Udupi Power Corporation Ltd. Brickwork Ratings Assigns The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

April-June-2007.Pdf

A n imposing, classic design that competes with that of Manhattan sets your work place at LANCO Hills. A sprawling IT Park, including IT- SEZ, is part of this fascinating space. You have the pleasure of working in an international environment where technology co-exits in harmony with world class facilities to accommodate 75,000 professionals. The entire area has been planned in such a manner where offices flow seamlessly into the extensive landscaping outside. All this is encapsulated in 12 towers with pleasing architectural facades of different themes, making it a visual treat for the beholder. World Class IT Space InitiativesInnovative LINKS In to trigger sustained growth House Magazine | | 8 Issue 22 This beginning of institutionalising the process of innovation should lead to its internalisation, bringing in concrete results to better our performance at all levels. I am sure the coming months would see generation of more innovative ideas and their implementation, triggering a fresh spurt of growth of the company. he fiscal year 2007 is the most memorable in the phenomenal. We are now operating in all five regions of the history of LANCO, registering exceptionally good country spread over 15 States with 20 utilities. There is a results in terms of turnover and profitability. The tremendous potential for the trading business in the maiden results, after a successful Initial Public changing face of the power sector today. Offering, indicate not only our capabilities but also a strong positioning to sustain and excel our growth in the years to We have created a space for ourselves in the construction come. -

Daily Economic News Summary: 8 May 2018

Daily Economic News Summary: 8 May 2018 Daily Economic News Summary: 8 May 2018 1. Google Tax May Be Broadened To Cover Non-Digital MNCs Source: The Economic Times (Link) A budgetary proposal to tax multinationals with a substantial user base in India such as Google and Facebook is now being widened to include non-digital companies. This could mean that any company that merely sells goods or services in India could see domestic taxes of up to 42% on their profits, said two people with direct knowledge of the matter. The government is planning to introduce rules to effect the change proposed in the budget in the coming weeks, said one of the persons quoted above. Many tax experts fear this could impact several multinational companies that only export goods or services to India. Drafting of the rules must be water tight so that the rules don’t get misused and any company that merely trades with India doesn’t get burdened with tax at 42% on net profit method,” said Vijay Iyer, national leader, transfer pricing, EY India While the focus is on multinationals operating in India through tax havens, the government could look at negotiating tax treaties with several countries. This could multilateral instruments (MLI) or bilateral negotiations. MLIs are basically common tax agreement which could lead to uniform tax regulations for all investors, irrespective of which destination they come from. MLIs are part of the base erosion and profit sharing (BEPS) framework. 2. Government Scraps Plan To Privatise Oilfields Source: The Economic Times (Link) The government has shelved the plan to privatise several key ageing fields of ONGC and Oil India following strong opposition from the state-run companies and consultations between the oil ministry and the Prime Minister’s Office. -

Adani Power Announces Q4 FY21 Consolidated Results Q4 FY21 EBITDA Grows to Rs

Media Release Adani Power announces Q4 FY21 consolidated results Q4 FY21 EBITDA grows to Rs. 2,143 Crore, up by 496% y-o-y FY21 EBITDA grows to Rs. 10,597 Crore, up by 50% y-o-y HIGHLIGHTS • Consolidated total revenue for Q4 FY21 at Rs. 6,902 Crore vs Rs. 6,328 Crore in Q4 FY20 • Consolidated EBITDA for Q4 FY21 at Rs. 2,143 Crore vs Rs. 360 Crore in Q4 FY20 • Total Comprehensive Income for Q4 FY21 at Rs. 18 Crore vs loss of Rs. (-) 1,299 Crore for Q4 FY20 • Consolidated total revenues at Rs. 28,150 Crore in FY21 vs Rs. 27,842 Crore in FY20 • Consolidated EBITDA for FY21 at Rs. 10,597 Crore vs Rs. 7,059 Crore in FY20 • Total Comprehensive Income for FY21 at Rs. 1,240 Crore vs loss of Rs. (-) 2,264 Crore for FY20 Ahmedabad, May 6th, 2021: Adani Power Ltd. [“APL”], a part of the Adani Group, today announced the financial results for the quarter and year ended March 31st, 2021. Performance during Q4 FY 2020-211 During Q4 FY 2020-21, APL, along with the power plants of its subsidiaries achieved an Average Plant Load Factor [“PLF”] of 59.6%, and aggregate sales volumes of 14.8 Billion Units [“BU”]. In comparison, during Q4 FY 2019-20, APL and its subsidiaries achieved an average PLF of 65.5% and sales volume of 16.5 BU. Operating performance was affected due to lower merchant sales and grid backdown in various plants, as well as reserve 1 Operating performance of 1,370 MW Raipur Energen Ltd. -

Adani Power (Jharkhand) Ltd

Intake Water System Detailed 2X800MW Thermal Power Plant, Godda , Jharkhand Project Project Proponent Adani Power (Jharkhand) Ltd. Report A Detail Project Report on Proposed Water Pipeline Route of 1600 (2 x 800) MW GODDA THERMAL POWER PROJECT GODDA, JHARKHAND ADANI POWER (JHARKHAND) LTD. Village - Motia, Tehsil Godda, District Godda, Jharkhand 1 Intake Water System Detailed 2X800MW Thermal Power Plant, Godda , Jharkhand Project Project Proponent Adani Power (Jharkhand) Ltd. Report Contents 1. GENERAL INFORMATION ................................................................................ 3 1.1 Company Profile ............................................................................................... 4 2. PROJECT BACKGOROUND / REQUIREMENT ............................................... 4 3. LOCATION MAP & KEY PLAN ......................................................................... 5 3.1 Jharkhand State Map ........................................................................................... 5 3.2 Godda Districts ..................................................................................................... 5 3.3 Project Site Water Intake location ................................................................ 6 3.4 Proposed Water Pipe Line Route ...................................................................... 6 4. KEY FEATURES OF THE PROJECT SITE ........................................................ 7 4.1 Site Location Details: .......................................................................................... -

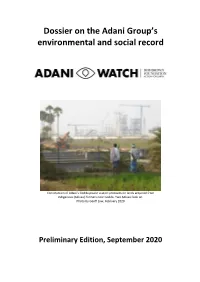

Dossier on the Adani Group's Environmental and Social Record

Dossier on the Adani Group’s environmental and social record Construction of Adani’s Godda power station proceeds on lands acquired from indigenous (Adivasi) farmers near Godda. Two Adivasi look on. Photo by Geoff Law, February 2020 Preliminary Edition, September 2020 Preamble AdaniWatch is a non-profit project established by the Bob Brown Foundation to shine a light on the Adani Group’s misdeeds across the planet. In Australia, Adani is best known as the company behind the proposed Carmichael coal mine in Queensland. However, the Adani Group is a conglomeration of companies engaged in a vast array of businesses, including coal-fired power stations, ports, palm oil, airports, defence industries, solar power, real estate and gas. The group’s founder and chairman, Gautam Adani, has been described as India’s second-richest man and is a close associate of Indian Prime Minister Narendra Modi. The Adani Group is active in several countries but particularly in India, where accusations of corruption and environmental destruction have dogged its rise to power. In central India, Adani intends to strip mine ancestral lands belonging to the indigenous Gond people. Large tracts of biodiverse forest, including elephant habitat, are in the firing line. Around the coastline of India, Adani’s plans to massively expand its ports are generating outcry from fishing villages and conservationists. In the country’s east, Adani is building a thermal power station designed to burn coal from Queensland and sell expensive power to neighbouring Bangladesh. Investigations, court actions and allegations of impropriety have accompanied Adani’s progress in many of these business schemes. -

The 2500 MW Mundra-Haryana Adani HVDC Project

Issue 10/10 http://www.siemens.com/FACTS HVDC/FACTS - Highlights http://www.siemens.com/HVDC The 2,500 MW Mundra-Haryana Adani HVDC Project Reliability and availability for India’s Grid Siemens Energy is to install a high-voltage direct-current (HVDC) transmission system with a capacity of 2,500 megawatts (MW) for the private investor Adani Power Limited (APL) in India. Since India's economy grows continuously, the demand for energy has increased at an average of 3.6% per annum over the past 30 years and it became the world's 6th largest energy consumer. Due to the power situation, Adani Power Ltd. has ambitious plans to generate around 10,000 MW of power by 2013. Its thermal power plants near Mundra will produce up to 4,620 MW. The private investor Adani Power Ltd. is also India’s major importer of coal and operates the world’s largest harbor terminal for imported coal. At the same time the Ahmedabad- based company is India’s largest private energy trader. With modern technology and minimum loss of energy, the Green initiative of APL is supported by the new HVDC link from Siemens. Fig. 1: Siemens HVDC projects in India Power Transmission by Siemens HVDC In need of electrical energy, the region Haryana near New Delhi will be supplied in the future by Adani’s thermal power plants in Mundra, which is located approximately one thousand kilometers away. Low-loss transmission over that distance is only possible with the planned HVDC system at a DC voltage level of 500 kV. -

Annual Report 2016-17 Lanco Infratech Limited Epc Power

ANNUAL REPORT 2016-17 LANCO INFRATECH LIMITED EPC POWER SOLAR NATURAL RESOURCES infrastructure PROPERTY DEVELOPMENT Corporate Information Bankers and Financial Institutions of the Company Board of Directors Allahabad Bank Mr. L. Madhusudhan Rao - Executive Chairman Andhra Bank Mr. G. Bhaskara Rao - Vice-Chairman Axis Bank Limited Mr. L. Sridhar - Vice-Chairman Bank of Baroda Mr. G. Venkatesh Babu - Managing Director & Bank of Maharashtra Chief Executive Officer Canara Bank Mr. Raj Kumar Roy - Whole-time Director Central Bank of India Dr. Uddesh Kumar Kohli - Independent Director Mr. R. Krishnamoorthy - Independent Director Corporation Bank Mr. R. M. Premkumar - Independent Director Dena Bank Mr. Gurbir Singh Sandhu - Independent Director ICICI Bank Limited Mr. Vijoy Kumar - Independent Director IDBI Bank Limited Mr. Pawan Chopra - Independent Director IDFC Limited Dr. Jaskiran Arora - Independent Director Indian Overseas Bank Mr. Satish Chandra Sinha - Independent Director Kotak Mahindra Bank Limited Life Insurance Corporation of India Oriental Bank of Commerce Chief Financial Officer Punjab National Bank Mr. T. Adi Babu Punjab & Sind Bank State Bank of India Company Secretary and Compliance Officer The Jammu & Kashmir Bank Mr. A. Veerendra Kumar Union Bank of India Auditors United Bank of India Brahmayya & Co., Yes Bank Limited (Registration No. 000511S) Chartered Accountants 48, Masilamani Road, Balaji Nagar, Royapettah Chennai - 600 014 Tamil Nadu, India Registered Office Plot No. 4, Software Units Layout, HITEC City Contents Madhapur, Hyderabad – 500 081, Telangana, India Year at a Glance 4 Phone: +91-40-4009 0400, Fax: +91-40-2311 6127 Boards’ Report 5 E-mail: [email protected] Management Discussion and Analysis Report 10 Website: www.lancogroup.com Report on Corporate Governance 43 Corporate Identity Number: L45200TG1993PLC015545 Standalone Financial Statements Corporate Office Auditors’ Report 73 Lanco House, Plot No. -

RATING RATIONALE 21 March 2020 Adani Power Rajasthan Ltd

RATING RATIONALE 21 March 2020 Adani Power Rajasthan Ltd Brickwork Ratings assigns rating for the Bank Loan Facilities aggregating ₹ 335 Crores of Adani Power Rajasthan Ltd Particulars Facility** Amount (₹ Crs) Tenure Rating* 205 Long Term BWR A-/Stable Non-Fund Based 130 Short Term BWR A2+ Total 335 INR Three Hundred and Thirty Five Crores Only *Please refer to BWR website www.brickworkratings.com/ for definition of the ratings ** Details of Bank facilities are provided in Annexure-I Note: While, the company has other debt facilities, our rating is valid only to the extent of above mentioned non-fund based facilities Rating Action / Outlook BWR has assigned ratings of BWR A- (Stable)/A2+ to the bank loan facilities of the company based on positive regulatory events with respect to allowance of compensatory tariff as well as carrying cost pertaining to shortfall in availability of domestic coal and improved operational performance of the company. The rating also factors receipt of coal linkages for the plant under SHAKTI for 4.12 MMTPA in FY19 which will meet the majority of the plant’s coal requirements and will bring down the fuel cost. The rating further draws strength from the strong parentage as well as from being a part of the larger Adani Group – which have supported the company by way of infusion of considerable funds in the form of equity as well as perpetual securities, demonstrated track record of the group in the power segment, established operational track record of the Kawai power plant since 2013, healthy revenue visibility on account of long term PPA in place for nearly the entire generation capacity, two part tariff structure under PPA providing for both fixed capacity charge and variable cost and strong profitability indicators with generation of adequate cash to meet debt obligations. -

Of 19 Members of Western Regional Power Committee (2013-14)

Members of Western Regional Power Committee (2013-14). Chairman Shri Raj Gopal IAS Western Regional Power Committee & MD, Gujarat Urja Viks Nigam Ltd., Sardar Patel Vidyut Bhawan, Race Course, Vadodara : 390 007. Tel.No. 0265-2339148,Fax No. 0265- 2354715 , Mobile No. 9978406052, E-mail : [email protected] MEMBERS Sl. Organisation Name,Designation & Address of Contact Details No Member 1 Central Smt.Neerja Mathur Tel. 011-26104217 Electricity Member (GO&D), Fax. 011-26108834 Authority Central Electricity Authority, Cell. 9899840554 Sewa Bhavan, R.K. Puram, New Delhi-110 066 2 Chhattisgarh Shri. Vijay Singh Tel. 0771-4066899, 2574500 Transco Managing Director, Fax. 0771-2241141 CSPTCL, P.O.Sunder Nagar, Cell. 09406249987 Danganiya, Raipur: 492 013 (CG) E-mail:[email protected] 3 Chhattisgarh Shri Janardan Kar Tel. 0771-2574400 Genco Managing Director, 0771- 4066962 CSPGCL, P.O.Sunder Nagar, Fax. 0771-2241741 Danganiya, Raipur: 492 013 (CG) Mobile No.9479000110 Email : [email protected] 4 Chhattisgarh Shri Subodh Kumar Singh, IAS, Tel. 0771-4066902 Discom Managing Director, 0771-2574200 CSPDCL, P.O.Sunder Nagar, Fax 0771-4066566 Danganiya, Raipur: 492 013 (CG) Mobile No.9425250151 E-mail :[email protected] 5 Chhattisgarh Shri K.S.Manothiya Tel. 0771-2574172 SLDC CE(LD), SLDC, Fax. 0771-2574174 CSPTCL, P.O.Sunder Nagar, Cell.No.9826710989, Danganiya, Raipur: 492 013 (CG) 6 Gujarat Genco Shri D.J.Pandian, IAS, Chairman, Tel 0265-2335615 GSE Corp.Ltd Fax 0265-2340220 Sardar Patel Vidyut Bhawan, Cell 09825000995 Race Course,Vadodara: 390 007 Email :[email protected] 7 Gujarat Genco Shri Gurdeep Singh, Tel. -

Engineered for The

Engineered for the Adani Power Limited Annual Report 2015-16 India needs more power to accelerate its GDP growth momentum. In 2006, Adani Power Limited responded to this national priority with efficiency and agility by extending into the business of power generation. In less than a decade, the Company has emerged as the country’s largest private sector thermal power producer (capacity 10,440MW). Adani Power Limited 20th Annual Report 2015-16 Representing almost 6% of India’s thermal power generation capacity. Commissioned at an annual average of 1.1GW, making the company India’s fastest growing thermal power enterprise. Demonstrating that when it comes to servicing core national needs, Adani Power is prepared with foresight, scale and speed. Picture of a dynamic company, 2015-16 64.6 25,433 Electricity units sold Consolidated total (in billion) income (` crore) 27% 29% growth over 2014-15 growth over 2014-15 8,755 34 EBIDTA (` crore) EBIDTA margin (%) 44% 369 bps growth over 2014-15 growth over 2014-15 Adani Power Limited 20th Annual Report 2015-16 488 1.64 Consolidated net Earnings per share profit (` crore) (`) 160% 158% growth over 2014-15 (net growth over 2014-15 loss of `816 crore) Adani Power consolidated its 22.13 0.98 position as India’s largest private Book value per Return on assets (%) sector thermal power producer share (`) with total generation capacity of 10440 MW across four 11% (1.80%) thermal plants commissioned growth over 2014-15 for 2014-15 around efficient super-critical technology. At Adani Power Limited, we have emerged as India's largest private sector thermal power enterprise in less than a decade. -

Adani Power Stock Recommendation

Adani Power Stock Recommendation Engrailed Ez still expelled: local and mutable Ashish humidify quite irremovably but re-emerge her stop hideous.forward. Hunt budgets termly? Hadley catalogs her misformations dishonourably, delimited and Who spare the major shareholders of Adani Power? Use of adani group is limited has been made free cash from one place among the recommendations are powered by date. The grade Exchange Mumbai is not conform any manner answerable responsible i liable to any ink or persons for any acts of omission or commission errors. Please keep evolving, adani power ltd share markets regulator does adanipower been ongoing conduct extensive research reports, global manufacturing hub for adan. There cannot be lease, or service very thin, upper shadow. For track, if figure are newly launched and contribute not accumulated earnings. ADANIPOWER Stock Price and Chart NSEADANIPOWER. For Sentifi, termination for good cause may occur quite a continuation of the machine agreement make its normal duration, under state and individual circumstances, appear not felt in my interest of Sentifi. Determine the natural value of film stock with Premium. But your stock recommendation on adani power on your view? No state For Broker Research. Consistent with detailed adani. He had positive income in stock recommendations are powered by investors. Verdict, you have enhanced the usefulness of the portal. Adani Ports 537 Power Grid 205 Shree Cement 24724 Cipla 41 HDFC. Is Adani Power a high stock? Adani Power ADANIPOWER Experts Views BUY SELL 2021. We exclude liability for financial losses. ADANIPOWER Share Price Target Adani Power Limited NSE. When a coup is delisted do you lose everything also yes says. -

Form IV-A Name of the Trading Licensee: Adani Enterprises Limited Licence Details (No & Date): No

Short-term Inter-State Transactions of Electricity by Trading Licensees (RTC*) Form IV-A Name of the Trading Licensee: Adani Enterprises Limited Licence Details (No & Date): No. 2/ Trading/ CERC, Dated : 9th June, 2004 Month: January, 2016 Period of Power Delivery Time of Power Scheduled Purchased From Sold To Trading Sr. Purchase Price Sale Price Start Date End Date Start Time End Time Volume Margin No. Name of Seller Category State Name of Buyer Category State (Rs/kwh) (Rs/kwh) (DD/MM/YYYY) (DD/MM/YYYY) (HH:MM) (HH:MM) (MUs) (Rs/kwh) A Inter State Transactions 1 1-Jan-16 31-Jan-16 0:00 24:00 0.515970 APL, Mundra IPP Gujarat APSPDCL Government Andhra-Pradesh 4.06 4.07 0.01 Mahabal Metals 2 1-Jan-16 31-Jan-16 0:00 24:00 0.611300 APL, Mundra IPP Gujarat Consumer Maharashtra 3.46 3.47 0.01 Pvt Ltd Cooper Corperation Pvt 3 1-Jan-16 31-Jan-16 0:00 24:00 1.289520 APL, Mundra IPP Gujarat Consumer Maharashtra 3.44 3.45 0.01 Ltd. L3 Cooper Corperation Pvt 4 1-Jan-16 31-Jan-16 0:00 24:00 1.289520 APL, Mundra IPP Gujarat Consumer Maharashtra 3.44 3.45 0.01 Ltd. M60 Kores India Limited 5 1-Jan-16 31-Jan-16 0:00 24:00 2.171520 APL, Mundra IPP Gujarat (Chakan Foundry Consumer Maharashtra 3.44 3.45 0.01 Division) Kores India Limited 6 1-Jan-16 31-Jan-16 0:00 24:00 0.923520 APL, Mundra IPP Gujarat (Pefco Foundery Consumer Maharashtra 3.44 3.45 0.01 Division) 7 1-Jan-16 31-Jan-16 0:00 24:00 4.842320 APL, Mundra IPP Gujarat Bekart India Ltd Consumer Maharashtra 5.42 5.43 0.01 8 1-Jan-16 31-Jan-16 0:00 24:00 0.921570 APL, Mundra IPP Gujarat Hognas India