Assessing and Managing the Impact of T Elecom Deregulation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MFP / Printer / Scanner Print Scan Card Reade LPR* Print Scan

USB Server Compatibility List MFP / Printer / Scanner Windows Vista / Windows Windows XP 7** No Brand Model Name Card Card Print Scan LPR* Print Scan LPR* Reade Reade 1 Avision MF3230 Pass Pass* N/A Pass Pass Pass* N/A Pass 2 BenQ CM3000 Pass Pass N/A N/A Pass Pass N/A N/A 3 BenQ CM3500 Pass Pass Pass N/A Pass Pass Pass N/A 4 Brother HL 2040 Pass N/A N/A Pass Pass N/A N/A Pass 5 Brother HL 5250DN Pass N/A N/A Pass Pass N/A N/A Pass 6 Brother MFC-240C Pass Pass Pass Pass Pass Pass* Pass Pass 7 Brother MFC-3820cn Pass Pass - Pass Pass Pass - Pass 8 Brother MFC-3320cn Pass N/A - Pass - N/A - Pass 9 Brother MFC-7420 Pass Pass N/A Pass Pass Pass* N/A Pass 10 Canon CanonScan Lide 5.0 N/A Pass N/A - N/A Pass N/A - 11 Canon ImageClass MF3110 Pass Pass N/A Pass Pass Pass N/A Pass 12 Canon ImageClass MF3112 - - - Pass - - - Pass 13 Canon ImageClass MF3220 - - - Pass - - - Pass 14 Canon ImageClass MF3222 - - - Pass - - - Pass 15 Canon ImageClass MF4010 Pass Pass N/A Pass Pass Pass N/A Pass 16 Canon ImageClass MF4150 Pass Pass N/A Pass Pass Pass N/A Pass 17 Canon iP100 - - - Pass - - - Pass 18 Canon iP1700 Pass N/A N/A - Pass N/A N/A - 19 Canon iP2500 Pass N/A N/A Pass Pass N/A N/A Pass 20 Canon iP2600 Pass N/A N/A - Pass N/A N/A - 21 Canon iP3300 Pass N/A N/A - Pass N/A N/A - 22 Canon iP3500 Pass N/A N/A - Pass N/A N/A - 23 Canon iP3600 Pass N/A N/A - Pass N/A N/A - 24 Canon iP4200 Pass N/A N/A Pass Pass N/A N/A Pass 25 Canon iP4300 Pass N/A N/A - - N/A N/A - 26 Canon iP4500 Pass N/A N/A - Pass N/A N/A - 27 Canon iP4600 Pass N/A N/A - Pass N/A N/A -

How to Insert Memory Cards Into the Corresponding Card Slots

How to insert memory cards into the corresponding card slots Ensure the memory card is oriented correctly, and insert it straight into the correct memory card slot. • For the latest information on supported media, visit the official ELECOM website. http://www.elecom.co.jp/global/download/compatibility.html • This product is designed to continue supporting the latest media via firmware updates. Slot 1 Slot 2 USB 2.0 Multi Type Card Reader microSD Memory Card CompactFlash MR-K010 series microSDHC Memory Card Microdrive User's manual Wide Narrow Forward Usage Precautions Align the convex part of the memory card slot Face the terminal with the concave part of the memory card. Thank you for purchasing the MR-K010 Series USB 2.0 card reader. • If the PC is started when a memory card is inserted in this product, a disk scan may end downwards label side This user’s manual explains how to set up the product. Please thoroughly read be performed automatically, even if the PC had no previous abnormal termination Wide Narrow this user’s manual before use, to ensure proper setup of the product. errors. • If the PC is started when a memory card is inserted in this product, even if the Safety Precautions device has been connected before, the "Found New Hardware" message may be Face the label side upwards • Always observe the cautions issued by PC and peripheral device manufacturers displayed. when connecting and disconnecting this product. • It may take a minute or so for this product to be recognised by the PC after it has been • Do not attempt to disassemble, modify or repair this product by yourself. -

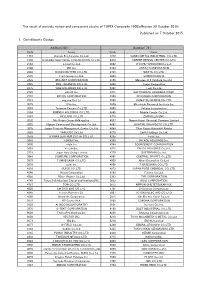

Published on 7 October 2016 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 31 October 2016) Published on 7 October 2016 1. Constituents Change Addition( 70 ) Deletion( 60 ) Code Issue Code Issue 1810 MATSUI CONSTRUCTION CO.,LTD. 1868 Mitsui Home Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 2196 ESCRIT INC. 2117 Nissin Sugar Co.,Ltd. 2198 IKK Inc. 2124 JAC Recruitment Co.,Ltd. 2418 TSUKADA GLOBAL HOLDINGS Inc. 2170 Link and Motivation Inc. 3079 DVx Inc. 2337 Ichigo Inc. 3093 Treasure Factory Co.,LTD. 2359 CORE CORPORATION 3194 KIRINDO HOLDINGS CO.,LTD. 2429 WORLD HOLDINGS CO.,LTD. 3205 DAIDOH LIMITED 2462 J-COM Holdings Co.,Ltd. 3667 enish,inc. 2485 TEAR Corporation 3834 ASAHI Net,Inc. 2492 Infomart Corporation 3946 TOMOKU CO.,LTD. 2915 KENKO Mayonnaise Co.,Ltd. 4221 Okura Industrial Co.,Ltd. 3179 Syuppin Co.,Ltd. 4238 Miraial Co.,Ltd. 3193 Torikizoku co.,ltd. 4331 TAKE AND GIVE. NEEDS Co.,Ltd. 3196 HOTLAND Co.,Ltd. 4406 New Japan Chemical Co.,Ltd. 3199 Watahan & Co.,Ltd. 4538 Fuso Pharmaceutical Industries,Ltd. 3244 Samty Co.,Ltd. 4550 Nissui Pharmaceutical Co.,Ltd. 3250 A.D.Works Co.,Ltd. 4636 T&K TOKA CO.,LTD. 3543 KOMEDA Holdings Co.,Ltd. 4651 SANIX INCORPORATED 3636 Mitsubishi Research Institute,Inc. 4809 Paraca Inc. 3654 HITO-Communications,Inc. 5204 ISHIZUKA GLASS CO.,LTD. 3666 TECNOS JAPAN INCORPORATED 5998 Advanex Inc. 3678 MEDIA DO Co.,Ltd. 6203 Howa Machinery,Ltd. 3688 VOYAGE GROUP,INC. 6319 SNT CORPORATION 3694 OPTiM CORPORATION 6362 Ishii Iron Works Co.,Ltd. 3724 VeriServe Corporation 6373 DAIDO KOGYO CO.,LTD. 3765 GungHo Online Entertainment,Inc. -

UE204 Supported Items List

B&B Electronics UE204, USB over IP Hub / Server Compatibility List MFP / Printer / Scanner Windows XP Windows Vista / Windows 7** No Brand Model Name Card Card Print Scan LPR* Print Scan LPR* Reader Reader 1 Avision MF3230 Pass Pass* N/A Pass Pass Pass* N/A Pass 2 BenQ CM3000 Pass Pass N/A N/A Pass Pass N/A N/A 3 BenQ CM3500 Pass Pass Pass N/A Pass Pass Pass N/A 4 Brother HL 2040 Pass N/A N/A Pass Pass N/A N/A Pass 5 Brother HL 5250DN Pass N/A N/A Pass Pass N/A N/A Pass 6 Brother MFC-240C Pass Pass Pass Pass Pass Pass* Pass Pass 7 Brother MFC-3820cn Pass Pass - Pass Pass Pass - Pass 8 Brother MFC-3320cn Pass N/A - Pass - N/A - Pass 9 Brother MFC-7420 Pass Pass N/A Pass Pass Pass* N/A Pass 10 Canon CanonScan Lide 5.0 N/A Pass N/A - N/A Pass N/A - 11 Canon ImageClass MF3110 Pass Pass N/A Pass Pass Pass N/A Pass 12 Canon ImageClass MF3112 - - - Pass - - - Pass 13 Canon ImageClass MF3220 - - - Pass - - - Pass 14 Canon ImageClass MF3222 - - - Pass - - - Pass 15 Canon ImageClass MF4010 Pass Pass N/A Pass Pass Pass N/A Pass 16 Canon ImageClass MF4150 Pass Pass N/A Pass Pass Pass N/A Pass 17 Canon iP100 - - - Pass - - - Pass 18 Canon iP1700 Pass N/A N/A - Pass N/A N/A - 19 Canon iP2500 Pass N/A N/A Pass Pass N/A N/A Pass 20 Canon iP2600 Pass N/A N/A - Pass N/A N/A - 21 Canon iP3300 Pass N/A N/A - Pass N/A N/A - 22 Canon iP3500 Pass N/A N/A - Pass N/A N/A - 23 Canon iP3600 Pass N/A N/A - Pass N/A N/A - 24 Canon iP4200 Pass N/A N/A Pass Pass N/A N/A Pass 25 Canon iP4300 Pass N/A N/A - - N/A N/A - 26 Canon iP4500 Pass N/A N/A - Pass N/A N/A - 27 -

Semiconductor Manufacturers. Our Primary Semiconductor Competitors

Semiconductor Manufacturers. Our primary semiconductor competitors currently include Hynix, IM Flash Technologies LLC, or IMFT (a company formed by Micron and Intel), Micron, Samsung, and Toshiba. Flash Memory Card and USB Drive Manufacturers. Our primary card and USB drive competitors currently include, among others, A-DATA Technology Co., Ltd., or A-DATA, Buffalo, Inc., or Buffalo, Chips and More GmbH, or CnMemory, Dane-Elec Memory, or Dane-Elec, Eastman Kodak Company, or Kodak, Elecom Co., Ltd., or Elecom, FUJIFILM Corporation, or FUJI, Gemalto N.V., or Gemalto, Hagiwara Sys-Com Co., Ltd., or Hagiwara, Hama, Hynix, Imation Corporation, or Imation, and its division Memorex Products, Inc., or Memorex, I-O Data Device, Inc., or I-O Data, Kingmax Digital, Inc., or KingMax, Kingston Technology Company, Inc., or Kingston, Lexar, Micron, Netac Technology Co., Ltd., or Netac, Panasonic, PNY Technologies, Inc., or PNY, RITEK Corporation, or RITEK, Samsung, Sony, STMicroelectronics N.V., or STMicroelectronics, Toshiba, Tradebrands International, or Tradebrands, Transcend Information, Inc., or Transcend, and Verbatim Americas LLC, or Verbatim. Solid-State Drive and Hard Disk Drive Manufacturers. Our SSDs face competition from other manufacturers of SSDs, including Intel, Samsung, Toshiba, and others. Our SSDs also face competition from hard disk drives, which are offered by companies including, among others, Seagate Technology LLC, or Seagate, Samsung and Western Digital Corporation, or Western Digital. Digital Audio/Video Player Manufacturers. Our digital audio/video players face strong competition from products offered by companies, including Apple Inc., or Apple, ARCHOS Technology, or ARCHOS, Coby Electronics Corporation, or Coby, Creative Technology Ltd., or Creative, Koninklijke Philips Electronics N.V., or Royal Philips Electronics, Microsoft Corporation, or Microsoft, Samsung and Sony. -

Stoxx® Japan 600 Esg-X Index

STOXX® JAPAN 600 ESG-X INDEX Components1 Company Supersector Country Weight (%) Toyota Motor Corp. Automobiles & Parts Japan 3.87 Sony Corp. Consumer Products & Services Japan 2.55 Softbank Group Corp. Telecommunications Japan 2.44 Keyence Corp. Industrial Goods & Services Japan 1.77 RECRUIT HOLDINGS Industrial Goods & Services Japan 1.54 Mitsubishi UFJ Financial Group Banks Japan 1.48 Shin-Etsu Chemical Co. Ltd. Chemicals Japan 1.36 Nippon Telegraph & Telephone C Telecommunications Japan 1.36 Nintendo Co. Ltd. Consumer Products & Services Japan 1.30 Nidec Corp. Technology Japan 1.30 Fast Retailing Co. Ltd. Retail Japan 1.25 Daikin Industries Ltd. Construction & Materials Japan 1.19 Takeda Pharmaceutical Co. Ltd. Health Care Japan 1.18 Tokyo Electron Ltd. Technology Japan 1.16 Honda Motor Co. Ltd. Automobiles & Parts Japan 1.10 Daiichi Sankyo Co. Ltd. Health Care Japan 1.08 Sumitomo Mitsui Financial Grou Banks Japan 1.04 Murata Manufacturing Co. Ltd. Technology Japan 1.03 KDDI Corp. Telecommunications Japan 1.02 Hitachi Ltd. Industrial Goods & Services Japan 0.92 Itochu Corp. Industrial Goods & Services Japan 0.92 Fanuc Ltd. Industrial Goods & Services Japan 0.90 Hoya Corp. Health Care Japan 0.84 Mitsubishi Corp. Industrial Goods & Services Japan 0.83 Mizuho Financial Group Inc. Banks Japan 0.76 SOFTBANK Telecommunications Japan 0.75 Denso Corp. Automobiles & Parts Japan 0.72 Mitsui & Co. Ltd. Industrial Goods & Services Japan 0.71 Tokio Marine Holdings Inc. Insurance Japan 0.70 Oriental Land Co. Ltd. Travel & Leisure Japan 0.68 SMC Corp. Industrial Goods & Services Japan 0.68 Mitsubishi Electric Corp. Industrial Goods & Services Japan 0.67 Seven & I Holdings Co. -

2. Hardware Periphery Compatibility 2.1. Hard Drives

2. Hardware Periphery Compatibility 2.1. Hard Drives []: Win7 Ready 2.1.1. Hard Disk Type Model Win7 Ready SATA WD WD WD1500ADFD SATA 3G ExcelStor ExcelStor J880S Hitachi Hitachi HDT721025SLA380 Hitachi HDS721010KLA330 Hitachi HDS721050CLA362 Hitachi HDS721010CLA332 Hitachi HDS722020ALA330 Hitachi HDP725016GLA380 Hitachi HDP725025GLA380 Hitachi HDP725032GLA380 Hitachi HDP725032GLA360 Hitachi HDP725050GLA360 Hitachi HDP725050GLA380 Maxtor Maxtor STM3500320AS Maxtor STM31000340AS Samsung Samsung HD103SJ Samsung HD153WI Samsung HD203WI Samsung HD321KJ Samsung HD502IJ Samsung HD753LJ Samsung HD103UJ Seagate Seagate ST3500320AS Seagate ST3750330AS Seagate ST31000333AS Seagate ST31500341AS Seagate ST3500418AS Seagate ST3750528AS Seagate ST31000528AS Seagate ST3500320NS Seagate ST32000540AS Seagate ST31000340NS Seagate ST95005620AS Seagate ST3808110AS Seagate ST3808115AS Seagate ST3250310AS Seagate ST3160815AS Seagate ST3250620AS Copyright 2012 ASUSTeK Computer Inc. PAGE 1 M5A97 EVO R2.0 Seagate ST3250410AS Seagate ST3320620AS Seagate ST3750640AS WD WD WD3000GLFS WD WD5000ABYS WD WD5000ABPS WD WD7500AYPS WD WD2502ABYS WD WD5002ABYS WD WD7501AALS WD WD10EACS-00ZJB0 WD WD10EACS-00D6B0 WD WD20EADS WD WD2001FASS WD WD10EARS WD WD15EARS WD WD20EARS WD WD30EZRS WD WD1600AAJS WD WD1600AVJS WD WD6400AAKS WD WD2500AAKS WD WD3200AAKS WD WD5000AAKS WD WD5000AAKB WD WD2500AAJB SATA 6G Hitachi Hitachi HDS723030ALA640 Seagate Seagate ST31000529AS Seagate ST32000641AS Seagate ST33000651AS -

Published on 7 October 2015 1. Constituents Change the Result Of

The result of periodic review and component stocks of TOPIX Composite 1500(effective 30 October 2015) Published on 7 October 2015 1. Constituents Change Addition( 80 ) Deletion( 72 ) Code Issue Code Issue 1712 Daiseki Eco.Solution Co.,Ltd. 1972 SANKO METAL INDUSTRIAL CO.,LTD. 1930 HOKURIKU ELECTRICAL CONSTRUCTION CO.,LTD. 2410 CAREER DESIGN CENTER CO.,LTD. 2183 Linical Co.,Ltd. 2692 ITOCHU-SHOKUHIN Co.,Ltd. 2198 IKK Inc. 2733 ARATA CORPORATION 2266 ROKKO BUTTER CO.,LTD. 2735 WATTS CO.,LTD. 2372 I'rom Group Co.,Ltd. 3004 SHINYEI KAISHA 2428 WELLNET CORPORATION 3159 Maruzen CHI Holdings Co.,Ltd. 2445 SRG TAKAMIYA CO.,LTD. 3204 Toabo Corporation 2475 WDB HOLDINGS CO.,LTD. 3361 Toell Co.,Ltd. 2729 JALUX Inc. 3371 SOFTCREATE HOLDINGS CORP. 2767 FIELDS CORPORATION 3396 FELISSIMO CORPORATION 2931 euglena Co.,Ltd. 3580 KOMATSU SEIREN CO.,LTD. 3079 DVx Inc. 3636 Mitsubishi Research Institute,Inc. 3093 Treasure Factory Co.,LTD. 3639 Voltage Incorporation 3194 KIRINDO HOLDINGS CO.,LTD. 3669 Mobile Create Co.,Ltd. 3197 SKYLARK CO.,LTD 3770 ZAPPALLAS,INC. 3232 Mie Kotsu Group Holdings,Inc. 4007 Nippon Kasei Chemical Company Limited 3252 Nippon Commercial Development Co.,Ltd. 4097 KOATSU GAS KOGYO CO.,LTD. 3276 Japan Property Management Center Co.,Ltd. 4098 Titan Kogyo Kabushiki Kaisha 3385 YAKUODO.Co.,Ltd. 4275 Carlit Holdings Co.,Ltd. 3553 KYOWA LEATHER CLOTH CO.,LTD. 4295 Faith, Inc. 3649 FINDEX Inc. 4326 INTAGE HOLDINGS Inc. 3660 istyle Inc. 4344 SOURCENEXT CORPORATION 3681 V-cube,Inc. 4671 FALCO HOLDINGS Co.,Ltd. 3751 Japan Asia Group Limited 4779 SOFTBRAIN Co.,Ltd. 3844 COMTURE CORPORATION 4801 CENTRAL SPORTS Co.,LTD. -

Final List of Participants

13th World Telecommunication/ICTIndicators Symposium Hiroshima, Japan, 30 November to 2 December 2015 Final List of Participants 1) Member States 2) ITU Sector Members Recognized Operating Agencies 3) ITU Sector Members Scientific or Industrial Organizations 4) ITU-D Sector Members Other Entities dealing with Telecommunications 5) ITU Sector Members Regional Telecommunication Organizations 6) United Nations and its Specialized Agencies 7) Guests 8) Academia 9) Sponsors 10) ITU Secretariat 1) Member States Afghanistan D Dr Mohammad Najib AZIZI, Chairman of Afghanistan Telecom Regulatory Authority (ATRA), Ministry of Communications and Information Technology (MCIT) Algeria (People's Democratic Republic of) D Mr Amar BALLA, Membre du Conseil, Autorité de Régulation de la Poste et des Télécommunications (ARPT) Angola (Republic of) D Ms Jacqueline LUZOLO INEZA, High Level Technician, Angolan Institute of Communications (INACOM) Australia D Ms Tonina STAUNTON, Director, Data Science and Analytics, Australian Government Department of Communications Bahrain (Kingdom of) D Mr Musab ABDULLA, Director of Telecommunications, Ministry of Transportation and Telecommunications D Mr Abdulrahman ALSOWAIDI, Manager, Market and Competition Department, Telecommunication Regulatory Authority of Bahrain D Mr Saeed MASHKOOR, Senior Market and Competition Analyst, Telecommunications Regulatory Authority Bangladesh (People's Republic of) D Mr Ashfaque AHMED, Assistant Director, Bangladesh Telecommunication Regulatory Commission D Mr M. A. Taleb HOSSAIN, Director, -

Fidelity® Total International Index Fund

Fidelity® Total International Index Fund Annual Report October 31, 2020 See the inside front cover for important information about access to your fund’s shareholder reports. Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary, such as a financial advisor, broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report. If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a fund electronically, by contacting your financial intermediary. For Fidelity customers, visit Fidelity’s web site or call Fidelity using the contact information listed below. You may elect to receive all future reports in paper free of charge. If you wish to continue receiving paper copies of your shareholder reports, you may contact your financial intermediary or, if you are a Fidelity customer, visit Fidelity’s website, or call Fidelity at the applicable toll-free number listed below. Your election to receive reports in paper will apply to all funds held with the fund complex/your financial intermediary. Account Type Website Phone Number -

Company Vendor ID (Decimal Format) (AVL) Ditest Fahrzeugdiagnose Gmbh 4621 @Pos.Com 3765 0XF8 Limited 10737 1MORE INC

Vendor ID Company (Decimal Format) (AVL) DiTEST Fahrzeugdiagnose GmbH 4621 @pos.com 3765 0XF8 Limited 10737 1MORE INC. 12048 360fly, Inc. 11161 3C TEK CORP. 9397 3D Imaging & Simulations Corp. (3DISC) 11190 3D Systems Corporation 10632 3DRUDDER 11770 3eYamaichi Electronics Co., Ltd. 8709 3M Cogent, Inc. 7717 3M Scott 8463 3T B.V. 11721 4iiii Innovations Inc. 10009 4Links Limited 10728 4MOD Technology 10244 64seconds, Inc. 12215 77 Elektronika Kft. 11175 89 North, Inc. 12070 Shenzhen 8Bitdo Tech Co., Ltd. 11720 90meter Solutions, Inc. 12086 A‐FOUR TECH CO., LTD. 2522 A‐One Co., Ltd. 10116 A‐Tec Subsystem, Inc. 2164 A‐VEKT K.K. 11459 A. Eberle GmbH & Co. KG 6910 a.tron3d GmbH 9965 A&T Corporation 11849 Aaronia AG 12146 abatec group AG 10371 ABB India Limited 11250 ABILITY ENTERPRISE CO., LTD. 5145 Abionic SA 12412 AbleNet Inc. 8262 Ableton AG 10626 ABOV Semiconductor Co., Ltd. 6697 Absolute USA 10972 AcBel Polytech Inc. 12335 Access Network Technology Limited 10568 ACCUCOMM, INC. 10219 Accumetrics Associates, Inc. 10392 Accusys, Inc. 5055 Ace Karaoke Corp. 8799 ACELLA 8758 Acer, Inc. 1282 Aces Electronics Co., Ltd. 7347 Aclima Inc. 10273 ACON, Advanced‐Connectek, Inc. 1314 Acoustic Arc Technology Holding Limited 12353 ACR Braendli & Voegeli AG 11152 Acromag Inc. 9855 Acroname Inc. 9471 Action Industries (M) SDN BHD 11715 Action Star Technology Co., Ltd. 2101 Actions Microelectronics Co., Ltd. 7649 Actions Semiconductor Co., Ltd. 4310 Active Mind Technology 10505 Qorvo, Inc 11744 Activision 5168 Acute Technology Inc. 10876 Adam Tech 5437 Adapt‐IP Company 10990 Adaptertek Technology Co., Ltd. 11329 ADATA Technology Co., Ltd. -

American Century Investments® Quarterly Portfolio Holdings Avantis

American Century Investments® Quarterly Portfolio Holdings Avantis® International Equity ETF (AVDE) November 30, 2020 Avantis International Equity ETF - Schedule of Investments NOVEMBER 30, 2020 (UNAUDITED) Shares/ Principal Amount ($) Value ($) COMMON STOCKS — 99.7% Australia — 6.5% Accent Group Ltd. 14,526 23,059 Adairs Ltd. 9,223 21,547 Adbri Ltd. 12,481 28,274 Afterpay Ltd.(1) 48 3,354 AGL Energy Ltd. 8,984 89,075 Alkane Resources Ltd.(1)(2) 41,938 31,367 Alliance Aviation Services Ltd.(1) 5,187 13,148 ALS Ltd. 2,039 14,302 Altium Ltd. 1,563 40,787 Alumina Ltd. 16,346 20,996 AMA Group Ltd.(1) 16,885 9,258 AMP Ltd. 223,348 280,458 Ampol Ltd. 2,595 58,421 Ansell Ltd. 1,333 36,644 APA Group 16,232 123,383 Appen Ltd. 1,821 42,222 ARB Corp. Ltd. 3,172 64,616 Ardent Leisure Group Ltd.(1) 22,550 13,624 Aristocrat Leisure Ltd. 12,775 300,907 ASX Ltd. 1,422 80,525 Atlas Arteria Ltd. 5,725 27,252 Atlassian Corp. plc, Class A(1) 2,086 469,454 Aurelia Metals Ltd. 60,190 18,351 Aurizon Holdings Ltd. 113,756 355,100 AusNet Services 71,401 97,009 Austal Ltd. 23,896 51,252 Australia & New Zealand Banking Group Ltd. 67,427 1,121,525 Australian Agricultural Co. Ltd.(1) 32,331 25,519 Australian Ethical Investment Ltd. 3,654 13,530 Australian Finance Group Ltd. 21,308 37,254 Australian Pharmaceutical Industries Ltd. 29,606 26,147 Bank of Queensland Ltd.