Japanese GAAP” Are to Generally Accepted Accounting Principles in Japan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prologis 2005 Summary Annual Report

® sustainability 2005 Summary Annual Report The long-term growth plan ProLogis set in motion a year ago is well underway. Our 2005 results were excellent, and we’re confident in our ability to continue to execute our plan for sustained, profitable growth well into the future. But sustaining our performance and building a company that excels long term transcends traditional financial growth. Our commitment includes creating an environment in which our people can recognize their full potential and build mutually beneficial relationships with our customers. And as a leader in our industry, we are committed to implementing innovative solutions for sustainable development while making a difference in our communities and our world. These are the keys to true sustainability. Mission Operating in: To be the leading global provider of distribution North America United States, Mexico, facilities and services to the world’s largest users Canada of distribution space, thereby creating value for our customers and shareholders. Europe Belgium, Czech Republic, France, Germany, Hungary, Profile Italy, The Netherlands, ProLogis is one of the world’s largest providers of Poland, Spain, Sweden, industrial distribution facilities, with operations in United Kingdom 77 markets across North America, Europe and Asia. Asia We have over 375 million square feet of industrial Japan, China, South Korea space in 2,340 buildings, representing over $22 billion of assets owned, managed and under development. These strategically located, state-of-the-art facilities help -

Investor Fact Sheet PLD $86.7B 3.3%

Fourth Quarter 2018 Investor Fact Sheet Prologis Park Narashino, Japan World’s Leading Logistics Real Estate Company PLD $86.7 B NYSE Assets Under Management Prologis is the leading global provider of logistics real estate, offering customers approximately 768 million square feet of distribution space (71 million square meters) in markets across the Americas, Europe and Asia. The company leases more than 3,500 industrial facilities in 19 3.3% 1 countries to more than 5,100 customers, including third-party logistics TTM Dividend Yield providers, transportation companies, retailers, and manufacturers. World-Class Platform MARKET ALLOCATION2 Other Americas • The undisputed leader in the industrial sector 6.0% • The best customer brand in the real estate industry • The only truly global real estate company active on four continents Europe 22.7% • World’s leading logistics real estate strategic capital franchise U.S. 59.8% 1 Asia Prologis At-a-Glance 11.5% • 97.5% occupancy in its owned and managed operating portfolio • Leased 34.9 million square feet (3.2 million square meters) in the operating and development portfolios during 4Q 2018 • Commenced $930 million of development across three continents in Q4 and generated $185 million of value creation (Prologis share) on stabilizations 1. As of December 31, 2018 (PLD closed at $58.72) 2. Market allocation based on owned and managed operating portfolio gross book • The company recast and upsized its global line of credit in January value as of December 31, 2018. On a Prologis share basis, ownership was 76.5% 2019, bringing its total liquidity to ~$4.0 billion US, 6.5% Other Americas, 13.2% Europe, 3.8% Asia. -

View Annual Report

PROLOGIS 2011 ANNUAL REPORT AN EXTRAORDINARY YEAR OF TRANSFORMATION $43.3B IN ASSETS UNDER MANAGEMENT ACROSS THE AMERICAS, EUROPE AND ASIA HOME SHAREHOLDERS LETTER LEADERSHIP YEAR IN REVIEW FINANCIAL HIGHLIGHTS FORM 10-K PROLOGIS 2011 ANNUAL REPORT SERVING LEADERS IN LOGISTICS PROVIDING MORE THAN 4,500 CUSTOMERS WITH LOGISTICS INFRASTRUCTURE HOME SHAREHOLDERS LETTER LEADERSHIP YEAR IN REVIEW FINANCIAL HIGHLIGHTS FORM 10-K PROLOGIS 2011 ANNUAL REPORT UNPARALLELED SCALE 600M SF (55.7 MSM) OF MODERN DISTRIBUTION FACILITIES IN 22 COUNTRIES HOME SHAREHOLDERS LETTER LEADERSHIP YEAR IN REVIEW FINANCIAL HIGHLIGHTS FORM 10-K PROLOGIS 2011 ANNUAL REPORT THE RIGHT PEOPLE IN THE RIGHT PLACES 1,300 REAL ESTATE PROFESSIONALS– THE MOST TALENTED REAL ESTATE ORGANIZATION IN THE INDUSTRY HOME SHAREHOLDERS LETTER LEADERSHIP YEAR IN REVIEW FINANCIAL HIGHLIGHTS FORM 10-K PROLOGIS 2011 ANNUAL REPORT ALIGNING OUR PORTFOLIO WITH OUR INVESTMENT STRATEGY $1.65B IN CONTRIBUTIONS AND DISPOSITIONS IN THE SECOND HALF OF 2011 HOME SHAREHOLDERS LETTER LEADERSHIP YEAR IN REVIEW FINANCIAL HIGHLIGHTS FORM 10-K PROLOGIS 2011 ANNUAL REPORT EXCEEDING EXPECTATIONS AND DELIVERING RESULTS OCCUPANCY IN OUR GLOBAL PORTFOLIO INCREASED 120 BASIS POINTS TO 92.2% FROM THE THIRD QUARTER HOME SHAREHOLDERS LETTER LEADERSHIP YEAR IN REVIEW FINANCIAL HIGHLIGHTS FORM 10-K PROLOGIS 2011 ANNUAL REPORT LETTER TO OUR SHAREHOLDERS Dear Shareholders, The past year was one of transformation for our company. In June 2011, we closed the merger between the former ProLogis and AMB, bringing together the people and assets of the two leading companies in the industrial property sector and forming what is arguably one of the world’s pre-eminent real estate firms. -

Prologis Media Fact Sheet

PROLOGIS MEDIA FACT SHEET EUROPE U.S. 183 MSF 377 MSF 17% of NOI 70% NOI ASIA 66 MSF 4% of NOI*A OTHER AMERICAS 58 MSF 9% of NOI About Prologis TM Local Partner to Global Trade Global at a Glance (as of 12/31/2017) Prologis, Inc. is the global leader in logistics real estate with a focus on high-barrier, high-growth markets. As of December 31, 2017, the company • $78.7 billion in total assets under owned or had investments in, on a wholly owned basis or through co- management investment ventures, properties and development projects across 684 million square feet (63.6 million square meters) in 19 countries. Prologis • 684 million square feet (63.6 leases modern logistics facilities to a diverse base of approximately 5,000 million square meters) owned, managed or under development customers. These facilites assist the efficient distribution of goods for the world's best businesses and brands. • 3,282 industrial properties across the Americas, Europe and Asia • Properties in 19 countries around Operations Strategic Capital Development UNIQUE BUSINESS MODEL the world Real Estate Operations Strategic Capital Capital Deployment • 5,000 customers across a diverse range of industries • ~1,600 employees serving customers and investors • A member of the S&P 500 • Named among the “Global 100 Most Sustainable Corporations in the World” nine years running * This is a non-GAAP financial measure. Please see notes and definitions for further explanation. A NOI calculations based on Prologis share of the operating portfolio. Pier 1, Bay 1, San Francisco, CA 94111 United States | +1 415 394 9000 | www.prologis.com | NYSE: PLD PROLOGIS MEDIA FACT SHEET Our Leadership TOP 20 CUSTOMERS (as of 12/31/2017) Hamid R. -

2020 Third Quarter Real Estate Performance Report

13. Presentation by StepStone Group – 2020 Third Quarter Real Estate Performance Report 13 Quarterly Real Estate Monitoring Report For the period ended September 30, 2020 Report prepared for: WATER AND POWER EMPLOYEES' RETIREMENT PLAN IMPORTANT INFORMATION This document is meant only to provide a broad overview for discussion purposes. All information provided here is subject to change. This document is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, or as an offer to provide advisory or other services by StepStone Group LP, StepStone Group Real Assets LP, StepStone Group Real Estate LP, StepStone Conversus LLC, Swiss Capital Alternative Investments AG and Swiss Capital Invest Holding (Dublin) Ltd. or their subsidiaries or affiliates (collectively, “StepStone”) in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this document should not be construed as financial or investment advice on any subject matter. StepStone expressly disclaims all liability in respect to actions taken based on any or all of the information in this document. This document is confidential and solely for the use of StepStone and the existing and potential clients of StepStone to whom it has been delivered, where permitted. By accepting delivery of this presentation, each recipient undertakes not to reproduce or distribute this presentation in whole or in part, nor to disclose any of its contents (except to its professional advisors), without the prior written consent of StepStone. While some information used in the presentation has been obtained from various published and unpublished sources considered to be reliable, StepStone does not guarantee its accuracy or completeness and accepts no liability for any direct or consequential losses arising from its use. -

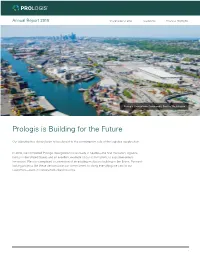

Prologis 2018 Annual Report

Annual Report 2018 Shareholders Letter Leadership Financial Highlights Headline Subhead Body Prologis Georgetown Crossroads, Seattle, Washington Prologis is Building for the Future Our objective has always been to be closest to the consumption side of the logistics supply chain. In 2018, we completed Prologis Georgetown Crossroads in Seattle—the first multistory logistics facility in the United States and an excellent example of our commitment to customer-centric innovation. We also completed a conversion of an existing multistory building in the Bronx. Forward- looking projects like these demonstrate our commitment to doing everything we can for our customers—even in constrained urban locations. 1 Annual Report 2018 Shareholders Letter Leadership Financial Highlights Prologis Labs team, Alan Findley, Tim Manochehri II, Gary Bruns and Greg Everson, San Leandro, California (not pictured, Robert Heekelaar) Customer-Centric Innovation and Technology Our scale enables us to invest in technology as we continue to seek solutions to help our customers run their businesses as efficiently as possible. Prologis Labs is a dedicated space for testing new products and services designed to ease our customers’ pain points. This recent investment in customer-centric innovation allows us to cycle quickly through ideas, invest in the winners and then scale those solutions across our global portfolio. Prologis Labs is currently focusing on: — Digital supply chain/digital warehouse — Attributes of the next-generation distribution center — Transportation — Urban fulfillment 2 Annual Report 2018 Shareholders Letter Leadership Financial Highlights Solar installation at Prologis International Park of Commerce, Tracy, California Sustainability is in Our DNA Environmental stewardship, social responsibility and governance have been key tenets of Prologis’ business practices for decades. -

Unilever Investing Plan Cautious Growth Fund

KTUC_2021_06.pdf FIDELITY LIFE FUNDS 30 JUNE 2021 UNILEVER INVESTING PLAN CAUTIOUS GROWTH FUND Fund objective Fund facts An appropriately diversified investment vehicle with an investment objective which aims to achieve Benchmark a return over the long term (5-years or more) that exceeds the return on the cash fund (albeit with a 27% MSCI World Index (Net) ; 12.5% 1 Month LIBOR + 3% ; 12.5% Bloomberg higher prospect that a negative absolute return could be experienced over the same period than Barclays Multiverse Corporate Index (Total Return Gross) Hedged to GBP the cash fund). This fund invests or reinsures into underlying funds managed by Fidelity or our Fund (JPFC) ; 12.5% FTSE Actuaries UK Conventional Gilts Over 15 Years Midday (Blackrock) ; 12.5% FTSE Actuaries UK Index Linked Gilts Over 5 Years Index Partners. Midday (Blackrock) ; 12.5% GBP 1W LIBID ; 7.5% BlackRock Global Property Securities Index ; 3% MSCI Global Emerging Markets Index (Blackrock) Fund size £15m Launch date Performance as at 30.06.2021 31.12.07 Past performance is not a reliable indicator of future results. Base currency GBP Yearly performance Annual management charge 1 July 2016 1 July 2017 1 July 2018 1 July 2019 1 July 2020 0.275%** to to to to to 30 June 2017 30 June 2018 30 June 2019 30 June 2020 30 June 2021 Other charges 0.084% Fund 10.3% 3.7% 6.0% 4.4% 9.9% Benchmark 9.1% 4.1% 6.6% 5.8% 7.4% Total Expense Ratio 0.359% **The charge shown represents a weighted average of AMCs of the underlying funds and Annualised performance any additional charge for the management of this plan specific fund. -

Facilities Permit Program 10/2/2020 Client and Building List Page 1 of 99

Facilities Permit Program 10/2/2020 Client and Building List Page 1 of 99 111 SW 5th Ave Investors LLC 19-134770-000-00-FC YORDANOS LONG UNICO PROPERTIES Building/Mechanical Inspector: Jeffrey Rago 4364025 Work: (503) 275-7461 Electrical Inspector: David Scranton [email protected] Plumbing Inspector: Chuck Luttmann M Fire Marshal: Mark Cole Building Address Folder Master US Bancorp Plaza:Unico Prop 555 SW OAK ST 19-134803-FC 19-134804-FA US Bancorp Prkng Struct:Unico Prop 129 SW 4TH AVE 20-101725-FC 20-101726-FA US Bancorp Tower:Unico Prop 111 SW 5TH AVE 19-134793-FC 19-134794-FA 200 Market Assoc. 99-125363-000-00-FC LAURA HUNDTOFT CUSHMAN & WAKEFIELD Building/Mechanical Inspector: Jeffrey Rago 2001906 Work: (503) 228-8666 Electrical Inspector: David Scranton Home: (503) 227-2549 Plumbing Inspector: Chuck Luttmann [email protected] Fire Marshal: Mark Cole Building Address Folder Master 200 MarketBldg:200 Market 200 SW MARKET ST 99-125649-FC 04-055199-FA Dielschneider:200 MARKET 71 SW OAK ST 09-124819-FC 09-124820-FA Fechheimer:200 MARKET 233 SW NAITO PKY 09-124830-FC 09-124831-FA FreimannKitchen:200 MARKET 79 SW OAK ST 09-124810-FC 09-124811-FA FreimannRestaurant:200 MARKET 240 SW 1ST AVE 09-124805-FC 09-124806-FA Hallock & McMillan:200 MARKET 237 SW NAITO PKWY 10-198884-FC 10-198885-FA Generated 10/02/2020 11:46 AM by CREPORTS_SVC from DSPPROD City of Portland, BDS - Report Code: 1109007 Facilities Permit Program 10/2/2020 Client and Building List Page 2 of 99 2020 Portland LLC c/o SKB 19-107059-000-00-FC Christina -

Prologis Park NEI Grant Line Road and Chrisman Road | Tracy, CA

Prologis Park NEI Grant Line Road and Chrisman Road | Tracy, CA ±100,000 up to ±1,500,000 Square Feet Available Breaking Ground Fall 2020 www.prologis.com www.cbre.us Master Site Plan - Buildings A, B and C Tracy, California About Prologis Park NEI • 86 acre Master-Planned Industrial Park • Premier Central Valley location, ideally located in East Tracy providing service to the Bay Area, Northern California, and the Western United States • Three building plan shown, but able to deliver state-of-the-art warehouse and manufacturing facilities ranging from 100,000 SF up to 1,500,000 SF • Flexible site, capable of meeting the needs of today’s users • Corporate neighbors include: Amazon, Clutter, Crate & Barrel, DHL, Home Depot, International Paper, Katerra, Kellogs, Pepsi • Direct Access to I-205, I-5, I-580, Hwy 120 & Hwy 99 • Close proximity to BNSF & Union Pacific Class 1 Intermodals • Great proximity to Oakland, San Francisco, San Jose, and Sacramento international airports www.prologis.com www.cbre.us Building A Tracy, California Property Description • 665,000 SF, divisible • State-of-the-art Warehouse/Manufacturing facility • 36’ minimum clear height • ESFR fire suppression system • Office space to suit • 2% skylights • 56’ x 60’ typical column spacing • 70’ speed bay • 6.5” reinforced concrete floors • 4,000 Amps, 277/480v, 3-phase, expandable Loading • Cross-dock design • Four (4) 12’ x 14’ grade level doors • 185’ Truck court with 60’ concrete truck aprons • One Hundred Thirty-Five (135) 9’x10’ dock high positions Parking • 189 trailer -

An Integrated Approach to Sustainability an INTEGRATED ENVIRONMENTAL SOCIAL ETHICS and GRI APPROACH STEWARDSHIP RESPONSIBILITY GOVERNANCE MATERIALS

2016 Sustainability Report An Integrated Approach to Sustainability AN INTEGRATED ENVIRONMENTAL SOCIAL ETHICS AND GRI APPROACH STEWARDSHIP RESPONSIBILITY GOVERNANCE MATERIALS Table of Contents Prologis Overview 3 A Message from our CEO 4 The Year in Review from our Head of Sustainability 6 An Integrated Approach 7 Three Complementary Lines of Business 8 Drive Enduring Value Creating Sustainable Value for our Stakeholders 9 Materiality and Stakeholder Engagement 10 Stakeholder Priorities and Engagement 11 Awards and Recognition 12 Environmental Stewardship 13 Environmental Goals and Objectives 14 High-Quality, Resilient Design 15 Innovations in Energy 16 Energy Efficiency 17 Water and Waste 18 Operations and Supply Chain 19 Corporate Carbon Footprint Reporting 20 Social Responsibility 21 People at Prologis 22 Employee Volunteerism and Giving 23 Employee Benefits and Well-Being 24 Ethics and Governance 26 Acting with Integrity 27 GRI Materials 29 Memberships and Associations 30 External Assurance Statement 31 GRI Standards Content Index 32 Data Snapshot 36 Engage With Us 39 All data in this report is as of 12/31/2016. Cover photo: Prologis team members, Denver, Colorado. Table of contents: LED light installation 2 AN INTEGRATED ENVIRONMENTAL SOCIAL ETHICS AND GRI APPROACH STEWARDSHIP RESPONSIBILITY GOVERNANCE MATERIALS About Prologis Prologis is the global leader in logistics real estate. We own, manage and develop high-quality properties in the world’s most vibrant centers of commerce. Our 3,322 buildings in 20 countries serve 5,200+ of the world’s best brands and businesses. Customers turn to us because they know an efficient supply chain will make their operations run better and more sustainably, and that a strategic relationship with Prologis will create competitive advantage. -

Q3 2020 Market Reports

LEE-ASSOCIATES.COM/RESEARCH Q3 2020 MARKET REPORTS FEATURED MARKET REPORTS THE LEE ADVANTAGE Every Lee & Associates office delivers world-class service to an array of regional, national, and international clients - from small businesses and local investors to major corporate users and institutional investors. Our professionals combine the latest technology, resources, and market intelligence with their experience, expertise, and commitment to superior service to optimize client results. WHAT SETS US APART? Since 1979, Lee & Associates has reimagined the way that commercial real estate companies should be structured. Each Lee & Associates office is owned and operated by its professionals. As shareholders of the company, this separates us from our competition and creates one common goal; to provide seamless, consistent execution and value- driven market-to-market services to our clients. SERVICES TO MEET THE NEEDS OF OUR CLIENTS Lee & Associates’ offices offer a broad array of real estate services tailored to meet the needs of the company’s clients in each of the markets it operates, including commercial real estate brokerage, integrated services, and construction services. With specialty practice groups in each of these disciplines, our professionals regularly collaborate to make sure they are providing their clients with the most advanced, up-to-date market technology and information. LOCAL EXPERTISE INTERNATIONAL REACH With offices in 60+ markets across North America and a strategic international alliance with Gerald Eve, Lee & Associates has the ability to deliver first-class services to our clients both locally and internationally. Q3 2020 INDUSTRIAL OVERVIEW PANDEMIC SPARKS Q3 E-COMMERCE DEMAND FEATURED REPORTS A sharp increase in online shopping that was brought on by the pandemic has heightened third- • AZ, Phoenix quarter demand for industrial space. -

About Prologis

MEDIA FACT SHEET I Third Quarter 2018 About Prologis U.S. EUROPE ASIA 457 182 72 MSF MSF MSF 77% 13% 3% NOI NOI NOI OTHER AMERICAS 60 MSF 7% NOI Ahead of what’s next GLOBAL AT A GLANCE Prologis, Inc. is the global leader in logistics real estate with a focus on high-barrier, high- MSF MSQM growth markets. As of Sept. 30, 2018, the company owned or had investments in, on 771 / 71 owned, managed or under development a wholly owned basis or through co-investment ventures, properties and development projects across 771 million square feet (71 million square meters) in 19 countries. Prologis leases modern logistics facilities to a diverse base of approximately 5,500 customers. These $92 B 3,742 facilites assist the efficient distribution of goods for the world’s best businesses and brands. in total assets under industrial properties management across the Americas, Europe and Asia UNIQUE BUSINESS MODEL (%) 5,500 ~1,600 customers across colleagues serving Real Estate Strategic Capital a diverse range customers and Operations Capital Deployment of industries investors 77 74 S&P 500 Global 100 member “Most Sustainable 51 Corporations in the World” 49 9 years running 23 26 U.S. Outside U.S. U.S. Outside U.S. U.S. Outside U.S. Q3 2018 Supplemental Financial Report TOP 20 CUSTOMERS SELECT AWARDS AND RECOGNITION Comprise 19.4% of Net Effective Rent (%) • Included in 2018 Dow Jones Sustainability North America (Prologis), Asia Pacific (Nippon Prologis REIT) Amazon.com 3.3 and MILA Pacific Alliance (FIBRA Prologis) Indices DHL 1.4 • 8 GRESB Green Stars: