The Philippine Payment System: Efficiency and Implications for the Conduct of Monetary Policy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telegraphic Transfer Format

PHILIPPINE RETIREMENT AUTHORITY TELEGRAPHIC TRANSFER FORMAT TO :________________________________________________________________________ (Name of Remitting International Bank) Pay To :________________________________________________________________________ (Name of Depository Bank) The Amount of US $ _____________________________________ to set up a FDCU time deposit acount in the name of Mr/Ms. _________________________________________________________ (Name of Retiree/Applicant) under the (PRA) Retirement Program. Upon the receipt of the remittances, please telephone/ advise PRA Immediately. __________________________________________________________________ (Signature of Retiree/Applicant) BANK OF COMMERCE Wachovia Bank, Int'l Division Contact Person: Account No. 2000-19113363-5 or MR. EDMUND B. SANTOS Union Bank of California, N.Y. Tel No. (632) 840-3261 Account No. 91-280123-1121 E-mail:[email protected] BANKWISE Union Bank of California Contact Person: International New York MR. DENNIS ROLDAN Swift BOFCUS33NYK MR. AURORA A. CRUZ CHIPS ABA 505 OR MS.LEA PROTACIO FEDWIRE Routing 026005050 Tel. No. (632) 894-4242: 894-4029 813-7419 EQUITABLE PCI BANK Bank of New york,New York Contact Person: Swift Code: IRVTUS3N or American Express Bank, NY MR. ALLAN DAVID L. MATUTINA Swiff code: AEIBUS33 Tel. Nos: (632) 891-2467;840-7000 EAST WEST BANK Wachovia Bank, New York Contact Person: FAO: East West Bank Manila MS. ELIZABETH P. AQUINO Acct. No. 2000-19100258-8 MR. DAVE DE CASTRO For further credit to EWBC Tel. Nos.(632) 830-8741/42 DOLLAR PRIME FUND 818-0080 ACCT. No. 09-70-00516-1 E-mail: [email protected] [email protected] EXPORT BANK Union Bank of California Contact Person: International New York MS. MA. CRISTINA B. GUARINA Account No. 91-278275-1121 Tel. Nos. (632) 533-3546;533-3550 RIZAL COMMERCIAL BANKING CORPORATION Citibank New York, U.S.A. -

Country Diagnostic: Philippines

Philippines BETTERTHANCASH COUNTRY DIAGNOSTIC ALLIANCE Empowering People Through Electronic Payments July 2015 Development Results Focused Research Program Country Diagnostic: Philippines by James Hokans, Bankable Frontier Associates Philippines BETTERTHANCASH COUNTRY DIAGNOSTIC ALLIANCE Empowering People Through Electronic Payments July 2015 Development Results Focused Research Program Country Diagnostic: Philippines by James Hokans, Bankable Frontier Associates BETTERTHANCASH ALLIANCE Empowering People Through Electronic Payments INTRODUCTION TO THE BETTER THAN CASH ALLIANCE The Better Than Cash Alliance (the Alliance) is a partnership of governments, companies, and international organizations that accelerates the transition from cash to digital payments in order to drive inclusive growth and reduce poverty. Shifting from cash to digital payments has the potential to improve the lives of low-income people, particularly women, while giving governments, companies and international organizations a more transparent, time- and cost-efficient, and often safer means of making and receiving payments. We partner with governments, companies, and international organizations that are the key drivers behind the transition to make digital payments widely available by: 1. Advocating for the transition from cash to digital payments in a way that advances financial inclusion and promotes responsible digital finance. 2. Conducting research and sharing the experience our members to inform strategies for making the transition 3. Catalyzing the development -

This Document Was Downloaded from Duplication Or Reproduction Is Allowed

This document was downloaded from www.psbank.com.ph. Duplication or reproduction is allowed. Please do not modify its content. Document Classification: PUBLIC COVER SHEET 15552 SEC Registration Number P H I L I P P I N E S AV I N G S B A N K (Company’s Full Name) P S B a n k C e n t e r , 7 7 7 P a s e o d e R o x a s c o r n e r S e d e ñ o S t r e e t , M a k a t i C i t y (Business Address: No. Street City/Town/Province) Leah M. Zamora 845-8888 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting – To be Announced) (Secondary License Type, If Applicable) Markets and Securities Regulation Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 1,455 Total No. of Stockholders Domestic Foreign As of March 31, 2020 To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. This document was downloaded from www.psbank.com.ph. Duplication or reproduction is allowed. Please do not modify its content. Document Classification: PUBLIC SEC Number 15552 FILE Number PHILIPPINE SAVINGS BANK (COMPANY’S NAME) PSBank Center 777 Paseo de Roxas cor. Sedeño St., Makati City (COMPANY’S ADDRESS) 8885-82-08 (TELEPHONE NUMBER) DECEMBER 31 (FISCAL YEAR ENDING MONTH & DAY) SEC FORM 17-A (FORM TYPE) December 31, 2019 (PERIOD ENDED DATE) Government Securities Eligible Dealer (SECONDARY LICENSE TYPE AND FILE NUMBER) This document was downloaded from www.psbank.com.ph. -

The State of Digital Payments in the Philippines (Released in 2015) Found That Adoption Had Been Limited

COUNTRY DIAGNOSTIC The State of Digital Payments in the Philippines DECEMBER 2019 PHILIPPINES Authors Project Leads: Keyzom Ngodup Massally, Rodrigo Mejía Ricart Technical authors: Malavika Bambawale, Swetha Totapally, and Vineet Bhandari Cover photo: © Better Than Cash Alliance/Erwin Nolido 1 FOREWORD Our country was one of the first to pioneer digital payments nearly 20 years ago. Recognizing the untapped market potential and the opportunity to foster greater access to financial inclusion, the Bangko Sentral ng Pilipinas (BSP) has worked, hand in hand, with the government and the leaders across financial, retail, and regulatory sectors to boost digital payments. Over the past three years, since the launch of the first digital payments diagnostic, the Philippines has experienced remarkable progress toward building an inclusive digital payments ecosystem. In 2013, digital payments accounted for only 1% of the country’s total transaction volume. In 2018, this follow through diagnostic study showed that the volume of digital payments increased to 10% corresponding to 20% share in the total transaction value. These numbers speak of significant progress and success. I am optimistic that e-payments will gain further momentum as we have laid the necessary building blocks to accelerate innovation and inclusive growth over the next few years. Notably, Filipino women are ahead of men in the uptake of digital payments, placing us ahead of global standards. The rise of fintech and their solutions are starting to play a transformative role, as we can see from the rapidly-growing adoption of the emerging QR codes for digital transactions. I am confident that the BSP has built a good digital foundation and is well positioned to leverage fintech in increasing the share of digital payments toward a cash- lite Philippines. -

Standard Document Cover Sheet for Sec Filings

STANDARD DOCUMENT COVER SHEET FOR SEC FILINGS All documents should be submitted under a cover page which clearly identifies the company and the specific document form as follows: SEC Number * 121 (required) File Number ** BANK OF THE PHILIPPINE ISLANDS 6768 BPI BUILDING, AYALA AVENUE, MAKATI CITY 818-5541 to 48 December 31, 2009 SEC FORM I7 -A (Form type) AMENDMENT DESIGNATION (if applicable) FOR THE PERIOD ENDED DECEMBER 31, 2009 (if a report, financial statement, GIS, or related amendment or show-cause filing) NONE EACH ACTIVE SECONDARY LICENSE TYPE AND FILE NUMBER (state “NONE” if that is the case) * SEC will assign SEC No. to new companies. ** SEC will assign File No. to new applications or registrations. *** Companies should display the File No. on any filing which is an amendment to an application or registration 2 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended : DECEMBER 31, 2009 2. SEC Identification Number : 121 3. BIR Tax Identification No. : TIN: 047-000-438-366 4. BANK OF THE PHILIPPINE ISLANDS Exact name of issuer as specified in its charter 5. Ayala Avenue, Makati City, Metro Manila, Philippines Province, Country or other jurisdiction of incorporation or organization 6. Industry Classification Code : (SEC Use Only) 7. BANK OF THE PHILIPPINE ISLANDS BUILDING Cor. Ayala Avenue & Paseo de Roxas Makati City, Metro Manila ZIP Code 1226 Address of principal office Postal Code 8. (02) 818-5541 to 48 Issuer’s telephone number, include area code 9. -

Philequity Corner (May 8, 2017) by Wilson Sy the Hunter Games After

Philequity Corner (May 8, 2017) By Wilson Sy The Hunter Games After consolidating for more than three months between 7,100 to 7,400, the PSEi closed last Friday at 7,842. Aside from robust global markets, one of the catalysts that contributed to the PSEi’s strong move is the speculation about possible M&As in the banking sector. Speculation on RCBC takeover leads bank stocks higher Recently, there has been speculation that some banks may be in play as potential acquisition targets. This started with RCB’s gap up move on April 17. 4/12/17 5/5/17 % Chg RCB 39.00 58.70 50.5% PNB 57.50 68.65 19.4% EW 20.80 22.70 9.1% MBT 84.50 86.95 2.9% UBP 79.65 81.95 2.9% BDO 121.00 123.00 1.7% BPI 105.00 105.10 0.1% SECB 217.00 215.60 -0.6% CHIB 38.20 36.45 -4.6% Sources: Bloomberg, Wealth Research From the table above, it can be seen that RCB has risen 50.5% since April 12. Moreover, it has surged 104.2% from its bottom of 28.75 on March 22, 2016 (at the height of the AMLA investigations). Note that RCB has been rumoured to be a takeover target for several years. PNB and EastWest Bank follow RCBC’s lead Aside from RCB, both PNB and EastWest Bank (EW) gained significantly since mid-April. Not surprisingly, these three banks were trading below book value and were the cheapest among liquid banking stocks before this recent move ensued. -

2004 (Fiscal Year Ending) (Month/Day/Year)

Sec Number 5223 File Number _____ Equitable PCI Bank Tower I, Makati Ave. cor. H.V. dela Costa St., Makati City (Company’s Address) 632) 840-7000 (Telephone Number) December 31, 2004 (Fiscal Year Ending) (month/day/year) SEC Form 17-A (Annual Report) (Form Type) SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended: December 31, 2004 2. SEC Identification Number: 5223 3. BIR Tax Identification No.: 000-453-086 1. Exact name of registrant as specified in its charter: EQUITABLE PCI BANK, INC. 5. Philippines 6. (SEC Use Only) Province, Country or other jurisdiction of Industry Classification Code incorporation or organization 7. Equitable PCI Bank Tower I Makati Ave. cor H.V. de la Costa St. Makati City, Metro Manila Address of principal office 8. (632) 840-7000 ______ Issuer’s telephone number, including area code 9. Former name, former address, and former fiscal year, if changed since last report. 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sec. 4 and 8 of the RSA Number of Shares of Common Stock Title of Each Class Outstanding and Amount of Debt Outstanding Common shares 727,003,345 11. Are any or all of these securities listed on a Stock Exchange? YES [ x ] NO [ ] Name of Stock Exchange: Philippine Stock exchange, Inc. Class of Securities Listed: Common Shares 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a) -1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports); YES [ x ] NO [ ] (b) has been subject to such filing requirements for the past 90 days. -

We Are Pleased to Furnish Your Good Office with a Copy Of

March 20, 2019 PHILIPPINE STOCK EXCHANGE, INC. Disclosure Department 6F PSE Tower One Bonifacio High Street 28th Street corner 5th Avenue Bonifacio Global City Taguig City Attention: MS. JANET A. ENCARNACION Head - Disclosure Department PHILIPPINE DEALING & EXCHANGE CORP. 37/F Tower 1, The Enterprise Center 6766 Ayala Avenue cor Paseo de Roxas Makati City Attention: ATTY. JOSEPH B. EVANGELISTA Head- Issuer Compliance and Disclosure Department Gentlemen: We are pleased to furnish your good office with a copy of our SEC Form 20 Information Statement Definitive (pursuant to section 20 of the Securities Regulation Code) filed with the Securities and Exchange Commission (SEC). For your information and guidance. Thank you. Very truly yours, ALEXANDER C. ESCUCHA Senior Vice President & Head Investor & Corporate Relations Group CHINA BANKING CORPORATION 8745 Paseo de Roxas corner Villar Street, Makati City, Philippines Tel. No. 885-5555 • Fax No. 815-3169 • www.chinabank. P R O X Y That I/we, the undersigned stockholder/s of CHINA BANKING CORPORATION (“China Bank”), do hereby appoint _________________________________________________________ or in his absence, the Chairman of the meeting, as my/our proxy, to represent me/us and vote all shares of stocks registered in my/our name, at the Annual Meeting of Stockholders of China Bank on May 2, 2019, Thursday, and at any of the adjournments and postponements thereof, for the purpose of acting on the following matters: 3. Approval of Annual Report 1. Election of Directors ___ Yes ___ No ___ Abstain ___ Vote for all nominees listed below: Hans T. Sy Harley T. Sy 4. Approval of financial statements for the year ended Gilbert U. -

2020 Annual Report

2020 ANNUAL REPORT MOVING FORWARD, FUTURE READY 2020 ANNUAL REPORT 1. CORPORATE POLICY Our Vision: We are the preferred savings bank with a highly competent and dedicated professional team committed to delivering excellent service and providing responsive and innovative solutions to our chosen markets. Our Mission: We provide a highly rewarding and significantly beneficial experience to our stakeholders by: • Delivering efficient and personalized service to our customers; • Ensuring the professional growth and personal well-being of our employees; • Optimizing return on shareholder investment; • Maximizing synergy with business partners; and • Promoting corporate social responsibility. About the Bank: • Equicom Savings Bank (EqB) is a medium-sized savings bank established on September 29, 2008 with 10 branches located in NCR, Southern Luzon, Visayas, and Mindanao • Proud member of the Equicom Group and BancNet • As of end-December 2019, EqB was among the country’s top 20 thrift banks (in a group of 49 small, medium, and large thrift banks) in terms of total assets, total deposits, total loan portfolio volume, and return on equity • On April 2018, EqB was one of the five (5) pilot BSP-supervised institutions to launch instaPay, representing the thrift banks • On July 2012, EqB was the first bank to receive the "Pagtugon Award" bestowed by the Bangko Sentral ng Pilipinas (BSP). This award recognizes EqB’s excellence in responding to issues or concerns of clients referred to the Bank by the BSP • EqB’s strong presence in its niche market not only rests on its solid banking relationship with its clients and its synergistic connection with other companies in the Equicom Group, but also draws momentum from the dedicated efforts of its highly-competent professional teams steeped in sound banking practices and operations 4 EQUICOM SAVINGS BANK Business Model of the Bank We opened our doors in 2008 and currently engaged in retail banking, credit, debit, and prepaid cards, and commercial banking services. -

2007 BDO Annual Report Description : Building for the Future

B U I L D I N G 07 annual FOR THE FUTURE report FINANCIAL HIGHLIGHTS CORPORATE MISSION To be the preferred bank in every market we serve by consistently providing innovative products and flawless delivery of services, proactively reinventing (Bn PhP) 2006 2007 % CHANGE RESOURCES 628.88 617.42 -1.8% ourselves to meet market demands, creating shareholder value through GROSS CUSTOMER LOANS 257.96 297.03 15.1% superior returns, cultivating in our people a sense of pride and ownership, DEPOSIT LIABILITIES 470.08 445.40 -5.3% and striving to be always better than what we are today…tomorrow. CAPITAL FUNDS 52.42 60.54 15.5% NET INCOME 6.39 6.52 2.0% CORE VALUES RESOURCES CAPITAL FUNDS Commitment to Customers 700 70 We are committed to deliver products and services that surpass customer 600 60 629 617 61 expectations in value and every aspect of customer service, while remaining to 500 50 52 ) 400 ) 40 be prudent and trustworthy stewards of their wealth. P P h h P P 300 30 (Bn (Bn Commitment to a Dynamic and Efficient Organization 200 20 234 20 180 17 We are committed to creating an organization that is flexible, responds to 100 149 10 15 0 0 change and encourages innovation and creativity. We are committed to the 03 04 05 06 07 03 04 05 06 07 process of continuous improvements in everything we do. BDO Merged BDO-EPCI BDO Merged BDO-EPCI Commitment to Employees GROSS CUSTOMER LOANS DEPOSIT LIABILITIES NET INCOME We are committed to our employees’ growth and development and we 350 500 7.0 will nurture them in an environment where excellence, integrity, teamwork, 300 470 6.0 6.5 445 6.4 297 400 250 5.0 professionalism and performance are valued above all else. -

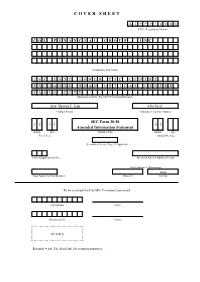

C O V E R S H E

C O V E R S H E E T A 1 9 9 9 1 0 0 6 5 S.E.C. Registration Number C O L F I N A N C I A L G R O U P , I N C . (Company's Full Name) 2 4 F E A S T T O W E R P S E C E N T R E E X C H A N G E R O A D O R T I G A S C E N T E R P A S I G C I T Y (Business Address: No. Street City/Town/Province) Atty. Sharon T. Lim 636-54-11 Contact Person Company Telephone Number SEC Form 20-IS 1 2 3 1 0 3 Amended Information Statement Month Day FORM TYPE Month Day Fiscal Year Annual Meeting Secondary License Type, If Applicable Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings none Total Number of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document I.D. Cashier STAMPS Remarks = pls. Use black ink for scanning purposes PROXY The undersigned stockholder of COL FINANCIAL GROUP, INC., (the “Corporation”) hereby appoints ______________________ or in his absence, the Chairman of the meeting, as attorney and proxy, with power of substitution, to represent and vote all shares registered in my name as proxy of the undersigned stockholder, at the Annual Meeting of Stockholders of the Corporation on March 29, 2019, and at any adjournments thereof for the purpose of acting on the following matters: 1. -

MERCHANT AGREEMENT A

MERCHANT AGREEMENT This Merchant Agreement (the “Agreement”) is made and executed in the City of ___________________, on this day of _______________________________, by and between: BANK OF THE PHILIPPINE ISLANDS, a universal banking corporation duly organized and existing under and by virtue of the laws of the Republic of the Philippines, with principal office and place of business at BPI Card Center, 8753 Paseo de Roxas, Makati City, hereinafter referred to as “BPI”; - and - ________________________________________, a corporation duly organized and existing under and by virtue of the laws of the Philippines/sole proprietorship owned and operated by ___________________________________________________, doing business under the name and style “______________________________________________”, with principal office and place of business at __________________________________________________________________________, represented herein by its authorized representative _________________________________________ , hereinafter referred to as the “MERCHANT”. WITNESSETH THAT: WHEREAS, BPI is engaged in the business of acquiring credit, debit and/or prepaid card transactions at affiliated merchant establishments and is licensed to enter into this Agreement with MERCHANT to honor these cards for the purchase of goods and/ or services from the MERCHANT’s establishments; WHEREAS, the MERCHANT is duly licensed to engage in business and agrees to honor all credit, debit and/or prepaid cards, whether BPI issued or not, (each, a “Card”) as payment for its sale of goods and/or services, and agrees to be bound by the terms and conditions set forth hereunder; NOW THEREFORE, for and in consideration of the foregoing premises, BPI and MERCHANT agree as follows: DEFINITION OF TERMS The following terms used in this Agreement shall have the following meanings: a.