Planning Gain Supplement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Imy Wyatt Corner [email protected]

Imy Wyatt Corner [email protected] Directing SHOW THEATRE/ VENUE WRITER LENGTH OF RUN YEAR Humane Pleasance Theatre * Polly Creed 3 weeks (postponed) 2021 Gaslight Playground Theatre * Patrick Hamilton 3 weeks 2019 Baby, What Blessings Theatre503 * Siofra Dromgoole 1 week 2019 Baby, What Blessings Edinburgh Fringe Siofra Dromgoole 2 weeks 2019 Baby, What Blessings Bunker Theatre Siofra Dromgoole 1 night 2019 Baby, What Blessings Brewery Arts Centre, Siofra Dromgoole 1 night 2019 Kendal Q&A Southwark Playhouse Jess Moore 1 night 2019 From There to Here Old Red Lion Theatre Amanda Lane 2 nights 2019 We, The People Etcetera Theatre * Eleanor Ross 1 night 2019 Walk Swiftly & With Purpose North Wall Arts Centre Siofra Dromgoole 2 nights 2019 Walk Swiftly & With Purpose Theatre503 * Siofra Dromgoole 1 week 2018 Walk Swiftly & With Purpose Edinburgh Fringe Siofra Dromgoole 2 weeks 2018 NSA The Mono Box Charles Entsie 1 night 2018 Our Lemon Sherbet Sky Arcola Theatre Eleanor Ross 1 night 2018 Flux Leyton Technical/ Plymouth Fringe Naomi Soneye-Thomas 4 nights 2018 Happy Yet? International Theatre, Katie Berglof 4 nights 2018 Frankfurt * Happy Yet? Courtyard Theatre Katie Berglof 1 week 2017 Happy Yet? Edinburgh Fringe Katie Berglof 2 weeks 2016 Assistant Directing SHOW THEATRE/ VENUE DIRECTOR LENGTH OF RUN YEAR NoF*cksgiven Vault Festival Michael Oakley 1 week 2019 R&D Felt Little Angel/ The North Wall * Pip Williams 10 days 2020/21 Humane Pleasance Theatre Polly Creed 1 week 2019 Baby, What Blessings Brewery Arts, Kendal Siofra Dromgoole 1 week 2019 *= professional Other Work & Training Bristol Old Vic Theatre School, MA Drama Directing (2020 – ongoing) Everywoman & Other Confessions,*Producer. -

Who We Are Week Runs, One Offs & Matinees

Valid until 31.12.2018 265 CAMDEN HIGH STREET - NW1 7BU - LONDON 0207 482 4857 - [email protected] 1996 Guinness Ingenuity Award for Pub Theatre WHO WE ARE As a home is not just a house, a Theatre is not just a space. HISTORY & LOCATION Since its foundation in 1986, the Etcetera Theatre has become one of the milestone venues of the London fringe circuit. The theatre is ideally located right on Camden High Street, one of the busiest tourist and shopping areas in London only seventy-five metres away from Camden Town tube station. The Etcetera works to establish a healthy and sustainable relationship with all incoming companies and we are happy to provide support and advice throughout the production process. We have been established here for twenty nine years and are happy to pass on useful contacts and advice to incoming companies. THE TEAM Since 2014, the Etcetera has not only become a family business but an artistic one at that! Run by Maud (actress) & her brother Pierre (musician), their experience of being self represented artists and their passion for the live arts is definitely one of the main assets of this new management as they can fully understand the ins and outs of putting on a show. WEEK RUNS, ONE OFFS & MATINEES These prices include the use of our PA system and lights as well as our furniture and microphones. WEEK RUNS Include 6 performances from TUE – SUN and are available on two different slots. EARLY SLOT: 7PM – 8PM (6.30PM – 8PM for 90min shows) LATER SLOT: 9PM – 10PM LATER SLOT EXTENDED: 9PM – 10.30PM NB: on Sundays all shows start and finish an hour earlier. -

Amy De Bhrún

AMY DE BHRÚN NolanMuldoonAgency HEIGHT 5’ 8” HAIR Blonde EYES Blue/Green NATIONALITY Irish TRAINING Laine Theatre Arts Company FILM & TELEVISION Production Part Director Company Penny Dreadful Prostitute J.A. Bayona Showtime Casualty Alana Steve Hughes BBC Treasure The Stag Rachel John Butler Entertainment Vikings Ingigerd Johan Renck History Channel All is By My Side Pheobe John Ridley Matador The Crown and the Dragon Ellen Barethon (L) Anne K Black Arrowstorm The South Bank Show Tess Durberville Matt Cain ITV Bigga Than Ben Girl in Bookshop Suzie Halewood Annex Films Lovelorn Doctor Becky Preston Tread Softly Dance Invasion Sarah Collins (L) Liam Beale Chaos Weekly Films Girl in Motion Girl (L) Phil Bowman Doublecrossed We Few Head Operator Lee Stringer Lucas Films THEATRE Play Part Director Venue/Company Till Death We Part One Woman Show Helena Browne Theatre Upstairs Theatre Row, New Female of the Species One Woman Show Helena Browne York Life A One Woman Show Grainne Helena Browne Solas Productions The Money Man Sophie Helena Browne Rumor Mill, LA NolanMuldoonAgency / +353 1 288 1537 / www.nolanmuldoonagency.com Facing the Space Emma Helena Browne Mayfield Café Life Grainne Helena Browne Roundhouse, London 2am Jono Helena Browne Etcetera Theatre 3 Women for the Moon La Helena Browne Bewley’s Café Theatre A Short Swim in the Air Jessie Helena Browne Pleasance Theatre The Maids Claire Helena Browne Etcetera Theatre The Donahue Sisters Annie Helena Browne Etcetera Theatre The House of Bernarda Alba Magdalena Mhairi Grealis Pentameters -

Theatre6 Present

THEATRE6 PRESENT ADAPTED BY STEPHANIE DALE DIRECTED BY KATE Mc GREGOR MUSIC BY MARIA HAÏK ESCUDERO ADAPTED BY STEPHANIE DALE WELCOME FROM THEATRE6’S Persuasion debuted at the Playground ARTISTIC DIRECTOR, KATE MCGREGOR Theatre on Tuesday 17 April 2018. Welcome to Theatre6’s production of Jane Austen’s final novel Persuasion. This LATE SUMMER 1814 brand new adaptation by Stephanie Dale celebrates 200 years since the novel’s TO SPRING 1815. publication. Opening at the Playground Theatre in London, this production will tour Anne and Wentworth were young across the country, including two performances at one of the novel’s most famous and in love. Persuaded by her locations – Lyme Regis. prosperous and prominent family to refuse Wentworth’s proposal, Jane Austen loved the sea, music, nature and her family. She wrote during the Anne lost the great love of her life. Napoleonic Wars and saw two of her brothers become Captains in the Navy. Bath Our play, as in Austen’s original was a place she spent a great deal of time. Her own life was not free of tragedy story, takes place eight years after and heartbreak. What is remarkable about Jane’s writing is not only her detailed these events. understanding of her characters, plots, locations and the impact of society and history on people but also her ability to write about the human spirit. In a time where The performance lasts for approximately women had very little agency and power in society, she created female protagonists 2 hours including an interval. with aspirations, who longed for adventure, who were able to decipher their feelings and analyse their place in a changing world. -

Women in Theatre 2006 Survey

WOMEN IN THEATRE 2006 SURVEY Sphinx Theatre Company 2006 copyright. No part of this survey may be reproduced without permission WOMEN IN THEATRE 2006 SURVEY Sphinx Theatre Company copyright 2006. No part of this survey may be reproduced without permission The comparative employment of men and women as actors, directors and writers in the UK theatre industry, and how new writing features in venues’ programming Period 1: 16 – 29 January 2006 (inclusive) Section A: Actors, Writers, Directors and New Writing. For the two weeks covered in Period 1, there were 140 productions staged at 112 venues. Writers Of the 140 productions there were: 98 written by men 70% 13 written by women 9% 22 mixed collaboration 16% (7 unknown) 5% New Writing 48 of the 140 plays were new writing (34%). Of the 48 new plays: 30 written by men 62% 8 written by women 17% 10 mixed collaboration 21% The greatest volume of new writing was shown at Fringe venues, with 31% of its programme for the specified time period featuring new writing. New Adaptations/ New Translations 9 of the 140 plays were new adaptations/ new translations (6%). Of the 9 new adaptations/ new translations: 5 written by men 0 written by women 4 mixed collaboration 2 WOMEN IN THEATRE 2006 SURVEY Sphinx Theatre Company copyright 2006. No part of this survey may be reproduced without permission Directors 97 male directors 69% 32 female directors 23% 6 mixed collaborations 4% (5 unknown) 4% Fringe theatres employed the most female directors (9 or 32% of Fringe directors were female), while subsidised west end venues employed the highest proportion of female directors (8 or 36% were female). -

Foxfinder by Dawn King Directed by Blanche Mcintyre

Press Information New Writing at the Finborough Theatre Season November 2011 to January 2012 Papatango Theatre Company in partnership with the Finborough Theatre present four world premieres The Papatango Playwriting Festival 2011 Foxfinder by Dawn King Directed by Blanche McIntyre. Designed by James Perkins. Lighting by Gary Bowman. Sound by George Dennis. Cast: Kirsty Besterman. Tom Byam Shaw. Becci Gemmell. Gyuri Sarossy. Papatango have teamed up with one of London's leading new writing venues, the Finborough Theatre to present the winning entries in the 2011 Papatango Playwriting Competition 2011, featuring this year's winning play Foxfinder by Dawn King which will play for a four week limited season from 29 November (Press Night: Thursday, 1 December 2011 at 8.30pm). “You, Foxfinder, must be clean in body and mind. Always remember that the smallest fault in your character could become a crack into which the beast may insinuate himself, like water awaiting the freeze that will smash the stone apart.” William Bloor, a Foxfinder, arrives at Sam and Judith Covey’s farm to investigate a suspected contamination. What follows will change the course of all their lives, forever. Foxfinder is a gripping, unsettling and darkly comic exploration of belief, desire and responsibility. Playwright Dawn King was one of ten writers from across the UK chosen for the BBC Writersroom 10 scheme, a prestigious mentoring and support programme. Through this she is developing a new play with West Yorkshire Playhouse. She is also currently writing My One and Only, an afternoon play for BBC radio 4. Her episode of horror series The Man in Black will broadcast on BBC radio 4 Extra later this year. -

Scenes on the Sand – Cast Biographies 1

SCENES ON THE SAND – CAST BIOGRAPHIES MON 4TH AUG SIREN by David Elms SIREN: Emma Sidi Emma Sidi is an actor and comic based in South London. She is a former member of the Cambridge Footlights, performing in the International Tour Show 2013. Recent theatre credits include Sweet Meat (Tristan Bates Theatre), EXP (Etcetera Theatre) and Three Sisters (ADC Theatre). Film includes Gregor, written and directed by Mickey Down and Konrad Kay. She also recently directed the short play The Walls Are Thin (Tristan Bates Theatre). SAILOR: Barney McElholm Barney is a LAMDA graduate and co-Artistic Director of Soggy Arts Productions. Theatre credits include: Tomorrow and Middle Child (West Yorkshire Playhouse), Romeo & Juliet, (Young Shakespeare Company; National Tour), The Long Trick and Bucket Club (Nightingale Theatre), Wind in the Willows (Cambridge Touring Theatre; Gilded Balloon), Uprooted, Full House (National Tour). Television and Film: Oliver Ball, The Lurker (Soggy Arts), Pete, The Rambling Men (Soggy Arts). TREASURE by Alexander Owen JAMES: Ian Targett Theatre credits include: The Breadwinner (Orange Tree), Bows and Arrows (Royal Court), Why Me? (Novello), The Kiss of Life and A View of Kabul (Bush), Romeo and Juliet (Lyric Hammersmith), Eurydice (BAC), Burning Point (Tricycle), The Woman in Black (PW Productions), A Small Family Business (West Yorkshire Playhouse). Tours include An Inspector Calls, The Winslow Boy, Arsenic and Old Lace, Dracula. TV work includes: Marks, A Taste of Honey, Over the Rainbow, Mind Games, Babylon, The Last Detective, Ghostboat, Midsomer Murders, Monroe, Eastenders, Emmerdale, Trust Me, Casualty, Forever Green, Doctors, Films include: The Fool, A Dangerous Man, and The Lover MOIRA: Sasha Waddell Sasha has just returned from touring the Far East with Yes Prime Minister. -

Introduction to Ecovenue Ecovenue Is a Signifi Cant Theatre-Specifi C Environmental Project Being Run by the Theatres Trust

Introduction to Ecovenue Ecovenue is a signifi cant theatre-specifi c environmental project being run by The Theatres Trust. It aims to improve the environmental performance of forty-eight London theatres and raise awareness of how to make theatres greener. Ecovenue is promoting the sustainability of theatres and the reduction of carbon emissions through the provision of free theatre-specifi c, environmental advice. The project started in 2009 and runs until 2012. Forty-eight venues each undergo an Environmental Audit, and receive a Display Energy Certifi cate (DEC) and Advisory Report. They track their energy use through SMEasure. Each venue receives a second DEC a year after their fi rst to measure progress. Ecovenue includes a ‘DEC Pool’ of performing arts venues across the UK that have obtained DECs. The DEC Pool helps us to evaluate the project and share best practice and information, establish meaningful benchmarks, and provide a better understanding of energy use of theatres. Any theatre can join the DEC Pool. The Trust’s Theatres Magazine provides quarterly reports on the participants and the work of the Ecovenue project. The Theatres Trust Ecovenue project receives fi nancial support from the European Regional Development Fund. Participating Theatres Albany Theatre Etcetera Theatre Old Vic Arcola Finborough Theatre Orange Tree Theatre Arts Theatre Gate Theatre Pleasance Islington artsdepot Greenwich & Lewisham Young Polka Theatre Brockley Jack People’s Theatre Putney Arts Theatre Bush Theatre Greenwich Playhouse Questors Camden People’s -

Download Publication

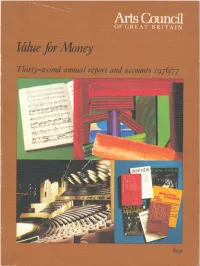

Arts Council OF GREAT BRITAI N Value fir Money ;ES;VHH AND IN,'-ORMATiON L13PARY DO NOT REMOVE FROM OM THIS ROOM Thirty-second annual report and accounts year ended 31 March 1977 Thirty-second Annual Report and Accounts 197 7 ISBN 07287 0143 X Published by the Arts Council of Great Britai n 105 Piccadilly, London W 1 V OA U Designed by Paul Sharp Printed in England by Shenval Pres s The montage on the cover illustrates the work of the Art s Council's specialist departments : Music : Page of vocal score of Sir William Walton 's Troilus and Cressida, showing revisions made by the composer for the 1976 production by the Royal Opera Art : Foy Nissen's Bombay by Howard Hodgkin Drama : The Olivier auditorium at the National Theatr e Literature : Some books and magazines published or subsidise d by the Council Contents Chairman 's Introduction 5 Secretary-General's Report 7 Regional Activities 15 Drama 1 6 Drama 1948-1977 (a personal commen t by N. V. Linklater) 20 Music 23 Visual Arts 26 Literature 30 Touring 3 1 Community Arts 32 Festivals 34 Housing the Arts 34 Training 35 Research and Information 36 Marketing 36 Scotland 37 Wales 41 Membership of Council and Staff 44 Council, Committees and Panels 45 Annual Accounts 53 The objects for which the Arts Council of Great Britai n is established by Royal Charter are : 1 To develop and .Improve the knowledge, understanding and practice of the arts ; 2 To increase the accessibility of the arts to the publi c throughout Great Britain ; and 3 To co-operate with government departments, local authorities and other bodies to achieve these objects. -

Theatre Archive Project Archive

University of Sheffield Library. Special Collections and Archives Ref: MS 349 Title: Theatre Archive Project: Archive Scope: A collection of interviews on CD-ROM with those visiting or working in the theatre between 1945 and 1968, created by the Theatre Archive Project (British Library and De Montfort University); also copies of some correspondence Dates: 1958-2008 Level: Fonds Extent: 3 boxes Name of creator: Theatre Archive Project Administrative / biographical history: Beginning in 2003, the Theatre Archive Project is a major reinvestigation of British theatre history between 1945 and 1968, from the perspectives of both the members of the audience and those working in the theatre at the time. It encompasses both the post-war theatre archives held by the British Library, and also their post-1968 scripts collection. In addition, many oral history interviews have been carried out with visitors and theatre practitioners. The Project began at the University of Sheffield and later transferred to De Montfort University. The archive at Sheffield contains 170 CD-ROMs of interviews with theatre workers and audience members, including Glenda Jackson, Brian Rix, Susan Engel and Michael Frayn. There is also a collection of copies of correspondence between Gyorgy Lengyel and Michel and Suria Saint Denis, and between Gyorgy Lengyel and Sir John Gielgud, dating from 1958 to 1999. Related collections: De Montfort University Library Source: Deposited by Theatre Archive Project staff, 2005-2009 System of arrangement: As received Subjects: Theatre Conditions of access: Available to all researchers, by appointment Restrictions: None Copyright: According to document Finding aids: Listed MS 349 THEATRE ARCHIVE PROJECT: ARCHIVE 349/1 Interviews on CD-ROM (Alphabetical listing) Interviewee Abstract Interviewer Date of Interview Disc no. -

Amy Clare Tasker Theatre CV

AMY CLARE TASKER THEATRE MAKER & CREATIVE PRODUCER London 2013 - present. co-director of Pinecone Performance Lab San Francisco 2008 - 2013. arLsLc director of Inkblot Ensemble +44 (0)7462 550062 @AmyClareTasker [email protected] www.amyclaretasker.com | www.pineconeperformance.com THEATRE MAKING DIRECTING & DEVISING WITH MY OWN COMPANY PINECONE PERFORMANCE LAB ChanGe of Art | creave producer, singer-songwriter a mulE-arts collecEve, fostering community and HOT (Helen of Troy) | writer & performer conversaEon through creaEve intervenEons. a patriarchy-smashing solo show with Greek mythology, www.changeofart.org.uk power ballads, and a 90s pop culture twist 2017: Change of Art FesEval, in partnership with HOPE not The Cockpit (London) February 2020 hate & Amnesty InternaEonal UK. artsdepot residency (London) Sept 2019 2018: Hear Here, an audio installaEon commissioned by Upstart Theatre, at DARE FesEval, Shoreditch Town Hall. Home Is Where… | director, creator, producer verbaEm theatre & oral history project, devised by the The Helen Project - later became HOT (Helen of Troy) company from interviews with Cross Culture Kids. director, co-writer, producer CLF Art Cafe, Bussey Building R&D (London) 2019 by Megan Cohen & Amy Clare Tasker Theatre Delicatessen R&D (London) June 2017 Face to Face FesEval at LOST Theatre (London) 2014 RichMix R&D (London) September 2016 DIVAfest (San Francisco) 2013 Camden People’s Theatre scratch (London) January 2016 Dirty Laundry inspired by Lorca’s Yerma CREATIVE PRODUCING director & dramaturg The Collaboratory -

International Theatre Programs Collection O-018

http://oac.cdlib.org/findaid/ark:/13030/c8b2810r No online items Inventory of the International Theatre Programs Collection O-018 Liz Phillips University of California, Davis General Library, Dept. of Special Collections 2017 1st Floor, Shields Library, University of California 100 North West Quad Davis, CA 95616-5292 [email protected] URL: https://www.library.ucdavis.edu/special-collections/ Inventory of the International O-018 1 Theatre Programs Collection O-018 Language of Material: English Contributing Institution: University of California, Davis General Library, Dept. of Special Collections Title: International Theatre Programs Collection Creator: University of California, Davis. Library Identifier/Call Number: O-018 Physical Description: 19.1 linear feet Date (inclusive): 1884-2011 Abstract: Mostly 19th and early 20th century British programs, including a sizable group from Dublin's Abbey Theatre. Researchers should contact Special Collections to request collections, as many are stored offsite. Scope and Contents The collection includes mostly 19th and early 20th century British programs, including a sizable group from Dublin's Abbey Theatre. Access Collection is open for research. Processing Information Liz Phillips converted this collection list to EAD. Preferred Citation [Identification of item], International Theatre Program Collection, O-018, Department of Special Collections, General Library, University of California, Davis. Publication Rights All applicable copyrights for the collection are protected under chapter 17 of the U.S. Copyright Code. Requests for permission to publish or quote from manuscripts must be submitted in writing to the Head of Special Collections. Permission for publication is given on behalf of the Regents of the University of California as the owner of the physical items.