Worldwide Tax Summaries Corporate Taxes 2017/18

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tax Appeals Rules Procedures

Tax Appeals Tribunal Rules & Procedures The rules of the game February 2017 Glossary of terms KRA Kenya Revenue Authority TAT Tax Appeals Tribunal TATA Tax Appeals Tribunal Act TPA Tax Procedures Act VAT Value Added Tax 2 © Deloitte & Touche 2017 Definition of terms Tax decision means: a) An assessment; Tax law means: b) A determination of tax payable made to a a) The Tax Procedures Act; trustee-in-bankruptcy, receiver, or b) The Income Tax Act, Value Added liquidator; Tax Act, and Excise Duty Act; and c) A determination of the amount that a tax c) Any Regulations or other subsidiary representative, appointed person, legislation made under the Tax director or controlling member is liable Procedures Act or the Income Tax for under specified sections in the TPA; Act, Value Added Tax Act, and Excise d) A decision on an application by a Duty Act. taxpayer to amend their self-assessment return; Objection decision means: e) A refund decision; f) A decision requiring repayment of a The Commissioner’s decision either to refund; or allow an objection in whole or in part, or g) A demand for a penalty. disallow it. Appealable decision means: a) An objection decision; and b) Any other decision made under a tax law but excludes– • A tax decision; or • A decision made in the course of making a tax decision. 3 © Deloitte & Touche 2017 Pre-objection process; management of KRA Audit KRA Audit Notes The TPA allows the Commissioner to issue to • The KRA Audits are a tax payer a default assessment, amended undertaken by different assessment or an advance assessment departments of the KRA that (Section 29 to 31 TPA). -

A Glimpse at Taxation and Investment in Cyprus 2019 WTS Cyprus Cyprus

Cyprus Tax and Investment Facts A Glimpse at Taxation and Investment in Cyprus 2019 WTS Cyprus Cyprus WTS Cyprus was established It is our philosophy to provide in 2009 by professionals with attentive, re sponsive and per- significant experience in their sonalised services. For this pur- fields of expertise to serve pose the firm's management the needs of local and inter- team are closely involved in national clients as a “single all assignments and the firm’s point of contact” in the areas staff are highly committed to of Tax, Financial and Business completing engagements on Consulting services. a timely and efficient basis. Our goal is to be exceptional Our Services: in every way we can. We are → Tax Advisory and Tax committed to providing Compliance Services professional services of the → Financial and Business highest level to our clients, Advisory Services regardless of size or market. → Risk Management and We specialise in providing Assurance Engagements Tax Advisory and Tax → Accounting Compliance services, → Payroll Services Accounting and Business Advisory, as well as Risk Find more on wtmscyprus.co Management and Assurance engagements. Our services Contacts in Cyprus are not just limited to Cyprus- Nicolas Kypreos, Partner oriented matters. We can [email protected] serve clients in various other jurisdictions through our inter- Pambos Chrysanthou, Partner national network of experts, pambos.chrysanthou@ WTS Global. wtscyprus.com WTS Cyprus Ltd. is a member of WTS Global for Cyprus. 2 Tax and Investment Facts 2019 x Cyprus Table of Contents 1 Ways of Doing Business / Legal Forms of Companies 4 2 Corporate Taxation 11 3 Double Taxation Agreements 38 4 Transfer Pricing 39 5 Anti-avoidance Measures 42 6 Taxation of Individuals / Social Security Contributions 47 7 Indirect Taxes 57 8 Inheritance, Gift and Wealth Tax 63 Tax and Investment Facts 2019 x Cyprus 3 1 Ways of Doing Business / Legal Forms of Companies The Republic of Cyprus is a member of the eurozone and a Member State of the European Union. -

Tax Avoidance in Albania

ISSN 2411-9571 (Print) European Journal of Economics September – December 2020 ISSN 2411-4073 (online) and Business Studies Volume 3, Issue 3 Tax Avoidance in Albania Viola Tanto PhD Candidate in Tax Law, European University of Tirana Abstract This paper was written in order of the reforming of the tax system’s framework. Analysing phenomena such as tax evasion, tax avoidance, the use of legal loopholes to reduce tax liability in Albania was very challenged. In this paper is analysed also some other jurisdictions, which have served as a reference model for the reform of Albanian legislation, such as the Italian one and the legislation of the European Union. Recently, we were witnesses of a significant increase, in the quantitative and qualitative level, of tax evasion and tax avoidance. Often, the "battle" between the taxpayer and the contributor in bad faith is based on the probative power (burden of proof) of the elements of the transaction which must be verified by the tax administration. Even more often, this fight takes place over the basis of the correct interpretation of legal norms. Evasion is leaving more and more room for refined avoidance. Avoidance is no longer just the prerogative of big companies, corporations or powerful business groups, but it is turned into an ordinary management instrument for small and medium enterprises, even in special cases, even for natural persons. The paper analyses problems such as: basic and key aspects of tax evasion, by distinguishing with other concepts of tax law, such as tax planning and tax evasion, which are the forms of identifying tax evasion/avoidance, the meaning of the doctrine of abuse right. -

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries

Creating Market Incentives for Greener Products Policy Manual for Eastern Partnership Countries Creating Incentives for Greener Products Policy Manual for Eastern Partnership Countries 2014 About the OECD The OECD is a unique forum where governments work together to address the economic, social and environmental challenges of globalisation. The OECD is also at the forefront of efforts to understand and to help governments respond to new developments and concerns, such as corporate governance, the information economy and the challenges of an ageing population. The Organisation provides a setting where governments can compare policy experiences, seek answers to common problems, identify good practice and work to co-ordinate domestic and international policies. The OECD member countries are: Australia, Austria, Belgium, Canada, Chile, the Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Israel, Italy, Japan, Korea, Luxembourg, Mexico, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, Turkey, the United Kingdom and the United States. The European Union takes part in the work of the OECD. Since the 1990s, the OECD Task Force for the Implementation of the Environmental Action Programme (the EAP Task Force) has been supporting countries of Eastern Europe, Caucasus and Central Asia to reconcile their environment and economic goals. About the EaP GREEN programme The “Greening Economies in the European Union’s Eastern Neighbourhood” (EaP GREEN) programme aims to support the six Eastern Partnership countries to move towards green economy by decoupling economic growth from environmental degradation and resource depletion. The six EaP countries are: Armenia, Azerbaijan, Belarus, Georgia, Republic of Moldova and Ukraine. -

Tax Code SECTION VII. VALUE ADDED TAX

ANNEX III Tax Code SECTION VII. VALUE ADDED TAX CHAPTER 24. General Provisions Article 176. Concept of value added tax The value added tax, hereinafter VAT, is a form of collection to the budget of a portion of the value added in the process of the production and circulation of goods, works, and services on the territory of the Republic of Tajikistan, and of a portion of the value of all taxable goods imported onto the territory of the Republic of Tajikistan. The value added tax, as an indirect tax, is payable at all stages of the production and supply of goods, fulfilment of works, and rendering of services. The amount of VAT payable with respect to taxable turnover is determined as the difference between the sum of tax assessed on this turnover and the sum of tax that is creditable according to issued VAT invoices in accordance with this Section. CHAPTER 25. Taxpayers Article 177. Taxpayers 1. A VAT taxpayer is a person who is registered or is required to be registered as a VAT taxpayer. 2. A person who is registered is a VAT taxpayer from the time the registration takes effect. A person who is not registered, but who is required to apply to be registered, is a VAT taxpayer from the beginning of the accounting period following the period in which the obligation to apply for registration arose. 3. In addition to persons who are VAT taxpayers under point 1, all persons carrying out taxable import of goods to the Republic of Tajikistan are considered VAT taxpayers with respect to such import. -

Manual for the Negotiation of Bilateral Tax Treaties

United Nations United Nations Manual for the Negotiation of Bilateral Tax Treaties Treaties Tax the Negotiation of Bilateral for Manual Manual for the Negotiation of Bilateral Tax Treaties between Developed and Developing Countries between Developed and Developing Countries United Nations Manual for the Negotiation of Bilateral Tax Treaties between Developed and Developing Countries asdf United Nations New York, 2016 Copyright © June 2016 For further information, please contact: United Nations United Nations All rights reserved Department of Economic and Social Affairs Financing for Development Office United Nations Secretariat Two UN Plaza, Room DC2-2170 New York, N.Y. 10017, USA Tel: (1-212) 963-7633 • Fax: (1-212) 963-0443 E-mail: [email protected] Preface Domestic resource mobilization, including tax revenues, is central to achieving sustainable development. Taxes represent a stable source of finance that, complemented by other sources, is critical to financing the 2030 Agenda for Sustainable Development, including the Sustainable Development Goals (SDGs). Taxation is essential to providing public goods and services, increasing equity and helping manage macroeco- nomic stability. SDG 17 on the means of implementation and global partnership for sustainable development calls on the international community to strengthen domestic resource mobilization, including through international support to developing countries, to improve domestic capacity for tax and other revenue collection. Mobilizing domestic public revenue for investment in sus- tainable development has featured prominently on the financing for development agenda since the 1990s. The Addis Ababa Action Agenda (AAAA) of the Third International Conference on Financing for Development (Addis Ababa, 13 – 16 July 2015) provides a new global framework for financing sustainable development by aligning all financial flows and policies with economic, social and environmental priorities. -

Revenue Assignments in the Practice of Fiscal Decentralization

Georgia State University ScholarWorks @ Georgia State University ECON Publications Department of Economics 2008 Revenue assignments in the practice of fiscal decentralization Jorge Martinez-Vazquez Georgia State University, [email protected] Follow this and additional works at: https://scholarworks.gsu.edu/econ_facpub Part of the Economics Commons Recommended Citation Jorge Martinez-Vazquez. Revenue assignments in the practice of fiscal decentralization in Nuria Bosch and Jose M. Duran (eds.) Fiscal Federalism and Political Decentralization: Lessons from Spain, Germany and Canada, 27-55. Edward Elgar Publishing, 2008. This Book Chapter is brought to you for free and open access by the Department of Economics at ScholarWorks @ Georgia State University. It has been accepted for inclusion in ECON Publications by an authorized administrator of ScholarWorks @ Georgia State University. For more information, please contact [email protected]. Fiscal Federalism and Political Decentralization STUDIES IN FISCAL FEDERALISM AND STATE-LOCAL FINANCE Series Editor: Wallace E. Oates, Professor o f Economics, University o f Maryland, College Park and University Fellow, Resources for the Future, USA This important series is designed to make a significant contribution to the develop ment of the principles and practices of state-local finance. It includes both theo retical and empirical work. International in scope, it addresses issues of current and future concern in both East and West and in developed and developing countries. The main purpose of the series is to create a forum for the publication of high- quality work and to show how economic analysis can make a contribution to under standing the role of local finance in fiscal federalism in the twenty-first century. -

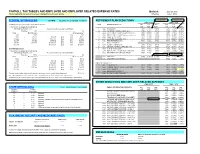

PAYROLL TAX TABLES and EMPLOYEE and EMPLOYER RELATED EXPENSE RATES Updated: June 27, 2012 *Items Highlighted in Yellow Have Been Changed Since the Last Update

PAYROLL TAX TABLES AND EMPLOYEE AND EMPLOYER RELATED EXPENSE RATES Updated: June 27, 2012 *items highlighted in yellow have been changed since the last update. Effective: July 1, 2012 FEDERAL WITHHOLDING 26 PAYS FEDERAL TAX ID NUMBER 86-6004791 RETIREMENT PLAN DEDUCTIONS 10.5% AT 50/50 10.5% AT 50/50 EMPLOYEE EMPLOYER (a) SINGLE person (including head of household) - CODE RETIREMENT PLAN DED OLD NEW DED OLD NEW If the amount of wages (after subtracting CODE RATE RATE CODE RATE RATE withholding allowances) is: The amount of income tax to withhold is: 1 ASRS PLAN-ASRS 7903 11.13% 10.90% 7904 9.87% 10.90% Not Over $83 ............................................................................................. $0 2 CORP JUVENILE CORRECTIONS (501) 7905 8.41% 8.41% 7906 9.92% 12.30% Over But not over - of excess over - 3 EORP ELECTED OFFICIALS & JUDGES (415) 7907 10.00% 11.50% 7908 17.96% 20.87% $83 - $417 10% $83 4 PSRS PUBLIC SAFETY (007) (ER pays 5% EE share) 7909 3.65% 4.55% 7910 38.30% 48.71% $417 - $1,442 $33.40 plus 15% $417 5 PSRS GAME & FISH (035) 7911 8.65% 9.55% 7912 43.35% 50.54% $1,442 - $3,377 $187.15 plus 25% $1,442 6 PSRS AG INVESTIGATORS (151) 7913 8.65% 9.55% 7914 90.08% 136.04% $3,377 - $6,954 $670.90 plus 28% $3,377 7 PSRS FIRE FIGHTERS (119) 7915 8.65% 9.55% 7916 17.76% 20.54% $6,954 - $15,019 $1,672.46 plus 33% $6,954 9 N/A NO RETIREMENT $15,019 ………………………………………………………$4,333.91 plus 35% $15,019 0 CORP CORRECTIONS (500) 7901 8.41% 8.41% 7902 9.15% 11.14% B PSRS LIQUOR CONTROL OFFICER (164) 7923 8.65% 9.55% 7924 38.77% 46.99% (b) MARRIED person F PSRS STATE PARKS (204) 7931 8.65% 9.55% 7932 18.50% 25.16% If the amount of wages (after subtracting G CORP PUBLIC SAFETY DISPATCHERS (563) 7933 7.96% 7.96% 7934 7.50% 7.90% withholding allowances) is: The amount of income tax to withhold is: H PSRS DEFERRED RET OPTION (DROP) 7957 8.65% 9.55% 0.24% AT 50/50 Not Over $312 ............................................................................................ -

Download Article (PDF)

5th International Conference on Accounting, Auditing, and Taxation (ICAAT 2016) TAX TRANSPARENCY – AN ANALYSIS OF THE LUXLEAKS FIRMS Johannes Manthey University of Würzburg, Würzburg, Germany Dirk Kiesewetter University of Würzburg, Würzburg, Germany Abstract This paper finds that the firms involved in the Luxembourg Leaks (‘LuxLeaks’) scandal are less transparent measured by the engagement in earnings management, analyst coverage, analyst accuracy, accounting standards and auditor choice. The analysis is based on the LuxLeaks sample and compared to a control group of large multinational companies. The panel dataset covers the years from 2001 to 2015 and comprises 19,109 observations. The LuxLeaks firms appear to engage in higher levels of discretionary earnings management measured by the variability of net income to cash flows from operations and the correlation between cash flows from operations and accruals. The LuxLeaks sample shows a lower analyst coverage, lower willingness to switch to IFRS and a lower Big4 auditor rate. The difference in difference design supports these findings regarding earnings management and the analyst coverage. The analysis concludes that the LuxLeaks firms are less transparent and infers a relation between corporate transparency and the engagement in tax avoidance. The paper aims to establish the relationship between tax avoidance and transparency in order to give guidance for future policy. The research highlights the complex causes and effects of tax management and supports a cost benefit analysis of future tax regulation. Keywords: Tax Avoidance, Transparency, Earnings Management JEL Classification: H20, H25, H26 1. Introduction The Luxembourg Leaks (’LuxLeaks’) scandal made public some of the tax strategies used by multinational companies. -

Environmental Taxes and Subsidies: What Is the Appropriate Fiscal Policy for Dealing with Modern Environmental Problems?

William & Mary Environmental Law and Policy Review Volume 24 (2000) Issue 1 Environmental Justice Article 6 February 2000 Environmental Taxes and Subsidies: What is the Appropriate Fiscal Policy for Dealing with Modern Environmental Problems? Charles D. Patterson III Follow this and additional works at: https://scholarship.law.wm.edu/wmelpr Part of the Environmental Law Commons, and the Tax Law Commons Repository Citation Charles D. Patterson III, Environmental Taxes and Subsidies: What is the Appropriate Fiscal Policy for Dealing with Modern Environmental Problems?, 24 Wm. & Mary Envtl. L. & Pol'y Rev. 121 (2000), https://scholarship.law.wm.edu/wmelpr/vol24/iss1/6 Copyright c 2000 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository. https://scholarship.law.wm.edu/wmelpr ENVIRONMENTAL TAXES AND SUBSIDIES: WHAT IS THE APPROPRIATE FISCAL POLICY FOR DEALING WITH MODERN ENVIRONMENTAL PROBLEMS? CHARLES D. PATTERSON, III* 1 Oil spills and over-fishing threaten the lives of Pacific sea otters. Unusually warm temperatures are responsible for an Arctic ice-cap meltdown. 2 Contaminated drinking water is blamed for the spread of avian influenza from wild waterfowl to domestic chickens.' Higher incidences of skin cancer are projected, due to a reduction in the ozone layer. Our environment, an essential and irreplaceable resource, has been under attack since the industrial age began. Although we have harnessed nuclear energy, made space travel commonplace, and developed elaborate communications technology, we have been unable to effectively eliminate the erosion and decay of our environment. How can we deal with these and other environmental problems? Legislators have many methods to encourage or discourage individual or corporate conduct. -

Taxation of Individuals 2020

Taxation of individuals Luxembourg 2020 kpmg.lu Tax year The tax year corresponds to the calendar year. Tax rates Progressive tax rates ranging from 0% to 45.78% apply to taxable income not exceeding €200,004 (€400,008 for couples taxed jointly). The excess is subject to 45.78%. The calculation of Luxembourg income taxes depends on the taxable income and the individual’s family status, i.e. the tax class. Tax classes - residents Without With Aged at least children dependent 65 years children on 1 January 2020 Single 1 1a 1a Married / Partners * 1 1/1a 1 Married/Partners - joint 2 2 2 taxation ** Separated / Divorced*** 2 / 1 2 / 1a 2 / 1a Widow(er)*** 2 / 1a 2 / 1a 2 / 1a * Joint application before 31 March of the following year for separate tax filing ** Married taxpayers file jointly: mandatory joint taxation Taxpayers who have entered into a registered partnership agreement and who shared a common residence during the whole tax year can elect to be taxed jointly *** Residents who separated (legal separation), divorced or were widowed during a specific tax year are granted tax class 2 for the next 3 tax years 2 Taxation of individuals – Luxembourg 2020 3 Tax classes - non-residents Without With Aged at least children dependent 65 years children on 1 January 2020 Single 1 1a 1a Married * / Partners 1 1 1 Married/Partners filing 2 2 2 jointly** Separated / Divorced*** 2 / 1 2 / 1a 2 / 1a Widow(er)*** 2 / 1a 2 / 1a 2 / 1a * Tax class 1a maintained for partners with dependent children or aged at least 65 years ** Specific requests before -

Tax Us If You Can 2012 FINAL.Pdf

City Research Online City, University of London Institutional Repository Citation: Murphy, R. and Christensen, J.F. (2012). Tax us if you can. Chesham, UK: Tax Justice Network. This is the published version of the paper. This version of the publication may differ from the final published version. Permanent repository link: https://openaccess.city.ac.uk/id/eprint/16543/ Link to published version: Copyright: City Research Online aims to make research outputs of City, University of London available to a wider audience. Copyright and Moral Rights remain with the author(s) and/or copyright holders. URLs from City Research Online may be freely distributed and linked to. Reuse: Copies of full items can be used for personal research or study, educational, or not-for-profit purposes without prior permission or charge. Provided that the authors, title and full bibliographic details are credited, a hyperlink and/or URL is given for the original metadata page and the content is not changed in any way. City Research Online: http://openaccess.city.ac.uk/ [email protected] tax us nd if you can 2Edition INTRODUCTION TO THE TAX JUSTICE NETWORK The Tax Justice Network (TJN) brings together charities, non-governmental organisations, trade unions, social movements, churches and individuals with common interest in working for international tax co-operation and against tax avoidance, tax evasion and tax competition. What we share is our commitment to reducing poverty and inequality and enhancing the well being of the least well off around the world. In an era of globalisation, TJN is committed to a socially just, democratic and progressive system of taxation.