Pharmaceuticals Stellar Quarter; Healthy Outlook Sector Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SANJEEVAK 1586083 01/08/2007 MANOJ ANANT JOSHI Trading As ;AKSHAY PHARMA REMEDIES KAVRANA HOUSE, OPP

Trade Marks Journal No: 1836 , 12/02/2018 Class 5 SANJEEVAK 1586083 01/08/2007 MANOJ ANANT JOSHI trading as ;AKSHAY PHARMA REMEDIES KAVRANA HOUSE, OPP. COTTON GREEN RLY. STN. MUMBAI-400033. MANUFACTURE & MERCHANT INDIAN NATIONAL Used Since :31/01/2001 MUMBAI MEDICINAL PREPARATIONS. 537 Trade Marks Journal No: 1836 , 12/02/2018 Class 5 SEPTIGARD 1741718 08/10/2008 INDERJIT SINGH trading as ;INDERJIT SINGH B-104 , SWASTHYA SINGH , NEW DELHI -92 MERCHANTS & MANUFACTUERERS Address for service in India/Agents address: MAHTTA & CO. 43 - B/3, MAHTTA HOUSE,UDHAM SINGH NAGAR, LUDHIANA - 141 001, (PUNJAB). Proposed to be Used DELHI MEDICINAL & PHARMACEUTICAL PREPARATIONS. 538 Trade Marks Journal No: 1836 , 12/02/2018 Class 5 FAIR & BEAUTY 1803779 08/04/2009 GALPHA LABORATORIES LIMITED 221, Kanakia Zillion, E Wing Bandra Kurla Complex Annex LBS Marg & CST Road Junction Kurla West MUMBAI 400070 MANUFACTURERS AND MERCHANTS INDIAN NATIONAL Used Since :15/11/2007 MUMBAI PHARMACEUTICAL AND MEDICINAL PREPARATIONS AND SUBSTANCES 539 Trade Marks Journal No: 1836 , 12/02/2018 Class 5 O-BAMA 1815900 08/05/2009 KREMOINT PHARMA PVT. LTD. 151/5, SHRI KRISHNA DARSHAN, GARODIA NAGAR, GHATKOPAR (E), BOMBAY-400 077. MANUFACTURERS AND MERCHANTS. A CORPORATE ENTITY INCORPORATED IN INDIA UNDER THE COMPANIES ACT 1956. Address for service in India/Attorney address: KRISLAW CONSULTANTS BUILDING NO.4, C/104, SHANKESHWAR PALMS, BEHIND MODEL SCHOOL, KUMBHARKHANPADA, SUBHASH ROAD, DOMBIVILI(W) 421202 Used Since :02/05/2009 MUMBAI PHARMACETICAL AND MEDICINAL PREPARATIONS. 540 Trade Marks Journal No: 1836 , 12/02/2018 Class 5 AYUSHAKTI D-VYRO 1815928 08/05/2009 SMITA NARAM BUNGALOW NO.31, NEXT TO M. -

Hy Sun Missed the Pharma Rally: the Answer Is Hidden in a Bet Many Failed — Speciality Drugs - the Economic Times

12/3/2020 Sun Pharma: Why Sun missed the pharma rally: the answer is hidden in a bet many failed — speciality drugs - The Economic Times Home ETPrime Markets News Industry RISE Politics Wealth MF Tech Jobs Opinion NRI Panache ET NOW More Aayush English Edition | E-Paper Tech Consumer Markets Corporate Governance Telecom + OTT Auto + Aviation Pharma Fintech + BFSI Economy Infra Environment Energy Business News › Prime › Pharma › Why Sun missed the pharma rally: the answer is hidden in a bet many failed — speciality drugs Getty Images MARKETS hy Sun missed the pharma rally: the answer is hidden in a bet many failed — speciality drugs Dilip Shanghvi, founder and managing director, Sun Pharmaceuticals Synopsis Sun Pharma is the only Indian company to have made some inroads into speciality drugs. What worries investors is high investments and uncertainties over ramp up in revenue. The stock can still see upside because of its current valuations, strong India business, and any positive surprises in US generic business. But it is crucial that its speciality bet pays off. BACK TO TOP https://economictimes.indiatimes.com/prime/pharma-and-healthcare/why-sun-missed-the-pharma-rally-the-answer-is-hidden-in-a-bet-many-failed-spe… 1/11 12/3/2020 Sun Pharma: Why Sun missed the pharma rally: the answer is hidden in a bet many failed — speciality drugs - The Economic Times Home ETPrime Markets NeCwasllI nitd uas trbyleRssISiEngP oilniti cdsisWgeuailthse fMoFr tTheceh InJodbisanOpinion NRI Panache ET NOW More pharmaceutical industry. The stocks of pharma companies have been on a tear since the beginning of the Covid-19 crisis. -

Saturday, 23Rd August 2014 Index Levels : Market Trend (Nifty)

` Saturday, 23rd August 2014 Index Levels : Market Trend (Nifty): Trend Reversal Point INDEX SUPPORTS RESISTANCES Period Current Trend (TRP)Nifty close basis NIFTY# 7930/8000/8090 Short Term Trend UP DOWN BELOW 7750 (7913.20) 7850/7760 SENSEX# 26250/26000 26550/26700/27200 Medium Term UP DOWN BELOW 7650 (26419.55) ITE-35* -------- -------- Long Term Trend UP DOWN BELOW 6500 (10239.68) ND #as on 22 August 2014 Imtiaz Merchant’s Best Picks: Indices: CURRENT Domestic COMPANY NAME SIZE SECTOR Close Points % Chg PRICE Indices Large Cipla Health Care 499 BSE Sensex 26419.55 59.44 0.23 % Cap Large Industrials and UPL 338 Nifty 7913.20 22.10 0.28 % Cap Capital Goods ITE Shariah 10239.68 42.83 0.42 % 35* S&P CNX 500 1919.15 4.92 0.12 % Note: (Buying should be done from a medium to long term perspective) Shariah Advance/ Advance Decline AD Un- Market Brief Decline Ratio Changed BSE 1462 1572 0.93:1 114 On the back of positive global cues and some NSE 693 782 0.89:1 60 reform announcements by the Union Shariah Government, the markets on Friday ended the Universe*** 291 269 1.08:1 15 day and the week on positive note; Auto, Info. Technology and Health Care sectors were the flavor of the week. The undertone appears to Global Indices Close Points % Chg be bullish. All the trends are up. More reform Dow Jones* 16979.13 60.36 0.36% announcements from the Govt. and good NASDAQ* 4526.48 5.62 0.12% corporate results will further fuel the rally and FTSE* 6755.48 22.18 0.33% the Nifty is likely to see the 8000 level soon. -

In the United States District Court for the Eastern District of Michigan

Case 2:10-cv-10656-AC-MKM Document 1 Filed 02/16/10 Page 1 of 11 IN THE UNITED STATES DISTRICT COURT FOR THE EASTERN DISTRICT OF MICHIGAN ABBOTT LABORATORIES and ) ABBOTT RESPIRATORY LLC, ) ) Plaintiffs, ) ) C.A. No. 2:10-cv-10656 v. ) ) SUN PHARMACEUTICAL INDUSTRIES, LTD. ) and SUN PHARMA GLOBAL FZE, ) ) Defendants. ) COMPLAINT Plaintiffs Abbott Laboratories and Abbott Respiratory LLC (collectively, “Abbott”), by their attorneys, hereby allege as follows: Nature of the Action This is an action for patent infringement of U.S. Patent Nos. 6,080,428 (“the ‘428 patent”) and 6,469,035 (“the ‘035 patent”), arising under the patent laws of the United States, Title 35, United States Code, 35 U.S.C. §§ 271 and 281. This action relates to Abbreviated New Drug Application (“ANDA”) No. 20-0484 filed by Sun Pharma Global FZE (“Sun FZE”) with the U.S. Food and Drug Administration (“FDA”) for approval to market 500 mg and 1000 mg niacin extended-release tablets that are generic versions of the 500 mg and 1000 mg strength versions of Abbott’s highly successful NIASPAN® drug product. Related Actions The present action is related to an identical patent infringement action pending before the United States District Court for the District of Delaware, Abbott Laboratories and Abbott Case 2:10-cv-10656-AC-MKM Document 1 Filed 02/16/10 Page 2 of 11 Respiratory, LLC v. Sun Pharmaceutical Industries, Ltd. and Sun Pharmaceuticals, Inc. (C.A. 10-cv-112) (the “Delaware Sun Action”), pertaining to ANDA No. 20-0484 filed by Sun FZE for approval to market generic versions of Abbott’s 500 mg and 1000 mg strength NIASPAN® tablets. -

INDIA OUTBOUND T&A Consulting Volume 6 Issue 4 3Rd April, 2017

INDIA OUTBOUND T&A Consulting Volume 6 Issue 4 3rd April, 2017 As the Financial Year comes to an end so has an eventful The trend among Indian pharma firms of “building brands“ quarter. With the liquidity shock of de-monetization having been continued, with Aurobindo Pharma adding to its portfolio of managed and a healthy, albeit counter-intuitive GDP data biosimilars acquired from a Swiss firm and leveraging market (annualised GDP growth at 7.0% for Oct-Dec Qtr) having access across specialized therapeutic segments provided by a established the soundness of macroeconomic fundamentals, the Portugese generics firm. Also active was Piramal Enterprises, high for the current Government came in the form of results for acquiring the drug portfolio of UK-based Mallinckrodt LLC to reach a the Uttar Pradesh elections. The win for the Bhartiya Janata targeted segment across eight European markets. Sun Pharma and Party in U.P. has consolidated its hold at the Centre and across Zydus Cadilla were active in North America, with Zydus acquiring a India. What that means going forward is further stability on US drug firms for a sizeable cheque to bolster its specialty India’s policy front. Case in point has been the Government’s pharmaceuticals segment whilst Sun Pharma acquired a small push in the on-going budget session of Parliament to meet the Canadian drug discovery firm. On the IT front, the bigger boys of Indian July 2017 deadline in implementing the Goods and Services IT were active acquiring assets in Latin America and their preferred market Tax. The outbound investment story nevertheless continues - United States. -

Chairperson Speech 2021-Final.Cdr

Unwavering Purpose Chairperson’s AGM Speech 43rd Annual General Meeting Friday, July 23, 2021, Bengaluru, India Kiran Mazumdar-Shaw Executive Chairperson 2 Dear Shareholders, As we connued with our operaons, we also focused on protecng our people and ensuring It gives me great pleasure to welcome you their health and well-being. We invested in to the 43rd Annual General Meeting of implemenng strict safety protocols and your company. regularly engaged with our people to keep them movated. The leadership team constantly The pharmaceutical and healthcare monitored the fast-evolving situaon and took industry's fight against COVID-19 data-driven decisions for operaonal planning across our facilies. intensified over the past year as fresh waves of infections hit many countries REALIZING THE BIOSIMILARS PROMISE around the world. As the pandemic left societies and economies in disarray, Our Biosimilars business revenue at Rs 28,002 million, recorded a growth of 21% in FY21. We biotechnology-led companies quickly commercialized our third biosimilar, Insulin developed diagnostics, vaccines and Glargine, in the U.S. and obtained regulatory therapies to tilt the battle in favor of approvals for key biosimilars Bevacizumab and humanity. Insulin Aspart in the European Union. Our biosimilars benefited 3.1 million paents during India has been at the forefront of this the year. crusade, producing cost-effective As the only company from India to have three vaccines at scale for millions of people. biosimilars commercialized in the U.S. and among At the same time, the country has the select few globally to have five biosimilars approved in Europe, we are confident of enabling continued to supply the world with affordable access to expensive biologic drugs for generic and biosimilar therapies to millions of paents globally. -

Annual-Report-1.Pdf

p Composite Default screen Cover.prn D:\SUN BACK UP\Sun annula report-03-04\H8532 COVER and BK Aws.cdr Monday, August 22, 2005 12:23:20 PM p Composite Default screen Inside Ft.prn D:\SUN BACK UP\Sun annula report-03-04\H8532 COVER and BK Aws.cdr Monday, August 22, 2005 12:25:28 PM Color profile: Disabled Composite 175 lpi at 45 degrees A female bias for the blues? For long, scientists have observed that women are more vulnerable to depression. For long, this has been attributed by turns to an excitable nervous system, the opposing tugs of work and family. Researchers are now looking for a scientific reason for this discrepancy and it may be because of genes. Scientists say that depression in women is a global phenomenon cutting across class divides, spanning life experiences. Several genes, along with the surges in hormones may influence brain chemistry and trigger The cover shows 2 images from breakthroughs in depression. A risk factor linked to ruminating, over thinking, mulling over issues and re- neuroscience: a neuron, an MRI scan. living sad incidents is more common in women and could lead on to depression. However, half the risk could be genetic, with areas that cause this deep sadness now Two ideas that took learning from one field,and in an identified. And these genes act in concert with estrogen receptors with variations in sex inspired moment, “a flash of lightening” showed hormones in a complex interplay of hormones, neurotransmitters and receptor how best they could be applied to another field, activation. -

No. 31015/68/2017-Pricing GOVERNMENT of INDIA MINISTRY of CHEMICALS & FERTILIZERS DEPARTMENT of PHARMACEUTICALS ………

No. 31015/68/2017-Pricing GOVERNMENT OF INDIA MINISTRY OF CHEMICALS & FERTILIZERS DEPARTMENT OF PHARMACEUTICALS ……….. A Wing, Shastri Bhawan, New Delhi 110 001 Subject: Two review applications of M/s Abbott Healthcare Pvt. Limited against price fixation of their formulations “Sodium Valproate - CR Tablets 300mg and Sodium Valproate - CR Tablets 500mg” vide NPPA order No. S.O. 1687(E), dated 24.05.2017 issued under Drugs (Prices Control) Order, 2013 (DPCO 2013). Ref: 1) Two review applications, both dated 16.06.2017 2) NPPA notification under review S.O. No.1687(E), dated 24.05.2017 3) Record Note of discussions held in the personal hearing on 10.10.2017. 1. These are two petitions under paragraph 31 of the Drugs (Prices Control) Order, 2013 (hereinafter called the DPCO) filed by M/s Abbott Healthcare Pvt. Limited (hereinafter called the petitioner) against notification S.O. No.1687(E), dated 24.05.2017 issued by the National Pharmaceutical Pricing Authority (hereinafter called the NPPA) fixing the ceiling price of their formulations Sodium Valproate - CR Tablets 300mg and Sodium Valproate - CR Tablets 500mg. 2. The petitioner has contended as under: (i) Company submitted that NPPA has not considered MAT value & PTR data of M/s Sun Pharma who is a major player in this molecule. (ii) M/s Sun Pharma’s data as per AWACS dataset as given below:- SKU Name Company Aug’15 PTR MAT VAL (RS.) Encorate Sun Pharma Laboratories 52.34 21,98,63,785 Chrono 300 mg Limited tablet 10 Encorate Sun Pharma Laboratories 83.90 29,69,90,018 Chrono 300 mg Limited tablet 10 (iii) In view of above, company requested to advise NPPA to correct the apparent variance in calculation. -

Sun Pharma Launches Ready-To-Infuse INFUGEM in the U.S

Sun Pharmaceutical Industries Ltd. SUN HOUSE, CTS No. 201 B/1, Western Express Highway, Goregaon (E), Mumbai 400063, India Tel.: (91-22) 4324 4324 Fax.: (91-22) 4324 4343 CIN: L24230GJ1993PLC019050 www.sunpharma.com FOR IMMEDIATE RELEASE Sun Pharma Launches Ready-to-Infuse INFUGEM in the U.S. INFUGEMTM (gemcitabine in sodium chloride injection) is the first and only chemotherapy product in a premixed, ready-to-infuse formulation Use of ready-to-infuse bags eliminates steps in the complex chemotherapy preparation process, reducing exposure and mitigating inherent provider and patient safety risks Mumbai, India & Princeton, NJ, April 8, 2019 -- – Sun Pharmaceutical Industries Ltd. (Reuters: SUN.BO, Bloomberg: SUNP IN, NSE: SUNPHARMA, BSE: 524715, “Sun Pharma” and includes its subsidiaries and/or associate companies) today announced that INFUGEM™ (gemcitabine in sodium chloride injection), for intravenous use, is now commercially available in the U.S. INFUGEM, the first chemotherapy product that comes in a premixed, ready-to-infuse formulation, was approved by the U.S. Food and Drug Administration (FDA) in July 2018 in combination with other drugs for the treatment of breast, ovarian, non-small cell lung cancers, and as a single agent for the treatment of pancreatic cancer. INFUGEM is an alcohol-free, clear, colorless, sterile solution of 10mg/mL gemcitabine in 0.9% sodium chloride that is supplied to pharmacists in ready-to-infuse bags as a Spike & Go™ package. It involves dose banding practice, whereby standardized doses of intravenous cytotoxic drugs are used for ranges (or “bands”) of doses calculated for individual patients. INFUGEM is the only available gemcitabine formulation that does not require reconstitution and syringe withdrawal prior to intravenous administration. -

Trend Analysis of Cost Components in Select Pharmaceutical Companies

International Journal of Recent Technology and Engineering (IJRTE) ISSN: 2277-3878, Volume-8 Issue-4, November 2019 Trend Analysis of Cost Components in Select Pharmaceutical Companies C Samuel Joseph, F J Peter Kumar, S. Paul Jefferson Clarence entrepreneurial, and ‘in-touch’ with reality. Spending for Abstract: The purpose in this paper is to identify the cost Medicine in India is expected to raise between 9-12 percent components which are vital in consideration towards for 2018-22 which is driven by increasing consumer manufacturing especially in pharmaceutical companies. The spending, and raising healthcare insurance among others. manufacturing costs are significant in total expenses in pharmaceutical industry. In this study, a thorough investigation 1.2 Statement of Problem on the cost components and the trend in expenses and operating profit of pharma companies are studied, giving due regard to cost In Pharmaceutical sector, the cost of a new drug to reach components to have understanding and to find out how they may the market place has been steadily goes in an upward swing. differ among various types of pharma companies. The data But at the same time the market showed 5.5 per cent in 2017 published in the annual reports from 2009 to 2018 of top five to 7.1 per cent. Medicine sales in India raised to 8.1 per cent pharmaceutical companies based on their annual revenues has year-on-year in November 2017. Much expenses are incurred been selected for further diagnosis. The analysis reveals that in the pre-clinical trials. Further it takes about 7 to 10 years of manufacturing costs are different for all the five companies. -

Pharma Majors Collaborate for Clinical Trial of Investigational Oral Anti-Viral Drug Molnupiravir for COVID-19

Pharma Majors Collaborate for Clinical Trial of Investigational Oral Anti-Viral Drug Molnupiravir for COVID-19 Cipla, Dr. Reddy’s, Emcure, Sun Pharma and Torrent to collaborate for clinical trial of investigational anti-viral drug Molnupiravir for COVID-19 India. June 29, 2021 - Cipla Limited (BSE: 500087; NSE: CIPLA EQ, referred to as “Cipla”), Dr. Reddy’s Laboratories Ltd. (BSE: 500124, NSE: DRREDDY, NYSE: RDY, NSEIFSC: DRREDDY, hereafter referred to as “Dr. Reddy’s”), Emcure Pharmaceuticals Limited (hereafter referred to as “Emcure”), Sun Pharmaceutical Industries Limited (Reuters: SUN.BO, Bloomberg: SUNP IN, NSE: SUNPHARMA, BSE: 524715, “Sun Pharma” and includes its subsidiaries and/or associate companies), and Torrent Pharmaceuticals Limited (“Torrent”, BSE: 500420, NSE: TORNTPHARM), announced today that the five companies will collaborate for the clinical trial of the investigational oral anti-viral drug Molnupiravir for the treatment of mild COVID-19 in an outpatient setting in India. Between March and April this year, these five pharma companies had individually entered into a non-exclusive voluntary licensing agreement with Merck Sharpe Dohme (MSD) to manufacture and supply Molnupiravir to India and over 100 low and middle-income countries (LMICs). The five pharma companies have entered into a collaboration agreement, wherein the parties will jointly sponsor, supervise and monitor the clinical trial in India. As per the directive of the Subject Expert Committee (SEC) of the Central Drugs Standard Control Organization, Dr. Reddy’s will conduct the clinical trial using its product, and the other four pharma companies will be required to demonstrate equivalence of their product to the product used by Dr. -

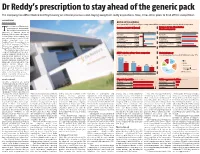

Dr Reddy's Prescription to Stay Ahead of the Generic Pack

Dr Reddy’s prescription to stay ahead of the generic pack The company has differentiated itself by focusing on internal processes and staying away from costly acquisitions. Now, it has other plans to fend off the competition B DASARATH REDDY Hyderabad, 8 August BATTLE OF THE GENERICS As the patent cliff in the US levels off, generic drug makers will face increasing pressure to develop other kinds of products he revenues of Hyderabad- Revenues in 2011-12 (Actual) Revenue for top-three Indian based generic drug maker, Pharma companies T Dr Reddy's Laboratories, is expected to surpass those of ~ crore Revenue Net profit ~ crore 2012-13 2013-14* Ranbaxy Laboratories, the largest Ranbaxy 9,977 Ranbaxy 11,309 Indian generic drug company, and Laboratories* -2,900 Laboratories 12,615 now a subsidiary of Japan’s Daiichi Dr Reddy's 9,674 Dr Reddy's 11,286 Sankyo, sometime next year. Laboratories** 1,426 Laboratories 12,663 Barclays Equity Research projects 8,006 9,694 Dr Reddy’s revenues for FY14 at Sun Pharmaceutical Sun Pharmaceutical 2,587 11,472 ~12,663 crore, slightly higher than Industries** Industries Ranbaxy’s (at ~12,615 crore). *Calendar year 2011, **FY ended March 2012 *Estimates This would be big news for any company battling it out in a chal- ANDA* pipeline of top-three companies Global pharmacy lenging industry. However, the Approved Pending Share of consolidated revenues for Dr Reddy's in the year ‘11-12 generic-drug business is more than just that. It’s a fiercely com- 241 petitive business, driven by vol- umes and characterised by con- 148 148 stantly falling prices and, 101 therefore, steep margins.