Registration Document 2016 • ENGIE

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ORES Assets Scrl

ORES Assets scrl ANNUAL REPORT 2017 1 TABLE OF ORES Assets scrl ANNUAL REPORT 2017 CONTENTS I. Introductory message from the Chairman of the Board of Directors and the Chief Executive Officer p.4 II. ORES Assets consolidated management report p.6 Activity report and non-financial information p.6 True and fair view of the development of business, profits/losses and financial situation of the Group p.36 III. Annual financial statements p.54 Balance sheet p.54 Balance sheet by sector p.56 Profit and loss statement p.60 Profit and loss statement by sector p.61 Allocations and deductions p.69 Appendices p.70 List of contractors p.87 Valuation rules p.92 IV. Profit distribution p.96 V. Auditor’s report p.100 VI. ORES scrl - ORES Assets consolidated Name and form ORES. cooperative company with limited liability salaries report p.110 VII. Specific report on equity investments p.128 Registered office Avenue Jean Monnet 2, 1348 Louvain-la-Neuve, Belgium. VIII. Appendix 1 point 1 – List of shareholders updated on 31 December 2017 p.129 Incorporation Certificate of incorporation published in the appen- dix of the Moniteur belge [Belgian Official Journal] on 10 January 2014 under number 14012014. Memorandum and articles of association and their modifications The memorandum and articles of association were modified for the last time on 22 June 2017 and published in the appendix of the Moniteur belge on 18 July 2017 under number 2017-07-18/0104150. 2 3 networks. However, it also determining a strategy essen- Supported by a suitable training path, the setting up of a tially hinged around energy transition; several of our major "new world of work" within the company should also pro- business programmes and plans are in effect conducted to mote the creativity, agility and efficiency of all ORES’ active succeed in this challenge with the public authorities, other forces. -

REFERENCE DOCUMENT Containing the Annual Financial Report Fiscal Year 2016 PROFILE

REFERENCE DOCUMENT containing the Annual Financial Report Fiscal Year 2016 PROFILE The Lagardère group is a global leader in content publishing, production, broadcasting and distribution, whose powerful brands leverage its virtual and physical networks to attract and enjoy qualifi ed audiences. The Group’s business model relies on creating a lasting and exclusive relationship between the content it offers and its customers. It is structured around four business divisions: • Books and e-Books: Lagardère Publishing • Travel Essentials, Duty Free & Fashion, and Foodservice: Lagardère Travel Retail • Press, Audiovisual (Radio, Television, Audiovisual Production), Digital and Advertising Sales Brokerage: Lagardère Active • Sponsorship, Content, Consulting, Events, Athletes, Stadiums, Shows, Venues and Artists: Lagardère Sports and Entertainment 1945: at the end of World 1986: Hachette regains 26 March 2003: War II, Marcel Chassagny founds control of Europe 1. Arnaud Lagardère is appointed Matra (Mécanique Aviation Managing Partner of TRAction), a company focused 10 February 1988: Lagardère SCA. on the defence industry. Matra is privatised. 2004: the Group acquires 1963: Jean-Luc Lagardère 30 December 1992: a portion of Vivendi Universal becomes Chief Executive Publishing’s French and following the failure of French Offi cer of Matra, which Spanish assets. television channel La Cinq, has diversifi ed into aerospace Hachette is merged into Matra and automobiles. to form Matra-Hachette, 2007: the Group reorganises and Lagardère Groupe, a French around four major institutional 1974: Sylvain Floirat asks partnership limited by shares, brands: Lagardère Publishing, Jean-Luc Lagardère to head is created as the umbrella Lagardère Services (which the Europe 1 radio network. company for the entire became Lagardère Travel Retail ensemble. -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

Présentation Powerpoint

VIVA TECHNOLOGY 2017 SECOND EDITION: PARIS, JUNE 15 TO 17, 2017 Paris, 21 February 2017 Viva Technology, the event for those inventing the world of tomorrow, announces its second edition on 15, 16, and 17 June 2017 in Paris, at the Porte de Versailles. The President of the French Republic will attend the event where the outline of the 2017 edition will be revealed. It is thanks to the development of the French digital ecosystem, helped by the policies implemented by the government that the launch of such an event as Viva Technology is today possible. Organized by Publicis Groupe and Groupe Les Echos, Viva Technology is becoming the world’s leading innovation event, bringing together startups and large companies to give them a unique opportunity to initiate and develop successful collaborations. More ambitious perspective in 2017 with an emphasis on the international dimension and a richer experience The goal is to welcome more than 50,000 visitors including 5,000 startups. The international dimension of Viva Technology is further pronounced, with a significantly higher proportion of international speakers, visitors, and startups, as well as the presence of several country pavilions. Viva Technology seeks to give its visitors a more efficient experience through new contact schemes such as Talent Connect, to facilitate the search for jobs in the digital sector; Mentor Connect, to help startups find Mentors; and the Office Hours platform to encourage meetings between investors, VCs, and startups. Partnerships with industry leaders This new edition of Viva Technology is supported by platinum partners such as BNP Paribas, Google, Orange, and La Poste, which are deeply involved in the organization and success of the event. -

Nuclear Hvac

NUCLEAR HVAC ENGIE Axima, your key partner ENGIE Axima your local partner for engineering, procurement, construction and operation maintenance of your nuclear HVAC projects. Gravelines With a network of GravelinesDunkerque Lille Boulogne-sur-Mer Dunkerque Lille Boulogne-sur-MerPenly St-Omer Dieppe Chooz Cherbourg Penly St-Omer Amiens Paluel Dieppe Chooz FlamanvilleCherbourg Amiens Compiègne Cattenom officies Paluel Rouen Flamanville Compiègne Cattenom Phalsbourg Engineering Procurement Construction Rouen PARIS Saint-Brieuc Caen Reims Metz ENGIE_axima RÉFÉRENCES COULEUR Brest Phalsbourg Haguenau • Design of HVAC & air treatment systems, • Qualification of the equipment (either • Installation of HVAC systems in in France ChartresPARIS Nogent/Seine gradient_MONO_WHITE Saint-Brieuc MontaubanCaen Reims Metz 22/10/2015 Brest Nancy HaguenauSTRASBOURG Landivisiau de Bretagne LeChartres Mans Nogent/Seine Troyes 24, rue Salomon de Rothschild - 92288 Suresnes - FRANCE of process fluids, process vacuum, and by analysis or testing). coordination with other work packages. Montauban Tél. : +33 (0)1 57 32 87 00 / Fax : +33 (0)1 57 32 87 87 Quimper Web : www.carrenoir.com WHITE cooling systems, including the preparation Landivisiau de BretagneRennesLe Mans Orléans Troyes Nancy Epinal STRASBOURGColmar Lorient Chaumont • Long-term partnership with reputable • Testing, commissioning, acceptance, Quimper Angers Fessenheim of the technical specifications for the VannesRennes St-LaurentOrléans Epinal MulhouseColmar suppliers for the procurement of all operation -

INTERNATIONAL ASSOCIATION for ENERGY ECONOMICS BIOGRAPHICAL SKETCHES 2020 ELECTION BALLOT (Listed in Alphabetical Order)

INTERNATIONAL ASSOCIATION FOR ENERGY ECONOMICS BIOGRAPHICAL SKETCHES 2020 ELECTION BALLOT (Listed in alphabetical order) JACQUELINE BOUCHER – for IAEE Vice President for Business & Government Affairs (2021-2022) Current Affiliation: Carbon Neutral Transformation Project Manager ENGIE, Brussels, Belgium; Board Member ENGIE Energy Management (Brussels), Laborelec (Belgium) and ENGIE Energy Management Gmbh, Köln, Germany; Lecturer Ecole Polytechnique UCLouvain, Louvain-la-Neuve, Belgium and ICHEC Business School, Brussels Education: PhD in Mathematics, University of Namur, Belgium; Specialized Ms In Economics Energy, UCLouvain, Louvain-la-Neuve, Belgium Former Affiliations: Chief Power Asset Manager and Member of the Management Committee, ENGIE Global Energy Management, Paris (France) & Brussels (2016-20); SVP Economic and Modeling Studies, GFDSUEZ Strategy, Paris & Brussels (2010-15); Board Member Elia SA, Brussels (2007 – 2009) and Fluxys SA, Brussels (2006 – 2009); SVP Strategy Electrabel, Brussels (2005-09); Chief Risk Officer & Head of Risk and Asset Liability Management, Electrabel, Brussels (2002-05); Head of Microeconomics & Regulation / Quantitative Analysis, Electrabel, Brussels (1994-2002); Start-up co- founder and senior consultant, COHERENCE , Louvain-la-Neuve, Belgium (1989-1994); Researcher, CORE, UCLouvain, Louvain-la-Neuve (1980-1994) IAEE Activities: Board Member (2012-14) JEAN-MICHEL GLACHANT – for IAEE Vice President for Communications (2021 to 2022) Current Affiliation: Professor at Loyola de Palacio Chair in European Energy Policy, Robert Schuman Center, European University Institute, Florence; and Director of Florence School of Regulation (FSR); since 1st Oct. 2008 Education: PhD in Economics, La Sorbonne University, Paris, France. Former Affiliations: Professor and Dean for Economics, Faculté d’Orsay, Université Paris - Sud (2000-2008); Lecturer, associate Professor in economics, La Sorbonne University, Paris (1982-2000) IAEE Activities: Member since 1997. -

Viva Technology 2019 Preview

PRESS RELEASE VIVA TECHNOLOGY 2019 PREVIEW VivaTech is back in 2019 with an even bigger event to celebrate innovation from 16-18 May 2019 at Porte de Versailles in Paris Paris, 12 February 2019 – In three short years Viva Technology has become an unmissable European stop on the global tech calendar, drawing more than 100,000 participants in 2018. Viva Technology stands out for its ability to bring together startups and established companies, providing a one-of-a-kind platform where professionals can do business and where the general public can preview new products and see how tech will impact the future. Viva Technology is back with a 4th edition that’s bigger and better than ever: more space, more startups, more innovations, and more opportunities to grow your business and accelerate your digital transformation. More than ever before, Viva Technology is the place to make sense of the most important trends in technology and innovation and to take advantage of them today. The Main Stage will welcome nearly 5000 attendees in the Dôme de Paris (formerly the Palais de Sports) across from Hall 1. More than 450 speakers from around the world and some of the biggest names in tech will be featured: Young Sohn (Samsung) - SY Lau (Tencent) - Dr Kai Fu Lee (author) - Amnon Shashua (Mobileye) - Gillian Tans (Booking.com) - Garry Kasparov (Avast Ambassador and former world chess champion) - David Kenny (Nielsen) - Jean-Laurent Bonnafé (BNP Paribas) - Philippe Wahl (La Poste) - Bernard Arnault (LVMH) - Stéphane Richard (Orange) - Sébastien Missoffe (Google) - Jean-Paul Agon (L’Oréal) - Fatoumata Ba (Janngo) - Ankiti Bose (Zilingo) - Flora Coleman (Transferwise ) - Daniel Dines (UiPath) - Tanya Harrison (Arizona State University) - Casper Klynge (Danish Government) - Carine Magescas (AngelPad) - Frédéric Mazzella (BlaBlaCar) - Carlos Moedas (European Commission) - Pierre Moscovici (European Commission) - Emily Orton (Darktrace) - Françoise Soulié-Fogelman (Hub France IA) - Roxanne Varza (Station F). -

Oil Analyses Condition Assessment of Transformers and Rotating Machinery

Oil Analyses Condition assessment of transformers and rotating machinery • Detecting and preventing faults • Increasing availability • Optimizing maintenance Transformers Prevent failures A sudden breakdown of a power or industrial transformer usually means unforeseen costs for maintenance, new investments to be made, or unexpected production interruption. As many transformers in companies throughout Europe become older, the probability of such a breakdown increases. What you should know about transformer failures • The average transformer age at failure is 18 years. • The largest financial losses are due to failures of industrial and generator step-up transformers (study by the Hartford Insurance Company). • Insulation failure is the leading cause (responsible for one fourth of all failures). • The cost of insulation failures alone accounts for more than half of all failure costs. • Large power transformers have delivery times between 18 and 24 months. Check your transformer’s health The insulating oil in a transformer can tell you a lot about the actual state of your transformer and its remaining lifetime. Based on this information, you can anticipate potential failures and put in place a precisely targeted maintenance or replacement plan. What your transformer oil can tell you An in-depth analysis of your transformer’s oil gives you a Electrabel power plant good insight into the condition of your transformer and its Herdersbrug, Bruges (B) electrical insulation. ‘Thanks to the early detection of a hotspot, irreversible damage to the transformer — and in the • Internal faults: you can detect the presence of electrical worst case an explosion — was avoided.’ or thermal faults and determine its exact type (partial discharges, hot spots, arcing, et cetera). -

Publishing in the Nineteenth Century

1 Publishing in the Nineteenth Century Originally published as “Editer au XIXe siècle”, Revue d’histoire littéraire de la France, vol. 107, no. 4, 2007, pp. 771–90. Introduction When Roger Chartier and Henri-Jean Martin were preparing the introduction to the first volume of their monumental Histoire de l’Édition francaise (History of French publishing), which they entitled Le livre conquérant. Du Moyen Age au milieu du XVIIe siècle (The Conquering Book. From the Middle Ages to the mid-seventeenth century), they encountered a problem – one might even call it an aporia. They explained their twin debt both to Lucien Febvre, the initiator of research into the history of the book,1 and to Jean-Pierre Vivet, a journalist turned director of Promodis Publishing, who had expressed his desire to “see [the publisher] placed at the center of these four volumes,” which he had entrusted to them.2 This outspoken directive implied that the figure of the publisher long predated the invention of printing, and that he had been performing the role of broker or mediator without interruption from the thirteenth up to the twentieth century, as is the case today. The two editors were very well aware that sustaining such a notion could prove risky, and so they added this further comment, which partly contradicted what had gone before: The story we would like to tell is one in which the role of the publisher was gradually asserted and became more clearly defined; he was bold in the age of the conquering 1 Lucien Febvre and Henri-Jean Martin, L’apparition du livre (Paris: Albin Michel, 1958), translated into English as The Coming of the Book: The Impact of Printing, 1450-1800 (London: Verso, 1976). -

Reference Document 2008

REFERENCE DOCUMENT 2008 REDISCOVERING ENERGY REFERENCE DOCUMENT 2008 Incorporation by reference Pursuant to Article 28 of European Regulation No. 809/2004 of April 29, 2004, this Reference Document incorporates by reference the following information to which the reader is invited to refer: • with regard to the fiscal year ended December 31, 2007 for Gaz de France: management report, consolidated financial statements, prepared in accordance with IFRS accounting principles and the related Statutory Auditors’ reports found on pages 113 to 128 and pages 189 to 296 of the Reference Document, registered on May 15, 2008 with l’Autorité des Marchés Financiers (French Financial Markets Authority, or AMF), under R. 08-056; • with regard to the fiscal year endedD ecember 31, 2007 for SUEZ: management report, consolidated financial statements, prepared in accordance with IFRS accounting principles and the related Statutory Auditors’ reports found on pages 117 to 130 and pages 193 to 312 of the Reference Document, filed onM arch 18, 2008 with l’Autorité des Marchés Financiers (French Financial Markets Authority, or AMF), under D. 08-0122 as well as its update filed on June 13, 2008 under D. 08-0122-A01; • with regard to the fiscal year ended December 31, 2006 for Gaz de France: management report, consolidated financial statements, prepared in accordance with IFRS accounting principles and the related Statutory Auditors’ reports found on pages 105 to 118 and pages 182 to 294 of the Reference Document, registered on April 27, 2007 with l’Autorité des Marchés Financiers (French Financial Markets Authority, or AMF), under R. 07-046; • with regard to the fiscal year ended December 31, 2006 for SUEZ: management report, consolidated financial statements, prepared in accordance with IFRS accounting principles and the related Statutory Auditors’ reports found on pages 117 to 130 and pages 194 to 309 of the Reference Document, filed on April 4, 2007 withl’Autorité des Marchés Financiers (French Financial Markets Authority, or AMF), under D. -

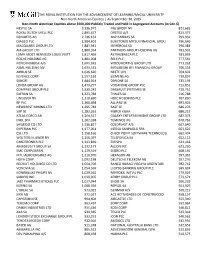

The Royal Institution for the Advancement

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Non-North American Equities │ As September 30, 2019 Non-North American Equities above $500,000 Publicly Traded and Held in Segregated Accounts (in Cdn $) NESTLE SA 3,136,972 ING GROEP NV 822,665 ROYAL DUTCH SHELL PLC 2,895,677 ORSTED A/S 813,377 NOVARTIS AG 2,736,152 BNP PARIBAS SA 799,331 DIAGEO PLC 1,984,601 SUMITOMO MITSUI FINANCIAL GROU 796,646 MACQUARIE GROUP LTD 1,881,942 IBERDROLA SA 796,483 AIA GROUP LTD 1,880,954 PARTNERS GROUP HOLDING AG 781,932 LVMH MOET HENNESSY LOUIS VUITT 1,817,469 ASTRAZENECA PLC 781,059 ROCHE HOLDING AG 1,801,008 RELX PLC 777,561 NOVO NORDISK A/S 1,695,931 WOOLWORTHS GROUP LTD 771,262 ASML HOLDING NV 1,633,531 MITSUBISHI UFJ FINANCIAL GROUP 766,553 AIRBUS SE 1,626,620 NESTE OYJ 764,602 KEYENCE CORP 1,557,193 SIEMENS AG 739,857 SANOFI 1,484,014 DANONE SA 733,193 LONZA GROUP AG 1,479,277 VODAFONE GROUP PLC 723,852 COMPASS GROUP PLC 1,339,242 DASSAULT SYSTEMES SE 720,751 SAFRAN SA 1,323,784 THALES SA 716,788 UNILEVER NV 1,319,690 HSBC HOLDINGS PLC 707,830 BP PLC 1,300,498 ALLIANZ SE 693,905 NEWCREST MINING LTD 1,295,783 BASF SE 686,276 SAP SE 1,283,261 MERCK KGAA 686,219 ATLAS COPCO AB 1,264,517 GALAXY ENTERTAINMENT GROUP LTD 683,373 ENEL SPA 1,262,338 TEMENOS AG 670,763 SHISEIDO CO LTD 1,236,827 COLOPLAST A/S 667,640 EXPERIAN PLC 1,177,061 INTESA SANPAOLO SPA 663,622 CSL LTD 1,158,166 CHECK POINT SOFTWARE TECHNOLOG 662,404 WOLTERS KLUWER NV 1,156,397 TELEFONICA SA 652,113 CARDTRONICS PLC 1,143,839 ENI SPA 641,418 AMADEUS IT GROUP SA -

2019 Vivatech Challenges Are Open for Business

News Release Ready, Steady, Innovate! 2019 VivaTech Challenges are open for business Win a chance to bring your best startup game to the fourth edition of Viva Technology 16-18 May 2019, Porte de Versailles, Paris Paris, 13 December 2018 – For the fourth consecutive year, VivaTech is hosting the Open Innovation Challenges to foster cooperation between startups and established companies while increasing business opportunities in global tech. Startups from around the world are invited to apply on VivaTech’s online platform, challenges.vivatechnology.com, with innovative solutions to the Challenges of leading companies in their sectors. The deadline for applications: 15 February 2019. The list of selected startups will be announced in March. Among VivaTech’s major partners who have confirmed their participation in this year’s Challenges: LVMH (who has already launched its Challenge), Orange, AccorHotels, ManpowerGroup, RATP Groupe, Région Sud, Sanofi, Sodexo, and Vinci Energies. Thousands of startups from around the world are expected to apply this year, but only 1000 or so will be selected. They will win an exhibition space on a “Lab”* hosted by one of VivaTech’s major partners, and they will have the opportunity to establish privileged links with leading companies present during the three-day event in Paris. This initial encounter at VivaTech is a first step that can flourish over time into the development of fruitful partnerships, providing startups with incubation or acceleration and even financial investment. “Our model of Open Innovation, pairing startups with established companies, has contributed to VivaTech’s success since the beginning,” explain Julie Ranty and Maxime Baffert, co-Managing Directors of Viva Technology.