No Safe Harbor

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UPDATED 09.20.12 WNET Amgradday CPB Fact Sheet Nat'l

Contact: Donna Williams WNET New York Public Media 212-560-8030; [email protected] American Graduate Day Web site: www.americangraduate.org/grad-day American Graduate Day Fact Sheet Program Title: American Graduate Day Airdate: Saturday, September 22, 2012 from 1:00-8:00 pm ET on public television Program description: American Graduate Day Presented by WNET and Public Radio Exchange (PRX ), American Graduate Day is a multi-platform event featuring a live television broadcast, radio playlist with premiere documentaries, and participation from more than 20 national partner organizations, celebrities and athletes to spotlight solutions to the nation’s dropout crisis in which one in four students do not finish high school. Viewers and listeners will be encouraged to become an “American Graduate Champion” by offering their time, donating resources, connecting with the organizations on social media or learning more about the crisis. With special guests including Michael Powell, representing America’s Promise Alliance , and PBS NewsHour senior correspondent Ray Suarez, the national television broadcast will air live on public television stations from the Tisch WNET Studios at Lincoln Center from 1:00 to 8:00 p.m. EST on Sept. 22 (check local listings). Participating public television stations around the country will take the live feed and have an opportunity to add local content to support the national broadcast. American Graduate Day highlights community partners, educators and youth, who help keep at-risk students in school, across the nation. Each community partner profiled will provide viewers with information on how to become involved with American Graduate and the featured organizations. -

THE NATIONAL ACADEMY of TELEVISION ARTS & SCIENCES ANNOUNCES NOMINATIONS for the 44Th ANNUAL DAYTIME EMMY® AWARDS

THE NATIONAL ACADEMY OF TELEVISION ARTS & SCIENCES ANNOUNCES NOMINATIONS FOR THE 44th ANNUAL DAYTIME EMMY® AWARDS Daytime Emmy Awards to be held on Sunday, April 30th Daytime Creative Arts Emmy® Awards Gala on Friday, April 28th New York – March 22nd, 2017 – The National Academy of Television Arts & Sciences (NATAS) today announced the nominees for the 44th Annual Daytime Emmy® Awards. The awards ceremony will be held at the Pasadena Civic Auditorium on Sunday, April 30th, 2017. The Daytime Creative Arts Emmy Awards will also be held at the Pasadena Civic Auditorium on Friday, April 28th, 2017. The 44th Annual Daytime Emmy Award Nominations were revealed today on the Emmy Award-winning show, “The Talk,” on CBS. “The National Academy of Television Arts & Sciences is excited to be presenting the 44th Annual Daytime Emmy Awards in the historic Pasadena Civic Auditorium,” said Bob Mauro, President, NATAS. “With an outstanding roster of nominees, we are looking forward to an extraordinary celebration honoring the craft and talent that represent the best of Daytime television.” “After receiving a record number of submissions, we are thrilled by this talented and gifted list of nominees that will be honored at this year’s Daytime Emmy Awards,” said David Michaels, SVP, Daytime Emmy Awards. “I am very excited that Michael Levitt is with us as Executive Producer, and that David Parks and I will be serving as Executive Producers as well. With the added grandeur of the Pasadena Civic Auditorium, it will be a spectacular gala that celebrates everything we love about Daytime television!” The Daytime Emmy Awards recognize outstanding achievement in all fields of daytime television production and are presented to individuals and programs broadcast from 2:00 a.m.-6:00 p.m. -

Rebecca Jarvis, AB ‘03

T H E U N I V E R S I T Y O F C H I C AG O | T h e C o l l e g e CLASS DAY 2 0 1 9 J U N E 14 PRESENTED BY: Rebecca Jarvis, AB ‘03 Hello class of 2019. Congratulations! I have good news and bad news. The bad news is that I’m not here to pay off your student loans. The good news is that I’m confident at least one of you out there today, will be able to make good on that class gift in the not so distant future. Thank you, Dean Boyer and Dean Ellison for the invitation to speak today. Thank you students for having me here to share in your class day celebrations! It is such an honor to be here with all of you. I graduated from the University of Chicago in 2003 with a degree in law, letters & society and economics. This campus is where i had some of the greatest debates of my life. Where my own assumptions and views were challenged daily. Where I learned how not what to think – truly one of the greatest gifts of a UChicago education. It’s also where I met my husband and made lifelong friends. But 16 years ago, sitting where you are, I still had so many questions. I was free! I was going to do big things. But how exactly would I do those big things? So I come here today with five hopefully valuable lessons, some more hard won than others, that I’ve learned on my post-UChicago journey. -

T O P S T O R I E S O F 2 0

TOP STORIES OF 2014 Politics was practically purged from the nightly news agenda in 2014. Never have midterm elections been treated with such disdain. And never have federal domestic policy debates made such little news. Not a single White House nor Capitol Hill correspondent qualified for the Top 20 ranking of reporters. The TOP TWENTY STORIES OF 2014 Economy logged record lows too, a positive contrary indicator. mins Total ABC CBS NBC What made news instead? Led by Istanbul-based correspondent Winter weather 515 161 172 182 Holly Williams, CBS turned to the crises in Syria and Iraq Ebola outbreak in west Africa 496 136 173 186 (401 min vs NBC 252, ABC 167) and to Ukraine. CBS had its Ukraine divided: Crimea, fighting 392 68 187 138 busiest year of International coverage since 1990. Ebola in MH370 missing in Indian Ocean 306 91 101 114 west Africa should have been an international story too—but only Police: killing in Ferguson Mo 284 69 109 107 9% had a foreign dateline, so it became a domestic scare instead. Iraq civil war intensifies 272 46 137 89 Transportation had its heaviest year on record, as star-crossed Israel-Palestinian conflict: Gaza 234 51 93 90 Malaysian Airlines lost jetliners over the Indian Ocean and in Sochi Winter Olympic Games 219 60 39 121 Ukraine. NBC’s Tom Costello and ABC’s David Kerley led Islamic State declared by ISIS 208 49 89 71 coverage. Safety woes at General Motors were CBS’ specialty. Wild forest fires in western states 156 51 41 64 ABC, under new anchor David Muir, continued to downplay the Syria civil war continues 150 14 92 43 year’s top stories—not only international and political news, but Afghanistan war: US pulls out 144 39 53 51 also protests against police use of deadly force and the young MH017 shot down over Ukraine 131 40 48 43 refugees seeking asylum at the Mexican border. -

45Th Annual Daytime Emmy Award Nominations Were Revealed Today on the Emmy Award-Winning Show, the Talk, on CBS

P A G E 1 6 THE NATIONAL ACADEMY OF TELEVISION ARTS & SCIENCES ANNOUNCES NOMINATIONS FOR THE 45th ANNUAL DAYTIME EMMY® AWARDS Mario Lopez & Sheryl Underwood to Host Daytime Emmy Awards to be held on Sunday, April 29 Daytime Creative Arts Emmy® Awards Gala on Friday, April 27 Both Events to Take Place at the Pasadena Civic Auditorium in Southern California New York – March 21, 2018 – The National Academy of Television Arts & Sciences (NATAS) today announced the nominees for the 45th Annual Daytime Emmy® Awards. The ceremony will be held at the Pasadena Civic Auditorium on Sunday, April 29, 2018 hosted by Mario Lopez, host and star of the Emmy award-winning syndicated entertainment news show, Extra, and Sheryl Underwood, one of the hosts of the Emmy award-winning, CBS Daytime program, The Talk. The Daytime Creative Arts Emmy Awards will also be held at the Pasadena Civic Auditorium on Friday, April 27, 2018. The 45th Annual Daytime Emmy Award Nominations were revealed today on the Emmy Award-winning show, The Talk, on CBS. “The National Academy of Television Arts & Sciences is excited to be presenting the 45th Annual Daytime Emmy Awards, in the historic Pasadena Civic Auditorium,” said Chuck Dages, Chairman, NATAS. “With an outstanding roster of nominees and two wonderful hosts in Mario Lopez and Sheryl Underwood, we are looking forward to a great event honoring the best that Daytime television delivers everyday to its devoted audience.” “The record-breaking number of entries and the incredible level of talent and craft reflected in this year’s nominees gives us all ample reasons to celebrate,” said David Michaels, SVP, and Executive Producer, Daytime Emmy Awards. -

For August 1, 2010, CBS

Page 1 26 of 1000 DOCUMENTS CBS News Transcripts August 1, 2010 Sunday SHOW: CBS EVENING NEWS, SUNDAY EDITION 6:00 PM EST For August 1, 2010, CBS BYLINE: Russ Mitchell, Don Teague, Sharyl Attkisson, Seth Doane, Elaine Quijano GUESTS: Richard Haass SECTION: NEWS; International LENGTH: 2451 words HIGHLIGHT: On day 104 of the Gulf oil spill, news that a key step to seal the well could begin Tuesday as evidence mounts that B.P. used too many chemical dispersants to clean up the Gulf. President Obama may not be welcome on the campaign trail this fall as Democratic candidates fight to win their seats. Worries of drug violence in Mexico could spill over the border to the U.S. as National Guard`s troops get set to beef up border security. RUSS MITCHELL, CBS NEWS ANCHOR: Tonight on day 104 of the Gulf oil spill, news that a key step to seal the well could begin Tuesday as evidence mounts that B.P. used too many chemical dispersants to clean up the Gulf. I`m Russ Mitchell. Also tonight, campaign concerns. Why President Obama may not be welcome on the campaign trail this fall as Democratic candidates fight to win their seats. Border patrol, worries of drug violence in Mexico could spill over the border to the U.S. as National Guard`s troops get set to beef up border security. And just married, an inside account of the wedding yesterday of Chelsea Clinton and Marc Mezvinsky. And good evening. It is shaping up to be a very important week in the Gulf oil spill. -

Rebecca Jarvis

SM 633 Transcript EPISODE 633 [INTRODUCTION] [0:00:35.3] FT: Welcome to So Money everyone. I’m your host, Farnosh Torabi. Happy Monday. Excited to announce that this week we are doing a podcast crossover with No Limits, with Rebecca Jarvis. Have you heard of this amazing new podcast? You should subscribe. Rebecca Jarvis is a friend. She's also the senior business economics and technology correspondent for ABC News and on this podcast, the No Limits Podcast, she interviews female visionaries and entrepreneurs from cosmetics queen; Bobby Brown, to the Grammy award- winning musician; Jewel, and they talk all about their hard-earned lessons, their climb to success, their challenges with wealth. On today show, Rebecca stops by to talk about her favorite interviews so far. We also discussed intrapreneurship and her predictions about the economy, the markets as somebody who covers all of these stuff very closely. I was very curious to hear her take. Tomorrow you can head over to her podcast, No Limits, and hear her interview with me. I have to say on that podcast she asked questions that were a bit difficult to answer and I think I ended up revealing a lot. In fact, when it was over, I went back and begged the producer to edit parts of it and I don't think they did. There you go. That's not a teaser for you to run over to No Limits and hear what I had to say about love and marriage. I go there. Don't miss her show. -

Wes Moore to Host “American Graduate Day 2014

Wes Moore to Host “American Graduate Day 2014 Live from Tisch WNET Studios at Lincoln Center in NYC, airing September 27 on WXXI-TV Day-long Multiplatform Event Celebrates the “Stories of Champions” -- Individuals and Organizations Committed to Improving Outcomes for Youth and Raising Graduation Rates Special Guests Include Tony Bennett, Juju Chang, Bianna Golodryga, Ingrid Michaelson, Gen. Colin Powell & Alma Powell, The Raise Up Project, Sesame Street’s Elmo, Hari Sreenivasan, Trenton Public Schools Marching Band, Lauren Wanko, Brian & Jane Williams, Allison Williams, Doug Williams Local Broadcast to Showcase Hillside Work-Scholarship Connection, the Rochester City School District’s Universal PreK Program, Special Olympics, Homework Hotline & Rochester Dial-A-Teachers Efforts to Address the Needs of At-Risk Kids (Rochester, NY) September 24, 2014 – American Graduate Day 2014 returns this fall for its third consecutive year. Wes Moore, best-selling author and U.S. Army veteran, will host the all-day broadcast which premieres Saturday, September 27 from 11 a.m. to 6 p.m. on WXXI-TV and City 12. Broadcast and streamed live from the Tisch WNET Studios at Lincoln Center in New York City, the annual multiplatform event is part of the public media initiative, American Graduate: Let’s Make It Happen, helping communities bolster graduation rates through the power and reach of local public media stations. Featuring seven hours of national and local programming, live interviews and performances, American Graduate Day 2014 will celebrate the exceptional work of individuals and groups across the country who are American Graduate Champions: those helping local youth stay on track to college and career successes. -

48 Annual Daytime Emmy Awards NOMINATIONS

a 48th Annual Daytime Emmy Awards NOMINATIONS – June 25th Please read below and check your entries for the correct spelling, title, and to make sure nobody who is eligible is missing. This list marks everyone who is officially a Daytime Emmy nominee in these categories and is the list we will use to verify statue orders in the event of a win. To make changes to this list, please read below carefully for the instructions: Please send an email to Daytime Administration at [email protected] with the subject line “Nominee Corrections and Additions – June 25th” and list the following information in the body of the email: Category Show Title Entrant’s Name Entrant’s Title # of Episodes in 2020 (if a Series) Job Description (if an off-list title)** **All off-list titles, or individuals with less than the required minimum percentage of episodes, are subject to approval by the Awards Committee. All changes made prior to the ceremony on June 25th will be gratis for this year. We accept changes for $150 per change for 30 days after the ceremony. Changes beyond 30 days after the ceremony will not be accepted under any circumstances. Deadlines are established by the ceremony date in which that category is rewarded. This list will be updated with accepted changes once a week on Fridays at 5pm ET! OUTSTANDING DRAMA SERIES The Bold and the Beautiful CBS Bradley P. Bell, Executive Producer Edward J. Scott, Supervising Producer Casey Kasprzyk, Supervising Producer Cynthia J. Popp, Producer Mark Pinciotti, Producer Ann Willmott, Producer Days of Our Lives -

THE NATIONAL ACADEMY of TELEVISION ARTS & SCIENCES ANNOUNCES WINNERS of the 45Th ANNUAL DAYTIME EMMY® AWARDS

THE NATIONAL ACADEMY OF TELEVISION ARTS & SCIENCES ANNOUNCES WINNERS OF THE 45th ANNUAL DAYTIME EMMY® AWARDS Susan Seaforth Hayes and Bill Hayes Honored with the Lifetime Achievement Award Los Angeles, CA – April 29, 2018 – The National Academy of Television Arts & Sciences (NATAS) tonight announced the winners of the 45th Annual Daytime Emmy® Awards at a grand gala held at the Pasadena Civic Auditorium in Pasadena, Southern California. “What a fantastic evening to be celebrating Daytime television in the magnificent Pasadena Civic Auditorium,” said Chuck Dages, Chairman, NATAS. “The National Academy is excited to be honoring the men and women who make Daytime television one of the staples of the entertainment industry.” The evening’s show was hosted by the charming and talented Mario Lopez (EXTRA) and Sheryl Underwood (The Talk), and included many star-studded presenters such as Marie & David Osmond, Jane Pauley (CBS Sunday Morning), Loretta Swit and Jamie Farr, Tom Bergeron (Dancing with the Stars), Peter Marshall, Larry King (Larry King Now), Chris Harrison (Who Wants to be a Millionaire/The Bachelor), Nancy O’Dell and Kevin Frazier (ET), Valerie Bertinelli (Valerie’s Home Cooking), Julie Chen, Eve, Sara Gilbert (The Talk), Adrienne Houghton, Tamera Mowry-Housley, Loni Love, and Jeannie Mai (The Real), Gaby Natale (Super Latina), Mark Steines, Debbie Matanopoulis (Home and Family), A.J. Gibson, Viveca A. Fox, Martha Byrne and Elizabeth Hubbard, and Gloria Allred, plus Brandon McMillan (Lucky Dog), Kellie Pickler and Ben Aaron (Pickler & Ben). Also presenting were cast members from the four daytime soaps, including Deidre Hall, Suzanne Rogers, Sal Stowers and Greg Vaughan (Days of Our Lives), Carolyn Hennesy, Finola Hughes, Michelle Stafford, Chris Van Etten and Laura 1 Wright (General Hospital), Katherine Kelly Lang, Heather Tom and Rena Sofer (The Bold & the Beautiful), and Sharon Case and Kristoff St. -

43Rd Annual Daytime Emmy Award Nominations Were Revealed Today on the Emmy-Winning Show, “The Talk,” on CBS

1 THE NATIONAL ACADEMY OF TELEVISION ARTS & SCIENCES ANNOUNCES The 43rd ANNUAL DAYTIME EMMY® AWARD NOMINATIONS Daytime Emmy Awards To be held at the Westin Bonaventure Hotel and Suites on May 1st Daytime Creative Arts Emmy® Awards Gala on April 29th Individual Achievement in Animation Honorees Announced New York – March 24th, 2016 – The National Academy of Television Arts & Sciences (NATAS) today announced the nominees for the 43rd Annual Daytime Emmy® Awards. The awards ceremony will be held at the Westin Bonaventure Hotel and Suites on Sunday, May 1st. The Daytime Creative Arts Emmy Awards will also be held at the Bonaventure on Friday, April 29th, 2016. The 43rd Annual Daytime Emmy Award Nominations were revealed today on the Emmy-winning show, “The Talk,” on CBS. “After last year’s critically successful Daytime telecast, it is with great disappointment that The National Academy of Television Arts & Sciences (NATAS) announces that there will not be a broadcast of the 43rd Annual Daytime Emmy ® Awards,” said Bob Mauro, President. “After months of negotiations to find show sponsorship, the NATAS Executive Board has decided that the current climate for awards shows prohibits the possibility of a telecast this year. With that said, we will be putting on a world-class awards celebration honoring the best and brightest of Daytime television and look forward to an exciting show. All efforts regarding returning the annual gala to television in 2017 are underway.” “We are especially grateful for our passionate Daytime fans and are looking forward to producing a grand gala that honors the talents and artistries of all the professionals that represent Daytime television,” said David Michaels, SVP, Daytime Emmy Awards. -

2020 the Dropout

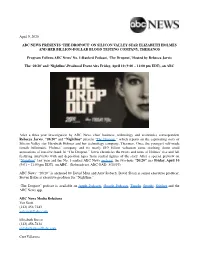

April 9, 2020 ABC NEWS PRESENTS ‘THE DROPOUT’ ON SILICON VALLEY STAR ELIZABETH HOLMES AND HER BILLION-DOLLAR BLOOD TESTING COMPANY, THERANOS Program Follows ABC News’ No. 1-Ranked Podcast, ‘The Dropout,’ Hosted by Rebecca Jarvis The ‘20/20’ and ‘Nightline’-Produced Event Airs Friday, April 10 (9:00 – 11:00 pm EDT), on ABC After a three-year investigation by ABC News chief business, technology and economics correspondent Rebecca Jarvis, “20/20” and “Nightline” present “The Dropout,” which reports on the captivating story of Silicon Valley star Elizabeth Holmes and her technology company, Theranos. Once the youngest self-made female billionaire, Holmes’ company and its nearly $10 billion valuation came crashing down amid accusations of massive fraud. In “The Dropout,” Jarvis chronicles the twists and turns of Holmes’ rise and fall featuring interviews with and deposition tapes from central figures of the story. After a special preview on “Nightline” last year and the No. 1-ranked ABC News podcast, the two-hour “20/20” airs Friday, April 10 (9:01 – 11:00 pm EDT), on ABC. (Rebroadcast. ABC OAD: 3/15/19) ABC News’ “20/20” is anchored by David Muir and Amy Robach. David Sloan is senior executive producer. Steven Baker is executive producer for “Nightline.” “The Dropout” podcast is available on Apple Podcasts, Google Podcasts, TuneIn, Spotify, Stitcher and the ABC News app. ABC News Media Relations Van Scott (212) 456-7243 [email protected] Elizabeth Russo (212) 456-7414 [email protected] Curt Villarosa (212) 456-3742 [email protected] For more information follow ABC News PR on Facebook, Twitter and Instagram.