P Ocket Guide

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download PDF (77.1

Index Abraham, K.S. 133 Beck, Ulrich 129 absorbing risk 133 behavioral anomalies 6, 84–9, 243–4 actuarial estimation 109–10 behavior-control functions 106 ad hoc Beijing Normal University 90, 189, assistance 196 235 compensation tool 45 Ben-Shahar, Omri 134 direct payment 40, 169, 207 Biggert-Waters Flood Insurance institutions 30 Reform Act of 2012 69, 152 relief 71, 97 Bruggeman, Véronique 95 adaptation 253 business interruption 104 and climate change 103, 164 adverse selection 5, 13, 47, 54, 66–8, California Earthquake Authority 55, 75, 81–2, 97, 99, 111, 127, 140, 142 162, 246 capacity (of insurers) 6–8, 11, 19, 30, AES v Steadfast 116–19 53, 63–6, 82–4, 89–91, 96, 113, agricultural insurance 122–3, 126, 136, 152, 161–2 173, government-subsidized 50 176, 179–80, 217, 222, 225, 227–8, pilot projects 49 242–3, 249–52 policies 49, 50 and reinsurance 199, 206–8, 215 Regulation on Agriculture Insurance capacity gap 82, 228, 242, 252 50, 94 capital markets 11, 53, 54, 59, 64–5, aircraft insurance 110 212, 217–8, 221, 226–40 all-hazard insurance policy 245 Caribbean Catastrophe Risk Insurance Alternative Risk Transfers (ARTs) 217, Facility 60 221, 236 catastrophe (cat) bonds 3, 113, 182, ambiguity of risk 112–13 212 217–40 see also uncertainty see also insurance-linked securities, American International Group (AIG) insurance securitization 1, 104 catastrophe derivatives 182, 221–2 “appetite” of insurers 84 catastrophe disasters 5, 8, 12–6, 72, 74, Arrow, Kenneth 35 92, 102, 155, 171–3, 255–6 asbestos claims 108–9 see also natural catastrophes assessment insurance 110 catastrophe fund 142, 210–12, 254 asset-backed securitization 237 catastrophe insurance 6, 8–11, 13–4, Association of British Insurers (ABI) 44, 73, 80, 89–99, 103, 105, 108, 148, 149 112–14, 121–8, 129–175, 208–9, authoritarian regime 7, 33 212–5, 216 availability crisis 52 affordability 63, 66, 69–70, 125, 127–8 174, 206, 250, 256 Baker, Tom 133, 134 demand 84–9, 92–3 Barry, D. -

Auto –Accidents - What Is “No-Fault” Insurance?

AUTO –ACCIDENTS - WHAT IS “NO-FAULT” INSURANCE? If you are injured in a car accident who pays your medical bills? Believe it or not, your medical insurance carrier does not have the primary responsibility to pay your medical bills for injuries sustained in an automobile accident - The applicable automobile insurance carrier does. But remember, if your injuries or above a certain threshold you can still sue the person who cause your injuries for money damages above what the applicable automobile insurance carrier provides. In New York State each automobile insurance policy must provide coverage known as Personal Injury Protection (“PIP”) and typically referred to a “No-Fault” insurance. Medical bills, some or all of the injured party’s lost wages and other expenses are paid from this portion of the policy, whether or not the injured party caused the accident. So if were in a car accident driving your own vehicle and you are injured as a result of another person's negligence, the no-fault portion of your automobile insurance policy will cover your medical bills to the extent that you have coverage. If your coverage runs out other insurance will kick in. The New York State Insurance Law, requires that all automobile insurance policies issued in this state contain a Personal Injury Protection (“PIP”) or “No-Fault” endorsement with a minimum of $50,000.00 in coverage. Generally speaking, this coverage extends to the driver and passengers in a covered vehicle, as well as to a pedestrian struck by the covered vehicle. The coverage “kicks in” regardless of fault in connection with an accident; under most circumstances, a covered individual will be afforded certain enumerated benefits regardless of that individual’s fault in connection with the happening of the accident. -

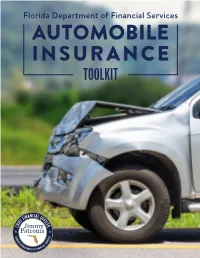

AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit

Florida Department of Financial Services AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or even the death of a loved one. There are a wide variety of insurance products available and choosing the correct type and amount of coverage can be a challenge. This toolkit provides information to assist you with insuring your automobile and tips for settling an automobile insurance claim. TABLE OF CONTENTS Click a title or page number to navigate to a section. 01 Coverages & Minimum Requirements - 4 Coverage Descriptions - 5 Insurance Requirements for Special Cases - 8 02 Underwriting Guidelines - 11 Underwriting Factors That Cannot Affect Your Ability to Purchase Insurance - 11 Underwriting Factors That Affect Your Insurance Policy Premium - 12 Other Factors Affecting Your Premiums - 13 Shopping for Auto Insurance - 13 03 Automobile Claims - 14 Actions to Take Before and After an Auto Accident - 14 Disputing Claim Settlements - 16 04 Shopping for Coverage Checklist - 17 01 Coverages & Minimum Requirements In Florida, vehicle owners may be required to The second type of auto insurance is outlined in the purchase two types of auto insurance. Florida Financial Responsibility Law. It requires drivers The first type of auto insurance is outlined in the who have caused accidents involving bodily injury/death Florida Motor Vehicle No-Fault Law (s. 627.736, Florida or received certain citations, to purchase bodily injury Statutes). It requires every person who registers a liability (BI) coverage with minimum limits of $10,000 vehicle in Florida to provide proof they have personal per person and $20,000 per accident, referred to as injury protection (PIP) and property damage liability split limits. -

What You Need to Know

What AutoAuto you InsuranceInsurance need to know A consumer information publication The Minnesota Department of Commerce has prepared this guide to help you better understand auto insurance. It gives you information on shopping for insurance, the different types of coverage, and a basic understanding of “no fault” coverage. The Minnesota Department of Commerce regulates insurance agents, agencies, adjusters, and companies operating in Minnesota. If they are licensed to do business in the State, they are responsible for adhering to the laws and rules that govern the industry. This guide does not list all of these regulations. If you have a question about your insurance, please contact the Department’s Consumer Response Team at 651-296-2488, or toll free 800-657-3602. Duplication of this guide is encouraged. Please feel free to copy this information and share it with others. Department of Commerce Auto Insurance can protect you from the financial costs of an accident or injury, provided you have the proper coverage. Yet many people are unclear about what their insurance policy cov- ers until it is too late. They may have difficulties settling a claim or face rate increases or termination of coverage. Auto Insurance I s ... Protection. Insurance is a way of transferring risk for a loss among a certain group of people. You, and others, pay premiums to an insurance company to be reimbursed if you have an acci- dent. The amount you can collect and under what circumstances are outlined in your policy. Required. Under most circumstances, a licensed vehicle in the state of Minnesota must have liability, personal injury protection, uninsured motorist, and underinsured motorist coverage. -

Pocket Guide to Lloyd's

Our Market Our Past Our Home Pocket Guide “For more than three Welcome to Lloyd’s centuries, the Lloyd’s Lloyd’s is the world’s leading market has been insurance and reinsurance sharing risk to protect marketplace. Through the collective intelligence and risk-sharing people and businesses, 03 inspiring them to expertise of the market’s underwriters and brokers, Lloyd’s Our Market create a braver world” helps to create a braver world. The Lloyd’s market provides the John Neal, CEO, Lloyd’s leadership and insight to anticipate and understand risk, and the knowledge to develop relevant, new and innovative forms of insurance for customers globally. And it promises a trusted, enduring partnership built on the confidence that Lloyd’s protects what matters most: helping people, businesses and communities to recover in times of need. Our Market: Lloyd’s in a day Most of the business written at Lloyd’s is still conducted face-to-face in the world- famous Underwriting Room at our London Every day, people, businesses and Lime Street headquarters. Brokers place communities in over 200 countries their clients’ risk with Lloyd’s specialist and territories rely on the Lloyd’s underwriters who evaluate, price and market to protect what matters most. accept the risks. On any given working day, ‘The Room’ welcomes more than 5,000 05 And every day, more than 50 leading people, sees more than £100m in premiums insurance companies, over 300 come into the market and sees more than Our Market registered brokers and a global network £49.9m paid out in claims – that’s more than of over 3,900 coverholder office £34,620 in claims per minute. -

Incentives and Barriers of the Cyber Insurance Market in Europe June 2012

Incentives and barriers of the cyber insurance market in Europe June 2012 Incentives and barriers of the cyber insurance market in Europe I Acknowledgements This Study was commissioned and managed by ENISA with specialist services provided by RAND Europe. ENISA would like to thank Mr. Neil Robinson for his professionalism and dedication to this project. In addition, ENISA wishes to acknowledge and thank Prof. Robin Bloomfield of City University of London, Mr. Andrea Renda of CEPS, Mr. Michael Mainelli of Z/Yen, Mrs. Simona Cavallini and Mr. Fabio Bisogni of Formit Foundation for their prompt support, valuable input and material provided for the compilation of this Study. II Incentives and barriers of the cyber insurance market in Europe About ENISA The European Network and Information Security Agency (ENISA) is a centre of network and information security expertise for the EU, its member states, the private sector and Europe’s citizens. ENISA works with these groups to develop advice and recommendations on good practice in information security. It assists EU member states in implementing relevant EU legislation and works to improve the resilience of Europe’s critical information infrastructure and networks. ENISA seeks to enhance existing expertise in EU member states by supporting the development of cross-border communities committed to improving network and information security throughout the EU. More information about ENISA and its work can be found at www.enisa.europa.eu Contact details For contacting ENISA or for general enquiries on this Study on cyber insurance market in Europe please contact Nicole Falessi and Dr. Konstantinos Moulinos and use the following details: Resilience and CIIP Program Technical Department Email: [email protected] Incentives and barriers of the cyber insurance market in Europe III Legal notice Notice must be taken that this publication represents the views and interpretations of the authors and editors, unless stated otherwise. -

The RAM Health Insurance Cooperative Is NOW Thriving

Health Insurance Cooperative The RAM Health Insurance Cooperative is NOW thriving – and growing – in 2020! The program offers RAM members: A 3% DISCOUNT OFF PREMIUM RATES FOR SMALL BUSINESSES IN THE SMALL GROUP MARKET (Groups of 1-50 employees) ACCESS TO EVERY SMALL GROUP PLAN OFFERED BY BCBSMA & ALMOST ALL SMALL GROUP PLANS OFFERED BY FALLON HEALTH DEFINED CONTRIBUTION OPTIONS TO ADDRESS THE NEEDS OF BOTH YOUR BUSINESS AND YOUR EMPLOYEES And for those members who choose a BCBSMA plan, the program also offers additional value-added benefits including: A WELLNESS PROGRAM WITH POTENTIAL EMPLOYEE INCENTIVES OF UP TO $300 AND AN OPPORTUNITY TO EARN 7.5% IN BACK END EMPLOYER INCENTIVES A FREE SUPPLEMENTAL HOSPITALIZATION POLICY FOR ALL SUBSCRIBERS, WHICH COVERS $750 FOR A HOSPITAL ADMISSION AND $150 EACH ADDITIONAL DAY UP TO 10 DAYS A FREE $10,000 LIFE INSURANCE POLICY FOR ALL SUBSCRIBERS Visit www.retailersma.org or call us at (617) 523-1900 to learn more! Health Insurance Cooperative Dear RAM Member, RAMHIC is a service of the Retailers Association of Massachusetts—the leading voice for more choice and fairer premiums for small businesses and their employees in the Massachusetts insurance market. RAMHIC is an important example of our efforts to deliver economic equality for Main Street. Since the adoption of universal healthcare in Massachusetts, small businesses have received disproportionate increases in their health insurance premiums compared to their large competitors and government programs. In response, RAM fought for the creation of small business group purchasing cooperatives designed to allow like-minded businesses to join together and negotiate with carriers for reduced premium rates based on the projected experience of the group. -

Lloyd's Policy Signing Office, Quoting the Lloyd's Policy Signing Office Number and Date Or Reference Shown in the Table

Lloyd’s Policy of the Syndicates whose definitive numbers We, Underwriting Members and proportions are shown in the Table attached hereto (hereinafter referred to as 'the Underwriters'), hereby agree, in consideration of the payment to Us by or on behalf of the Assured of the Premium specified in the Schedule, to insure against loss, including but not limited to associated expenses specified herein, if any, to the extent and in the manner provided in this Policy. The Underwriters hereby bind themselves severally and not jointly, each for his own part and not one for another, and therefore each of the Underwriters (and his Executors and Administrators) shall be liable only for his own share of his Syndicate's proportion of any such Loss and of any such Expenses. The identity of each of the Underwriters and the amount of his share may be ascertained by the Assured or the Assured's representative on application to Lloyd's Policy Signing Office, quoting the Lloyd's Policy Signing Office number and date or reference shown in the Table. If the Assured shall make any claim knowing the same to be false or fraudulent, as regards amount or otherwise, this Policy shall become void and all claim hereunder shall be forfeited. In Witness whereof the General Manager of Lloyd's Policy Signing Office has signed this Policy on behalf of each of Us. LLOYD'S POLICY SIGNING OFFICE General Manager If this policy (or any subsequent endorsement) has been produced to you in electronic form, the original document is stored on the Insurer's Market Repository to which your broker has access. -

Understanding How Insurance Works: a Case Study About Lucy (Guide) Cfpb Building Block Activities Understanding-How-Insurance-Works-Lucy Guide.Pdf

BUILDING BLOCKS TEACHER GUIDE Understanding how insurance works: A case study about Lucy Students read about how insurance works, then review a case study to see how insurance choices can affect personal finances for a rural young adult. Learning goals KEY INFORMATION Big idea Building block: When you purchase insurance, you are Executive Function transferring financial risk from yourself to an Financial knowledge and insurance company. decision-making skills Essential questions Grade level: High school (9–12) § What is the main benefit of choosing to Age range: 13–19 purchase insurance? Topic: Protect (Managing risk) § How do the insurance company and the policyholder share risks and costs? School subject: CTE (Career and technical education), Math, Physical education or Objectives health, Social studies or history Teaching strategy: Cooperative learning, § Understand how insurance works Simulation § Apply insurance policy specifics to a case study to evaluate costs and benefits Bloom’s Taxonomy level: Understand, Apply, Evaluate What students will do Activity duration: 45–60 minutes § Read about how the insurance process works and discover what roles the insurance STANDARDS company and the policyholders play. § Review information about specific types of Council for Economic Education Standard VI. Protecting and insuring insurance policy coverage and costs. Jump$tart Coalition Risk management and insurance – Standard 1 To find this and other activities go to: Consumer Financial Protection Bureau consumerfinance.gov/teach-activities 1 of 7 Winter 2020 § Evaluate a case study to see how one policyholder’s insurance choices affected her financially. § Write an advice email about the value of insurance in that policyholder’s life. -

My Insurance Doesn't Cover What?

MYMY INSURANCE INSURANCE DOESN’T DOESN’T COVER COVER WHAT? WHAT? AvoidAvoid surprises surprises by understanding by understanding your homeowners your insurance insurance policy policy DepartmentDepartment of Commerceof Commerce & Consumer & Consumer Affairs Affairs InsuranceInsurance Division Division CCA.HAWAII.GOV/INS @INSURANCEHI TABLE OF CONTENTS 1 My Insurance Doesn’t Cover What? . .2 2 Home Inventory . 4 3 Theft . 5 4 Fire . 6 5 Flooding . 7 6 Natural Disasters . 8 7 Preventative Measures and Actions . 10 8 What Isn’t Typically Covered . 12 9 The Claims Process . 13 The State of Hawaii Department of Commerce and Consumer Affairs (DCCA) is a regulatory agency that promotes a strong and healthy business environment by upholding fairness and public confidence in the marketplace. The department also strives to increase knowledge and opportunity for businesses and individuals, and to protect consumers against unfair and deceptive business practices. The DCCA Insurance Division oversees the insurance industry in the State of Hawaii. Its regulatory functions include: issuing licenses, examining the fiscal condition of Hawaii-based companies, reviewing rate and policy filings, and investigating insurance-related complaints. The National Association of Insurance Commissioners (NAIC) is the U.S. standard-setting and regulatory support organization created and governed by the chief insurance regulators from the 50 states, the District of Columbia and five U.S. territories. The NAIC’s website is a great source of consumer information at www.naic.org. This guide was created to equip you with information to better prepare for an emergency and understand what may or may not be covered by their insurance policy or policies. -

The Royal Engineers Journal

THE ROYAL ENGINEERS JOURNAL. Vol. XII. No. 6. DECEMBER, 1910. CONTENTS. PAGI'. 1. The Military Uses of the Aerostat. By Capt. P. W. L. BROKE-SMITH, R. E. ... 395 2. A Field Practice Sub-Target. By Capt. F. V. THOMPSON, R.E ... ... 403 3. Gibraltar under Moor, Spaniard, and Briton (conlinyted). By Col. E. R. KENYON, R. E. ... ... ... ... ... ... ... 409 4. Major-General Sir William Reid, R.E., G.C.M.G., K.C.B., F.R.S. (concluded). By Col. ROBT. H. VETCH, C.B., late R.E. (Wih Photo) . ... ... 427 5. Memoir:-Major-General Edward Renouard James, Royal Engineers (concluded). By Col. ROBT. H. VETCH, C.B., late R.E. .. 443 6. Transcript:-The Demolition of the Hun-Io Railway Bridge. (From the Razvyedchik). (With Photo) ... .. ...... ... 453 7. Notices of Magazines .. ... ... ... ... 455 8. Recent Publications of Military Interest ... ... ... 459 9. Correspondence:-Militia Post, Miranshah, Tochi Valley. By Major D. H. McNEILE, Comdt., N.W. Militia .. ... ... 466 INSTITUTION OF RE OFFICE COPY DO NOT REMOVE p. GUARANTEED: Immunity from repairs. Smooth on both sides. Roofs 5,781 Ibs. \ covered with "Eternit" Tensile Strength, T Crushing Force, 8,281 Ibs. lew weigh about 22 bs. Per Squarequare Inch andand LIGHT. per square yard. always inoreasing : \ with age. ON THE ADMIRALTY AND WAR OFFICE LISTS. For Diagonal or Honeycomb Style of Roofing. Colours: Grey, Blue and Red. Stock Size, l.5" Iby 15" ETERNIT" ROOF TILES (Ilatslhcek's Oliginal Patent). G. R. SPEAKER & CO., 29, MINCING LANE, LONDON, E.C. ENGINEERS Lees than one-half the cost of /and Broseley Tiles. /SURVEYOR Prompt delivferyv . -

Covering the Increased Liability of New Launch Markets

32nd Space Symposium, Technical Track, Colorado Springs, Colorado, United States of America Presented on April 11-12, 2016 COVERING THE INCREASED LIABILITY OF NEW LAUNCH MARKETS Robert Williams, [email protected] Kevin Walsh, [email protected] ABSTRACT The next generation space race prize is the integration of space dependent technology reliably in modern society. This paper is offered as an examination of an expanding diverse space launch industry as well as the necessity for increased capacity of resources in the underwriting space. Consumers are already space application dependent. There are 1 billion GPS receivers already deployed and expected to grow to 7 billion by 2022. As an example, satellites transformed 800 analogue channels in 1991 to more than 25,000 digital channels today. Without GPS, money isn’t accessible from an ATM. Space plays a greater role in day-to-day life and liability coverage will become more important. If a satellite fails for example, businesses relying on satellite services to function may want to claim for lost income or expenses incurred. Growth of space business has been characterized by a shift away from military and the public over to the private sector. Space activity was largely funded through government bodies such as NASA, the European Space Agency or the Japanese Space Agency. With recent estimates by the Satellite Industry Association placing cumulative satellite industry revenues at over $195.2 billion, a number of private companies are successfully entering the space industry and space application world. Governments and space agencies, which were ordering and building space hardware themselves, are now shifting towards buying services from private companies.