The Specific Plan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Our Location & Our People

Ourour locationStrength & our people is Community Profile Inland Southern Moreno California Valley Moreno Valley is the fourth largest city in the Inland Empire and our future is soaring! Community Profile Moreno Valley is a progressive city with a bright future. While maintaining its friendly small town attitude, the 50-square-mile community boasts big city amenities including contemporary retail destinations and neighborhood shopping centers, plus a multitude ...superb of options for entertainment, dining, cultural, and recreational experiences and an array of housing options. “quality The City is dedicated to fostering new business and well-managed growth to create a superb quality of life for residents and visitors to enjoy. of life...” Population Moreno Valley’s youthful population totals 203,266 and is projected to exceed 215 thousand by 2019. Solid growth has propelled Moreno Valley to its position as the second largest city in Riverside County, fourth largest in the Inland Empire. POPULATION GROWTH 672,464 643,002 247,736 260,103 203,266 215,504 104,650 109,081 2014 2019 2014 2019 2014 2019 2014 2019 Total Population Within 3 miles Within 5 miles Within 10 Miles Growth Citywide of MV Mall of MV Mall of MV Mall SOURCE: Nielsen, updated April 2014 2 Moreno Valley is the fourth largest city in the Inland Empire and our future is soaring! Market Culture Households by Income Number of households Citywide Within 3 miles Within 5 miles Within 10 Miles ...superb of MV Mall of MV Mall of MV Mall Below $15,000 - $34,999 18,038 11,631 23,885 -

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

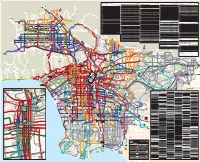

Metro Bus and Metro Rail System

Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Approximate frequency in minutes Metro Bus Lines East/West Local Service in other areas Weekdays Saturdays Sundays North/South Local Service in other areas Weekdays Saturdays Sundays Limited Stop Service Weekdays Saturdays Sundays Special Service Weekdays Saturdays Sundays Approximate frequency in minutes Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Line Route Name Peaks Day Eve Day Eve Day Eve Weekdays Saturdays Sundays 102 Walnut Park-Florence-East Jefferson Bl- 200 Alvarado St 5-8 11 12-30 10 12-30 12 12-30 302 Sunset Bl Limited 6-20—————— 603 Rampart Bl-Hoover St-Allesandro St- Local Service To/From Downtown LA 29-4038-4531-4545454545 10-12123020-303020-3030 Exposition Bl-Coliseum St 201 Silverlake Bl-Atwater-Glendale 40 40 40 60 60a 60 60a 305 Crosstown Bus:UCLA/Westwood- Colorado St Line Route Name Peaks Day Eve Day Eve Day Eve 3045-60————— NEWHALL 105 202 Imperial/Wilmington Station Limited 605 SANTA CLARITA 2 Sunset Bl 3-8 9-10 15-30 12-14 15-30 15-25 20-30 Vernon Av-La Cienega Bl 15-18 18-20 20-60 15 20-60 20 40-60 Willowbrook-Compton-Wilmington 30-60 — 60* — 60* — —60* Grande Vista Av-Boyle Heights- 5 10 15-20 30a 30 30a 30 30a PRINCESSA 4 Santa Monica Bl 7-14 8-14 15-18 12-18 12-15 15-30 15 108 Marina del Rey-Slauson Av-Pico Rivera 4-8 15 18-60 14-17 18-60 15-20 25-60 204 Vermont Av 6-10 10-15 20-30 15-20 15-30 12-15 15-30 312 La Brea -

Brea (Los Angeles), California Oil, Oranges & Opportunities

BUSINESS CARD DIE AREA 225 West Washington Street Indianapolis, IN 46204 (317) 636-1600 simon.com Information as of 5/1/16 Simon is a global leader in retail real estate ownership, management and development and an S&P 100 company (Simon Property Group, NYSE:SPG). BREA (LOS ANGELES), CALIFORNIA OIL, ORANGES & OPPORTUNITIES Brea Mall® is located in the heart of North Orange County, California, a few miles from California State University, Fullerton and their approximately 40,000 students and staff. — Brea and its surrounding communities are home to major corporations including American Suzuki Motor Corporation, Raytheon, Avery Dennison, Beckman Coulter and St. Jude Hospital. — The city’s Art in Public Places has integrated public art with private development. This nationally recognized collection features over 140 sculptures throughout the city including in Brea Mall. — The new master-planned communities of La Floresta and Blackstone, both in the city of Brea and less than four miles from Brea Mall, have added over 2,100 new luxury housing units to the area. — Brea City Hall and Chamber of Commerce offices are adjacent to the mall, located across the parking lot from Nordstrom and JCPenney. — One of the earliest communities in Orange County, Brea was incorporated in 1917 as the city of oil, oranges and opportunity. SOCAL STYLE Brea Mall has long served as a strategic fashion- focused shopping destination for the communities of North Orange County. The center continues in this tradition with a newly renovated property encompassing world-class shopping and dining. BY THE NUMBERS Anchored by Five Department Stores Nordstrom, Macy’s Women’s, Macy’s Men’s & Furniture Gallery, JCPenney Square Footage Brea Mall spans 1,319,000 square feet and attracts millions of visitors annually. -

The Role of Anchor Tenant in Driving Traffic in a Shopping Mall: the Case of Nakumatt Exit from Three Shopping Malls in Nairobi

JOURNAL OF LANGUAGE, TECHNOLOGY & ENTREPRENEURSHIP IN AFRICA Vol. 10 No. 1 MAY 2019 ________________________________________________________________________ THE ROLE OF ANCHOR TENANT IN DRIVING TRAFFIC IN A SHOPPING MALL: THE CASE OF NAKUMATT EXIT FROM THREE SHOPPING MALLS IN NAIROBI Peter N. Kiriri United States international University – Africa Email: [email protected] Abstract The current study investigates the role of an anchor tenant in driving traffic in a shopping mall. As the main tenant in a shopping mall, anchor tenants are expected to attract both human and vehicular traffic into a shopping mall. The traffic to the anchor tenant is expected to spill over to the non- anchor tenants and thus benefit them. This expectation is sometimes not met especially when an anchor tenant is posting sub-optimal performance or when they exit the mall. The background of this study was based on the malls in Nairobi who had Nakumatt Supermarkets chain as the anchor tenant. Nakumatt was the largest chain of supermarket with about 64 outlets in East Africa at its highest level at the beginning of 2017. However, due to a myriad of management challenges, the chain was forced to close most of its stores to a low of about 5 operational stores in mid-2018. As a result, and based on the findings, this affected the shopping malls as traffic reduced by almost 50% in some malls. The effects were felt in terms of reduced business activities in the mall, reduced occupancy levels, lower rental rates and general decline of mall financial performance. It is recommended that shopping malls should consider having more than one anchor tenant to mitigate against the effects of sub-optimal performance or exit of the anchor tenant. -

Pirates Theaters 010308

The Pirates Who Don't Do Anything - A VeggieTales Movie - - - In Theaters January 11th Please note: This list is current as of January 3, 2008 and is subject to change. Additional theaters are being added over the next few days, so be sure to check back later for an updated list. To arrange for group ticket sales, please call 1-888-863-8564. Thanks for your support and we'll see you at the movies! Theater Address City ST Zip Code Sunridge Spectrum Cinemas 400-2555 32nd Street NE Calgary AB(CAN) T1Y 7X3 Scotiabank Theatre Chinook (formerly Paramoun 6455 Macleod Trail S.W. Calgary AB(CAN) T2H 0K4 Empire Studio 16 Country Hills 388 Country Hills Blvd., N.E. Calgary AB(CAN) T3K 5J6 North Edmonton Cinemas 14231 137th Avenue NW Edmonton AB(CAN) T5L 5E8 Clareview Clareview Town Centre Edmonton AB(CAN) T5Y 2W8 South Edmonton Common Cinemas 1525-99th Street NW Edmonton AB(CAN) T6N 1K5 Lyric 11801 100th St. Grande Prairie AB(CAN) T8V 3Y2 Galaxy Cinemas Lethbridge 501 1st. Ave. S.W. Lethbridge AB(CAN) T1J 4L9 Uptown 4922-49th Street Red Deer AB(CAN) T4N 1V3 Parkland 7 Cinemas 130 Century Crossing Spruce Grove AB(CAN) T7X 0C8 Dimond Center 9 Cinemas 800 Dimond Boulevard Anchorage AK 99515 Goldstream Stadium 16 1855 Airport Road Fairbanks AK 99701 Grand 14 820 Colonial Promenade Parkway Alabaster AL 35007 Cinemagic Indoor 1702 South Jefferson Street Athens AL 35611 Wynnsong 16-Auburn 2111 East University Drive Auburn AL 36831 Trussville Stadium 16 Colonial Promenade Shopping Center Birmingham AL 35235 Lee Branch 15 801 Doug Baker Blvd. -

2004 1St Round Applicant List TCAC # Project Name Address City County

2004 1st Round Applicant List Low Federal $ State $ Geographic Total Income TCAC # Project Name Address City County Zip requested Requested Set-aside Type Area Units Units Owner Name CA-2004- Nonprofit Homeless 004 Rainbow Apartments 643 South San Pedro Street Los Angeles Los Angeles 90014 $937,147 $0 Apportionment Special Needs Los Angeles 89 87 Rainbow Apartments, LP CA-2004- J Street, Between 14th and 005 Lillian Place 15th Avenues San Diego San Diego 92101 $1,143,622 $0 Nonprofit Large Family San Diego 74 59 Lillian Place, L.P. CA-2004- 26th & Santa Monica 2601 & 2615 Santa Monica Community Corporation of 006 Family Housing Boulevard Santa Monica Los Angeles 90404 $792,734 $0 Nonprofit Large Family Los Angeles 44 43 Santa Monica CA-2004- 007 Hercules Senior Housing 102 Civic Drive Hercules Contra Costa 94547 $771,389 $0 Nonprofit Seniors East Bay 52 51 Eden Housing, In.c Norhteast corner of Church CA-2004- Road and Washington 008 Earlimart Village Avenue Earlimart Tulare 93219 $524,920 $1,944,148 Rural Large Family Central 44 43 Self-Help Enterprises CA-2004- 009 Del Rey Village 10563 E. Jefferson Del Rey Fresno 93616 $508,033 $1,881,607 Rural / RHS 514 Large Family Central 48 47 Self Help Enterprises CA-2004- 1424 Broadway & 1512 Community Corporation of 010 1424 Broadway Apartments 15th Street Santa Monica Los Angeles 90404 $786,801 $0 Nonprofit Large Family Los Angeles 41 40 Santa Monica Austin Street, Alhambra CA-2004- Court, and Belmont Street, Housing Authority of Kern 011 Casas del Valle South of First Avenue Delano Kern 93216 $354,200 $0 Small Development Large Family Central 20 20 County CA-2004- Morrill Road and Lenay Willow Pointe Apartment 012 Willow Point Apartments Way Riverbank Stanislaus 95367 $146,380 $553,065 Rural / RHS 515 Seniors Central 25 24 of Riverbank, LP CA-2004- Talmadge Senior Village Ken-Tal Senior Partners, 013 Apartments 5252 El Cajon Boulevard San Diego San Diego 92115 $1,296,283 $0 Nonprofit Seniors San Diego 91 90 L.P. -

Burbank Community Transit Needs Study

I I I B U R B A N K I Community Transit Needs Study I MILESTONE REPORT 1 I Identification of Unmet Transit Needs I .1 I I Prepared for I City of Burbank I I I ·I Prepared by Barton-Aschman Associates ·1 Myra L. Frank and Associates I I J I I I I I I .I I I I I I Prepared for City of Burbank I Prepared by I Bartal-AaJD:iil Associates I Myra L. Frank am Associates I I>eaiut>er, 1984 I I I I I I I I 1. INTroDUCTIOO 1 I 2. EXISTIOO AND Pro.JEX::l'ED CX)Nl)ITIONS 5 A. Geographic Setting 6 B. Land Uses 6 I c. Deroographic Characteristics 12 D. Employment Trends 15 I E. Transportation Facilities and Services 17 1. Highways 18 2. Transit 20 I 3. Plans and Programs 30 3. IDENTIFICATION OF UNMET TRANSIT NEEDS 34 I A. Analysis of Census of Population Data 34 1. Household Characteristics 35 I 2. Ccmnuting Patterns 50 B. Analysis of Service 65 I 1. RID 65 2. Burbank Transportation Service 73 I c. Surveys of Households and Transit Riders 74 1. Survey of Burbank Households 74 I 2. Survey of Burbank Transportation Services Riders 100 3. Survey of R'ID Riders 106 I D. Interviews with Other Agencies 108 E. Key Conclusions 111 I 1. Existing Conditions 112 2. Projected Coooitions 114 I I I I I I I 1. RID Bus Routes in Burbank 22 I 2. Trip Origins of Burbank Airport's Boarding Passengers 29 3. -

Life After Death – Coping with the Aftermath of a Co-Tenancy Failure

Life After Death – Coping with the Aftermath of a Co-Tenancy Failure Author: Sunita Mahant, Senior Director, Legal Affairs, Ivanhoé Cambridge Inc.1 Susan. D. Rosen, Partner, Gowling WLG (Canada) LLP Co-authors: Katherine Garretto and Daniel Minuk2 Today, we hear phases such as “retail apocalypse”, “the end of the mall”, “death of brick and mortar retail”. These are just a few of the phrases that have been used to describe the current state of the retail real estate market. There is no denying that the global commercial real estate market has undergone a significant seismic shift over the past few years, and the forces that have precipitated those changes, are ongoing and continuing to change the way in which commercial retail real estate is developed, renovated, repurposed, rejuvenated and effectively leased. The aforementioned seismic shift in the retail landscape is also having a significant impact on how existing co-tenancy clauses are being interpreted, the remedies that are practically available when these clauses are violated and the manner in which new co- tenancy clauses should be written in view of the e-commerce retail revolution. Historically, a tenant of a certain size and/or brand recognition (the “Benefitting Tenant”), would require a co-tenancy clause be inserted into its lease to ensure that it would have the benefit of being located in a shopping center that had existing leases with one or more large department stores, grocery stores, supermarkets and/or named brand retailers, all with the expectation that these types of anchor or major tenants would drive traffic to the shopping centre generally, and to the Benefitting Tenant specifically. -

ORLANDO Vacation Guide & Planning Kit

ORLANDO Vacation Guide & Planning Kit Orlando, Florida Overview Table of Contents Orlando, the undisputed “Vacation Capital of the World,” boasts Orlando, Florida Overview 1 beautiful weather year round, world-class theme parks, thrilling water Getting To And Around Orlando 2 parks, unique attractions, lively dinner theaters, outdoor recreation, Orlando Theme Parks 3 luxurious health spas, fine dining, trendy nightclubs, great shopping Walt Disney World Resort 3 opportunities, championship golf courses and much more. The seat of Universal Orlando® Resort 4 Orange County, Florida, Orlando boasts a population of approximately SeaWorld® Orlando 4 228,000 – making it the sixth largest city in Florida. Easily accessible Orlando Attractions 5 via Interstate 4 and the Florida Turnpike, Orlando is also home to the Orlando Dining 8 Orlando International Airport – the 10th busiest airport in the United Orlando Live Entertainment 8 States and the 20th busiest in the world. Orlando Shopping 9 Orlando Golf 10 Experience the magic of Walt Disney World® Resort – Discover the Orlando Annual Events 11 enchanted lands of Disney’s Magic Kingdom® Park, blast off into the Orlando Travel Tips 13 future at Epcot®, journey through the fascinating history of Hollywood movies at Disney’s Hollywood Studios™ and take a fun-filled safari expedition at Disney’s Animal Kingdom® Theme Park. Don’t miss the thrilling rides at the two amazing theme parks of Universal Orlando® Resort – Universal Studios® Florida and Universal’s Islands of Adventure®, as well as the up-close animal encounters of SeaWorld® Orlando. Cool off at one of Orlando’s state-of-the-art water parks such as Aquatica, Wet ‘n Wild® Water Park, Disney’s Blizzard Beach or Disney’s Typhoon Lagoon. -

2018 EARLY DECEMBER 2018 Text & Photos by Mike Ritto [email protected] Fullerton Photo Quiz NEW in TOWN

OBSERVER 40 TH B-D AY page 20 COMMUNITY Fullerton bsCeALErNDAvR Peage 1r 3-15 O EAR FULLERTON’S ONLY INDEPENDENT NEWS • Est.1978 (printed on 20% recycled paper) • Y 40 #20 • EARLY DECEMBER 2018 Submissions: [email protected] • Contact: (714) 525-6402 • Read Online at : www.fullertonobserver.com Vinny De La Torre Honored by Fullerton and France by Ed Paul The City of Fullerton proudly recognized long-time resident, Ventura “Vinny” De La Torre, for his heroic service to his country over 70 years ago. The presentation was made at the November 19 Council meeting and Vinny was given a standing ovation by all present. Vinny De La Torre was also recognized by receiving France’s Legion of Honor, the coun - try’s highest honor, on November 11, 2018, in recognition for his service with Gen. George Patton’s Third Army during WWII. Vinny was in more than 200 days of contin - uous combat, liberating many French cities and in 1945, was part of the division that fought at the Battle of the Bulge and liberated two concentration camps, Buchenwald and Ebensee. He was almost 21 years old at that time. Like many of the WW II generation, Vinny kept much of this story to himself. But in recent years his family, mostly his grandchil - dren, slowly obtained bits and pieces of his service. They conducted some research and provided it to the French Consulate General who, after reviewing it for over a year, made the presentation to Vinny on November 11 at the National Cemetery in West Los Angeles. -

The Walking Company Holdings, Inc

Case 18-10474 Doc 1 Filed 03/06/18 Page 1 of 36 United States Bankruptcy Court for the: DISTRICT OF DELAWARE Case number ~rrk~ow~~ Chapter 11 ❑ Check if this an amended filing Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy 4/16 If more space is needed, attach a separate sheet to this form. On the top of any additional pages, write the debtor's name and case number (if known). For more information, a separate document, Instructions for Bankruptcy Forms for Non-Individuals, is available. 1. Debtor's name The Walking Company Holdings, Inc. 2. All other names debtor used in the last 8 years Include any assumed names, trade names and doing business as names 3. Debtor's federal Employer Identification 52-1868665 Number (EIN) 4. Debtor's address Principal place of business Mailing address, if different from principal place of business 25 W. Anapamu Santa Barbara, CA 93101 Number, Street, City, State &ZIP Code P.O. Box, Number, Street, City, State &ZIP Code Santa Barbara Location of principal assets, if different from principal County place of business Number, Street, City, State &ZIP Code 5. Debtor's website (URL) 6. Type of debfor ~~~~~~~~~~~~~(including Limited Liability Company (LLC) and Limited Liability Partnership (LLP)) ❑ Partnership (excluding LLP) ❑ Other. Specify: Official Form 201 Voluntary Petition for Non-Individuals Filing for Bankruptcy page 1 Case 18-10474 Doc 1 Filed 03/06/18 Page 2 of 36 Debtor Case number (if known) The Walking Company Holdings, II1C. _._ Name — 7. Describe debtor's business A.