Director of Professional Standards MICHAEL GURBUTT, Associate Chief Auditor J. GORDON SEYMOUR, General Counsel JACOB LESSER, Associate General Counsel OBSERVERS BRIAN CROTEAU, Securities and Exchange Commission NEAL R. GROSS COURT REPORTERS AND TRANSCRIBERS 1323 RHODE ISLAND AVE., N.W. (202) 234-4433 WASHINGTON, D.C. 20005-3701 www.nealrgross.com 2 PANELISTS JULIE ALLECTA, Trustee and Chairman of the Audit Committee, Forward Funds JANICE HESTER AMEY, Portfolio Manager, Corporate Governance, California State Teachers' Retirement System (CalSTRS) ANDREW D. BAILEY, JR., Professor Emeritus, University of Illinois at Urbana-Champaign; former Deputy Chief Accountant, US Securities and Exchange Commission WILLIAM H. -

EMBARGOED UNTIL 00:01 FRIDAY 13Th SEPTEMBER the BIG FOUR

EMBARGOED UNTIL 00:01 FRIDAY 13th SEPTEMBER THE BIG FOUR PROFESSIONAL SERVICES ORGANISATIONS LATEST TO JOIN FORCES ON BUSINESS DISABILITY INCLUSION • The Big Four professional service organisations, Deloitte UK, EY, KPMG UK and PwC UK have signed up to disability inclusion campaign The Valuable 500 • The campaign is seeking 500 global business leaders and brands to commit to putting disability on their board agendas in 2019 • This marks the first ever collaboration on disability inclusion in business between all four leading accountancy organisations LONDON, 13th SEPTEMBER: Deloitte UK, KPMG UK and PwC UK have today announced that they have signed up to The Valuable 500 – the global initiative striving to place disability inclusion on the business agenda. EY has already pledged to The Valuable 500 at a global level. This collaborative move from the leading professional services organisations places the sector at the forefront of creating better inclusivity in business. This move follows the large number of banks that recently committed to The Valuable 500 including Barclays, HSBC, Bank of England, RBS and Lloyds Banking Group, signifying a huge step forward for the financial sector as a whole. The Valuable 500, launched at the World Economic Forum’s Annual Summit in Davos earlier this year, is seeking 500 global business leaders to place disability on their board agendas, and will hold each accountable for disability inclusion in their businesses by ensuring it is discussed at leadership level and action is taken. To date businesses employing well over two million employees globally have signed up to put disability inclusion on their board agendas. -

Auto 04 Temp.Qxd

FORD AUTOTEAM THE MAGAZINE FOR ALL FORD DEALER STAFF ISSUE 3/2016 EDITORIAL Changing Times It’s all change for the management team at the Henry Ford Academy. Stuart Harris has moved on to a new position within Ford of Europe and, as I move into his role, I hope to continue with his goal of driving up training standards. Also joining the team is new Academy Principle, Kevin Perks, who brings with him a lifetime of automotive industry experience. Dan Savoury, the new Vice Principal, joined the Academy earlier this year and also has a wealth of industry and training experience that will help us continue to improve our training which, in turn, benefits your business. I hope to use the experience gained in my previous sales and marketing roles within Ford to help our training continue to grow in scope and quality. It is a really exciting time to be a part of the Ford family; with new vehicles joining the range and new technology transforming the industry more widely. Good training is vital to our success and we continue to strive to achieve the highest standards and keep you up to date with this rapidly changing industry, from the technical training for the All-new Ford Mustang detailed on page 4, to ensuring our Commercial Vehicle Sales staff can give their customers the best advice with courses such as Commercial Vehicle Type Approval and Legislation on page 30. The success of our training programmes is demonstrated in this issue, with Chelsea Riddle from TrustFord in Bradford a great example of what the Ford Masters Apprenticeship scheme offers to young people, or the success that Mike Gates from Dinnages Ford in Burgess Hill has achieved with a university scholarship through the Henry Ford Academy. -

New Avenues of Research to Explain the Rarity of Females at the Top of the Accountancy Profession

ARTICLE Received 29 Jul 2016 | Accepted 9 Feb 2017 | Published 7 Mar 2017 DOI: 10.1057/palcomms.2017.11 OPEN New avenues of research to explain the rarity of females at the top of the accountancy profession Anne Jeny1 and Estefania Santacreu-Vasut1 ABSTRACT The rarity of females in leadership positions has been an important subject of study in economics research. The existing research on gender inequality has established that important variations exist across time and place and that these differences are partly attri- butable to the cultural differences regarding gender roles. The accounting research has also established that women are rarely promoted to the top of the Big Four audit firms (KPMG, Deloitte, PricewaterhouseCoopers and Ernst & Young). However, the majority of research in accountancy has focused on Anglo-Saxon contexts (the United States, the United Kingdom and Australia) or country case studies without explicitly considering the role that cultural variations may play. Because the Big Four are present in more than 140 countries, we argue that the accountancy research that attempts to explain gender disparities at the top of these organizations would benefit from considering cultural factors. Such research, however, faces a key methodological challenge—specifically, the measurement of the cultural dimensions that relate to gender. To address this challenge, we propose an emerging approach that uses the gender distinctions in language to measure cultural attitudes toward gender roles. The idea that language may capture gender roles and even influence their formation and per- sistence has been the focus of emerging research in linguistics and economics. To support our proposition, we follow two steps. -

JH Inv Funds Series I OEIC AR 05 2021.Indd

ANNUAL REPORT & ACCOUNTS For the year ended 31 May 2021 Janus Henderson Investment Funds Series I Janus Henderson Investment Funds Series I A Who are Janus Henderson Investors? Global Strength 14% 13% £309.6B 55% 45% 31% 42% Assets under Over 340 More than 2,000 25 Over 4,300 management Investment professionals employees Offi ces worldwide companies met by investment teams in 2020 North America EMEA & LatAm Asia Pacifi c Source: Janus Henderson Investors, Staff and assets under management (AUM) data as at 30 June 2021. AUM data excludes Exchange-Traded Note (ETN) assets. Who we are Janus Henderson Investors (‘Janus Henderson’) is a global asset manager off ering a full suite of actively managed investment products across asset classes. As a company, we believe the notion of ‘connecting’ is powerful – it has shaped our evolution and our world today. At Janus Henderson, we seek to benefi t clients through the connections we make. Connections enable strong relationships based on trust and insight aswell as the fl ow of ideas among our investment teams and our engagement with companies. These connections are central to our values, to what active management stands for and to the long-term outperformance we seek to deliver. Our commitment to active management off ers clients the opportunity to outperform passive strategies over the course of market cycles. Through times of both market calm and growing uncertainty, our managers apply their experience weighing risk versus reward potential – seeking to ensure clients are on the right side of change. Why Janus Henderson Investors At Janus Henderson, we believe in linking our world-class investment teams and experienced global distribution professionals with our clients around the world. -

2013 ANNUAL REPORT the UK’S Leading Car Retailer CONTENTS

2013 ANNUAL REPORT The UK’s leading car retailer CONTENTS AT A GLANCE 2 OUR OPERATIONAL AND FINANCIAL HIGHLIGHTS 7 OUR CHAIRMAN 11 OUR MARKETS AND BUSINESSES 12 Our Markets 12 Our Businesses 20 OUR BUSINESS MODEL AND STRATEGY 26 Business Model 26 STRATEGIC REVIEW Strategy 28 Key Performance Indicators 30 Risk Overview and Management 34 Our People 38 OPERATIONAL AND FINANCIAL REVIEW 40 Operational Review 40 Financial Review 44 DIRECTORS' REPORTS 50 Board of Directors 51 Chairman's Corporate Governance Letter to Shareholders 52 Corporate Governance Report 53 Corporate Social Responsibility Report 59 Committee Reports 62 Directors' Remuneration Report 68 GOVERNANCE Directors' Report 90 Directors' Responsibility Statement 96 INDEPENDENT AUDITORS REPORT 98 FINANCIAL STATEMENTS 102 Consolidated Income Statement 102 Consolidated Statement of Comprehensive Income 103 Consolidated Statement of Changes in Equity 104 Consolidated Balance Sheet 105 Consolidated Cash Flow Statement 106 Reconciliation of Net Cash Flow to Movement in Net Debt 107 FINANCIALS Notes to the Financial Statements 108 Company Balance Sheet 171 Reconciliation of Movements in Shareholders’ Funds of the Company 172 Notes to the Financial Statements of the Company 173 Shareholder Information 180 5 Year Group Review 181 AT A GLANCE THE UK’S LEADING AUTOMOTIVE RETAILER Pendragon’s principal markets are the retailing of new and used vehicles and the service and repair of vehicles (aftersales). Pendragon also operates in the dealership management system, leasing and wholesales parts markets. Brands Stratstone California 02 Mercedes-Benz GL 63 AMG available from Stratstone.com 02 AT A GLANCE What we do The UK's leading automotive retailer in the UK with 225 franchise points selling new and used vehicles and conducting service and repair activity (aftersales). -

Full Property Address Primary Liable

Full Property Address Primary Liable party name 2019 Opening Balance Current Relief Current RV Write on/off net effect 119, Westborough, Scarborough, North Yorkshire, YO11 1LP The Edinburgh Woollen Mill Ltd 35249.5 71500 4 Dnc Scaffolding, 62, Gladstone Lane, Scarborough, North Yorkshire, YO12 7BS Dnc Scaffolding Ltd 2352 4900 Ebony House, Queen Margarets Road, Scarborough, North Yorkshire, YO11 2YH Mj Builders Scarborough Ltd 6240 Small Business Relief England 13000 Walker & Hutton Store, Main Street, Irton, Scarborough, North Yorkshire, YO12 4RH Walker & Hutton Scarborough Ltd 780 Small Business Relief England 1625 Halfords Ltd, Seamer Road, Scarborough, North Yorkshire, YO12 4DH Halfords Ltd 49300 100000 1st 2nd & 3rd Floors, 39 - 40, Queen Street, Scarborough, North Yorkshire, YO11 1HQ Yorkshire Coast Workshops Ltd 10560 DISCRETIONARY RELIEF NON PROFIT MAKING 22000 Grosmont Co-Op, Front Street, Grosmont, Whitby, North Yorkshire, YO22 5QE Grosmont Coop Society Ltd 2119.9 DISCRETIONARY RURAL RATE RELIEF 4300 Dw Engineering, Cholmley Way, Whitby, North Yorkshire, YO22 4NJ At Cowen & Son Ltd 9600 20000 17, Pier Road, Whitby, North Yorkshire, YO21 3PU John Bull Confectioners Ltd 9360 19500 62 - 63, Westborough, Scarborough, North Yorkshire, YO11 1TS Winn & Co (Yorkshire) Ltd 12000 25000 Des Winks Cars Ltd, Hopper Hill Road, Scarborough, North Yorkshire, YO11 3YF Des Winks [Cars] Ltd 85289 173000 1, Aberdeen Walk, Scarborough, North Yorkshire, YO11 1BA Thomas Of York Ltd 23400 48750 Waste Transfer Station, Seamer, Scarborough, North Yorkshire, -

The Economics of Retail Banking

THE ECONOMICS OF RETAIL BANKING - An empirical analysis of the UK market for personal current accounts Céline Gondat-Larralde and Erlend Nier* 10 December 2003 (Preliminary. Please do not circulate or cite without permission) Abstract: This paper provides an analysis of the competitive process in the market for personal current accounts in the UK. Using NOP survey data, we first describe some stylised developments in this market over the past few years. We find a gradual change in the distribution of market shares over time. This contrasts with a marked dispersion in price, which appears to persist through time. Analysing the evolution of market shares, we address two key questions (i) Are bank market shares responding to price differentials? (ii) If not, which type of imperfect competition best fits the data? Our conclusions point to the existence of customer switching costs as a key determinant of the nature of competition in the market for personal current accounts. JEL Classification: D12, D43, D83, G21 and L13 Keywords: microeconomics; retail banking; competition; switching; price elasticity The views expressed in this paper are those of the authors and do not necessarily reflect those of the Bank of England. We would like to thank Charles Goodhart, Patricia Jackson, Kevin James, Glenn Hoggarth, Darren Pain, William Perraudin and Geoffrey Wood for useful discussions on an earlier draft of the paper and Jon Chu and Nyeong Lee for research assistance. _________________________________________ * Both authors are at the Bank of England. Céline Gondat-Larralde can be contacted at celine.gondat- [email protected], Tel:++44 20 7601 3328. -

UK Annual Report 2015 (Including the Transparency Report)

Investing to become the Clear Choice UK Annual Report 2015 (including the Transparency Report) December 2015 KPMG.com/uk Highlights Strategic report Profit before tax and Revenue members’ profit shares £1,958m £383m (2014: £1,909m) (2014: £414m) +2.6% -7% 2013 2014 2015 2013 2014 2015 Average partner Total tax payable remuneration to HMRC £623k £786m (2014: £715K) (2014: £711m) -13% +11% 2013 2014 2015 2013 2014 2015 Contribution Our people UK employees KPMG LLP Annual Report 2015 Annual Report KPMG LLP 11,652 Audit Advisory Partners Tax 617 Community support Organisations supported Audit Tax Advisory Contribution Contribution Contribution £197m £151m £308m (2014: £181m) (2014: £129m) (2014: £324m) 1,049 +9% +17% –5% (2014: 878) © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Strategic report Contents Strategic report 4 Chairman’s statement 10 Strategy 12 Our business model 16 Financial overview 18 Audit 22 Solutions 28 International Markets and Government 32 National Markets 36 People and resources 40 Corporate Responsibility 46 Our taxes paid and collected 47 Independent limited assurance report Governance 52 Our structure and governance 54 LLP governance 58 Activities of the Audit & Risk Committee in the year 59 Activities of the Nomination & Remuneration Committee in the year KPMG in the UK is one of 60 Activities of the Ethics Committee in the year 61 Quality and risk management the largest member firms 2015 Annual Report KPMG LLP 61 Risk, potential impact and mitigations of KPMG’s global network 63 Audit quality indicators 66 Statement by the Board of KPMG LLP providing Audit, Tax and on effectiveness of internal controls and independence Advisory services. -

Banks in Sweden Facts About the Swedish Banking Market Published in Nov 2008 Banks in Sweden

Banks in Sweden Facts about the Swedish banking market Published in Nov 2008 Banks in Sweden The Swedish financial market The economic role of the financial sector tween banking and insurance. It has led to that Efficient and reliable systems for saving, fi- all Sweden’s major banks are involved in the nancing, mediating payments, and risk man- life insurance business and some insurance agement are of fundamental importance for companies have their own banks. Sweden’s economic prosperity. These systems Another change is that branch offices have be- are operated by banks and other credit institu- come less important for bank customers’ daily tions, insurance companies, securities compa- services. Instead the customers tend to make nies and other companies in the financial sec- normal bank services through their internet tor. The financial sector channels in an effi- bank. Furthermore, opportunities to perform cient way society savings to investment and bank services in different ways have increased, consumption, such as household needs to e.g. cash- and debit card payments, cash with- smooth out consumption of various life stages drawals in supermarkets and credit applica- and the need for companies to finance invest- tions in chain stores. These new channels of ment. distribution have enabled the development of The financial industry account for almost four new services while existing services has per cent of the country’s total output, ex- changed. The new technology has also paved pressed as its Gross Domestic Product (GDP). the way for the establishment of new banks Around 100,000 people, representing about and increased competition in banking.