Biosimilar Vs. Generic, What's the Difference?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Top Twenty Pay-For-Delay Drugs: How Drug Industry Payoffs Delay Generics, Inflate Prices and Hurt Consumers

TOP TWENTY PAY-FOR-DELAY DRUGS: HOW DRUG INDUSTRY PAYOFFS DELAY GENERICS, INFLATE PRICES AND HURT CONSUMERS oo often, consumers are forced to shoulder a heavy financial burden, or even go without needed medicine, due to the high cost of brand-name drugs. Our research indicates that one significant cause is Tthe practice called “pay for delay,” which inflates the drug prices paid by tens of millions of Americans. In a pay-for-delay deal, a brand-name drug company pays off a would-be competitor to delay it from selling a generic version of the drug. Without any competition, the brand-name company can continue demanding high prices for its drug. This list of 20 drugs known to be impacted by pay-for-delay deals represents the tip of the iceberg. Annual reports by the Federal Trade Commission (FTC) indicate that generic versions of as many as 142 brand-name drugs have been delayed by pay-for-delay arrangements between drug manufacturers since 2005.1 However, because the details of these deals rarely become public, consumers have largely been kept in the dark about the extent of the problem. Information about these twenty specific drugs affected by pay-for-delay deals has been made public thanks to legal challenges brought by the FTC, consumer class action lawsuits, research by legal experts, and public disclosures by drug makers. Key findings of our analysis of these 20 drugs impacted by pay-for-delay deals: . This practice has held back generic . These brand-name drugs cost medicines used by patients with a wide 10 times more than their generic range of serious or chronic conditions, equivalents, on average, and as much as ranging from cancer and heart disease, to 33 times more. -

The Evolution of Biosimilars in Oncology, with a Focus on Trastuzumab

EVOLUTIONPERSPECTIVES OF BIOSIMILARS IN INONCOLOGY, ONCOLOGY Nixon et al. The evolution of biosimilars in oncology, with a focus on trastuzumab †‡ N.A. Nixon MD,* M.B. Hannouf PhD, and S. Verma MD* ABSTRACT Cancer therapy has evolved significantly with increased adoption of biologic agents (“biologics”). That evolution is especially true for her2 (human epidermal growth factor receptor-2)–positive breast cancer with the introduction of trastuzumab, a monoclonal antibody against the her2 receptor, which, in combination with chemotherapy, significantly improves survival in both metastatic and early disease. Although the efficacy of biologics is undeniable, their expense is a significant contributor to the increasing cost of cancer care. Across disease sites and indications, biosimilar agents are rapidly being developed with the goal of offering cost-effective alternatives to biologics. Biosimilars are pharmaceuticals whose molecular shape, efficacy, and safety are similar, but not identical, to those of the original product. Although these agents hold the potential to improve patient access, complexities in their production, evaluation, cost, and clinical application have raised questions among experts. Here, we review the landscape of biosimilar agents in oncology, with a focus on trastu- zumab biosimilars. We discuss important considerations that must be made as these agents are introduced into routine cancer care. Key Words Biosimilars, trastuzumab, Herceptin, value Curr Oncol. 2018 Jun;25(S1):S171-S179 www.current-oncology.com INTRODUCTION alternatives to biologics. Although these agents have the potential to improve patient access, complexities in their In recent years, cancer treatment has been revolutionized production, evaluation, and clinical application have raised by the introduction of biologic agents (“biologics”). -

Biopharmaceutical Notes

An Overview of the BioPharmaceutical Products and Market By Paul DiMarco, Vice President, Global Commercial Program, BioSpectra Inc. Table of Contents INTRODUCTION: ........................................................................................................................................ 2 History ....................................................................................................................................................... 2 Background information ........................................................................................................................... 3 Defining biological products ..................................................................................................................... 4 Small vs. Large Molecule Regulation and Registration in the USA and EU ............................................... 6 Controversial Regulatory Concepts: ......................................................................................................... 7 Extrapolation: ........................................................................................................................................ 7 Switching: .............................................................................................................................................. 8 Interchangeability: ................................................................................................................................ 9 Harmonization: .................................................................................................................................... -

Getting to Lower Prescription Drug Prices the Key Drivers of Costs and What Policymakers Can Do to Address Them

Getting to Lower Prescription Drug Prices The Key Drivers of Costs and What Policymakers Can Do to Address Them Henry A. Waxman Bill Corr Jeremy Sharp Ruth McDonald Kahaari Kenyatta OCTOBER 2020 OCTOBER 2020 Getting to Lower Prescription Drug Prices: The Key Drivers of Costs and What Policymakers Can Do to Address Them Henry A. Waxman, Bill Corr, Jeremy Sharp, Ruth McDonald, and Kahaari Kenyatta ABSTRACT ISSUE: Unsustainably high prescription drug prices are a concern for patients, employers, states, and the federal government. There is widespread public support for addressing the problem, and enacting policies to lower drug prices has been a top concern for Congress and the administration over the past three years. Despite this attention, structural changes have not been enacted to rein in drug prices. GOAL: To document the drivers of high U.S. prescription drug prices and offer a broad range of feasible federal policy actions. METHODS: Interviews with experts and organizations engaged on policies related to prescription drug pricing. Review of policy documents, white papers, journal articles, proposals, and position statements. KEY FINDINGS: Action in five areas is key to increasing access to and affordability of medications for Americans: 1) allow the federal government to become a more responsible purchaser; 2) stop patent abuses and anticompetitive practices that block price competition; 3) build a sustainable biosimilar market to create price competition; 4) fix incentives in the drug supply chain and make the supply chain more transparent; and 5) ensure public accountability in the government-funded drug development process. Congress and regulators have a wide range of tools at their disposal to address high drug prices and spending. -

The Process Defines the Product: What Really Matters in Biosimilar Design and Production?

RHEUMATOLOGY Rheumatology 2017;56:iv14iv29 doi:10.1093/rheumatology/kex278 The process defines the product: what really matters in biosimilar design and production? Arnold G. Vulto1 and Orlando A. Jaquez2 Abstract Biologic drugs are highly complex molecules produced by living cells through a multistep manufacturing process. The key characteristics of these molecules, known as critical quality attributes (CQAs), can vary based on post-translational modifications that occur in the cellular environment or during the manufacturing process. The extent of the variation in each of the CQAs must be characterized for the originator molecule and systematically matched as closely as possible by the biosimilar developer to ensure bio-similarity. The close matching of the originator fingerprint is the foundation of the biosimilarity exercise, as the analytical tools designed to measure differences at the molecular level are far more sensitive and specific than tools available to physicians during clinical trials. Biosimilar development, therefore, has a greater focus on preclinical attri- butes compared with the development of an original biological agent. As changes in CQAs can occur at different stages of the manufacturing process, even small modifications to the process can alter biosimilar attributes beyond the point of similarity and impact clinical effectiveness and safety. The manufacturer’s ability to provide consistent production and quality control will greatly influence the acceptance of biosimilars. To this end, preventing drift from the required specifications over time and avoiding the various implications brought by product shortage will enhance biosimilar integration into daily practice. As most prescribers are not familiar with this new drug development paradigm, educational programmes will be needed so that prescribers see biosimilars as fully equivalent, efficacious and safe medicines when compared with originator products. -

Filgrastim (Neupogen®); Filgrastim-Aafi (Nivestym™); Filgrastim- Sndz (Zarxio™); Tbo-Filgrastim (Granix®) (Subcutaneous/Intravenous)

Colony Stimulating Factors: Filgrastim (Neupogen®); Filgrastim-aafi (Nivestym™); Filgrastim- sndz (Zarxio™); Tbo-Filgrastim (Granix®) (Subcutaneous/Intravenous) Document Number: DMBA-0235 Last Review Date: 04/01/2020 Date of Origin: 10/17/2008 Dates Reviewed: 06/2009, 12/2009, 06/2010, 07/2010, 09/2010, 12/2010, 03/2011, 6/2011, 09/2011, 12/2011, 03/2012, 06/2012, 09/2012, 12/2012, 03/2013, 06/2013, 09/2013, 12/2013, 03/2014, 06/2014, 09/2014, 12/2014, 03/2015, 04/2015, 08/2015, 11/2015, 02/2016, 05/2016, 08/2016, 11/2016, 02/2017, 05/2017, 08/2017, 11/2017, 02/2018, 05/2018, 04/2019, 04/2020 I. Length of Authorization Coverage will be provided for four months and may be renewed. II. Dosing Limits A. Quantity Limit (max daily dose) [NDC Unit]: − Neupogen 300 mcg vial: 3 vials per 1 day − Neupogen 300 mcg SingleJect: 3 syringes per 1 day − Neupogen 480 mcg vial: 3 vials per 1 day − Neupogen 480 mcg SingleJect: 3 syringes per 1 day − Nivestym 300 mcg vial: 3 vials per 1 day − Nivestym 300 mcg prefilled syringe: 3 syringes per 1 day − Nivestym 480 mcg vial: 3 vials per 1 day − Nivestym 480 mcg prefilled syringe: 3 syringes per 1 day − Zarxio 300 mcg prefilled syringe: 3 syringes per 1 day − Zarxio 480 mcg prefilled syringe: 3 syringes per 1 day − Granix 300 mcg pre-filled syringe: 4 syringes per 1 day − Granix 300 mcg single-dose vial: 4 vials per 1 day − Granix 480 mcg pre-filled syringe: 3 syringes per 1 day − Granix 480 mcg single-dose vial: 3 vials per 1 day B. -

Merck & Co., Inc

As filed with the Securities and Exchange Commission on February 25, 2021 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D. C. 20549 _________________________________ FORM 10-K (MARK ONE) ☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the Fiscal Year Ended December 31, 2020 OR ☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from to Commission File No. 1-6571 _________________________________ Merck & Co., Inc. 2000 Galloping Hill Road Kenilworth New Jersey 07033 (908) 740-4000 New Jersey 22-1918501 (State or other jurisdiction of incorporation) (I.R.S Employer Identification No.) Securities Registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol(s) Name of Each Exchange on which Registered Common Stock ($0.50 par value) MRK New York Stock Exchange 1.125% Notes due 2021 MRK/21 New York Stock Exchange 0.500% Notes due 2024 MRK 24 New York Stock Exchange 1.875% Notes due 2026 MRK/26 New York Stock Exchange 2.500% Notes due 2034 MRK/34 New York Stock Exchange 1.375% Notes due 2036 MRK 36A New York Stock Exchange Number of shares of Common Stock ($0.50 par value) outstanding as of January 31, 2021: 2,530,315,668. Aggregate market value of Common Stock ($0.50 par value) held by non-affiliates on June 30, 2020 based on closing price on June 30, 2020: $195,461,000,000. Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

Cigna Standard 4-Tier Prescription Drug List

CIGNA STANDARD 4-TIER PRESCRIPTION DRUG LIST Coverage as of January 1, 2022 Offered by: Cigna Health and Life Insurance Company, Connecticut General Life Insurance Company, or their affiliates. 916152 j Standard 4-Tier O/I SRx 08/21 What’s inside? About this drug list 3 How to read this drug list 3 How to find your medication 5 Specialty medications 18 Medications that aren’t covered 25 Frequently Asked Questions (FAQs) 41 Exclusions and limitations for coverage 45 View the drug list online This document was last updated on 08/01/2021.* You can go online to see the current list of medications your plan covers. myCigna® App and myCigna.com. Click on the “Find Care & Costs” tab and select “Price a Medication.” Then type in your medication name to see how it’s covered. Cigna.com/PDL. Scroll down until you see a pdf of the Cigna Standard 4-Tier Prescription Drug List (all specialty medications covered on Tier 4). Questions? › myCigna.com: Click to chat Monday-Friday, 9:00 am-8:00 pm EST. › By phone: Call the toll-free number on your Cigna ID card. We’re here 24/7/365. * Drug list created: originally created 01/01/2004 Last updated: 08/01/2021, for changes Next planned update: 03/01/2022, for starting 01/01/2022 changes starting 07/01/2022 2 About this drug list This is a list of the most commonly prescribed medications covered on the Cigna Standard 4-Tier Prescription Drug List as of January 1, 2022.1,2 Medications are listed by the condition they treat, then listed alphabetically within tiers (or cost-share levels). -

2019 FDA Biopharmaceutical Approvals: a Record Year for Follow-On Products, but Is Innovation Lagging? Bioplan Associates, Inc

Confidential White Paper – Not for Distribution 2019 FDA Biopharmaceutical Approvals: A Record Year for Follow-on Products, But is Innovation Lagging? BioPlan Associates, Inc. January 2020 Introduction Although 2019 was overall a good year for biopharmaceutical product approvals, there was a lower percentage of approvals for fully new, innovative products compared with prior years. This may indicate problems with recent years’ pharmaceutical industry increased investment in biopharmaceutical vs. drug R&D, with a relative increase in resulting innovative product approvals not showing up yet. It may be too early to make conclusions regarding the extent of this pipeline trend, but the record portion of follow-on product approvals (63% of approvals) can be viewed as positive or negative for the industry. Biopharmaceuticals are here defined as prescription therapeutic products containing active agents manufactured using biotechnology methods, i.e., using living organisms (1). Figure 1 shows the numbers of recombinant and non-recombinant biopharmaceuticals approved by FDA since 1981, when the first recombinant protein received approval. Total biopharmaceutical approvals have increased over the years while remaining steady in the past few years. Figure 1: Numbers of Recombinant and Non-Recombinant Biopharmaceuticals Approved by FDA, 1981-2019 ©2020 BioPlan Associates, Inc, 2275 Research Blvd., Ste. 500, Rockville, MD 20850 (301) 921-5979 Page: 1 Confidential White Paper – Not for Distribution Approvals in 2019 In Table 1 we present approvals during 2019. Several oligonucleotide therapeutics, both antisense and RNAi, also received approval, but these are synthetically manufactured drugs and not considered biopharmaceuticals. Other products not included as biopharmaceuticals include medical devices, allergenic extract products, and diagnostics that receive biologics (BLA) approvals. -

Why Are Some Generic Drugs Skyrocketing in Price? Hearing Committee on Health, Education, Labor, and Pensions United States Sena

S. HRG. 113–859 WHY ARE SOME GENERIC DRUGS SKYROCKETING IN PRICE? HEARING BEFORE THE SUBCOMMITTEE ON PRIMARY HEALTH AND AGING OF THE COMMITTEE ON HEALTH, EDUCATION, LABOR, AND PENSIONS UNITED STATES SENATE ONE HUNDRED THIRTEENTH CONGRESS SECOND SESSION ON EXAMINING THE PRICING OF GENERIC DRUGS NOVEMBER 20, 2014 Printed for the use of the Committee on Health, Education, Labor, and Pensions ( Available via the World Wide Web: http://www.gpo.gov/fdsys/ U.S. GOVERNMENT PUBLISHING OFFICE 24–459 PDF WASHINGTON : 2017 For sale by the Superintendent of Documents, U.S. Government Publishing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate Nov 24 2008 13:32 May 19, 2017 Jkt 000000 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 S:\DOCS\24459.TXT DENISE HELPN-003 with DISTILLER COMMITTEE ON HEALTH, EDUCATION, LABOR, AND PENSIONS TOM HARKIN, Iowa, Chairman BARBARA A. MIKULSKI, Maryland LAMAR ALEXANDER, Tennessee PATTY MURRAY, Washington MICHAEL B. ENZI, Wyoming BERNARD SANDERS (I), Vermont RICHARD BURR, North Carolina ROBERT P. CASEY, JR., Pennsylvania JOHNNY ISAKSON, Georgia KAY R. HAGAN, North Carolina RAND PAUL, Kentucky AL FRANKEN, Minnesota ORRIN G. HATCH, Utah MICHAEL F. BENNET, Colorado PAT ROBERTS, Kansas SHELDON WHITEHOUSE, Rhode Island LISA MURKOWSKI, Alaska TAMMY BALDWIN, Wisconsin MARK KIRK, Illinois CHRISTOPHER S. MURPHY, Connecticut TIM SCOTT, South Carolina ELIZABETH WARREN, Massachusetts DEREK MILLER, Staff Director LAUREN MCFERRAN, Deputy Staff Director and Chief Counsel DAVID P. CLEARY, Republican Staff Director SUBCOMMITTEE ON PRIMARY HEALTH AND AGING BERNARD SANDERS, Vermont, Chairman BARBARA A. -

Biologic, Biosimilar, Generic, and Brand

BIOSIMILARS Breaking Down the Differences Between Drug Types: Biologic, Biosimilar, Generic, and Brand-Name Drugs BIOSIMILARS This resource is designed to help you understand the differences between biosimilar, biologic, generic, and brand-name drugs so that you can be as informed as possible when it comes to treatment decisions. TABLE OF CONTENTS 2 · Introduction 3 · An Analogy: Cookies & Beer ABOUT FIGHT 4 · Background: Small and COLORECTAL CANCER Large Molecule Drugs We FIGHT to cure colorectal cancer and serve as relentless champions 7 · The Comparisons: of hope for all affected by this Brand-Name vs Generic disease through informed patient & Biologic vs Biosimilar support, impactful policy change, and breakthrough research endeavors. 13 · Making Your Decision 14 · More Information MEDICAL DISCLAIMER & Support The information and services provided by Fight Colorectal Cancer are for general informational purposes only and are not intended to be substitutes for professional medical advice, diagnoses, or treatment. If you are ill, or suspect that you are ill, see a doctor immediately. In an emergency, call 911 or go to the nearest emergency room. Fight Colorectal Cancer never recommends or endorses any specific physicians, products, or treatments for any condition. This mini magazine does not serve as an advertisement or endorsement for any products COVER: or sponsors mentioned. Patrick Moote Stage III survivor 1 • FightCRC.org • INTRODUCTION HILE AT THE PHARMACY OR IN YOUR DOCTOR’S OFFICE, you may have heard the terms “generic” and “brand-name.” WGeneric and brand-name drugs will remain staples in our healthcare system, and there’s a new kid on the block that you may soon encounter: biosimilars. -

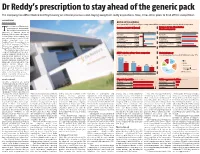

Dr Reddy's Prescription to Stay Ahead of the Generic Pack

Dr Reddy’s prescription to stay ahead of the generic pack The company has differentiated itself by focusing on internal processes and staying away from costly acquisitions. Now, it has other plans to fend off the competition B DASARATH REDDY Hyderabad, 8 August BATTLE OF THE GENERICS As the patent cliff in the US levels off, generic drug makers will face increasing pressure to develop other kinds of products he revenues of Hyderabad- Revenues in 2011-12 (Actual) Revenue for top-three Indian based generic drug maker, Pharma companies T Dr Reddy's Laboratories, is expected to surpass those of ~ crore Revenue Net profit ~ crore 2012-13 2013-14* Ranbaxy Laboratories, the largest Ranbaxy 9,977 Ranbaxy 11,309 Indian generic drug company, and Laboratories* -2,900 Laboratories 12,615 now a subsidiary of Japan’s Daiichi Dr Reddy's 9,674 Dr Reddy's 11,286 Sankyo, sometime next year. Laboratories** 1,426 Laboratories 12,663 Barclays Equity Research projects 8,006 9,694 Dr Reddy’s revenues for FY14 at Sun Pharmaceutical Sun Pharmaceutical 2,587 11,472 ~12,663 crore, slightly higher than Industries** Industries Ranbaxy’s (at ~12,615 crore). *Calendar year 2011, **FY ended March 2012 *Estimates This would be big news for any company battling it out in a chal- ANDA* pipeline of top-three companies Global pharmacy lenging industry. However, the Approved Pending Share of consolidated revenues for Dr Reddy's in the year ‘11-12 generic-drug business is more than just that. It’s a fiercely com- 241 petitive business, driven by vol- umes and characterised by con- 148 148 stantly falling prices and, 101 therefore, steep margins.