UAE Telecoms Sector

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Capital Markets Day 2020 Presentation

Etisalat Group February 19st, 2020 Capital Jumeirah Saadiyat, Abu Dhabi Markets 2020 Day DISCLAIMER Emirates Telecommunications Group Company PJSC and its subsidiaries (“Etisalat Group” or the “Company”) have prepared this presentation (“Presentation”) in good faith, however, no warranty or representation, express or implied is made as to the adequacy, correctness, completeness or accuracy of any numbers, statements, opinions or estimates, or other information contained in this Presentation. The information contained in this Presentation is an overview, and should not be considered as the giving of investment advice by the Company or any of its shareholders, directors, officers, agents, employees or advisers. Each party to whom this Presentation is made available must make its own independent assessment of the Company after making such investigations and taking such advice as may be deemed necessary. Where this Presentation contains summaries of documents, those summaries should not be relied upon and the actual documentation must be referred to for its full effect. This Presentation includes certain “forward-looking statements”. Such forward looking statements are not guarantees of future performance and involve risks of uncertainties. Actual results may differ materially from these forward looking statements. Business Overview Saleh Al-Abdooli Chief Executive Officer Etisalat Group Etisalat Group Serkan Okandan Financial Results Chief Financial Officer Etisalat Group Etisalat Group Hatem Dowidar International Chief Executive Officer -

Modern City Tours • Cultural Experiences • World-Class

TOURIST GUIDE TO THE UAE MODERN CITY TOURS • CULTURAL EXPERIENCES • WORLD-CLASS ATTRACTIONS • DESERT SAFARIS • & MORE ADVENTURES TO BE DISCOVERED INSIDE! A journey of relaxation, fun and excitement! Welcome to a place where people from all corners To make your stay as remarkable as you’ve wanted of the world converge – the United Arab Emirates it to be, we at Desert Adventures, the leading (UAE). destination management company in the region, have made the most of what the UAE has in store. Rich in cultural heritage and tradition, the UAE has Accordingly, we have put together some of the rapidly transformed its erstwhile empty desert choicest options that will certainly make every land into a sought-after holiday destination filled minute of your visit count. with exciting attractions and distinctive experiences. Browse through this guide and learn more about all the fun and excitement that you most definitely From well-appointed hotel accommodations and would not want to miss. Make the most of your trip thought-provoking sightseeing tours that by getting in touch with our local experts and showcase the UAE’s natural splendour and representatives. We will be more than happy to intriguing culture to fun-filled theme parks and assist you in making your stay truly memorable. In desert activities, bargain shopping and luxurious the meantime, keep turning the pages and grab an fine dining experiences – all these have made the experience of a lifetime! country a favourite and sought-after destination for both leisure and business travellers all year Here’s wishing you a unforgettable stay in our round. -

Lists of Current Accreditations for Operators (Networks)

Rich Communications Services Interoperability and Testing / Accreditation Lists of current accreditations for Operators (networks) Lists of current accreditations for Operators (networks) Accreditation List of services/service # Company name Network brand name Country Accreditation level Accreditation status type clusters UP-Framework, UP- Approved (valid until 1 Evolve Cellular Inc. Evolve Cellular USA Provisional Messaging, UP- Universal Profile 1.0 4.12.2018) EnrichedCalling China Mobile Communication UP-Framework, UP- Approved (valid until 2 China Mobile China Provisional Universal Profile 1.0 Co. Ltd. Messaging 25.02.2019) UP-Framework, UP- Universal Profile Approved (valid until 3 Vodafone Group Vodafone-Spain Spain Provisional Messaging, UP- Transition – Phase 1 20.12.2018) EnrichedCalling UP-Framework, UP- Universal Profile Approved (valid until 4 Vodafone Group Vodafone-Deutschland Germany Provisional Messaging, UP- Transition – Phase 1 20.12.2018) EnrichedCalling UP-Framework, UP- Vodafone Albania Sh. Universal Profile Approved (valid until 5 Vodafone Group Albania Provisional Messaging, UP- A Transition – Phase 1 20.12.2018) EnrichedCalling 29 January 2018 Rich Communications Services Interoperability and Testing / Accreditation Lists of current accreditations for Operators (networks) Accreditation List of services/service # Company name Network brand name Country Accreditation level Accreditation status type clusters UP-Framework, UP- Vodafone Czech Czech Universal Profile Approved (valid until 6 Vodafone Group Provisional -

Device-To-Device Communications in LTE-Advanced Network Junyi Feng

Device-to-Device Communications in LTE-Advanced Network Junyi Feng To cite this version: Junyi Feng. Device-to-Device Communications in LTE-Advanced Network. Networking and Internet Architecture [cs.NI]. Télécom Bretagne, Université de Bretagne-Sud, 2013. English. tel-00983507 HAL Id: tel-00983507 https://tel.archives-ouvertes.fr/tel-00983507 Submitted on 25 Apr 2014 HAL is a multi-disciplinary open access L’archive ouverte pluridisciplinaire HAL, est archive for the deposit and dissemination of sci- destinée au dépôt et à la diffusion de documents entific research documents, whether they are pub- scientifiques de niveau recherche, publiés ou non, lished or not. The documents may come from émanant des établissements d’enseignement et de teaching and research institutions in France or recherche français ou étrangers, des laboratoires abroad, or from public or private research centers. publics ou privés. N° d’ordre : 2013telb0296 Sous le sceau de l’Université européenne de Bretagne Télécom Bretagne En habilitation conjointe avec l’Université de Bretagne-Sud Ecole Doctorale – sicma Device-to-Device Communications in LTE-Advanced Network Thèse de Doctorat Mention : Sciences et Technologies de l’information et de la Communication Présentée par Junyi Feng Département : Signal et Communications Laboratoire : Labsticc Pôle: CACS Directeur de thèse : Samir Saoudi Soutenue le 19 décembre Jury : M. Charles Tatkeu, Chargé de recherche, HDR, IFSTTAR - Lille (Rapporteur) M. Jean-Pierre Cances, Professeur, ENSIL (Rapporteur) M. Jérôme LE Masson, Maître de Conférences, UBS (Examinateur) M. Ramesh Pyndiah, Professeur, Télécom Bretagne (Examinateur) M. Samir Saoudi, Professeur, Télécom Bretagne (Directeur de thèse) M. Thomas Derham, Docteur Ingénieur, Orange Labs Japan (Encadrant) Acknowledgements This PhD thesis is co-supervised by Doctor Thomas DERHAM fromOrangeLabs Tokyo and by Professor Samir SAOUDI from Telecom Bretagne. -

Infratil Limited and Vodafone New Zealand Limited

PUBLIC VERSION NOTICE SEEKING CLEARANCE FOR A BUSINESS ACQUISITION UNDER SECTION 66 OF THE COMMERCE ACT 1986 17 May 2019 The Registrar Competition Branch Commerce Commission PO Box 2351 Wellington New Zealand [email protected] Pursuant to section 66(1) of the Commerce Act 1986, notice is hereby given seeking clearance of a proposed business acquisition. BF\59029236\1 | Page 1 PUBLIC VERSION Pursuant to section 66(1) of the Commerce Act 1986, notice is hereby given seeking clearance of a proposed business acquisition (the transaction) in which: (a) Infratil Limited (Infratil) and/or any of its interconnected bodies corporate will acquire shares in a special purpose vehicle (SPV), such shareholding not to exceed 50%; and (b) the SPV and/or any of its interconnected bodies corporate will acquire up to 100% of the shares in Vodafone New Zealand Limited (Vodafone). EXECUTIVE SUMMARY AND INTRODUCTION 1. This proposed transaction will result in Infratil having an up to 50% interest in Vodafone, in addition to its existing 51% interest in Trustpower Limited (Trustpower). 2. Vodafone provides telecommunications services in New Zealand. 3. Trustpower has historically been primarily a retailer of electricity and gas. In recent years, Trustpower has repositioned itself as a multi-utility retailer. It now also sells fixed broadband and voice services in bundles with its electricity and gas products, with approximately 96,000 broadband connections. Trustpower also recently entered into an arrangement with Spark to offer wireless broadband and mobile services. If Vodafone and Trustpower merged, there would therefore be some limited aggregation in fixed line broadband and voice markets and potentially (in the future) the mobile phone services market. -

Cellular Internet of Things (C-Iot)

Release-13 Cellular IoT Deployments – November 2019 REGION COUNTRY OPERATOR NB-IoT LTE-M Africa 1 0 South Africa Vodacom 1 Asia & Pacific 19 10 Australia Telstra 1 1 Australia Vodafone Australia 1 China China Telecom 1 China China Unicom 1 China China Mobile 1 Hong Kong China Mobile (HK) 1 India Reliance Joi Infocomm 1 Indonesia Telkomsel 1 Indonesia XL Axiata 1 Japan KDDI (au) 1 Japan DOCOMO 1 Malaysia Maxis 1 New Zealand Spark 1 New Zealand Vodafone New Zealand 1 1 Singapore M1 1 Singapore Singtel 1 1 South Korea KT Corp 1 1 South Korea LG Plus 1 South Korea SK Telecom 1 Sri Lanka Dialog Axiata 1 1 Taiwan Asia Pacific Telecom (APT) 1 1 Taiwan Far EasTone 1 Vietnam Viettel 1 Eastern Europe 15 0 Croatia A1 Croatia 1 Croatia Hrvatski Telecom 1 Czech Republic Vodafone Czech Republic 1 Estonia Elisa 1 Estonia Telia Estonia 1 Hungary Magyar Telekom 1 Kazakhstan KaR-Tel (Beeline) 1 Poland Polkomtel 1 Poland T-Mobile Poland 1 Russia Beeline (Russia) 1 Russia MegaFon 1 Movile TeleSystems Russia (MTS) 1 Slovakia Slovak Telecom 1 Slovenia A1 Slovenia 1 Ukraine Lifecell 1 Latin America & Caribbean 2 3 Argentina Movistar (Argentina) 1 1 Brazil Vivo 1 1 Mexico AT&T Mexico 1 Middle East 5 1 Qatar Vodafone Qatar 1 United Arab Emirates Du 1 United Arab Emirates Etisalat 1 1 Turkey Turkcell 1 Turkey Vodafone Turkey 1 U.S. & Canada 3 4 Canada Bell Canada 1 Canada Telus 1 United States AT&T 1 1 United States T-Mobile US 1 United States Verizon 1 1 Western Europe 17 6 Austria T-Mobile 1 Belgium Orange 1 1 Belgium Proximus 1 Belgium Telenet 1 Denmark TDC -

Annual Report 2019 a World Without Limits

A WORLD WITHOUT LIMITS ANNUAL REPORT 2019 TABLE OF CONTENTS 01. Key Highlights of 2019 05 15. Saudi Arabia 49 02. Business Snapshot 07 16. Egypt 51 03. Chairman’s Statement 08 17. Morocco 53 04. Board of Directors 10 18. Pakistan 57 05. Etisalat’s Journey 14 19. Afghanistan 60 06. Group CEO’s Statement 16 14. E-Vision 61 07. Management Team 18 20. Etisalat Services Holding 62 08. Vision and Strategy 22 21. Human Capital 65 09. Key Events During 2019 29 22. Corporate Social Responsibility 69 10. Operational Highlights 30 23. Corporate Governance 73 11. Brand Highlights 34 24. Enterprise Risk Management 76 12. Etisalat Group’s Footprint 40 25. Financials 81 13. United Arab Emirates 43 26. Notice for General Assembly Meeting 170 3 KEY HIGHLIGHTS OF 2019 EBITDA NET PROFIT REVENUE (BILLION) (BILLION) (BILLION) 52.2 26.4 8.7 AED AED AED CAPEX AGGREGATE DIVIDEND PER (BILLION) SUBSCRIBERS (MILLION) SHARE 80 8.9 149 FILS AED ANNUAL REPORT 2019 4 5 ETISALAT GROUP BUSINESS SNAPSHOT Etisalat Group offers a range of communication services to consum- speed on its 5G standalone network, Etisalat enabled 5G networks ers, businesses, and government segments in multiple regions. Our across several key sites in the UAE. As part of Maroc Telecom’s inter- portfolio of products and services include mobile, fixed broadband, national development strategy and plan to consolidate the group’s TV, voice, carrier services, cloud and security, internet of things, mo- presence in Africa, Maroc Telecom completed the acquisition of Tigo bile money, and other value added services. -

The Facebooked Organisation a Critique of Corporate Social Media in New Zealand

The Facebooked Organisation A critique of corporate social media in New Zealand A thesis submitted to Auckland University of Technology in partial fulfilment of the requirements for the degree of Doctor of Philosophy By Sarah Gumbley i No one ever got broke by underestimating the intelligence of the American people. - PT Barnum ii Abstract The research illustrates that people on Facebook communicate with organizations as though the organisations are people too. Furthermore, organisations induce this behaviour through promotional materials that persuaded the follower to engage with them as friends. I began my research as it appeared that organisations hid potentially ruthless profit motives behind a smiling face of friendship on social media networks, particularly on Facebook, which I used daily. Facebook may be a relatively new technology, having been first developed only a decade ago, but it has dramatically changed the way the global society communicates. In New Zealand alone it is estimated half the population uses the tool1. Due to this, Facebook is surrounded by a kind of hysteria: in one form or another Facebook makes the news on a near-daily basis, from the celebrification of its founder, to panics over privacy. The dramatic impact Facebook has had in such a short period of time means many remain curious, uninformed and often fearful of how this tool will impact the future. In the last few years, Facebook has added functionality that now enables businesses to have a presence in this forum, which has made it possible for customers to interact with businesses in an entirely new way. This has resulted in hype in the business world, over the untapped potential of this new marketing tool. -

In-Building Telecommunication Network - Specification Manual

TRA UAE In-Building Telecommunication Network - Specification Manual Guidelines for FTTx in new Buildings V2.0 Released Issued by Telecommunication Regulatory Authority Dubai – United Arab Emirates Your Contact Person(s): Ms. Tahani Almulla Manager Infrastructure and Services Tel: + 97147774091 e-Mail: [email protected] @THEUAETRA, www.tra.gov.ae Table of Contents 1 Executive Summary ............................................................................................................................. 4 2 FTTx in new Buildings .......................................................................................................................... 6 2.1 Introduction ......................................................................................................................................... 6 2.2 Intention and Application .................................................................................................................. 7 2.3 Reference Architectur ....................................................................................................................... 8 2.4 Best Practice Approach ....................................................................................................................... 9 2.5 Securing Competition – The possibility of a further licensee ......................................................10 2.6 Licensees du and Etisalat ...................................................................................................................10 2.7 Common Master -

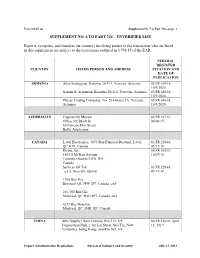

SUPPLEMENT NO. 6 to PART 744 – UNVERIFIED LIST Exports, Reexports, and Transfers

Unverified List Supplement No. 7 to Part 744—page 1 SUPPLEMENT NO. 6 TO PART 744 – UNVERIFIED LIST Exports, reexports, and transfers (in-country) involving parties to the transaction who are listed in this supplement are subject to the restrictions outlined in § 744.15 of the EAR. FEDERAL REGISTER COUNTRY LISTED PERSON AND ADDRESS CITATION AND DATE OF PUBLICATION ARMENIA Atlas Sanatgaran, Komitas 26/114, Yerevan, Armenia 85 FR 64014, 10/9/2020. Iranian & Armenian, Komitas 26/114, Yerevan, Armenia 85 FR 64014, 10/9/2020. Piricas Trading Company, No. 20 Heratsi 2A, Yerevan, 85 FR 64014, Armenia 10/9/2020. AZERBAIJAN Caspian Oil Montaj 82 FR 16732, Office 39, Block B 04/06/17. 30 Kaverochkin Street Baku, Azerbaijan CANADA Laval Electronics, 3073 Rue Edmond-Rostand, Laval, 83 FR 22844, QC H7P, Canada 05/17/18. Rizma, Inc. 80 FR 60532, 1403-8 McKee Avenue 10/07/15. Toronto, Ontario M2N 7E5 Canada Services GP Tek 83 FR 22844, a.k.a. Nouvelle Option 05/17/18. 1305 Rue Pise Brossard, QC J4W 2P7, Canada; and 203-760 Rue Gal Montreal, QC H4G 2P7, Canada; and 6271 Rue Beaulieu Montreal, QC, H4E 3E9, Canada CHINA Able Supply Chain Limited, Rm 511, 5/F, 84 FR 14610, April Corporation Park, 1 On Lai Street, Sha Tin, New 11, 2019. Territories, Hong Kong; and Rm 605, 6/F, Export Administration Regulations Bureau of Industry and Security July 12, 2021 Unverified List Supplement No. 7 to Part 744—page 2 Corporation Park, 1 On Lai Street, Sha Tin, New Territories, Hong Kong; and Unit C, 9/F, Winning House, No. -

Automatic Planning of 3G UMTS All-IP Release 4 Networks with Realistic Traffic

Automatic Planning of 3G UMTS All-IP Release 4 Networks with Realistic Traffic by Mohammad Reza Pasandideh A thesis submitted to The Faculty of Graduate and Postdoctoral Affairs in partial fulfillment of the requirements for the degree of Master of Applied Science in Electrical and Computer Engineering Ottawa-Carleton Institute for Electrical and Computer Engineering (OCIECE) Department of Systems and Computer Engineering Carleton University Ottawa, Ontario, Canada, K1S 5B6 Copyright 2011, Mohammad Reza Pasandideh Library and Archives Bibliotheque et 1*1 Canada Archives Canada Published Heritage Direction du Branch Patrimoine de I'edition 395 Wellington Street 395, rue Wellington Ottawa ON K1A 0N4 Ottawa ON K1A 0N4 Canada Canada Your file Votre ref6rence ISBN: 978-0-494-79548-4 Our file Notre reference ISBN: 978-0-494-79548-4 NOTICE: AVIS: The author has granted a non L'auteur a accorde une licence non exclusive exclusive license allowing Library and permettant a la Bibliotheque et Archives Archives Canada to reproduce, Canada de reproduire, publier, archiver, publish, archive, preserve, conserve, sauvegarder, conserver, transmettre au public communicate to the public by par telecommunication ou par I'lntemet, preter, telecommunication or on the Internet, distribuer et vendre des theses partout dans le loan, distribute and sell theses monde, a des fins commerciales ou autres, sur worldwide, for commercial or non support microforme, papier, electronique et/ou commercial purposes, in microform, autres formats. paper, electronic and/or any other formats. The author retains copyright L'auteur conserve la propriete du droit d'auteur ownership and moral rights in this et des droits moraux qui protege cette these. -

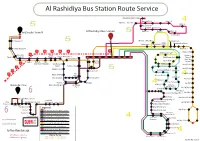

Al Rashidiya Bus Network

Al Rashidiya Bus Station Route Service Muhaisnah 2, Etisalat Academy Muhaisnah (1)-A 2 Mizhar 1, G 4 Muhaisnah 1, Intersection 1 Mizhar 1, F 1 5 Muhaisnah (1)-B 2 Al Mizhir 1, Arabian Center Gold Souq Bus Station 14 Al Rashidiya Bus Station 5 Mizhar 1, A 1 Mizhar 1, C 1 Mizhar 1, D 1 Al Mizhar Mall 1 Naif, Intersection 1 5 Muhaisnah 1, Etihad Mall 1 Khawaneej, Road 1 2 Mizhar 2 Khawaneej, Roundabout 1 Mushrif, Eppco 1 Mushrif, Park 1 Turno 1 Burj Nahar, Intersection 1 Khawaneej 1 1 M M M M M M Khawaneej, Park Mirdi, ETISALAT Tower 1 Union Metro M Airport Khawaneej Nakhal 1 2 Station A 2 Terminal 1 Emirates Metro Station 1 4 11A 44 F05 F03 F10 365 366 Mirdi, Private School 1 , Terminus Gulf & Safa Diaries 1 Rawabi Diary Rashidiya, Uptown Mirdif 1 Garhoud, Cargo ,Crossing 1 M Dnata 1 Street 38 Intersection 1 Village Gate Dubai Municipality Mirdi, Area 3 Amardi, Road 1 1 Garage 1 M Rashidiya, Village Al Warqa'a I 1 Mawakeb School 1 5 Amardi, Road 4 1 M Rashidiya, Park 1 Downtown Mirdi Gate 1 Al Warqa'a H 1 Awir, Etisalat 1 M Dubai Festival City Max 4 Garage Al Warqa'a Entrance 1 Al Warqa'a G 1 Inter Care Limited Umm Hani School 1 Awir, Palace 1 Al Warqa'a A 1 Al Warqa'a, Courtyard 1 Rebat Street 1 Rashidiya 2 4 Awir, CMC 1 Ghubaiba Bus Station Dubai Festival City, IKEA1 Umm Ramool Al Warqa'a C 1 Al Warqa'a, , Enoc 1 ETISALAT Tower 1 Awir, CMC Road 4 2 Al Warqa'a D 1 Al Warqa'a E 1 6 International City, Dragon Mart 1 Awir, Palace 2 Bits Pilani 2 Awir, Dewa Wells Unit 2 Al Fahidie Metro Station A1 Oud Metha Knowledge Village 1 2 Knowledge Village 2 2 Falcon BurJuman Metro Station A1 Metro Station 1 Police Stadium Awir, CMC Road 1 2 Intersection 1 Emirates Aviation University 2 Raa 1 Rolla Saeediya School 2 Dubai Mens College 1 2 Awir, Mosque 1 Karama 1 2 44 Al Rashidiya Bus Station To Al Ghubaiba Bst Dubai Mens College 2 2 6 Karama Ent.